United States Sterilization Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

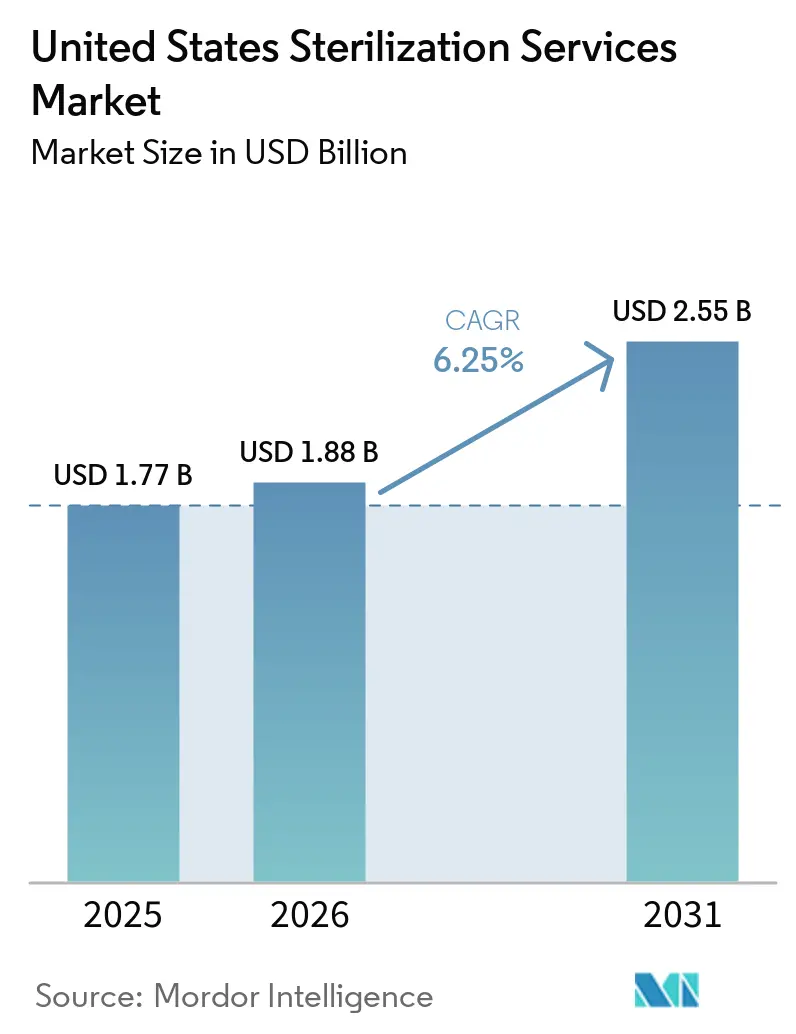

| Base Year Market Size (2025) | USD 1.77 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

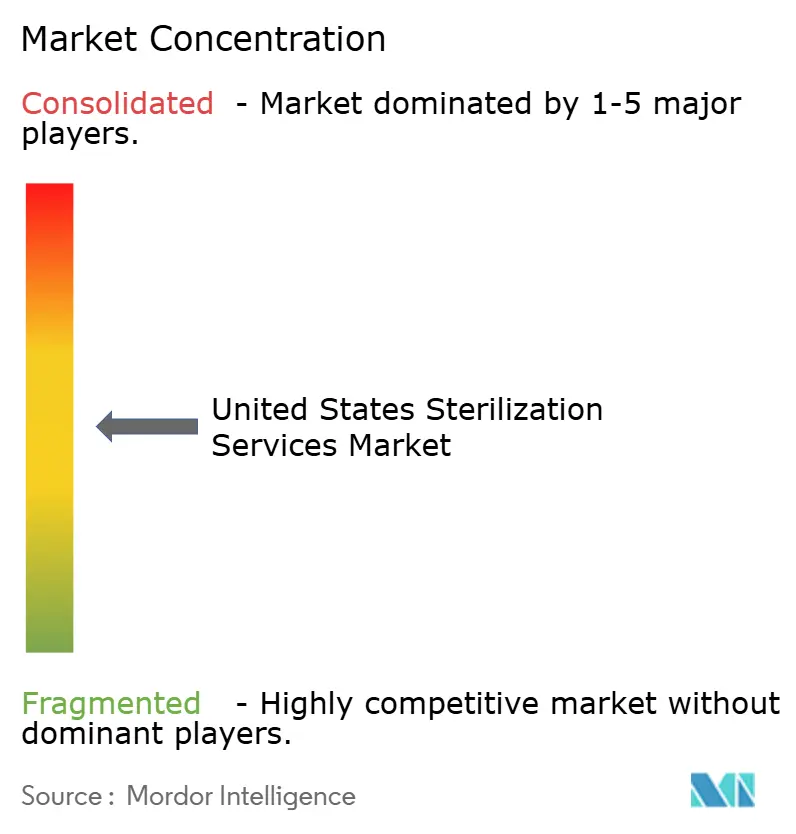

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Sterilization Services Market Analysis by Mordor Intelligence

The United States Sterilization Services Market size is projected to expand from USD 1.77 billion in 2025 and USD 1.88 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 6.25% between 2026 to 2031.

The market is being reshaped by the February 2026 start of the FDA Quality Management System Regulation, which extends ISO 13485:2016 quality obligations across outsourced sterilization relationships and raises the documentation standard for contract providers. The United States sterilization services market is also moving away from heavy reliance on ethylene oxide because air emissions rules, compliance costs, and legal exposure have made single-technology strategies less attractive than diversified portfolios. Demand remains firm because medical device production, sterile pharmaceutical activity, and procedure-related consumption continue to support high sterilization throughput, which is why large providers are still adding capacity and reinvesting in domestic sites. This combination favors operators with multi-modal networks, auditable quality systems, and the capital to fund both compliance upgrades and new irradiation assets. As a result, the United States sterilization services market is growing not only because volumes are rising, but also because pricing, capacity planning, and contract awards now depend more heavily on technology flexibility and proof of compliance.

Key Report Takeaways

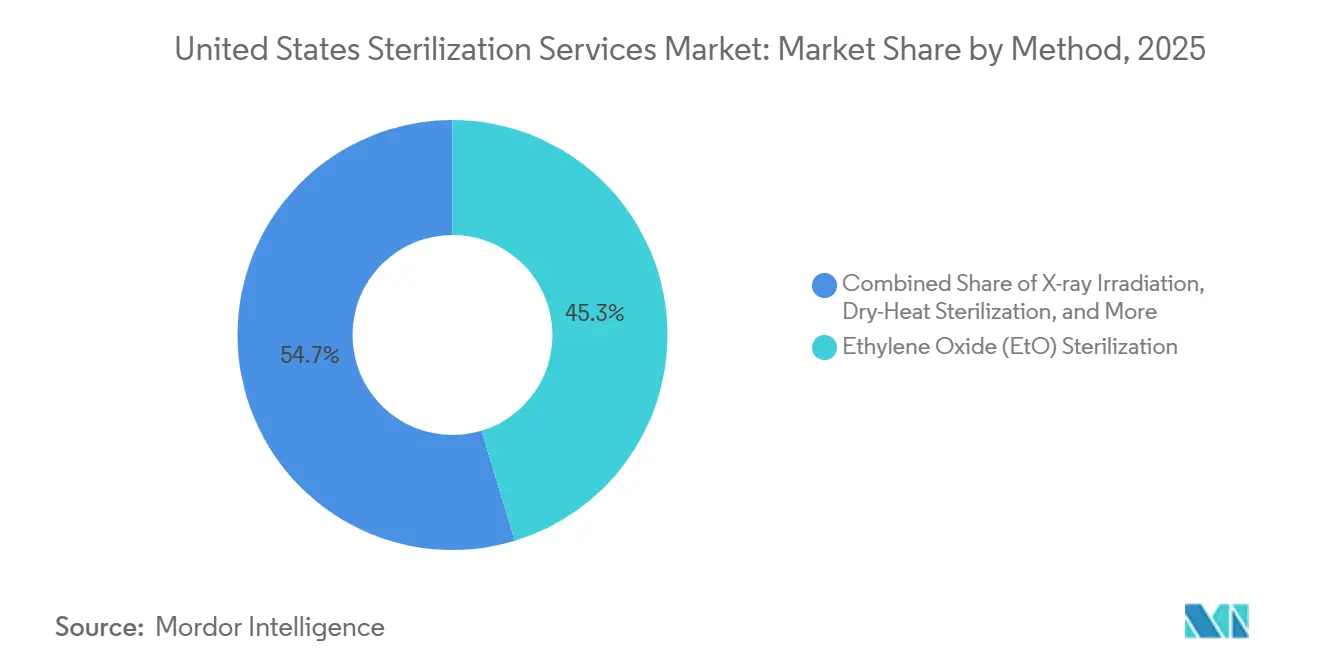

- By method, EtO sterilization held 45.31% of revenue in 2025, while X-ray irradiation is projected to expand at a 9.38% CAGR through 2031.

- By mode of delivery, off-site service-center sterilization held 66.24% of revenue in 2025, while on-site or in-house-as-a-service is forecast to grow at an 8.52% CAGR through 2031.

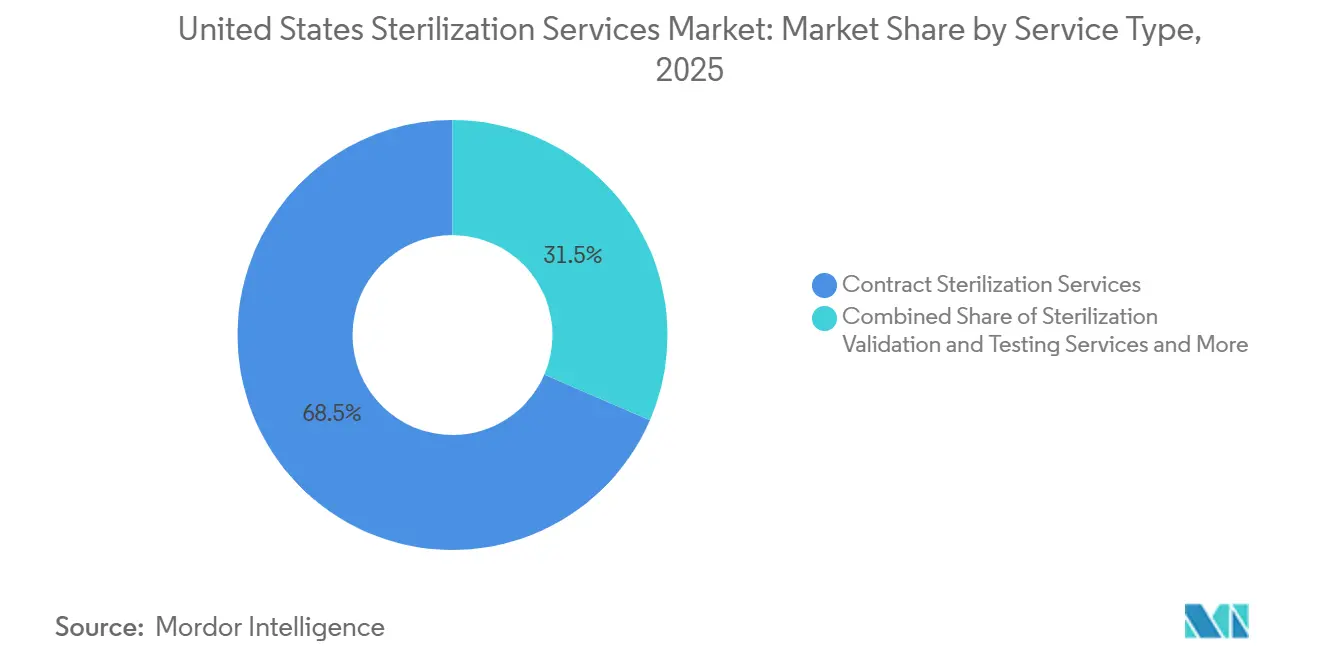

- By service type, contract sterilization services held 68.52% of revenue in 2025, while sterilization validation and testing services are expected to grow at an 8.25% CAGR through 2031.

- By end user, medical device manufacturers held 42.84% of revenue in 2025, while pharmaceutical and biopharmaceutical manufacturers are projected to expand at a 9.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Sterilization Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HAI Burden And Procedure Throughput | +1.0% | National, with elevated intensity in high-volume surgical states including Texas, Florida, California, and New York | Short term (≤ 2 years) |

| Outsourcing By Device And Pharma Manufacturers | +1.1% | National, concentrated in Midwest and Southeast device and pharma manufacturing clusters | Medium term (2-4 years) |

| FDA QMSR And ISO 13485 Alignment | +0.5% | National, with early compliance gains in states with high FDA inspection density | Short term (≤ 2 years) |

| Single-Use And Minimally Invasive Device Expansion | +1.2% | National, with demand spikes in ASC corridors across Sunbelt and urban markets | Medium term (2-4 years) |

| AI-Enabled Chain-Of-Custody And Cycle-Tracking | +0.3% | National, early adoption concentrated in large integrated health systems | Long term (≥ 4 years) |

| X-Ray Capacity Build-Outs Reducing EtO And Cobalt-60 Bottlenecks | +0.8% | National, with new facilities anchored in the Southeast and mid-Atlantic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising HAI Burden and Procedure Throughput

Healthcare-associated infections continue to keep sterilization performance under close clinical scrutiny, and the CDC’s 2023 national and state report showed that device-related and procedure-related infection control remains a material issue for acute care settings[1]Centers for Disease Control and Prevention, “2023 National and State HAI Progress Report for Acute Care Hospitals,” CDC STACKS, cdc.gov. In the United States sterilization services market, that pressure matters because more procedures are moving through ambulatory settings that want hospital-grade sterility assurance without the full footprint of advanced in-house infrastructure. Higher-acuity case migration into ambulatory surgery centers increases the need for validated processing, packaging integrity, and documented release controls. That shift supports more off-site contract demand because many centers have limited space for multi-modal equipment and limited tolerance for process failure. The United States sterilization services market therefore benefits when procedure growth and infection prevention standards rise together, since both push customers toward more formal sterilization partnerships.

Outsourcing by Device and Pharma Manufacturers

The market is seeing stronger outsourcing momentum because QMSR raises the cost of running compliant internal sterilization operations and makes vendor oversight more visible during inspections. RAPS reported that outsourcing and purchasing controls ranked as the second-most-cited QMSR observation in more than 100 completed inspections as of May 2026, which shows how closely the FDA is reviewing supplier management. ISO 13485:2016 Clause 4.1.5 now carries more weight in practice because outsourced processes must be controlled in proportion to risk, and sterilization is one of the clearest examples of that rule. Large contract providers gain an advantage under this framework because they can offer documented quality systems, validation records, and audit-ready traceability as part of the service. That is why the United States sterilization services market is shifting toward bigger, multi-modal platforms for long-term outsourced agreements.

Single-Use and Minimally Invasive Device Expansion

The United States sterilization services market is also supported by the expansion of single-use and minimally invasive products, since every disposable device needs a validated terminal sterilization pathway before patient use. Johnson & Johnson MedTech reported 4.6% Q1 2026 revenue growth tied to cardiovascular and surgical innovation, which points to continued commercial activity in device categories that depend on sterile accessories and packaged components. This matters because more advanced instruments and combination products bring tighter material limits, especially when electronics, coatings, or drug-contact surfaces are involved. As a result, method choice is increasingly shaped by material compatibility rather than only by unit processing cost. The United States sterilization services market gains from this shift because customers are more willing to qualify VHP, NO2, E-Beam, and X-ray options when a single EtO or gamma pathway no longer fits the whole product family.

X-Ray Capacity Build-Outs Reducing EtO and Cobalt-60 Bottlenecks

The market is getting a clear lift from new X-ray build-outs because they ease dependence on EtO and give customers another route when cobalt-60 planning becomes tight. Sterigenics opened a new X-ray sterilization facility in Haw River, North Carolina, in April 2026 to provide a broader mix of irradiation options in the Southeast manufacturing corridor. STERIS had already completed an X-ray expansion in Libertyville, Illinois, in June 2024, which showed that incumbent operators were moving early to add accelerator-based capacity. Steri-Tek also contracted for a Be Wide X-ray system at its Texas facility, with a stated fivefold capacity increase targeted by the end of 2027. This is why X-ray is the fastest-growing method in the United States sterilization services market, since it offers commercial-scale throughput and supply chain redundancy without relying on gas-based processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EtO Emissions And Compliance Volatility | -1.5% | National, with concentrated impact in Illinois, Georgia, and New Mexico due to state-level enforcement | Short term (≤ 2 years) |

| High Capex For Compliant Multi-Modal Capacity | -0.8% | National, with disproportionate burden on small and mid-size operators | Medium term (2-4 years) |

| Sterility-Assurance Talent Shortage | -0.5% | National, acute in Midwest and Southeast sterilization manufacturing hubs | Medium term (2-4 years) |

| Material-Compatibility Failures When Shifting Modalities | -0.4% | National, particularly affecting product portfolios in mid-EtO-to-radiation transitions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EtO Emissions and Compliance Volatility

EtO remains indispensable for many heat-sensitive products, but the United States sterilization services market faces uncertainty because the regulatory framework around emissions has changed quickly and remains contested. The EPA’s 2024 final rule projected USD 313 million in capital investment and USD 74 million in annualized compliance costs across 89 commercial EtO facilities, which materially changed the economics of standalone gas operations. The March 2026 reconsideration proposal then reopened core issues including risk-based standards, enclosure requirements, and continuous monitoring, which shortened planning horizons for operators and customers alike[2]Environmental Protection Agency, “National Emission Standards for Hazardous Air Pollutants, Ethylene Oxide Emissions Standards for Sterilization Facilities Residual Risk and Technology Review,” Federal Register, govinfo.gov. STERIS stated in January 2025 that an Illinois EtO trial had concluded, which highlights that legal exposure has become part of the operating environment for major participants as well. In the United States sterilization services market, this volatility pushes customers toward suppliers that can offer EtO only where needed and shift the rest of the load into radiation or other lower-temperature options.

High Capex for Compliant Multi-Modal Capacity

The market also faces a capital barrier because compliant multi-modal capacity now requires spending on emissions controls, irradiation systems, quality systems, and skilled site qualification at the same time. EPA analysis showed how large the burden already was for EtO compliance alone, and that did not include the extra investment needed to diversify into X-ray, E-Beam, or VHP platforms. Steri-Tek’s planned installation carried an announced value of USD 17 million to USD 21 million, which shows that new high-throughput X-ray assets require capital on the same scale as major emissions projects. BGS US also showed that even a straightforward radiation facility can take months to bring from buildout to certified operation, which delays revenue realization for new entrants. This gives larger incumbents an edge in the United States sterilization services market because they can spread long payback periods across broader networks and existing customer contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Method: Radiation Technologies Challenging EtO Structural Dominance

EtO sterilization accounted for 45.31% of the United States sterilization services market share by method in 2025, and that position still reflects its fit for heat-sensitive devices and complex assemblies. The EPA stated that EtO sterilizes 50% of all medical devices used in the country each year, or more than 20 billion units, which explains why the method remains hard to displace even under tighter regulation. Gamma irradiation held the second-largest position, supported by established customer validation pathways and cobalt-60-linked supply capacity. Sotera Health reported 25.8% constant-currency growth in Nordion cobalt-60 revenue in Q1 2026, which showed continued demand for radiation inputs tied to the broader sterilization ecosystem[3]Sotera Health Services, LLC, “Sotera Health Delivers Strong First-Quarter 2026 Results and Reaffirms 2026 Outlook,” GlobeNewswire, globenewswire.com.

X-ray irradiation is the fastest-growing method in the United States sterilization services market, with forecast growth of 9.38% through 2031. Sterigenics and STERIS both expanded commercial X-ray capacity, which signals that accelerator-based radiation is moving into a more mainstream role for contract services. BGS US also added E-Beam capacity in Pennsylvania in 2025, which widened the radiation choice set for manufacturers in the Northeast and mid-Atlantic. VHP, NO2, E-Beam, and dry-heat remain smaller niches, but their role rises when customers need low-temperature processing, fast turnaround, or better compatibility with sensitive materials.

By Mode of Delivery: Off-Site Model Under Pressure From Resilience Mandates

Off-site service-center sterilization held 66.24% of United States sterilization services market share by delivery mode in 2025, supported by the high cost of maintaining compliant multi-modal infrastructure inside each manufacturing site. The model remains attractive because it gives customers access to validated processes, trained operators, and established release documentation without full facility ownership. It also fits the long-duration service agreements that stabilize throughput for large contract sterilizers. In practice, this keeps the off-site model central to the United States sterilization services market even as customers ask for more redundancy and closer proximity to production lines.

On-site or in-house-as-a-service is the fastest-growing delivery model, with the United States sterilization services market size for this segment projected to grow at an 8.52% CAGR through 2031. Under this approach, the service provider installs, qualifies, and operates equipment at the customer site while maintaining the quality trail expected for outsourced processes. QMSR supports that shift because it places stronger emphasis on documented control over outsourced activities and clearer accountability across supplier relationships. That makes the model especially attractive for high-volume pharmaceutical programs and device lines that need more supply chain flexibility without taking on full regulatory responsibility for the sterilization unit.

By Service Type: Validation Complexity Creates New Revenue Tier Above Contract Sterilization

Contract sterilization services accounted for 68.52% of the United States sterilization services market size by service type in 2025, which reflects their core role in routine terminal processing. This segment stays large because switching suppliers is difficult once dose setting, packaging validation, and regulatory submissions are tied to an approved process. QMSR has increased the paperwork burden around outsourcing control, which means customers now expect sterilizers to provide stronger records as part of the base service offer. Advisory and process development services remain smaller in revenue terms, but they become essential when a manufacturer needs to move a product family from EtO to radiation or another low-temperature option.

Validation and testing services are the fastest-growing service category, with the United States sterilization services market size for this segment forecast to advance at an 8.25% CAGR through 2031. Nelson Labs announced in August 2025 that it would double cleanroom capacity at its Salt Lake City headquarters to support rising sterility assurance demand, with the work expected to be completed in 2026. Nelson Labs also introduced RapidCert in September 2025, which reduced biological indicator confirmation timelines and addressed a release bottleneck for customers managing inventory quarantine. The broader effect is that testing, advisory support, and execution are being bundled more tightly across the United States sterilization services market because customers want fewer handoffs and cleaner audit trails.

By End User: Biopharma Growth Outpacing Device Sector, Reshaping Capacity Priorities

Medical device manufacturers represented 42.84% of the United States sterilization services market size by end user in 2025, supported by high single-use volumes and long-duration supply agreements. This customer base is steady because leading device companies already work through validated sterilization pathways and established vendor relationships. Hospitals and ambulatory surgery centers remain relevant, but most of their direct sterile processing activity still focuses on in-house reprocessing for reusable instruments rather than large-scale outsourced terminal sterilization. Clinical laboratories, research organizations, and other end users add incremental demand where validated processing is needed for waste, consumables, and cleanroom materials.

Pharmaceutical and biopharmaceutical manufacturers are the fastest-growing end-user group in the United States sterilization services market, with demand forecast to rise at a 9.83% CAGR through 2031. Their requirements differ from device production because drug-contact surfaces, combination products, and single-use bioprocessing systems need tighter control over residues, dose, and material interaction. STERIS said in fiscal 2026 commentary that pharmaceutical buying patterns on the capital side were returning and that reshoring was supporting demand for United States-based sterilization capacity, which aligns with this segment’s stronger outlook. As this mix shifts, providers with E-Beam, X-ray, and advanced validation support are likely to win more new programs because those tools fit the operational profile of faster-growing pharmaceutical accounts.

Geography Analysis

The United States sterilization services market has its deepest commercial footprint in the Midwest, where medical device manufacturing, established logistics corridors, and legacy sterilization campuses still support high outsourced volumes. Ohio, Illinois, Indiana, and Minnesota remain central because they combine device production density with a long operating history in commercial sterilization services. STERIS completed its Libertyville, Illinois expansion in June 2024, adding X-ray capability to an existing irradiation campus and reinforcing the Midwest’s role in the radiation transition. STERIS also announced a USD 60 million sterility assurance manufacturing center of excellence in Mentor, Ohio, targeted for late 2027 operations, which shows that capital still flows into the region despite tighter regulatory expectations. This leaves the Midwest in a transition phase, where older EtO dependence is under pressure while irradiation and broader sterility assurance capacity continue to attract investment.

The Southeast is becoming the most active new-build zone in the United States sterilization services market because device and biopharma manufacturing are expanding there and customers want more regional redundancy. Sterigenics opened a new X-ray facility in Haw River, North Carolina, in April 2026 near Research Triangle Park and the BioPharma Crescent, which gave the region a broader outsourced irradiation base. That opening reduces transport distance for many Southeastern manufacturers and improves access to multi-technology sterilization planning. It also shows that new investment is concentrating in modalities positioned as flexible and supply-chain-resilient rather than tied to a single chemistry. In practical terms, the Southeast is gaining importance because it links new sterilization capacity more closely to active pharmaceutical and device production corridors.

The Northeast and mid-Atlantic are also rising in the United States sterilization services market as regional radiation coverage improves for the New Jersey and Pennsylvania biopharma corridor. BGS US began E-Beam operations at its 100,000-square-foot Imperial, Pennsylvania facility in July 2025, which marked the German specialist’s first United States site and added fresh regional capacity. That facility reduces the need for some Northeastern manufacturers to route loads to Midwestern sites for irradiation services. The Southwest and West Coast make up the next growth layer, with Texas positioned to gain relevance as X-ray capacity expands and California continuing to shape compliance expectations across suppliers serving national accounts. Taken together, regional development is moving the United States sterilization services market toward a more distributed network, where irradiation assets are added close to manufacturing hubs and customers place greater value on geographic backup options.

Competitive Landscape

The market is moderately concentrated at the top, with STERIS and Sterigenics operating the broadest integrated contract platforms by revenue base and site reach. STERIS said its Applied Sterilization Technologies segment exceeded USD 1 billion in fiscal 2026 revenue, and it reported 11% constant-currency service revenue growth for the year. Sotera Health reported Q1 2026 net revenue of USD 186 million and reaffirmed full-year 2026 guidance of USD 1.23 billion to USD 1.25 billion across its 3 businesses, with Sterigenics remaining a major pillar of that platform. These companies benefit from scale in sterilization, testing, and documentation, which matters more now that supplier oversight has become a larger part of inspection readiness under QMSR. Below them, the United States sterilization services market becomes much more fragmented, with regional EtO operators, E-Beam specialists, validation-focused laboratories, and smaller advisory firms serving narrower needs.

Technology investment is the clearest competitive separator in the United States sterilization services market. Sterigenics opened its Haw River X-ray site in 2026 to give customers broader modality choice from a single Southeast location, which strengthened its regional proposition for device and biopharma accounts. STERIS completed the Libertyville X-ray expansion in 2024, which made the same point from another direction by adding accelerator-based radiation to an established campus. BGS US added another pressure point when it launched a 100,000-square-foot E-Beam facility in Pennsylvania, creating regional competition and faster turnaround options in the Northeast. These moves matter because buyers increasingly prefer suppliers that can offer multiple validated pathways rather than ask customers to rebuild quality oversight around a single constrained method.

Service bundling is becoming another strong lever in the United States sterilization services market. Nelson Labs expanded cleanroom capacity and introduced RapidCert testing support, which reinforced the value of combining validation, biological indicator work, and release support with sterilization execution. STERIS also said it was executing a multiyear AI-based digital workflow project across its Healthcare and Life Sciences segments, while Censis continued promoting computer-vision-based instrument identification for sterile processing workflows. Providers with auditable systems that align to ISO 13485 and established radiation validation practice are in a better position to win multiyear contracts because customers want fewer quality gaps across qualification, routine processing, and testing. The result is a market where size still matters, but credible multi-modal capability and documented compliance discipline are deciding a larger share of new program awards in the United States sterilization services market.

United States Sterilization Services Industry Leaders

STERIS plc

Sotera Health

Andersen Sterilizers / Andersen Scientific

E-BEAM Services, Inc.

Prince Sterilization Services, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: STERIS plc announced a USD 60 million investment to construct a new sterility assurance manufacturing center of excellence in Mentor, Ohio, consolidating existing US production into a single, highly automated facility targeted for operational status by late calendar 2027.

- April 2026: Sterigenics (Sotera Health) opened a new X-ray sterilization facility at its Haw River, North Carolina campus, providing technology-agnostic irradiation capacity, gamma, X-ray, EtO, E-Beam, and NO2, from a single Southeast US location positioned 30 minutes from Research Triangle Park and 90 minutes from the BioPharma Crescent.

United States Sterilization Services Market Report Scope

As per the scope of the report, sterilization services refer to professional procedures or processes used to eliminate or destroy all forms of microbial life, including bacteria, viruses, fungi, and spores, from medical instruments, equipment, or surfaces. These services ensure that items are sanitized to a level that is safe for medical use, preventing infection and cross-contamination.

The United States sterilization services market is segmented by method, mode of delivery, service type, and end user. By method, the market includes ethylene oxide (EtO) sterilization, gamma irradiation, electron-beam (E-beam) irradiation, x-ray irradiation, steam (moist-heat) sterilization, dry-heat sterilization, vaporized hydrogen peroxide/gas plasma sterilization, and nitrogen dioxide sterilization. By mode of delivery, it is categorized into off-site (service-center) sterilization and on-site/in-house-as-a-service sterilization. By service type, the segmentation covers contract sterilization services, sterilization validation & testing services, and process development, advisory & optimization services. By end user, the market is divided into medical device manufacturers, pharmaceutical & biopharmaceutical manufacturers, hospitals & ambulatory surgery centers, clinical laboratories & research organizations, and other end users. For each segment, the market size and forecast are provided in terms of value (USD).

| Ethylene Oxide (EtO) Sterilization |

| Gamma Irradiation |

| Electron-Beam (E-beam) Irradiation |

| X-ray Irradiation |

| Steam (Moist-Heat) Sterilization |

| Dry-Heat Sterilization |

| Vaporized Hydrogen Peroxide / Gas Plasma Sterilization |

| Nitrogen Dioxide Sterilization |

| Off-site (Service-Center) Sterilization |

| On-site / In-house-as-a-Service Sterilization |

| Contract Sterilization Services |

| Sterilization Validation & Testing Services |

| Process Development, Advisory & Optimization Services |

| Medical Device Manufacturers |

| Pharmaceutical & Biopharmaceutical Manufacturers |

| Hospitals & Ambulatory Surgery Centers |

| Clinical Laboratories & Research Organizations |

| Other End Users |

| By Method | Ethylene Oxide (EtO) Sterilization |

| Gamma Irradiation | |

| Electron-Beam (E-beam) Irradiation | |

| X-ray Irradiation | |

| Steam (Moist-Heat) Sterilization | |

| Dry-Heat Sterilization | |

| Vaporized Hydrogen Peroxide / Gas Plasma Sterilization | |

| Nitrogen Dioxide Sterilization | |

| By Mode of Delivery | Off-site (Service-Center) Sterilization |

| On-site / In-house-as-a-Service Sterilization | |

| By Service Type | Contract Sterilization Services |

| Sterilization Validation & Testing Services | |

| Process Development, Advisory & Optimization Services | |

| By End User | Medical Device Manufacturers |

| Pharmaceutical & Biopharmaceutical Manufacturers | |

| Hospitals & Ambulatory Surgery Centers | |

| Clinical Laboratories & Research Organizations | |

| Other End Users |

Key Questions Answered in the Report

What is the 2026 value of the United States sterilization services market?

The United States sterilization services market is valued at USD 1.88 billion in 2026 and is forecast to reach USD 2.55 billion by 2031 at a 6.25% CAGR.

Why does EtO still lead by method if regulation is getting tighter?

EtO still held 45.31% of method revenue in 2025 because many heat-sensitive and complex medical devices still need a chemistry-based process that avoids heat, moisture, and some radiation effects.

Which sterilization method is growing the fastest through 2031?

X-ray irradiation is the fastest-growing method with a 9.38% CAGR through 2031, supported by new capacity additions in North Carolina, Illinois, and planned expansion in Texas.

Why are pharmaceutical and biopharmaceutical customers growing faster than device makers?

Pharmaceutical and biopharmaceutical manufacturers are projected to grow at a 9.83% CAGR through 2031 because their products and single-use systems need tighter control over residues, dose, and material compatibility.

How is QMSR changing vendor selection in sterilization services?

QMSR increases the need for stronger outsourcing controls, audit-ready documentation, and risk-based supplier management, which favors larger providers with mature quality systems.

Which delivery model is expanding the quickest?

On-site or in-house-as-a-service is the fastest-growing delivery model at an 8.52% CAGR through 2031 because it gives customers more resilience and control without requiring full ownership of sterilization infrastructure.

Page last updated on: