Postpartum Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

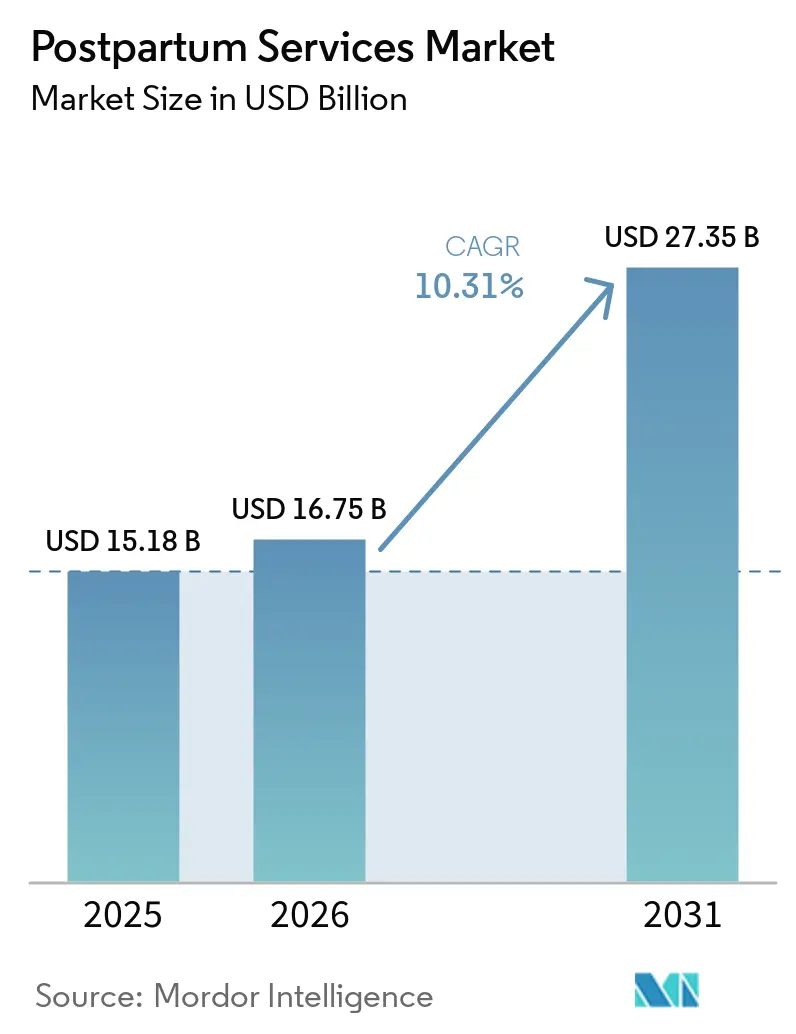

| Market Size (2026) | USD 16.75 Billion |

| Market Size (2031) | USD 27.35 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

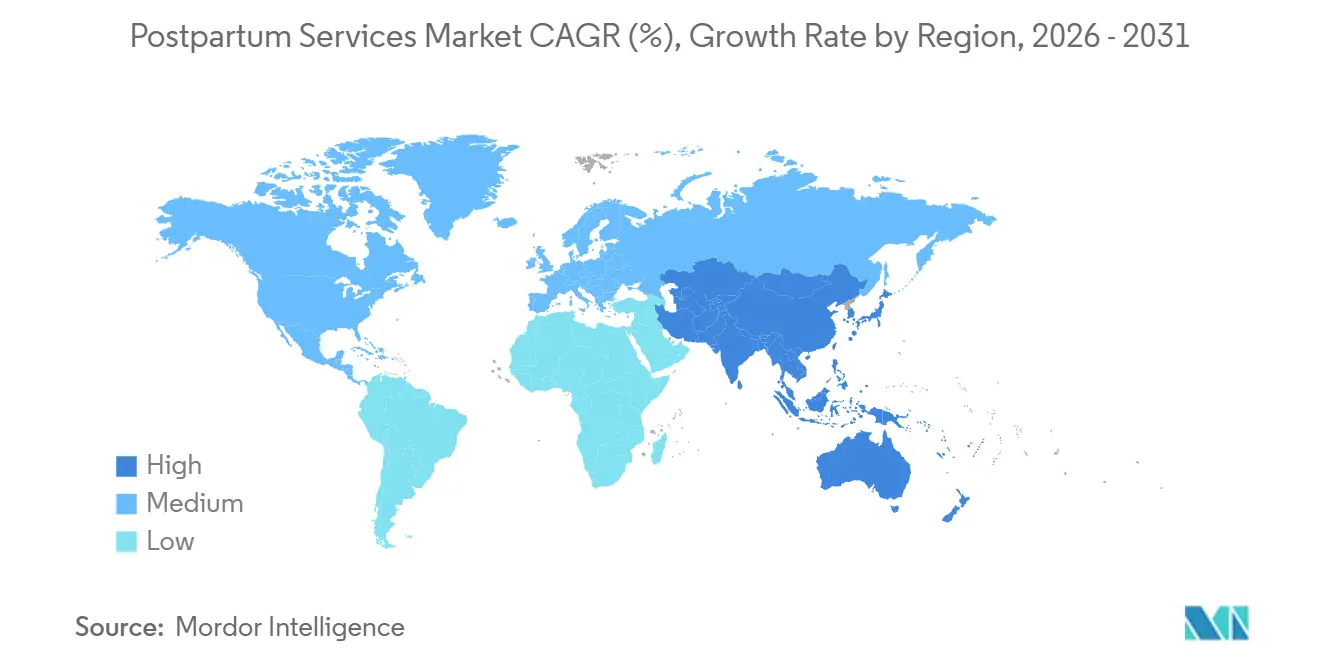

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Postpartum Services Market Analysis by Mordor Intelligence

The Postpartum Services Market size is expected to increase from USD 15.18 billion in 2025 to USD 16.75 billion in 2026 and reach USD 27.35 billion by 2031, growing at a CAGR of 10.31% over 2026-2031.

Increased clinical focus on the "fourth trimester," rising employer demand for healthier return-to-work timelines, and advancements in technology-enabled remote monitoring are driving a shift in expenditures. The market is transitioning from one-off, six-week check-ups to comprehensive care packages covering the first 12 weeks postpartum. Governments in North America and Europe are utilizing Medicaid, provincial health insurance, and statutory sick-leave benefits as strategic funding mechanisms. In the Asia-Pacific region, culturally aligned confinement hotels are being commercialized, integrating clinical oversight with traditional care practices. Digital platforms, supported by reimbursement-parity regulations, are addressing gaps caused by hospital shortages of certified lactation consultants. Simultaneously, the growing adoption of wearable devices is enabling real-time monitoring of uterine involution and cardiomyopathy. These developments are collectively driving the postpartum services market toward hybrid, omnichannel delivery models, offering improved clinical outcomes and enhanced patient engagement.

Key Report Takeaways

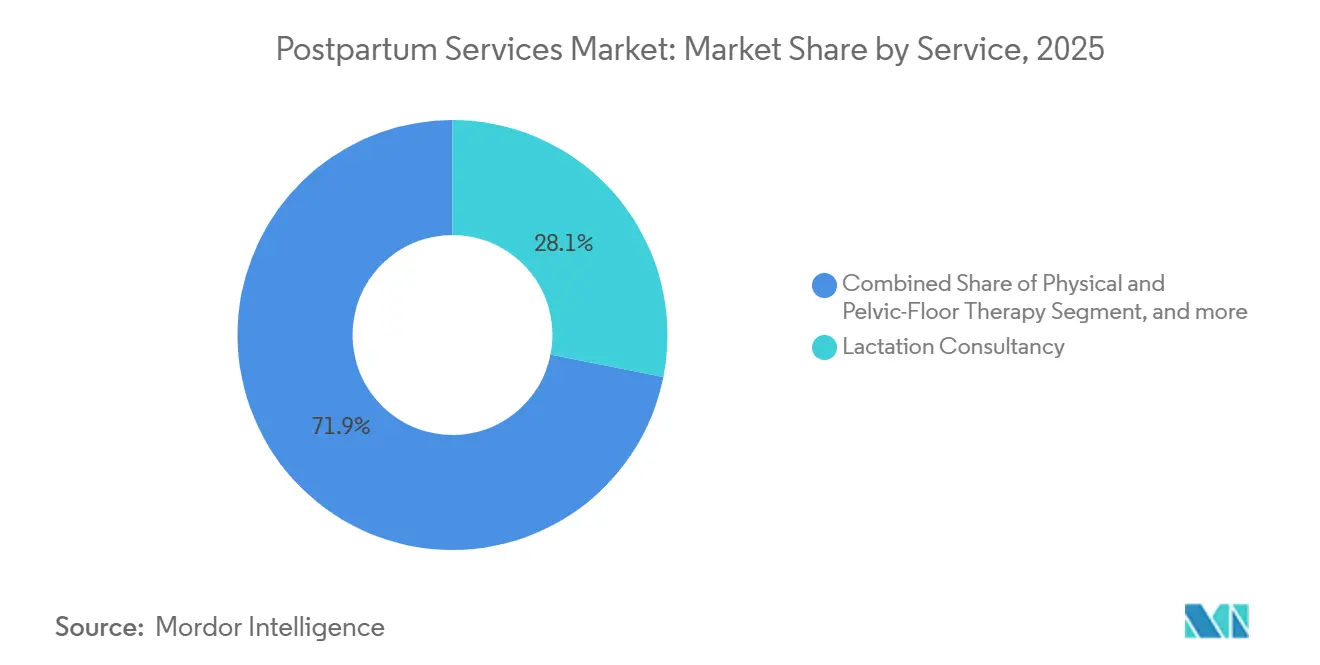

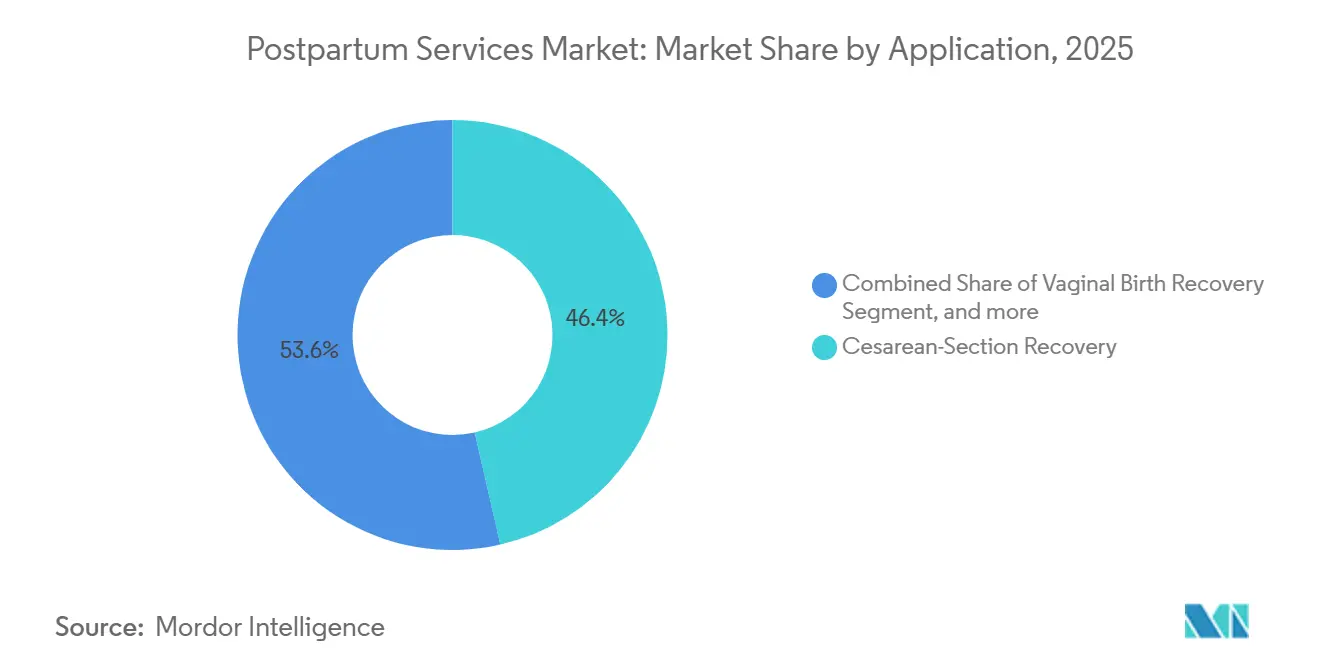

- By application, cesarean-section recovery led with 46.43% of postpartum services market share in 2025 and is projected to grow at a 12.87% CAGR through 2031.

- By facility type, private maternity hospitals and clinics accounted for 52.54% of the postpartum services market in 2025, while online platforms are advancing at a 13.21% CAGR through 2031.

- By service, lactation consultancy generated 28.12% of 2025 revenue, yet telehealth postpartum care is expanding at a 12.65% CAGR through 2031.

- By geography, North America accounted for 41.56% of global revenue in 2025; Asia-Pacific is set to register an 11.54% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Postpartum Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Maternal Health Awareness | +1.8% | Global, with stronger uptake in North America and Western Europe | Medium term (2-4 years) |

| Expansion of Government-Funded Postnatal Programs | +2.3% | North America, Europe, APAC (China, India) | Long term (≥ 4 years) |

| Growing Telehealth Adoption in Maternal Care | +2.1% | Global, led by North America and urban APAC | Short term (≤ 2 years) |

| Increasing Cesarean and High-Risk Birth Rates | +1.6% | Global, with highest rates in Latin America and China | Medium term (2-4 years) |

| Employer-Sponsored Postpartum Benefits Expansion | +1.2% | North America, Western Europe | Short term (≤ 2 years) |

| Emergence of Luxury Confinement Hotel Model in APAC | +0.9% | APAC core (China, Singapore, South Korea) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Maternal Health Awareness

Maternal-mortality audits revealed that 84% of U.S. pregnancy-related deaths in 2024 happened after discharge, immediately elevating postpartum follow-up to a public-health priority. Thirty-seven U.S. states now extend Medicaid coverage for a full year after delivery, granting 700,000 low-income mothers access to lactation support, wound care, and mental-health screening. Similar momentum is visible in Canada and Germany, where provincial and statutory insurers finance multiple home visits. Professional guidelines shifted in tandem; the American College of Obstetricians and Gynecologists recommends at least 3 visits within the first 12 weeks, rather than a single 6-week check-up[1]American College of Obstetricians and Gynecologists, “Optimizing Postpartum Care,” acog.org. Corporate America is reinforcing the trend, as 42% of companies with 500-plus staff subsidized postpartum services in 2025, up from 28% two years earlier.

Expansion of Government-Funded Postnatal Care Programs

New public-sector budgets are formalizing what had been volunteer or family-led support. India’s Pradhan Mantri Matru Vandana Yojana finances three postnatal home visits for 18 million mothers annually[2]Ministry of Health and Family Welfare, India, “Pradhan Mantri Matru Vandana Yojana 2025 Report,” mohfw.gov.in. China’s National Health Commission orders all tier-2 and tier-3 hospitals to operate dedicated recovery units, blending Western nursing standards with traditional Chinese medical techniques. The European Union’s 2025 Maternal Health Directive obligates every member state to reimburse four consultations within eight weeks, even in rural zones where clinics are scarce. Brazil’s public health service is piloting telehealth postpartum consultations across 12 states, illustrating how lower-income countries can scale services without new brick-and-mortar infrastructure.

Growing Telehealth Adoption in Maternal Care

Virtual platforms decouple care from geography. Maven Clinic logged a 140% year-on-year increase in video lactation visits in 2025, with two-thirds occurring after traditional clinic hours. Fourteen U.S. states enforce reimbursement parity, eliminating financial penalties for providers who deliver consultations online. Device innovation keeps pace: the FDA cleared abdominal sensors that measure fundal height plus wearables that flag cardiomyopathy, enabling earlier triage. Yet interoperability lags; fewer than 30% of vendors meet FHIR specifications, creating duplicate documentation when patients straddle hospital and app-based systems.

Increasing Cesarean and High-Risk Birth Rates

Cesarean sections constituted 21.1% of global births in 2025 and exceeded 40% in Brazil and China. Surgical deliveries result in longer recovery windows, increasing demand for wound care, physical therapy, and targeted lactation coaching. Johns Hopkins observed a 35% reduction in chronic pelvic pain when cesarean patients received two pelvic-floor sessions within six weeks. Rising maternal age—now 18% of U.S. births—fuels comorbidity, further intensifying postpartum monitoring needs.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce Shortage of Certified Postpartum Specialists | -1.4% | Global, acute in rural North America and sub-Saharan Africa | Long term (≥ 4 years) |

| Limited Insurance Coverage for Home-Based Services | -1.1% | North America, parts of Europe and Latin America | Medium term (2-4 years) |

| Fragmentation of Clinical Protocols Across Physical and Digital Settings | -0.7% | Global, most pronounced in North America and Western Europe | Short term (≤ 2 years) |

| Cultural Stigma Around Postpartum Mental Health in Emerging Economies | -0.6% | Middle East, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Workforce Shortage of Certified Postpartum Specialists

Only 22,400 International Board-certified lactation consultants remained active worldwide in 2025, a 12% slide from two years prior, driven by steep exam fees and unpaid clinical hours[3]International Board of Lactation Consultant Examiners, “2025 Annual Report,” iblce.org. U.S. families in rural counties waited an average of 21 days for an in-person consultation. Doulas face similar scarcity: fewer than 3,000 graduated across North America in 2024 against an estimated 400,000 annual service requests. Physical therapists specializing in pelvic-floor health stand at 1 per 530 postpartum women—well below the evidence-based benchmark of 1 per 200. Scholarships and hospital fellowships launched in 2025 are helpful, but will not close the gap before 2028.

Limited Insurance Coverage for Home-Based Services

A 2024 Kaiser Family Foundation review found that only 18% of U.S. commercial plans reimbursed postpartum nursing visits, with median payments of USD 85 against provider costs of USD 150–200. Doula engagements remain mostly out-of-pocket, pricing low-income households out. Oregon, Minnesota, and New Jersey introduced Medicaid doula reimbursement in 2024, but the USD 60 cap fails to cover travel or administrative time. Europe’s new directive pledges two funded home visits by 2027, yet fiscal constraints in Eastern Europe are slowing the rollout. Emerging-market public hospitals still rely on family caregivers, amplifying quality variability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Telehealth Outpaces Legacy Offerings

Lactation consultancy contributed 28.12% of 2025 revenue, firmly anchoring the postpartum services market, but telehealth care now sets the growth tempo at a 12.65% CAGR through 2031. Maven Clinic disclosed that virtual check-ins lowered postpartum hemorrhage readmissions by 22% through early hemodynamic alerts. Physical and pelvic-floor therapy follows, buoyed by a randomized 2024 study that cut stress incontinence incidence by 40% via eight therapy sessions. Medical complication management pivots around 24-hour hotlines embedded in hospital Bundles, while diet and nutrition counseling rides with gestational diabetes recovery mandates. Mental-health screening, now obligatory in 12 U.S. states, closes the loop on holistic care. Home-visit doula services remain premium due to staffing shortages and partial insurance coverage, capping penetration even as affluent urban families embrace continuous care.

AI-enabled triage bots pre-screen symptoms before routing to clinicians, and remote-patient-monitoring codes reimburse daily data uploads. Employers integrate postpartum services market offerings into leave benefits to curb attrition. Device makers cross-sell breast pumps and smart bassinets, expanding lifetime value per mother-infant dyad. As a result, the postpartum services market size for telehealth could top USD 9 billion by 2031 if parity laws expand to all 50 U.S. states.

By Application: Cesarean Recovery Commands Dual Leadership

Cesarean recovery accounted for 46.43% of 2025 revenue and should sustain a 12.87% CAGR, reinforcing its dominance in the postpartum services market. Private hospitals bundle abdominal binder fittings, scar management protocols, and 4 weeks of home nursing, with prices ranging from USD 3,500 to USD 8,000. Vaginal birth recovery remains critical for perineal trauma and pelvic-floor dysfunction, but lags cesarean in revenue because of shorter rehabilitation. Mental health management is emerging as the fastest-growing area of care, second only to cesarean care, propelled by universal screening guidelines. Breastfeeding support overlaps both birth types yet demands specialized interventions for surgical deliveries, where delayed lactogenesis is common.

In 2025, cesarean packages accounted for almost half of the postpartum services market size in Latin America, where Brazil’s 42% cesarean rate keeps demand elevated. Scar-care products, compression garments, and wound-healing teleconsults generate cross-selling opportunities. As national health systems debate optimal surgical thresholds, the postpartum services market share tied to cesarean recovery will likely remain resilient.

By Facility Type: Digital Platforms Disrupt Hospital Hegemony

Hospitals and private maternity clinics held 52.54% of the postpartum services market size in 2025, benefiting from patient capture during pregnancy and integrated electronic records. CloudNine converted 78% of delivery patients into postnatal packages, adding INR 1.2 billion (USD 14.4 million) in revenue. Yet online apps are climbing at a 13.21% CAGR, powered by employer contracts and parity statutes.

The luxury confinement centers, a niche but high-margin facility type, are blossoming in China, Singapore, and South Korea. Thomson Medical Group’s 28-day stay, priced at SGD 18,000 (USD 13,300), melds 24-hour lactation consultants with chef-curated meals, underscoring consumer readiness to pay for hotel-like recovery. Home-based services, constrained by workforce and reimbursement, cling to a premium, urban clientele.

Geography Analysis

North America generated 41.56% of 2025 global revenue, underpinned by Medicaid’s 12-month coverage extension, mandatory depression screening in 12 states, and rapid employer uptake of virtual benefits. The United States alone logged 1.2 million virtual postpartum visits on Maven Clinic in 2025. Canada’s provinces fund up to 4 home nurse visits for high-risk mothers, while Mexico pilots telehealth in states with a shortage of obstetricians.

Asia-Pacific is the fastest-growing region, with a 11.54% CAGR. China’s hospital mandate for recovery units, India’s three-visit home program that serves 18 million mothers, and Singapore’s confinement hotels all expand the postpartum services market. South Korea and Japan test municipal-funded hybrid centers that fuse traditional care with physical therapy.

Europe leverages universal health coverage: Germany reimburses unlimited midwife visits for the first 10 days, France funds 8 pelvic-floor physiotherapy sessions, and the EU directive sets a continent-wide minimum of 4 consultations. Eastern Europe lags in adopting home-visit reimbursement, though midwife scholarships in the United Kingdom aim to shorten rural wait times. The Middle East and Africa are building capacity through Gulf Cooperation Council investments in private maternity hospitals, while Brazil’s telehealth pilot hints at scalable solutions in South America.

Competitive Landscape

Competition is moderate. Integrated hospital systems such as HCA Healthcare and Ascension bundle prenatal, delivery, and postpartum episodes under one contract and exploit EMR data to automate follow-ups. Digital-native platforms Maven Clinic and Cocoon Postpartum Care pursue employer and direct-to-consumer channels, offering asynchronous chat, on-demand video, and wearable-enabled monitoring. Maven’s 2025 study linked its virtual lactation program to an 18% cut in ER visits for dehydration and jaundice.

Luxury confinement centers differentiate via hospitality-grade amenities. Thomson Medical Group expanded to Kuala Lumpur with a USD 16.3 million acquisition, signifying cross-border appetite for premium recovery experiences. Wearable device firms partner with insurers to monetize remote patient monitoring codes after the FDA cleared postpartum-specific sensors in 2024.

Strategic moves include HCA Healthcare’s rollout of telehealth-integrated programs across 50 hospitals, CloudNine’s mental-health screening at 16 Indian sites, and Ramsay Health Care’s wearable-synced teleconsult platform in Australia. Collectively, the top five organizations captured roughly 46% of global revenue in 2025.

Postpartum Services Industry Leaders

HCA Healthcare

UnityPoint Health

Thomson Medical Group Limited

The Cochin Birthvillage Pvt. Ltd.

Esther Postpartum Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: WellTheory, one of the leading whole-person care platform for autoimmune disease launched its Postpartum Program, a new offering designed to support women navigating the hormonal shifts that often trigger or worsen autoimmune symptoms after giving birth.

- November 2025: Carea, a pregnancy and postnatal wellbeing app that prioritises women’s health launched the Postpartum Mum Tracker to support the 1 in 5 new mothers who face post-birth mental health struggles.

- July 2025: Saint Bella Inc., the company behind the flagship ultra-premium postpartum care brand SAINT BELLA expanded into the United States market. The brand will offer its signature personalized postpartum care services.

Global Postpartum Services Market Report Scope

As per the scope of the report, the postpartum services market focuses on facilities that offer comprehensive care and support to women during the postpartum period, commonly known as the confinement period. These centers provide a range of services to promote the physical and emotional well-being of new mothers and the health and development of their newborns.

The postpartum services market is segmented by type, application, service, and geography. By service, the market is segmented into lactation consultancy, physical therapy, medical treatment, and others. By application, the market is segmented into cesarean section recovery and natural birth recovery. By type, the market is segmented into public centers and private centers. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.

| Lactation Consultancy |

| Physical & Pelvic-Floor Therapy |

| Medical Treatment & Complication Management |

| Diet & Nutrition Counseling |

| Mental-Health & PPD Services |

| Home Visits & Doulas |

| Telehealth Postpartum Care |

| Cesarean-Section Recovery |

| Vaginal Birth Recovery |

| Postpartum Depression & Anxiety Management |

| Breast-Feeding Support |

| Post-Partum Weight Management |

| Public Hospitals & Community Centers |

| Private Maternity Hospitals & Clinics |

| Home-Based Services |

| Online Platforms & Apps |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Lactation Consultancy | |

| Physical & Pelvic-Floor Therapy | ||

| Medical Treatment & Complication Management | ||

| Diet & Nutrition Counseling | ||

| Mental-Health & PPD Services | ||

| Home Visits & Doulas | ||

| Telehealth Postpartum Care | ||

| By Application | Cesarean-Section Recovery | |

| Vaginal Birth Recovery | ||

| Postpartum Depression & Anxiety Management | ||

| Breast-Feeding Support | ||

| Post-Partum Weight Management | ||

| By Facility Type | Public Hospitals & Community Centers | |

| Private Maternity Hospitals & Clinics | ||

| Home-Based Services | ||

| Online Platforms & Apps | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the postpartum services market projected to be by 2031?

It is forecast to reach USD 27.35 billion, expanding at a 10.31% CAGR from 2026 to 2031.

Which application area is recording the fastest revenue growth?

Cesarean-section recovery is advancing at a 12.87% CAGR through 2031, driven by rising surgical deliveries and longer rehabilitation timelines.

Why are telehealth platforms gaining momentum in postpartum care?

Reimbursement-parity laws in 14 U.S. states and FDA-cleared wearables for uterine and cardiac monitoring enable virtual visits that reduce hospital readmissions and fit parents schedules.

What proportion of global revenue did North America generate in 2025?

North America accounted for 41.56% of worldwide postpartum services revenue, supported by Medicaid coverage extensions in 37 states.

How do luxury confinement centers shape demand in Asia-Pacific?

Premium 28-day packages priced around SGD 18,000 (USD 13,300) blend clinical oversight with cultural care rituals, elevating willingness to pay and accelerating regional growth.

What remains the biggest obstacle to scaling home-based postpartum services?

Limited insurance reimbursement—only 18% of U.S. commercial plans cover home nursing visits—combined with shortages of certified doulas and lactation consultants constrains availability.

Page last updated on: