Sterile Injectable Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

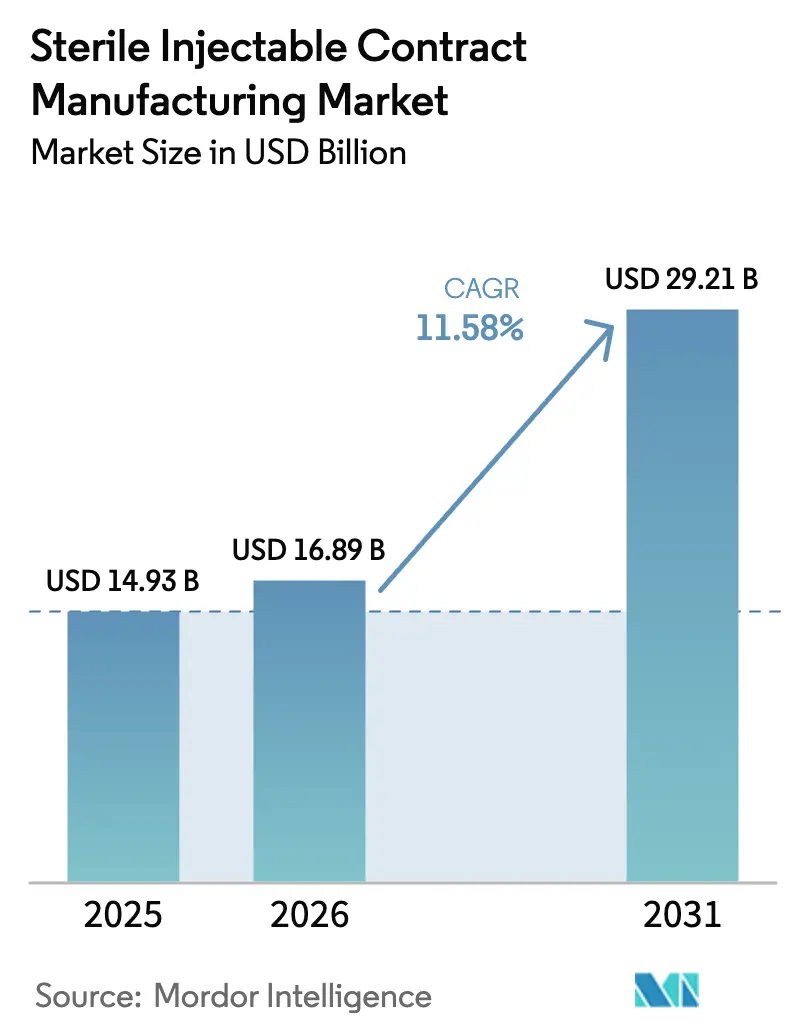

| Market Size (2026) | USD 16.89 Billion |

| Market Size (2031) | USD 29.21 Billion |

| Growth Rate (2026 - 2031) | 11.58% CAGR |

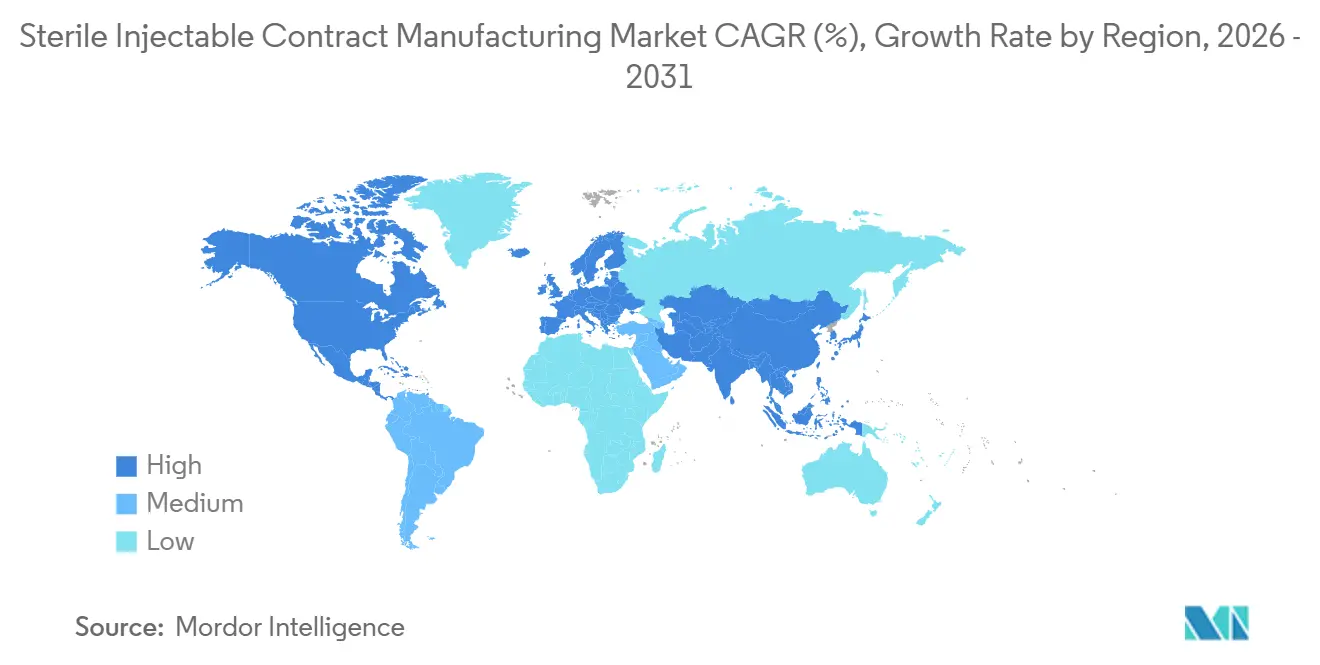

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterile Injectable Contract Manufacturing Market Analysis by Mordor Intelligence

The Sterile Injectable Contract Manufacturing Market size is projected to be USD 14.93 billion in 2025, USD 16.89 billion in 2026, and reach USD 29.21 billion by 2031, growing at a CAGR of 11.58% from 2026 to 2031.

The uptrend is anchored in drug-sponsor preference for asset-light supply chains, swelling biologics pipelines, and tighter drug-shortage rules that institutionalize dual sourcing. Capacity investments announced since 2024 illustrate how sponsors are outsourcing capital-intensive aseptic infrastructure while retaining product ownership. Prefilled devices for chronic therapies are increasingly displacing vials, thereby elevating demand for high-speed syringe filling and combination-product assembly. Biosimilar launches linked to looming patent cliffs add further volume and complexity, pulling CDMOs with proven regulatory credentials into long-term master service agreements. At the same time, supply-chain bottlenecks for borosilicate glass and single-use components temper near-term expansion of throughput.

Key Report Takeaways

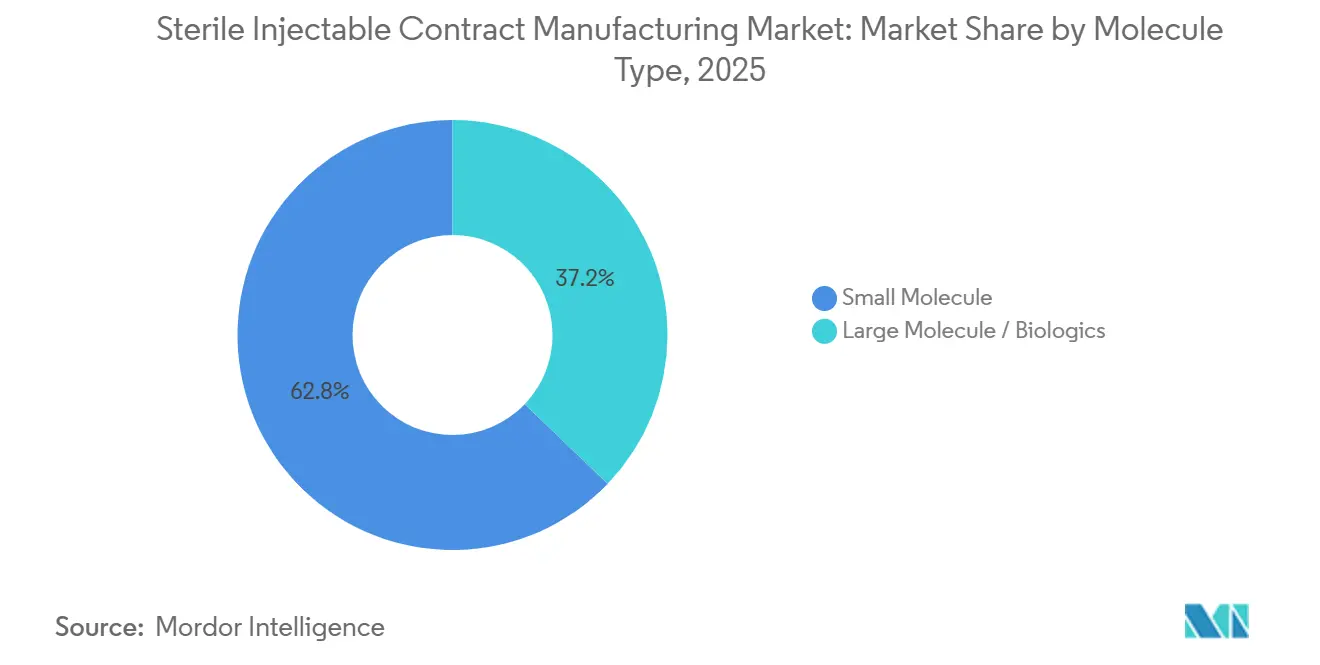

- By molecule type, small molecules captured 62.83% revenue share in 2025, while biologics are poised to expand at a 14.69% CAGR through 2031.

- By service stage, commercial manufacturing held 49.03% of the sterile injectable contract manufacturing market share in 2025, whereas clinical-stage services are projected to advance at a 15.65% CAGR through 2031.

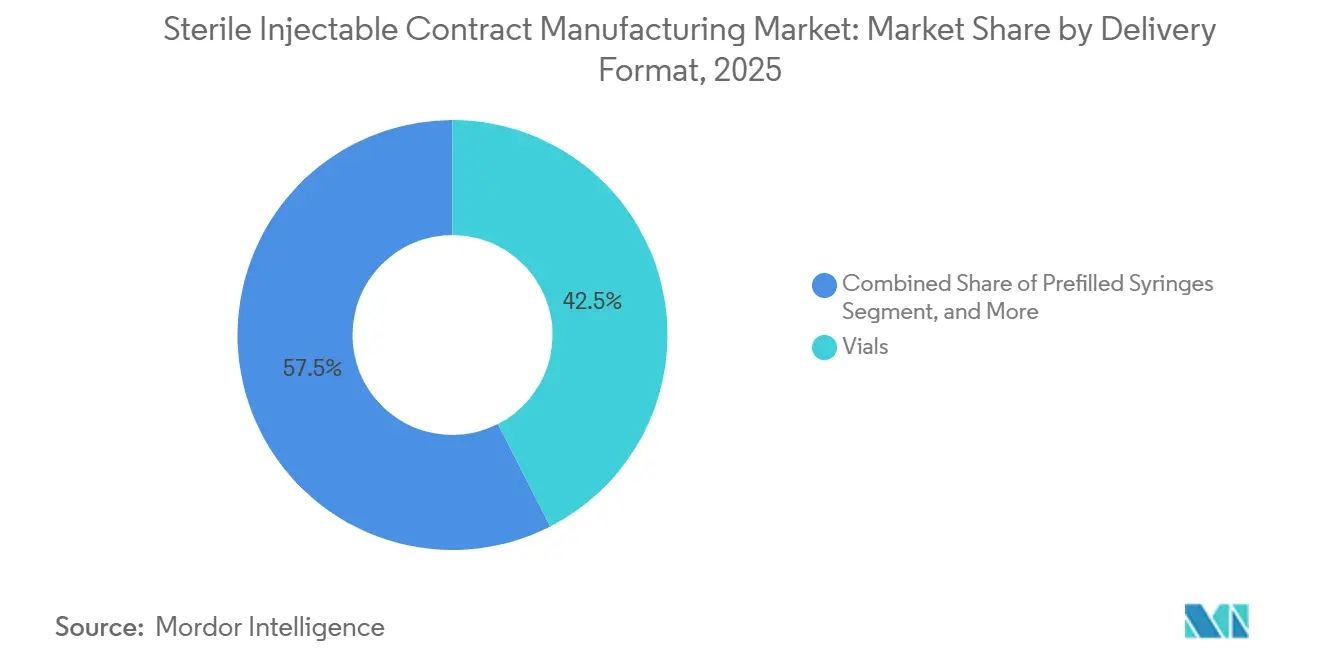

- By delivery format, vials held 42.48% of the sterile injectable contract manufacturing market share in 2025, and prefilled syringes are forecast to grow at a 12.84% CAGR to 2031.

- By geography, North America accounted for 37.26% of 2025 revenue; the Asia-Pacific region is projected to expand at a 16.04% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sterile Injectable Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics pipeline expansion boosts demand for specialized aseptic capacity | +2.8% | North America and Europe | Medium term (2-4 years) |

| Outsourcing surge to cut cap-ex and accelerate time-to-market | +2.5% | North America and Asia-Pacific | Short term (≤2 years) |

| Chronic-disease prevalence growing parenteral volumes | +1.9% | Global | Long term (≥4 years) |

| Patent cliffs spur generic and biosimilar injectables | +2.1% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Drug-shortage mitigation rules create mandatory dual sourcing | +1.6% | North America and EU | Short term (≤2 years) |

| Modular micro-fill isolators enable personalized therapy batches | +1.4% | North America and EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Biologics Pipeline Expansion Boosts Demand for Specialized Aseptic Capacity

The FDA cleared 16 novel biologics in 2024, up from 12 approvals the previous year, while the EMA approved 14 new biologicals, underscoring steady momentum in innovation.[1]U.S. Food and Drug Administration, “Novel Drug Approvals for 2024,” FDA.gov Cytotoxic antibody-drug conjugates require dedicated isolator suites, and fewer than 20 CDMOs presently offer such capacity at commercial scale. Cell and gene therapies add further complexity because autologous batches typically run below 100 units, prompting providers to adopt modular cleanrooms and single-use bioreactors that can be configured on demand. Catalent commissioned a USD 150 million biologics facility in Maryland in 2025, which features four independent high-potency suites, highlighting the capital expenditure (capex) race among top players.

Outsourcing Surge to Cut Cap-Ex & Accelerate Time-To-Market

Pfizer closed two legacy U.S. sterile plants in late 2024 and shifted output to partners, freeing USD 300 million in annual operating expense. More than 60% of Phase II oncology trials in 2025 were sponsored by virtual biotechs lacking internal manufacturing, increasing CDMO reliance for GMP supply. Continuous aseptic processing, now recognized under the FDA's Emerging Technology Program, can shorten lot-release times, yet it demands specialized know-how that most innovators source from contract partners.

Chronic-Disease Prevalence Growing Parenteral Volumes

The International Diabetes Federation counted 537 million adults living with diabetes in 2024, a burden forecast to surpass 640 million by 2030, lifting demand for GLP-1 receptor agonists delivered in prefilled pens.[2]International Diabetes Federation, “IDF Diabetes Atlas 2024,” IDF.org Injectable PCSK9 inhibitors reached 2 million U.S. patients in 2025, representing a 54% increase since 2023, and intensifying the need for high-speed syringe lines. Vetter reported an 18% year-over-year increase in syringe output in 2024, confirming the shift toward devices underway.

Patent Cliffs Spur Generic & Biosimilar Injectables

Blockbusters worth more than USD 100 billion in annual sales have patents expiring between 2024 and 2026, which is expected to catalyze a wave of biosimilar filings. Eight Humira biosimilars are expected to secure U.S. approvals by mid-2025, each requiring syringe or auto-injector fill-finish runs. Indian CDMOs capture a share by offering cost positions 30-40% below those of Western peers, while retaining EMA and WHO compliance. Contract fill-finish pricing for monoclonal antibodies decreased by 15% from 2023 to 2025, reflecting increased capacity and intense bidding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive GMP sterile facilities | -1.8% | Global | Long term (≥4 years) |

| Complex & evolving global regulatory compliance | -1.3% | North America & EU | Medium term (2-4 years) |

| Supply-chain pinch on pharma-grade borosilicate glass & SUT | -1.1% | Global | Short term (≤2 years) |

| Long lead times for isolator equipment causing capacity bottlenecks | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive GMP Sterile Facilities

Greenfield aseptic plants now exceed USD 200 million and require 3-5 years to qualify, deterring newcomers and limiting aggressive expansion among midsized providers. PwC measured ISO 5 cleanroom costs at USD 15,000 per square meter in 2025, up 22% from 2023, due to inflation in HVAC and validation. European CDMOs endured a 40% jump in utility bills during the 2024 gas-price spike, further squeezing project ROIs. Modular prefabs shrink timelines to 18 months but still face regulatory uncertainty about reconfiguration controls.

Complex & Evolving Global Regulatory Compliance

The FDA issued 127 sterile-manufacturing warning letters in 2024, a 15% increase over 2023, primarily due to environmental monitoring gaps. EMA Annex 1 revisions mandate real-time contamination controls that many plants struggled to install within an 18-month transition window.[3]European Medicines Agency, “Annex 1 Revisions,” EMA.europa.eu Divergent NMPA rules on local clinical trials for biosimilar compounds place the burden on global supply strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Type: Biologics Outpace Legacy Small-Molecule Volumes

Small molecules retained a 62.83% revenue share in 2025; however, biologics revenue is forecast to expand at a 14.69% CAGR, meaning that the Sterile Injectable Contract Manufacturing market size for biologics will accelerate faster than the broader service pool. Pfizer CentreOne confirmed that biologics represent 55% of pipeline deals, up sharply from 38% two years earlier. CDMOs with isolator-based cytotoxic suites enjoy premium pricing for ADC campaigns. Small-molecule volumes remain vital for saline, dextrose, and anesthetic lines, yet overcapacity in Eastern Europe has driven an 8% price decline since 2023. Subcutaneous biologics, recently cleared by the FDA for home use, are steering investment toward high-viscosity syringe filling. WuXi Biologics allocated USD 240 million to expand ADC capacity in Ireland, reflecting the scale of sponsor demand.

By Service Stage: Clinical Manufacturing Surges on Virtual-Biotech Demand

Commercial contracts accounted for 49.03% of 2025 revenue; however, clinical services are growing at a 15.65% CAGR, as virtual biotechs are dominating early-stage oncology and rare-disease pipelines. Deloitte found that over 60% of Phase II oncology studies in 2025 were conducted by firms with fewer than 50 employees, all of which outsourced GMP supply. Catalent reported a 19% revenue increase in 2024, driven by the onboarding of rapid-turnaround oncology programs. The FDA's Accelerated Approval pathway, which granted 15 oncology clearances in 2024, encourages sponsors to secure commercial-scale capacity earlier and to integrate clinical and commercial operations under multi-phase master agreements.

By Delivery Format: Prefilled Syringes Gain on Auto-Injector Integration

Vials still accounted for 42.48% of 2025 sales; however, prefilled syringes are expected to g row at a 12.84% CAGR, as patient-centric chronic-disease regimens increasingly favor self-administration. GLP-1 and TNF-alpha programs doubled syringe demand at Vetter in 2024. The Sterile Injectable Contract Manufacturing market size for prefilled formats benefits from the simultaneous demand for cartridge assemblies used in connected insulin pens. FDA combination-product guidance issued in 2025 obliges CDMOs assembling devices to register as device manufacturers, prompting strategic alliances between drug-fill specialists and device firms. Glass shortages in 2024 pushed some providers toward COC/COP barrels, although protein-adsorption validation remains a hurdle.

Geography Analysis

North America generated 37.26% of 2025 revenue thanks to dense clusters of FDA-inspected suites in North Carolina, New Jersey, and Maryland. Sponsors value proximity for tech-transfer collaboration, and premium pricing offsets higher labor costs. Nonetheless, Asia-Pacific is forecast to lead growth at a 16.04% CAGR through 2031. China’s “bio-security” policy encourages domestic fill-finish, and WuXi Biologics’ USD 200 million Wuxi plant exemplifies the surge in localization. India leverages the WHO prequalification to export biosimilars to cost-sensitive regions, thereby meeting demand well above its local needs.

The EMA centralized review process enables a single qualified site to serve all EU members, providing regional CDMOs with the flexibility to scale. High European energy prices, however, narrowed margins by 2024 and spurred interest in renewable power purchase agreements. Middle East & Africa, though tiny, is gaining relevance after Saudi Vision 2030 set a 40% local drug-manufacturing target, leading several CDMOs to scope greenfield projects.

South America benefits from Brazil’s streamlined biosimilar interchangeability rules, established in 2024, which attract foreign joint ventures seeking entry into the local market. National content mandates provide volume commitments critical for financing sterile suites, and they reduce regulatory risk for early-stage CDMOs entering the region.

Competitive Landscape

The sterile injectable contract manufacturing market is fragmented, reflecting low market concentration. Catalent, WuXi Biologics, Vetter, Pfizer CentreOne, and Boehringer Ingelheim BioXcellence leverage global quality systems and multiregional licensure to win long-term contracts. Catalent’s 2024 acquisition of a modular micro-fill platform extended its reach into autologous cell therapies, a segment poorly served by large-batch facilities. Patent analysis from USPTO revealed a 28% year-over-year rise in grants covering continuous aseptic processing, spotlighting process-innovation arms races among leading CDMOs.

Mid-tier challengers focus on niche capabilities such as ultra-potent ADC isolation and AI-driven real-time release. Recipharm reduced out-of-spec weights by 15% through machine-learning monitored filler heads, trimming batch disposition from weeks to days. Price pressure persists: antibody fill-finish rates declined by another 15% between 2023 and 2025, encouraging consolidation as providers seek to achieve volumetric scale. Isolator supply bottlenecks lengthen equipment delivery to 18 months, disadvantaging new entrants and cementing incumbent share.

Sterile Injectable Contract Manufacturing Industry Leaders

Recipharm AB

Aenova Group

Baxter BioPharma Solutions

Catalent Inc.

Vetter Pharma-Fertigung GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Delpharm committed USD 140 million to expand isolator-based capacity at its Boucherville, Canada, site.

- January 2025: PCI Pharma Services completed a USD 365 million enlargement of EU and U.S. lines for drug-device combinations.

- December 2024: Novo Holdings closed its USD 16.5 billion takeover of Catalent, integrating a global sterile network.

- November 2024: CordenPharma enhanced six technology platforms, including aseptic fill-finish, to serve complex injectables.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the sterile injectable contract manufacturing market as the value generated when third-party contract development and manufacturing organizations (CDMOs) formulate, fill-finish, and package parenteral drugs, small molecules, biologics, and vaccines under aseptic conditions that meet global cGMP guidelines.

Scope Exclusions: In-house production by innovator or generic firms, clinical trial batches below pilot scale, and non-sterile dose forms are left outside the model.

Segmentation Overview

- By Molecule Type

- Small Molecule

- Large Molecule / Biologics

- By Service Stage

- Pre-clinical Manufacturing

- Clinical Manufacturing

- Commercial Manufacturing

- By Delivery Format

- Vials

- Prefilled Syringes

- Cartridges

- Ampoules & Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Seasoned plant managers, quality leads, and procurement heads across North America, Europe, and Asia are interviewed or surveyed to validate utilization rates, average batch sizes, biologic fill yields, and planned capacity additions, allowing us to reconcile gaps found during secondary work.

Desk Research

We begin by mapping the installed fill-finish footprint, regulatory filings, and import-export streams through public datasets such as US FDA's Drug Establishment Current Registration, EMA EudraGMDP, UN Comtrade trade codes, and industry association yearbooks like ISPE's aseptic processing survey. Annual reports, 10-Ks, and investor decks help our analysts gauge client outsourcing ratios. Paid databases, D&B Hoovers for company revenue splits and Dow Jones Factiva for deal tracking, anchor financial signals. The sources named illustrate our approach and are not an exhaustive list.

Market-Sizing & Forecasting

A top-down reconstruction starts with global sterile drug production volumes and average outsourcing penetration, which are then cross-checked through selective bottom-up roll-ups of leading CDMO revenues. Key variables like annual FDA injectable approvals, share of biologics in late-stage pipelines, oncology incidence, global fill-finish capacity growth, and prevailing average selling prices feed a multivariate regression that projects demand; an ARIMA overlay captures cycle shifts. Where supplier data are missing, regional proxy ratios are applied and later aligned to interview feedback before locking the baseline.

Data Validation & Update Cycle

Outputs pass two-step peer review, anomaly scans against trade and approval trends, and variance checks versus prior editions. Reports refresh each year, with mid-cycle updates triggered by major plant closures, capacity expansions, or landmark drug approvals.

Why Our Sterile Injectable Contract Manufacturing Baseline Commands Reliability

Published estimates diverge because research firms select varied service mixes, molecule scopes, and refresh cadences.

Key gap drivers include whether pre-filled devices and vaccines are counted, the use of aggressive biologic ASP escalators, and refresh timing. Mordor runs annual model resets, while others rely on multi-year roll-forwards, leading to drift. Currency conversion choices and undisclosed capacity assumptions further widen spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.17 B (2025) | Mordor Intelligence | - |

| USD 17.9 B (2025) | Global Consultancy A | counts clinical batches and omits currency re-baselining |

| USD 17.88 B (2025) | Regional Consultancy B | applies uniform biologic price uplift without capacity cross-checks |

| USD 21.4 B (2024) | Trade Journal C | bundles device assembly and secondary packaging revenues |

Taken together, the comparison shows that when scope alignment, transparent variables, and timely refreshes are applied, Mordor's figure offers decision-makers a balanced, reproducible baseline they can confidently anchor to strategic plans.

Key Questions Answered in the Report

How fast is global demand for outsourced sterile injections growing?

Aggregate revenue is projected to rise at an 11.58% CAGR from 2026 to 2031, reflecting persistent biologics expansion and biosimilar launches.

Which region will add capacity the quickest?

Asia-Pacific is forecast to post a 16.04% CAGR through 2031 as China and India build fill-finish suites aligned with local biologics policies.

Why are prefilled syringes gaining share over vials?

Prefilled syringes support self-administration, reduce dosing errors, and integrate easily into auto-injectors, leading to a 12.84% forecast CAGR for the format.

What keeps new CDMOs from entering the market?

Building a compliant aseptic facility exceeds USD 200 million and can take up to five years, while equipment lead times for isolators stretch beyond 18 months.

What technology shifts matter most to sponsors?

Continuous aseptic processing, modular micro-isolators, and AI-enabled real-time release are increasingly decisive for contract-award decisions.

Page last updated on: