Iraq Healthcare Surgical Procedures Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

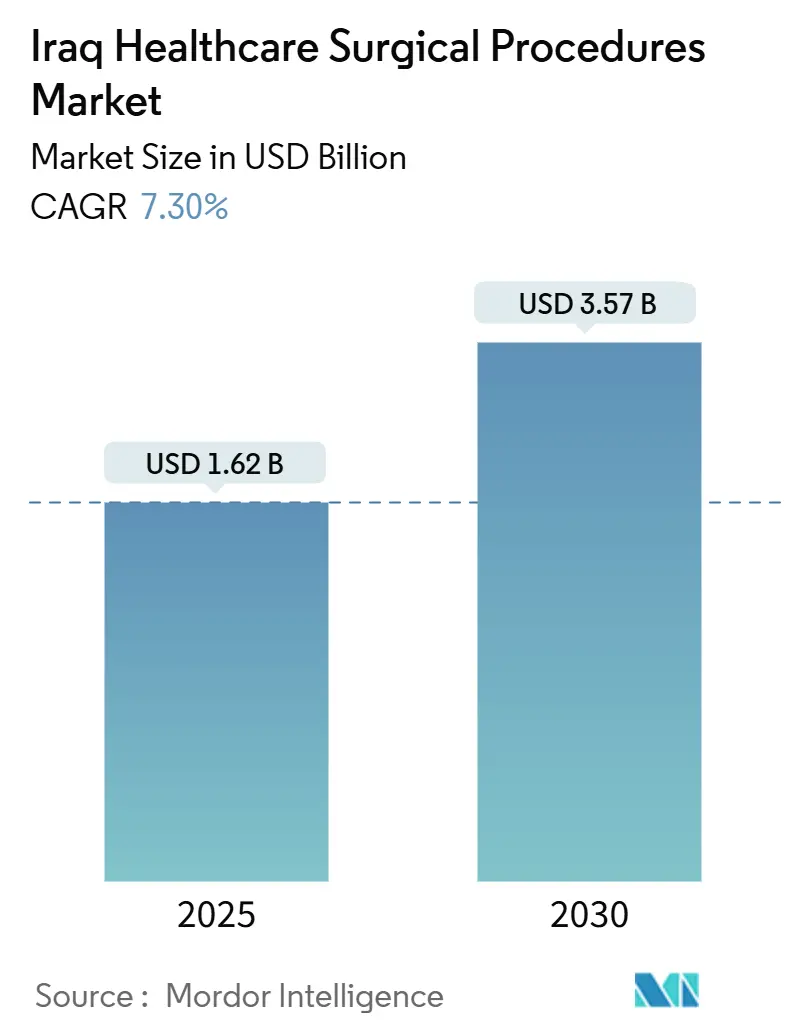

| Market Size (2025) | USD 1.62 Billion |

| Market Size (2030) | USD 3.57 Billion |

| Growth Rate (2025 - 2030) | 7.30% CAGR |

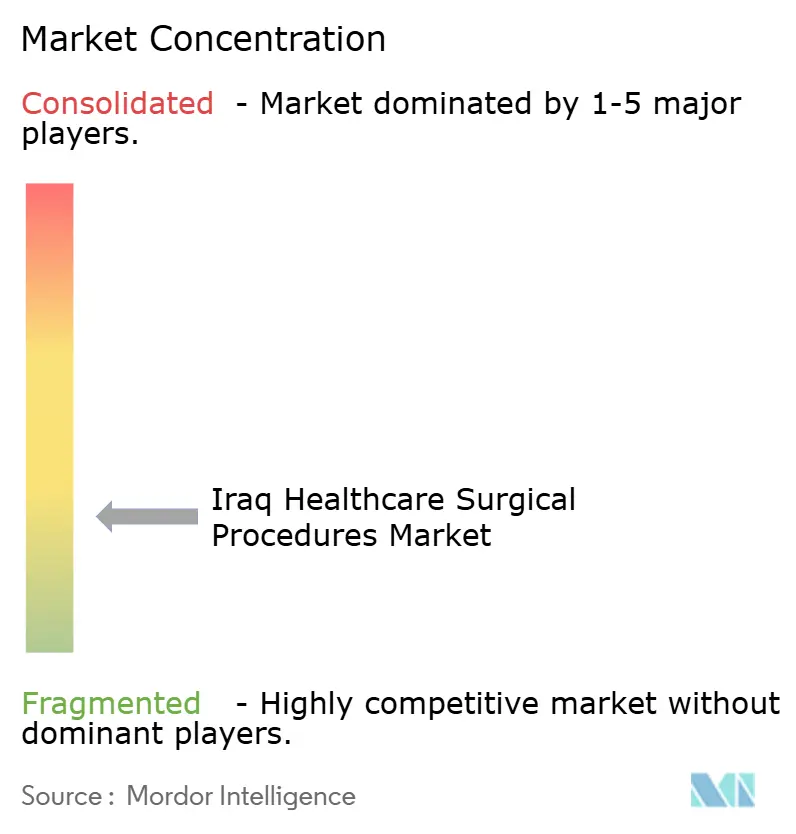

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq Healthcare Surgical Procedures Market Analysis by Mordor Intelligence

The Iraq healthcare surgical procedures market size stood at USD 1.62 billion in 2025 and is projected to reach USD 3.57 billion by 2030, registering a 7.30% CAGR over the forecast period. A shift from post-conflict trauma response toward comprehensive elective and specialty care underpins this growth, supported by more than USD 350 million in hospital construction agreements with Chinese engineering groups and the steady rollout of national fellowship programs that widen the surgical workforce pipeline. Orthopedic procedures continue to dominate volumes because of traffic accidents and legacy conflict injuries, while neurosurgery scales fastest on the back of intensive mentorship initiatives and expanded microsurgical capacity. Investment is also flowing into private hospitals that promise shorter waiting lists and international accreditation, although public tertiary centers still anchor the national referral network. Currency pressures, intermittent utilities in provincial theatres, and shortages of anesthesia staff present near-term operational barriers, yet the overall trajectory points to rising caseloads and broader service diversification across Iraq’s main urban hubs.

Key Report Takeaways

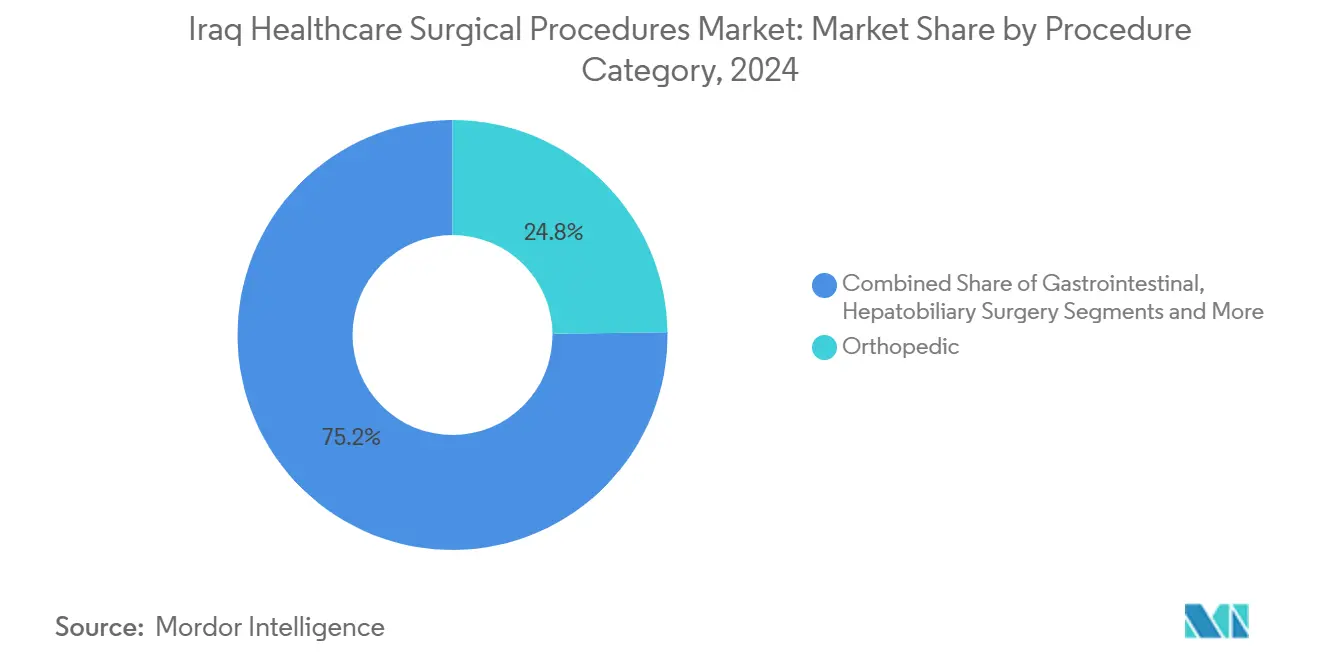

- By procedure category, orthopedics accounted for 24.8% of Iraq healthcare surgical procedures market share in 2024, while neurosurgery is forecast to advance at a 10.80% CAGR through 2030.

- By surgical approach, open surgery held 46.7% of the Iraq healthcare surgical procedures market share in 2024, and laparoscopic techniques are poised for the quickest uptake, expanding at a mid-single-digit CAGR to 2030.

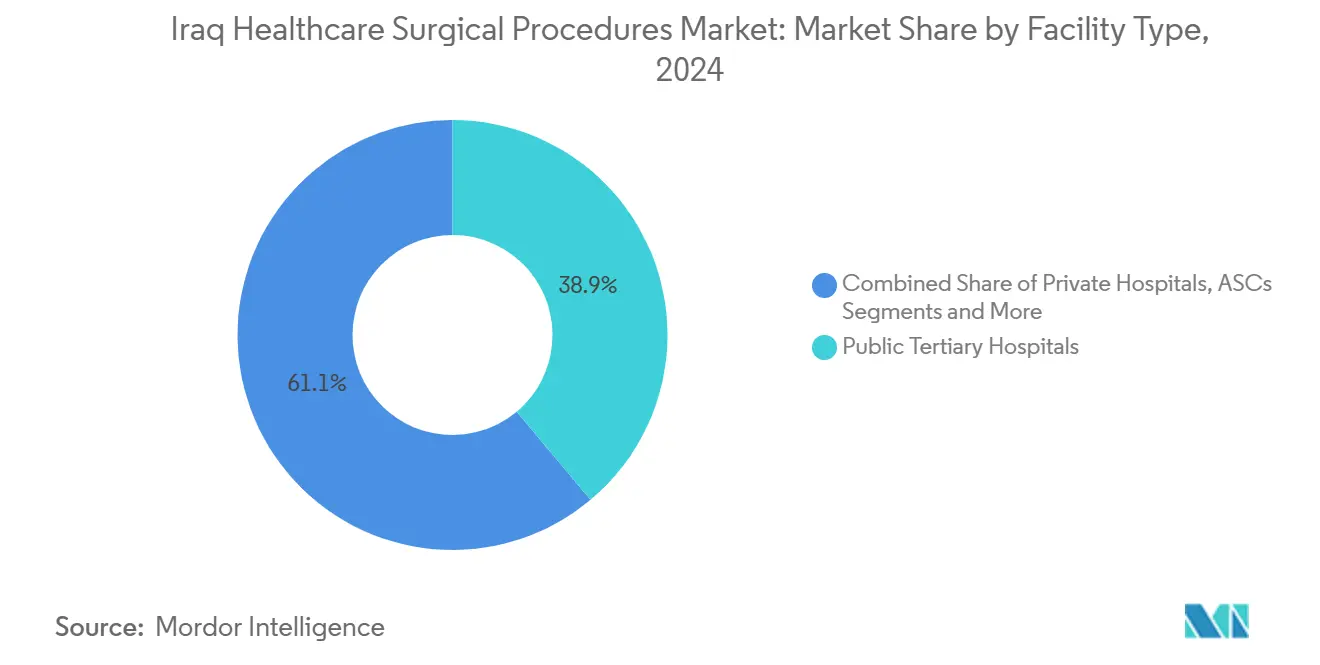

- By facility type, public tertiary hospitals captured 38.9% of the Iraq healthcare surgical procedures market size in 2024, while privately managed hospitals are growing fastest at 9.50% CAGR on the strength of international operating contracts.

Iraq Healthcare Surgical Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Foreca | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising trauma & conflict-related caseloads | +2.10% | Nineveh, Anbar, Baghdad | Medium term (2-4 years) |

| Expansion of private hospital chains | +1.80% | Baghdad and Erbil corridors | Long term (≥ 4 years) |

| Government investment in surgical training | +1.40% | Baghdad, Basra, Sulaimaniyah | Long term (≥ 4 years) |

| Re-establishment of national health insurance pilot | +1.20% | Nationwide | Medium term (2-4 years) |

| Medical tourism inflow from Syria & Yemen | +0.90% | Kurdistan border districts | Short term (≤ 2 years) |

| NGO-funded specialty surgical camps | +0.60% | Rural governorates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Trauma & Conflict-Related Caseloads Drive Orthopedic Surgery Demand

Orthopedic surgery represented 24% of total procedures in 2024, reflecting a steady flow of road-traffic and conflict injuries that require fracture fixation and limb-salvage techniques. At Baghdad’s Al-Kindy Teaching Hospital, maxillofacial fractures remain the most frequent emergency cases, while internal fixation audit data from Al-Kut registered a 3.9% implant failure rate in 558 patients—77.27% of which occurred in lower-limb repairs. Cross-border referrals persist, with Médecins Sans Frontières continuing to receive Iraqi trauma patients at its Amman center. Encouragingly, wartime upper-limb vascular injuries achieved 98.75% limb-salvage rates when treated within six hours, underscoring the system’s capacity for rapid orthopedic intervention.[1]Abdulkareem Al-Zahawi, “Fracture fixation outcomes at Al-Kut,” University of Thi-Qar Journal of Medicine, utq.edu.iq

Expansion of Private Hospital Chains Reshapes Care Delivery

International operators now manage nearly 1,000 beds across Karbala and Nasiriya, introducing ISO-accredited protocols and data-driven resource planning that cut perioperative delays and lift patient satisfaction. New builds such as the 400-bed Baghdad International Hospital incorporate 12 modular theatres and 80 outpatient suites designed for 600,000 annual visits, signaling a pivot toward mixed public-private models. These facilities adhere to Iraqi Ministry of Health standards while preparing for Joint Commission International audits, positioning them to capture rising middle-class demand for elective and minimally invasive procedures.

Government Investment in Surgical Training Modernizes Education

The University of Baghdad’s Surgery Department now offers tiered residency tracks across general, urology, cardiothoracic, and vascular disciplines, supplemented by a national neurosurgery mentorship program that has graduated 1,116 participants over six years. Curriculum updates emphasize simulation, modular skill labs, and blended digital content to ensure consistent competency despite resource constraints. Renal transplantation capacity has scaled to eight units performing 5,400 procedures by 2019, supported by a national registry that tracks outcomes and guides procurement.

Re-Establishment of National Health Insurance Expands Surgical Access

Social-security reforms introduced in 2024 extend coverage to informal workers and raise contribution rates for non-oil employees, targeting a reduction in catastrophic out-of-pocket payments that currently deter elective surgery uptake. The Health Insurance Authority, with backing from the IMF and ILO, is piloting e-claims processing to shorten reimbursement cycles and incentivize private-sector participation. Debates at Beit Al-Hikma emphasize alignment with universal-coverage principles to sustain equity and fiscal balance.[2]U.S. Social Security Administration, “International Update, March 2024,” ssa.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Foreca | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intermittent electricity & water supply in provincial theatres | -1.90% | Southern and northern provinces | Medium term (2-4 years) |

| Chronic shortage of anesthesia technicians | -1.50% | Nationwide, acute in rural sites | Long term (≥ 4 years) |

| Currency depreciation inflating imported consumable costs | -1.20% | National procurement hubs | Short term (≤ 2 years) |

| Security-related supply-chain disruptions | -0.80% | Mosul and Kirkuk corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage of Anesthesia Technicians Constrains Capacity

With only nine physicians per 10,000 residents and an estimated 20,000 doctors emigrating since 2010, Iraq struggles to staff operating theatres, particularly in anesthesia. A survey of 606 clinicians found 92% felt unsafe at work and one-third were considering emigration, trends that heighten perioperative risk and stretch duty rosters. Nursing education similarly battles outdated curricula and limited clinical placements, while the Kurdistan region—despite a calmer security backdrop—faces its own attrition of skilled personnel.[3]K. Smith, “Anaesthesia workforce shortage: reasons and potential solutions,” HealthManagement.org, healthmanagement.org

Currency Depreciation Threatens Supply-Chain Sustainability

Dinar weakness raises landed costs for sutures, implants, and anesthesia drugs that remain 90% import-dependent. Surveys in Babil governorate showed levofloxacin retailing at more than 9,000 dinars, eclipsing average daily wages and constraining postoperative infection management. Infection-control specialists warn that fluctuating exchange rates and fragmented pricing rules allow intermediaries to widen margins, perpetuating shortages of sterile disposables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Category: Trauma-Driven Orthopedics Hold the Lion’s Share

Orthopedic interventions formed the most significant segment of Iraq healthcare surgical procedures market, at 24.8% in 2024, owing to the country’s high incidence of high-energy limb fractures and degenerative joint disease. The Iraq healthcare surgical procedures market continues to rely on external NGO support for complex reconstructions. Yet, gradual improvements in implant supply chains and post-operative rehabilitation are elevating domestic case completions.

Neurosurgery is on a steeper growth curve, expanding at a 10.80% CAGR as endoscopic spinal decompressions and microvascular clipping gain traction in Baghdad and Basra. Mentorship exchanges with European societies and the deployment of neurosurgical microscopes in six public hospitals have brightened long-term neurological outcomes. Cardiovascular teams are also registering steady upticks in transcatheter workloads, notably with the Myval balloon-expandable heart valve that cut procedural times by 20% in a recent 50-patient series.

By Surgical Approach: Open Surgery Dominates but Minimally Invasive Methods Accelerate

Open operations represented 46.7% of Iraq healthcare surgical procedures market share in 2024, a testament to entrenched trauma workflows and limited access to advanced optics outside major centers. Nevertheless, laparoscopic liver and pulmonary hydatid cyst resections now achieve shorter operative windows, reduced blood loss, and quicker chest-tube withdrawal, outcomes that are persuading hospital managers to allocate capex toward tower systems and lightweight instruments.

Video-assisted thoracoscopic surgery and mini-thoracotomy approaches have also yielded superior pain profiles relative to conventional thoracotomy, while trans-radial coronary PCI registers a 96% technical-success rate alongside 80% patient preference for early ambulation. Pilot telesurgery links in Kurdistan are further expanding remote mentoring capabilities, signaling a gradual but decisive pivot toward technology-enabled care models.

By Facility Type: Public Tertiary Centers Anchor Care but Private Operators Gain Momentum

Public tertiary hospitals retained a 38.9% stake in the Iraq healthcare surgical procedures market during 2024, leveraging established residency programs and broad specialty coverage to handle the bulk of complex referrals. Infrastructure upgrades at Baghdad Teaching Hospital and Al-Kindi Teaching Hospital include modular theatres, negative-pressure ICUs, and integrated electronic medical record rollouts.

Private hospitals, although smaller on an individual basis, are the fastest-growing cohort at a 9.50% CAGR, buoyed by management contracts that fuse Gulf capital with European clinical governance. The 492-bed Al-Najaf Al-Ashraf Teaching Hospital, opened in 2024, typifies this model with 16 operating theatres, 44 ICU beds, and a 3,000-strong workforce operating under GKSD protocols. Ambulatory centers and military facilities round out the landscape, offering cost-sensitive day-surgery options and specialized trauma coverage, respectively.

Geography Analysis

The majority of surgical volume remains clustered in Baghdad, Basra, and Erbil, yet capital investments are diffusing services into Dhi Qar and Muthanna where Chinese-financed medical cities worth USD 350 million are under construction. Kurdistan sustains a buoyant medical-tourism trade, drawing patients from Syria and Yemen for basic orthopedic and general procedures, even as Iraqi citizens continue to seek higher-acuity cardiac and oncology interventions in Amman and Beirut.

Southern provinces face periodic electricity and water interruptions that delay theatre turnover, while northern corridors such as Mosul grapple with sporadic supply-chain disruptions linked to security incidents. Nevertheless, NGO missions have restored essential services in rural posts, with Heevie treating over 560,000 patients in 2023, including complex head and neck reconstructions. The interplay of domestic infrastructure upgrades, cross-border referral flows, and security dynamics will shape regional growth differentials through 2030.

Competitive Landscape

Competition is moderate, with no single provider exceeding a 10% caseload share. State-owned teaching hospitals dominate high-complexity workloads, whereas private chains capture expanding middle-income demand and are increasingly attractive to expatriate Iraqi surgeons. Estithmar Holding’s Elegancia Healthcare, Apex Health, and GKSD are the headline private operators, collectively managing around 1,900 licensed beds and introducing value-based care metrics that lift theatre utilization and reduce length of stay.

Technological innovation remains a differentiation lever: Basra Cardiac Center’s “Kurdistan technique” for complex coronary interventions reports 100% procedural success, while Baghdad institutions piloting trans-septal mitral valve repair cite 24-hour discharge protocols as a marketable edge. Pharmaceutical partnerships—such as Roche’s digital pathology rollout—advance diagnostic turnaround times, whereas local antibiotic manufacturing collaborations aim to buffer currency-linked cost spikes.

Iraq Healthcare Surgical Procedures Industry Leaders

Baghdad Teaching Hospital

Ibn Sina Hospital

Al-Kindi Teaching Hospital

Par Hospital

Basrah Teaching Hospital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: China State Construction Engineering Corporation signed a 490 billion-dinar (USD 350 million) contract to build a 13-facility medical city in Dhi Qar.

- March 2025: CAMC Engineering secured the Muthanna Provincial Hospital project covering 30,000 m² to serve 150,000 residents.

- August 2025: Apex Health obtained an investment license for the 400-bed Baghdad International Hospital featuring 12 ORs and 80 outpatient clinics.

Iraq Healthcare Surgical Procedures Market Report Scope

| Orthopedic Surgery |

| Cardiovascular Surgery |

| Gastrointestinal & Hepatobiliary Surgery |

| Obstetrics & Gynecological Surgery |

| Neurosurgery |

| Open Surgery |

| Laparoscopic Surgery |

| Endoscopic Procedures |

| Robotic-Assisted Surgery |

| Transcatheter / Percutaneous |

| Public Tertiary Hospitals |

| Public Secondary Hospitals |

| Private Hospitals |

| Ambulatory Surgical Centers |

| Military / Gov. Specialty Centers |

| By Procedure Category | Orthopedic Surgery |

| Cardiovascular Surgery | |

| Gastrointestinal & Hepatobiliary Surgery | |

| Obstetrics & Gynecological Surgery | |

| Neurosurgery | |

| By Surgical Approach | Open Surgery |

| Laparoscopic Surgery | |

| Endoscopic Procedures | |

| Robotic-Assisted Surgery | |

| Transcatheter / Percutaneous | |

| By Facility Type | Public Tertiary Hospitals |

| Public Secondary Hospitals | |

| Private Hospitals | |

| Ambulatory Surgical Centers | |

| Military / Gov. Specialty Centers |

Key Questions Answered in the Report

How big is Iraq healthcare surgical procedures market in 2025 and where is it headed by 2030?

Spending reached USD 1.6 billion in 2025 and is forecast to climb to USD 3.5 billion by 2030, reflecting a 7.30% CAGR.

Which surgery type generates the highest volume today?

Orthopedic procedures lead with a 24% share, driven by traffic accidents and residual conflict injuries.

What is the fastest-growing specialty through 2030?

Neurosurgery is expanding the quickest at a 10.80% CAGR, supported by structured mentorship programs and new microsurgical units.

Why are private hospitals gaining ground in Iraq?

Internationally managed facilities post a 9.50% CAGR because they shorten wait times, apply global quality standards, and attract self-pay patients.

How does currency depreciation affect operating rooms?

A weaker dinar inflates the cost of imported implants and disposables, tightening hospital budgets and risking intermittent shortages.

Will the re-established national health insurance improve access to surgery?

Yes, broader coverage for informal workers and faster e-claims processing aim to lower out-of-pocket spending and boost elective procedure volumes.

Page last updated on: