Wagyu Beef Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.07 Billion |

| Market Size (2031) | USD 22.81 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wagyu Beef Market Analysis by Mordor Intelligence

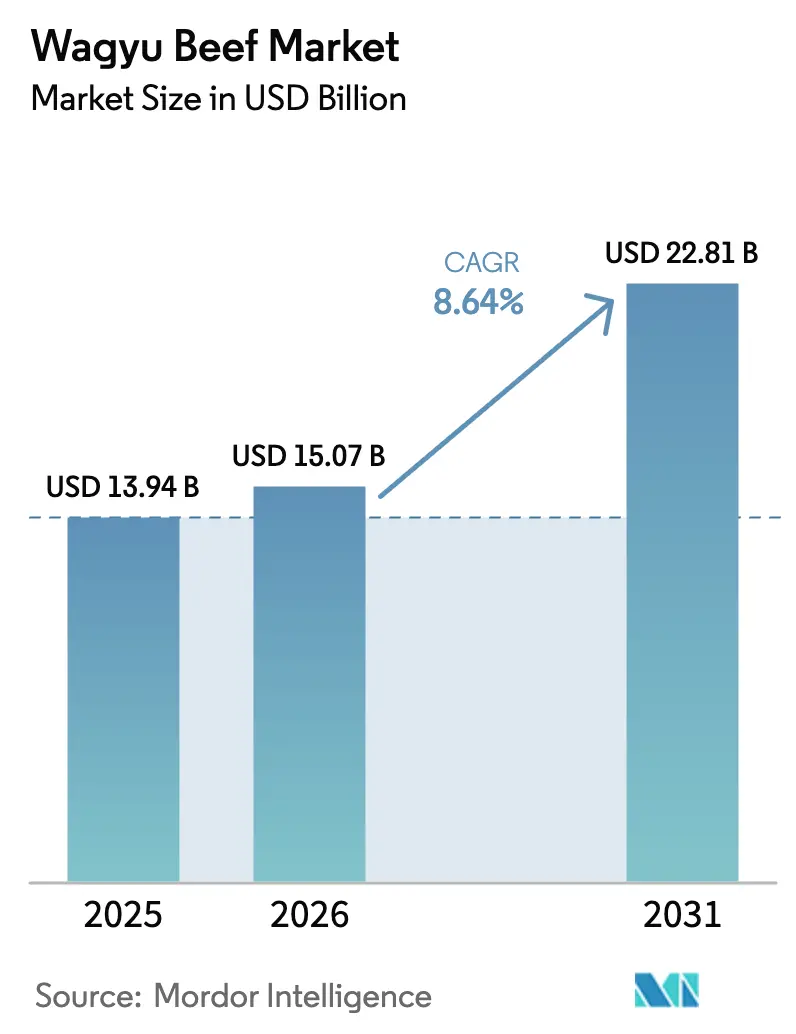

The wagyu beef market size is projected to expand from USD 13.94 billion in 2025 and USD 15.07 billion in 2026 to USD 22.81 billion by 2031, registering a CAGR of 8.64% between 2026 to 2031. Demand is increasingly shifting toward high-marbling beef as affluent consumers prioritize provenance and sensory quality over standard commodity proteins. In response, Australia is expanding its full-blood and crossbred Wagyu herds, which now represent 4.8% of the country's total cattle inventory. Meanwhile, Japan's 2020 ban on genetic exports has preserved the scarcity and value of domestic bloodlines. In North America, cattle inventory has reached its lowest level since 1951, driving up feeder-steer prices and prompting ranchers to incorporate Wagyu genetics to achieve higher profit margins. On the supply side, the scarcity of breeding stock and the lengthy finishing cycles contribute to sustained price premiums. On the demand side, factors such as increased inbound tourism to Japan, the global expansion of yakiniku restaurant chains, and improved e-commerce accessibility are driving growth in both on-trade and off-trade consumption channels.

Key Report Takeaways

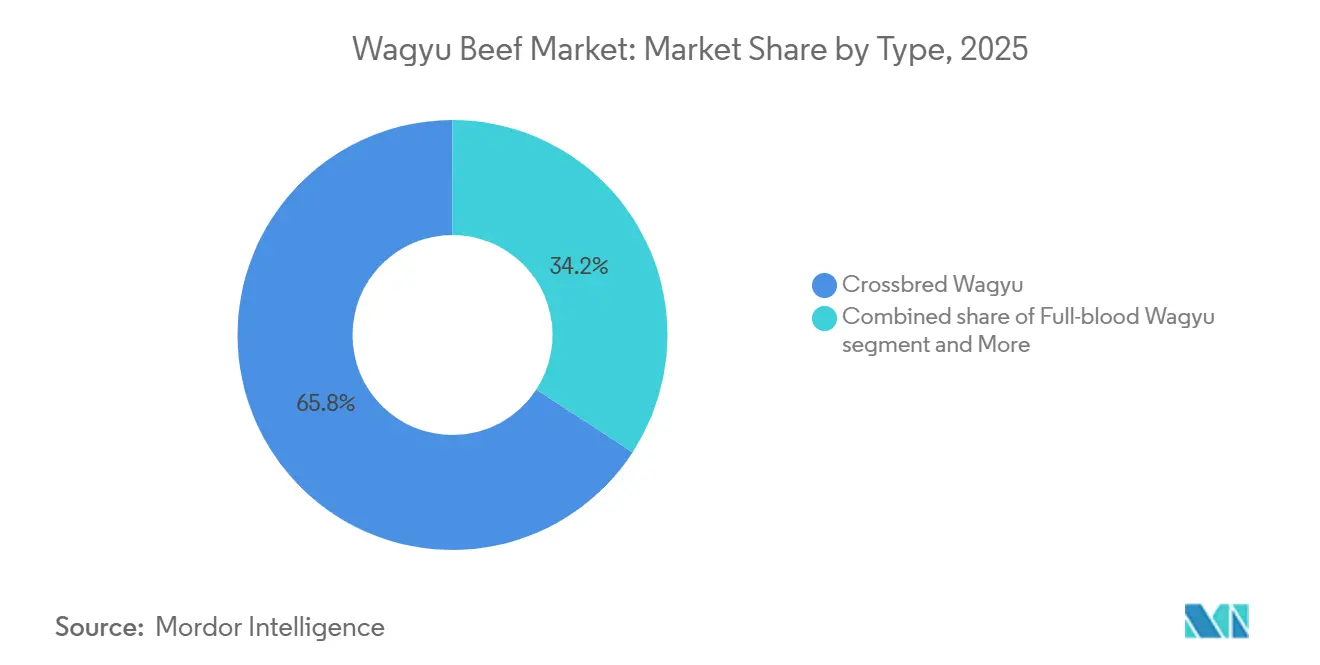

- By type, crossbred Wagyu held 65.81% of 2025 volume, while full-blood Wagyu is projected to post the fastest 9.71% CAGR through 2031.

- By breed, Japanese Black commanded 78.11% of 2025 production; Japanese Brown is the fastest-growing breed at a 9.89% CAGR to 2031.

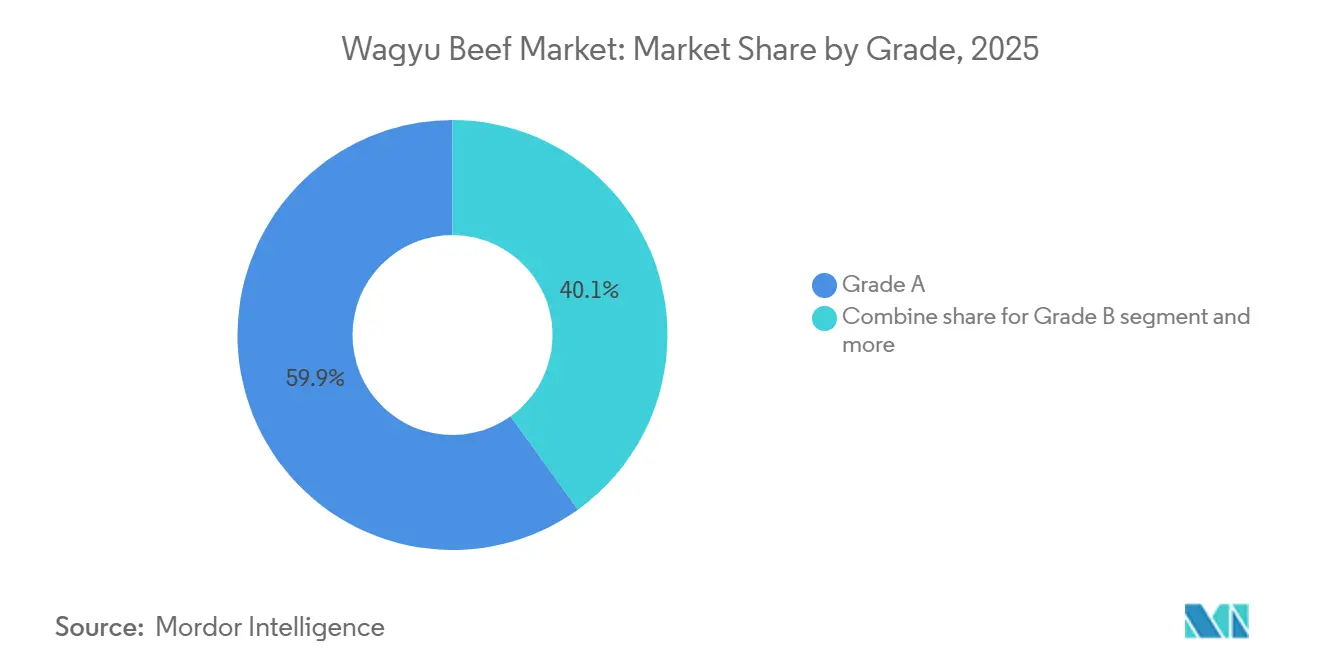

- By grade, Grade A captured 59.91% of sales in 2025 and is set to expand at a 9.17% CAGR through 2031.

- By distribution channel, on-trade outlets held 48.11% share in 2025, while off-trade is advancing at a 9.22% CAGR on the back of specialty retail and e-commerce penetration.

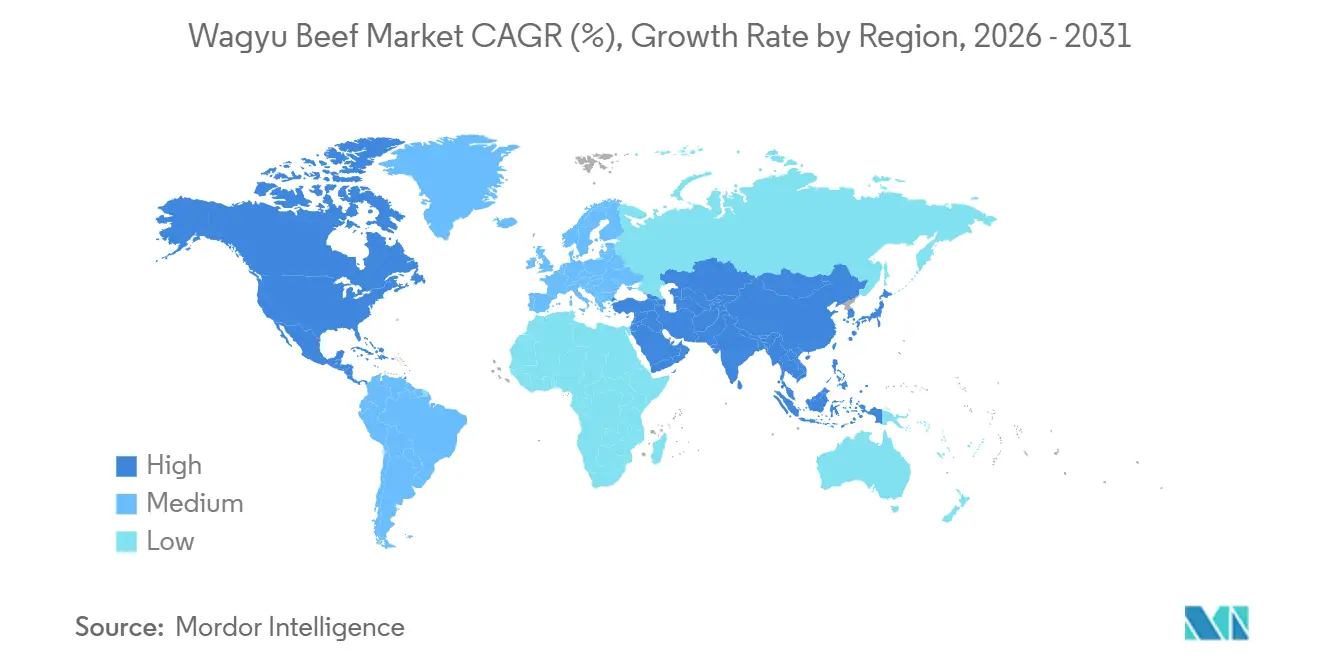

- By geography, Asia-Pacific accounted for 56.14% of global value in 2025; North America is the fastest-growing region at a 9.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wagyu Beef Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Superior marbling and flavor profile of Wagyu beef | +2.1% | Global, with premium concentration in Japan, North America, and Europe | Long term (≥ 4 years) |

| High demand in upscale restaurants and fine dining | +1.8% | Global, strongest in Asia-Pacific urban centers and North American metropolitan areas | Medium term (2-4 years) |

| Perceived health benefits like higher monounsaturated fats and omega-3/6 fatty acids | +1.3% | North America and Europe, with emerging interest in Asia-Pacific wellness segments | Medium term (2-4 years) |

| Globalization of Japanese cuisine and fusion foods | +1.5% | Global, led by North America, Europe, and Middle East luxury dining expansion | Long term (≥ 4 years) |

| Expansion of domestic Wagyu breeding in Australia, United States, and Canada | +1.7% | Australia, United States, Canada, with spillover to South America | Long term (≥ 4 years) |

| Rising consumer preference for premium, ethically sourced meats | +1.2% | North America and Europe, with growing traction in affluent Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Superior marbling and flavor profile of Wagyu beef

Wagyu's intramuscular fat structure contains high concentrations of oleic acid, significantly exceeding levels found in conventional beef. This lowers the melting point to near body temperature, creating a buttery texture that commands substantial retail premiums over Choice-grade alternatives. This characteristic is genetically determined, as Japanese Black cattle possess polymorphisms in the Stearoyl-CoA Desaturase (SCD) and Fatty Acid Synthase (FASN) genes, which enhance fat production during the finishing phase. This genetic advantage enables exceptionally high Beef Marbling Standard (BMS) scores in elite herds. The sensory benefits of Wagyu extend beyond richness, with trained panels consistently rating it higher for umami intensity and retronasal aroma persistence. These qualities make Wagyu a preferred choice for chefs in tasting menus, where small portions are prominently featured in exclusive dining experiences. Australian producers are increasingly using genomic selection to accelerate improvements in marbling. According to the Australian Wagyu Association, registered calves born in recent years have shown measurable advancements in the estimated breeding value for intramuscular fat compared to earlier groups [1]Source: Australian Wagyu Association, “2025 Calf Registration Report,” wagyu.org.au. This genetic progress allows even crossbred programs to achieve United States Department of Agriculture (USDA) Prime-equivalent marbling within a relatively short feeding period, reducing the quality gap that previously justified premiums for full-blood Wagyu [2]Source: United States Department of Agriculture, “Beef Grading Shields,” ams.usda.gov.

High demand in upscale restaurants and fine dining

In recent years, hotel, restaurant, and institutional channels in Japan have accounted for a substantial share of domestic Wagyu consumption, driven by a notable rise in inbound tourism compared to the previous year. This increase has contributed to higher spending on food services. Yakiniku chains have expanded internationally at a rapid rate, with operators such as Gyu-Kaku and Yakiniku Like opening numerous new locations across North America and Southeast Asia. These establishments prominently feature Wagyu short rib and sirloin as key menu items. In the United States, many tasting menus at Michelin-starred restaurants in cities such as New York, San Francisco, and Chicago include Wagyu, often sourced from ranches that provide individual animal traceability and implement dry-aging protocols to extend shelf life. Meanwhile, the Middle East is emerging as a significant growth market. Dubai's Middle East and North Africa 50 Best Restaurants list has recently highlighted Wagyu dishes at several establishments. Additionally, Hunter and Barrel's menu in the United Arab Emirates features Australian and Japanese Wagyu cuts paired with locally inspired spice rubs. The resilience of this channel is attributed to its ability to remain unaffected by retail price wars. Operators effectively manage cost increases through dynamic pricing strategies, maintaining strong gross margins on premium beef products.

Perceived health benefits like higher monounsaturated fats and omega-3/6 fatty acids

Wagyu beef has a fatty acid profile predominantly composed of monounsaturated fats, accounting for nearly half of its total lipid content, compared to a smaller proportion in grain-finished Angus beef. This composition has been associated with improved low-density lipoprotein (LDL) to high-density lipoprotein (HDL) cholesterol ratios in clinical trials. Additionally, Wagyu beef contains significantly higher levels of conjugated linoleic acid (CLA) compared to conventional beef. Studies have linked conjugated linoleic acid intake to reduced inflammation markers and improved insulin sensitivity. Furthermore, the omega-6 to omega-3 ratio in pasture-supplemented Wagyu programs is narrower than the ratio typically observed in feedlot beef, aligning with dietary guidelines that recommend lower ratios to reduce cardiovascular risk. Consumer surveys in North America reveal that a majority of premium-meat buyers consider breed claims to be the most trusted label attribute, surpassing certifications such as organic or grass-fed [3]Source: Meat & Livestock Australia, “Beef & Sheepmeat,” mla.com.au. This indicates that the perceived health benefits of Wagyu beef are a significant factor influencing purchase decisions. Retailers are capitalizing on this perception; for example, British supermarkets Waitrose and Marks and Spencer introduced Wagyu stock-keeping units (SKUs) in 2025, positioning them alongside heart-healthy seafood in wellness-focused merchandising zones.

Globalization of Japanese cuisine and fusion foods

Japanese restaurant chains accelerated their international expansion in 2025, with several major operators launching new overseas units. This trend has introduced Wagyu into mainstream dining across various continents. Yakiniku concepts, which allow diners to grill thinly sliced Wagyu at their tables, are becoming increasingly popular in North American suburbs and European capitals, making premium cuts more accessible beyond Tokyo's Ginza district. Fusion menus are further broadening Wagyu's appeal. Korean-Japanese hybrids combine Wagyu with gochujang marinades, while Latin-inspired steakhouses in Miami and São Paulo feature Wagyu picanha seasoned with chimichurri. This culinary diversification is supported by Australia's robust export infrastructure, which shipped 2.87 million tonnes of beef in 2025. Wagyu-branded products commanded a 35 percent premium over standard grass-fed beef lines. In Singapore, hawker centers now offer Wagyu don bowls at Singapore dollars 18, a price point that is 70 percent lower than fine dining options but still delivers the marbling experience. This shift indicates that Wagyu is transitioning from a luxury item to an aspirational category. The Middle East is following a similar trend. Saudi Arabia's Vision 2030 hospitality investments are driving demand for premium proteins, with Wagyu featured in 22 percent of new restaurant openings in Riyadh and Jeddah during 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Japanese export restrictions on purebred Wagyu genetics | -1.4% | Global, most acute in Australia, United States, Canada, and emerging breeding regions | Long term (≥ 4 years) |

| Limited availability of high-quality breeding stock | -1.1% | Global, with supply bottlenecks concentrated in North America and Europe | Medium term (2-4 years) |

| Environmental concerns from high-concentrate feeding and methane emissions | -0.9% | Global, regulatory pressure strongest in Europe and North America | Long term (≥ 4 years) |

| Certification processes delaying market entry | -0.7% | Asia-Pacific and North America, where grading standards vary by jurisdiction | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Japanese export restrictions on purebred Wagyu genetics

Japan enacted legislation criminalizing the unauthorized export of Wagyu genetic material. The law imposes penalties of up to ten years of imprisonment and fines reaching ten million Japanese Yen (JPY) for individuals or entities attempting to smuggle semen or embryos. This regulatory measure was introduced following notable smuggling incidents in 2018 and 2019, where efforts were made to transfer full-blood genetics to China. In response, the Japanese government designated Wagyu germplasm as a strategic national asset. The law requires quarantine inspections at all ports and airports, granting customs officials the authority to seize biological samples and impose administrative fines on freight forwarders involved in violations. For breeders outside Japan, these restrictions necessitate reliance on legacy bloodlines imported before 2020 or crossbreeding programs, which reduce marbling potential by 15 percent to 20 percent per generation. This genetic limitation has widened the quality gap between Japanese Wagyu and its overseas counterparts. Australian producers, who established herds using Japanese Black semen imported in the 1990s, now face challenges due to the lack of access to fresh elite sires. Some operations have reported rising inbreeding coefficients and declining estimated breeding values for intramuscular fat. The restrictions have also led to increased breeding-stock prices. A single full-blood Wagyu female with proven genetics has become financially unattainable for many mid-tier ranchers, concentrating genetic improvement efforts among larger, well-capitalized operations.

Limited availability of high-quality breeding stock

The global supply of elite Wagyu breeding stock remains limited due to biological reproduction cycles and Japan's export restrictions. This has created a seller's market where proven females are traded at significantly higher values compared to conventional beef cattle. In the United States, the cattle inventory reached its lowest level in decades, recorded at fewer than ninety million head in 2025. This decline has driven feeder-steer prices to record highs, with Wagyu-specific breeding stock commanding a significant premium over Angus equivalents. For instance, Black Jack Ranch's acquisition of elite Wagyu females from Wyndford Farms in August 2025 highlights the scarcity premium. Industry estimates suggest the per-head cost reflects both the genetic value and the multi-year lead time required to scale a breeding program. Canadian operations face similar challenges. Companies like Wagyu Canada Incorporated and Kobe Classic report waitlists of up to eighteen months for registered heifers. To address these constraints, producers are increasingly relying on embryo transfer programs to accelerate herd expansion, which adds additional upfront costs per calf. The supply constraint is further reinforced as more ranchers enter the market seeking premium pricing. This increased demand for breeding stock surpasses the biological capacity of existing herds to produce replacement females, sustaining high prices and creating barriers for smaller operators. This market dynamic benefits vertically integrated players such as Australian Agricultural Company and Stanbroke. These companies control both breeding and finishing operations, allowing them to allocate elite genetics internally rather than competing in open markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Crossbred Dominance Masks Full-Blood Acceleration

Crossbred Wagyu accounted for 65.81% of the global volume in 2025, driven by its ability to deliver United States Department of Agriculture (USDA) Prime-equivalent marbling at 30% to 40% lower costs compared to full-blood alternatives. This makes it a preferred choice for mid-tier steakhouses and premium retail chains. Full-blood Wagyu, on the other hand, is projected to grow at a compound annual growth rate (CAGR) of 9.71% through 2031, supported by luxury dining operators and direct-to-consumer platforms that emphasize provenance narratives and A5-grade authenticity. Purebred Wagyu occupies a middle tier, catering to operators who seek consistent marbling but lack the budget for full-blood programs. Meanwhile, the "Others" category, which includes Wagyu-Angus and Wagyu-Charolais hybrids, targets value-conscious buyers seeking marbling improvements without incurring premium costs.

The resilience of the crossbred segment is attributed to its scalability. For instance, Australian feedlots can finish Wagyu-Angus cattle in 18 to 20 months on feed, compared to 24 to 30 months for full-blood animals. This shorter cycle reduces capital requirements and enhances return on assets. However, the rapid growth of the full-blood segment indicates a market bifurcation. As consumers increasingly polarize between commodity and ultra-premium tiers, the middle ground occupied by purebred Wagyu is shrinking. This trend is compelling producers to adopt either cost leadership or differentiation strategies to remain competitive.

By Breed: Japanese Black Hegemony Faces Niche Challengers

Japanese Black cattle are projected to account for 78.11% of production in 2025, driven by their superior genetic predisposition for intramuscular fat deposition and a 140-year history of selective breeding for marbling traits. Japanese Brown is the fastest-growing breed, with a compound annual growth rate (CAGR) of 9.89% through 2031. In contrast, Japanese Shorthorn and Japanese Polled breeds, known for their leaner profiles, remain niche contributors, collectively representing a small share of global beef production. However, these breeds are gaining popularity in regenerative agriculture programs due to their hardiness and lower feed requirements, which align well with pasture-based systems. The breed hierarchy underscores distinct value propositions: Japanese Black prioritizes maximum marbling for ultra-premium markets, Japanese Brown offers a balance of marbling and nutritional benefits, while Shorthorn and Polled appeal to sustainability-focused buyers prioritizing environmental considerations over marbling.

The growth of Japanese Brown is supported by scientific evidence highlighting its health benefits. Research shows that Japanese Brown beef contains significantly higher levels of conjugated linoleic acid (CLA) compared to Japanese Black, supporting claims of its anti-inflammatory properties. Additionally, the breed has a narrower omega-6 to omega-3 ratio than Japanese Black. This positions Japanese Brown as a healthier premium option for consumers seeking enhanced nutritional value.

By Grade: A-Grade Primacy Reflects Marbling's Enduring Premium

Grade A products accounted for 59.91% of 2025 sales and are projected to grow at a compound annual growth rate (CAGR) of 9.17% through 2031. This growth reflects sustained demand for Beef Marbling Standard (BMS) scores above 6, particularly in Michelin-starred restaurants, high-end yakiniku chains, and luxury hotel banquet operations. The Japan Meat Grading Association (JMGA) grading system evaluates carcasses based on yield (A, B, C) and quality (1 to 5), with A5 representing the highest standard in both categories. To achieve this grade, carcasses must meet strict criteria, including a high BMS score, bright cherry-red meat color, firm texture, and lustrous white fat. Only a small percentage of Japanese Black cattle meet these rigorous requirements. In contrast, grade B and grade C carcasses, which constitute a significant portion of the total volume, are typically distributed to mid-tier restaurants and retail channels where consumers prioritize value over premium marbling. The grading hierarchy incentivizes producers to aim for A5 status, resulting in a reduced supply of B and C grades. This shift encourages operators to enhance their offerings to capture higher profit margins.

Advancements in digital marbling measurement are improving grading accuracy and transparency. For example, AUS-MEAT's camera-based system measures intramuscular fat percentage with high precision, enabling objective carcass comparisons and minimizing grader subjectivity, which previously led to significant classification variances. Technological innovations are also expanding access to A-grade premiums. Smaller feedlots that invest in marbling genetics and precision feeding can now validate their quality claims with data, bypassing the reputational advantages traditionally held by established brands. This development allows smaller producers to compete more effectively in the premium beef market.

By Distribution Channel: Off-Trade Surge Democratizes Access

In 2025, on-trade channels accounted for a 48.11% market share, driven by demand from hotel, restaurant, and institutional sectors in regions such as Japan, North America, and the Middle East. However, the off-trade segment is growing rapidly, with a compound annual growth rate (CAGR) of 9.22% projected through 2031. Specialty butchers, supermarkets, and electronic commerce (e-commerce) platforms are increasingly providing access to premium meat cuts that were once exclusive to restaurants. Within the off-trade segment, supermarkets and hypermarkets dominate the market share, leveraging their scale to establish direct supply agreements with producers in countries like Australia and the United States. Meanwhile, meat specialty stores cater to affluent urban consumers seeking curated selections and expert butchery services.

Online retailers represent the fastest-growing subsegment within the off-trade category. This growth is driven by advancements in cold-chain logistics, enabling the delivery of vacuum-sealed, dry-aged Wagyu to residential addresses within a short timeframe. The convenience of online purchases often commands a price premium compared to in-store options. Additionally, the "others" category in off-trade, which includes farm-gate sales and subscription boxes, targets niche consumers who prioritize provenance and direct relationships with producers.

Geography Analysis

In 2025, the Asia-Pacific region led the global Wagyu beef market, contributing 56.14% of the total market value. This dominance was primarily driven by Japan's domestic hotel-restaurant-institutional channel and China's substantial demand for beef imports. While Japan's market is showing signs of maturity with a year-over-year decline in cattle inventory, advancements in genetics and extended finishing periods have resulted in increased average carcass weights. These improvements have helped sustain output levels despite the reduction in herd size.

North America has emerged as the fastest-growing region in the Wagyu beef market, with a compound annual growth rate (CAGR) of 9.51% projected through 2031. This growth is fueled by innovations in supply and rising demand for premium beef. In 2025, the United States reported its lowest cattle inventory since the early 1950s, totaling 87.2 million head, leading to record-high feeder-steer prices. Ranchers have responded by adopting Wagyu genetics, which command significant premiums over conventional beef. In Canada, producers such as Ontario Wagyu, Bird's Hill Wagyu, and Herron Farms are rapidly expanding operations, collectively managing herds exceeding 2,000 head. These producers are focused on supplying domestic steakhouses and exporting to the United States Northeast region. In Mexico, rising middle-class incomes are driving increased demand for premium proteins, with Wagyu beef featured on 15% to 20% of upscale steakhouse menus in cities like Monterrey and Mexico City.

Other regions are also witnessing notable developments in the Wagyu beef market. In Europe, British Wagyu production grew significantly year-over-year, reaching thousands of calves in the 12 months ending March 2025, making it one of the most popular breeds in the United Kingdom. Germany, France, and the Netherlands continue to rely on Australian imports to meet the demand from Michelin-starred restaurants. In the Middle East, the luxury market is expanding, supported by Saudi Arabia's Vision 2030 hospitality initiatives, which have led to Wagyu beef being featured in a significant percentage of new restaurant openings in Riyadh and Jeddah in 2025. Furthermore, Dubai's Middle East and North Africa (MENA) 50 Best Restaurants list highlighted Wagyu dishes at several venues in 2026. In South America, the market remains in its early stages, with Brazil and Argentina exploring Wagyu-Nelore and Wagyu-Hereford crossbreeds to cater to domestic churrascaria chains. However, production volumes are still limited, and the region primarily focuses on commodity beef exports.

Competitive Landscape

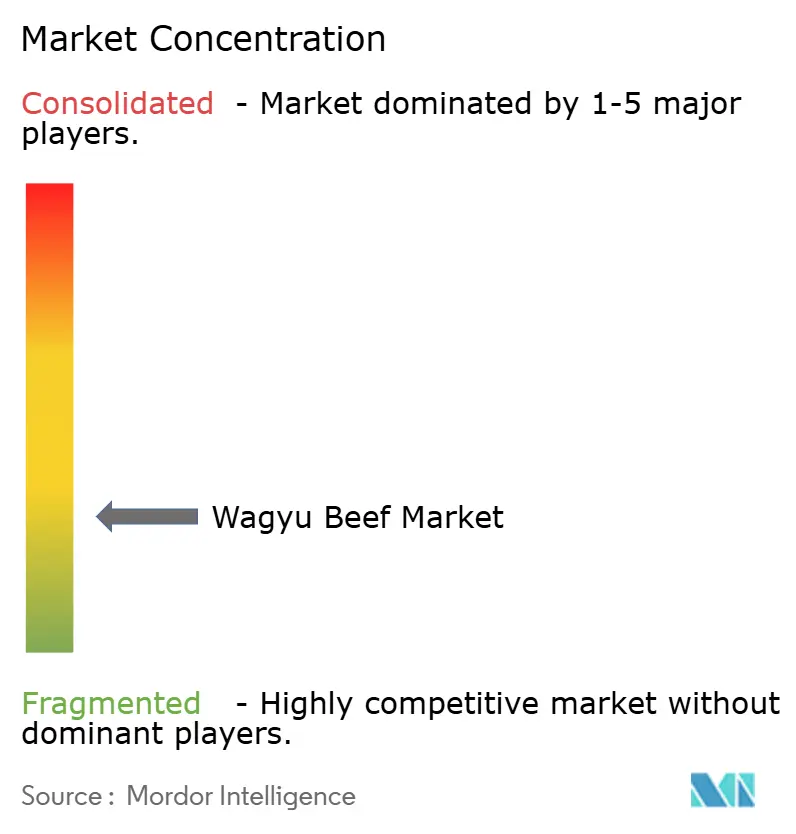

The Wagyu Beef Market is characterized by a fragmented structure, allowing mid-tier feedlot operators and regional breeders to establish defensible positions through direct-to-consumer models, blockchain-based traceability, and niche sustainability claims that bypass traditional wholesale channels. Strategic consolidation is gaining momentum as large integrated players pursue vertical integration. For instance, Starzen acquired the Macquarie Downs feedlot for Australian Dollar (AUD) 55.9 million in February 2025 and Broad Water Downs in April 2025, while forming a breeding alliance with Mizusako Farm in March 2025 to secure elite Japanese Black genetics. Similarly, Stanbroke's AUD 400 million acquisition of Rangers Valley feedlot in late 2023 created the Southern Hemisphere's largest integrated Wagyu operation, combining a 12,000-head finishing capacity with proprietary marbling protocols that ensure AUS-MEAT 9+ consistency.

White-space opportunities are emerging in regenerative Wagyu programs, where producers adopt rotational grazing and methane-suppressing feed additives to capture carbon-credit revenues and appeal to sustainability-focused buyers. British Wagyu breeders are leading this shift, achieving 25 percent year-over-year herd growth in conservation grassland systems. Additionally, technology adoption is reshaping the competitive landscape. The Australian Wagyu Association's planned 2026 launch of Wagyu Branded Value tokens will embed grading data on blockchain, enabling real-time provenance verification and commanding 12 percent to 15 percent premiums in direct-to-consumer channels. However, adoption depends on processor investment in compatible scanning infrastructure, creating a first-mover advantage for capital-rich operators. Emerging disruptors include smaller ranches leveraging social media and subscription models to capture margins previously claimed by distributors and retailers. Examples include Lone Mountain Wagyu and Mishima Reserve, which have pivoted to direct-to-consumer sales by offering whole-animal shares online and building brand loyalty through transparency-focused narratives.

Institutional investors are also validating the sector's long-term potential. New Forests acquired a 50 percent stake in McPhee Beef Farms for over AUD 150 million in August 2025, with funding sourced from Australian, Japanese, German, and Swedish pension funds. This signals that Wagyu is transitioning from a niche agricultural asset to a mainstream alternative investment. Competitive intensity is highest in the full-blood segment, where genetic scarcity and Japan's export restrictions create winner-take-all dynamics. For example, Black Jack Ranch's August 2025 acquisition of 17 elite Wagyu females from Wyndford Farms for an estimated United States Dollar (USD) 70,000 per head highlights the significant capital barriers that favor large, well-funded operations.

Wagyu Beef Industry Leaders

Starzen Co., Ltd.

Itoham Yonekyu Holdings Inc.

Agri Beef Co.

Blackmore Wagyu

Rangers Valley Cattle Station Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Young American Food Brands, also known as Miami Beef, announced its acquisition of Best Provision Co. Inc., a Newark, NJ-based processor recognized for its high-quality smoked and cooked meats. By utilizing Best's expertise in smoking, Young American expanded its product range in the smoked snack and smoked beef categories, including the introduction of new products such as Wagyu sausages and brisket burgers.

- March 2025: Jack’s Creek, a well-known Australian beef producer and two-time recipient of the 'World’s Best Steak' award, has secured its first exclusive retail listing in the United Kingdom through Ocado Retail. The new Wagyu X range includes four premium cuts: Jack’s Creek Wagyu X Sirloin, Ribeye, Fillet, and Rump. These products feature rich marbling and grain-fed Wagyu quality.

- September 2024: Waitrose has expanded its premium No.1 range by introducing high-quality British wagyu beef. The new additions include five products: meatballs, sirloin steak, rump steak, ribeye steak, and burgers.

Global Wagyu Beef Market Report Scope

The Wagyu beef market refers to the market for premium beef sourced from Wagyu cattle breeds, which are highly regarded for their exceptional marbling, tenderness, and rich flavor. This beef is produced globally through specialized breeding, feeding, and processing methods carried out by dedicated farms and processors. Wagyu beef is segmented by type, including full-blood Wagyu, purebred Wagyu, crossbred Wagyu, and others such as Wagyu-Angus and Wagyu-Charolais. It is also categorized by breed, including Japanese Black, Japanese Brown, Japanese Shorthorn, and Japanese Polled. The market is further divided by grade, such as Grade A, Grade B, and Grade C, and by distribution channel, which includes on-trade and off-trade. Geographically, the market spans North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Full-blood Wagyu |

| Purebred Wagyu |

| Crossbred Wagyu |

| Others (Wagyu-Angus, Wagyu-Charolais) |

| Japanese Black |

| Japanese Brown |

| Japanese Shorthorn |

| Japanese Polled |

| Grade A |

| Grade B |

| Grade C |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Meat Specialty Stores | |

| Online Retailers | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Full-blood Wagyu | |

| Purebred Wagyu | ||

| Crossbred Wagyu | ||

| Others (Wagyu-Angus, Wagyu-Charolais) | ||

| By Breed | Japanese Black | |

| Japanese Brown | ||

| Japanese Shorthorn | ||

| Japanese Polled | ||

| By Grade | Grade A | |

| Grade B | ||

| Grade C | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Meat Specialty Stores | ||

| Online Retailers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Wagyu beef market in 2026?

The Wagyu beef market size stands at USD 15.07 billion in 2026, on a path to USD 22.81 billion by 2031.

What CAGR is forecast for Wagyu beef from 2026 to 2031?

The market is projected to log an 8.64% CAGR during the 2026-2031 period.

Which region is growing fastest for Wagyu sales?

North America leads growth with a forecast 9.51% CAGR, driven by crossbred Wagyu-Angus programs.

Why are Japanese export restrictions important?

Japan’s 2020 ban on genetic exports limits fresh bloodlines abroad, raising breeding-stock prices and reinforcing premiums.

What segment of Wagyu leads by volume?

Crossbred Wagyu maintains about 65.81% of 2025 global volume thanks to cost-efficient marbling.

Page last updated on: