Hysteroscopy Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.69 Billion |

| Market Size (2031) | USD 12.73 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

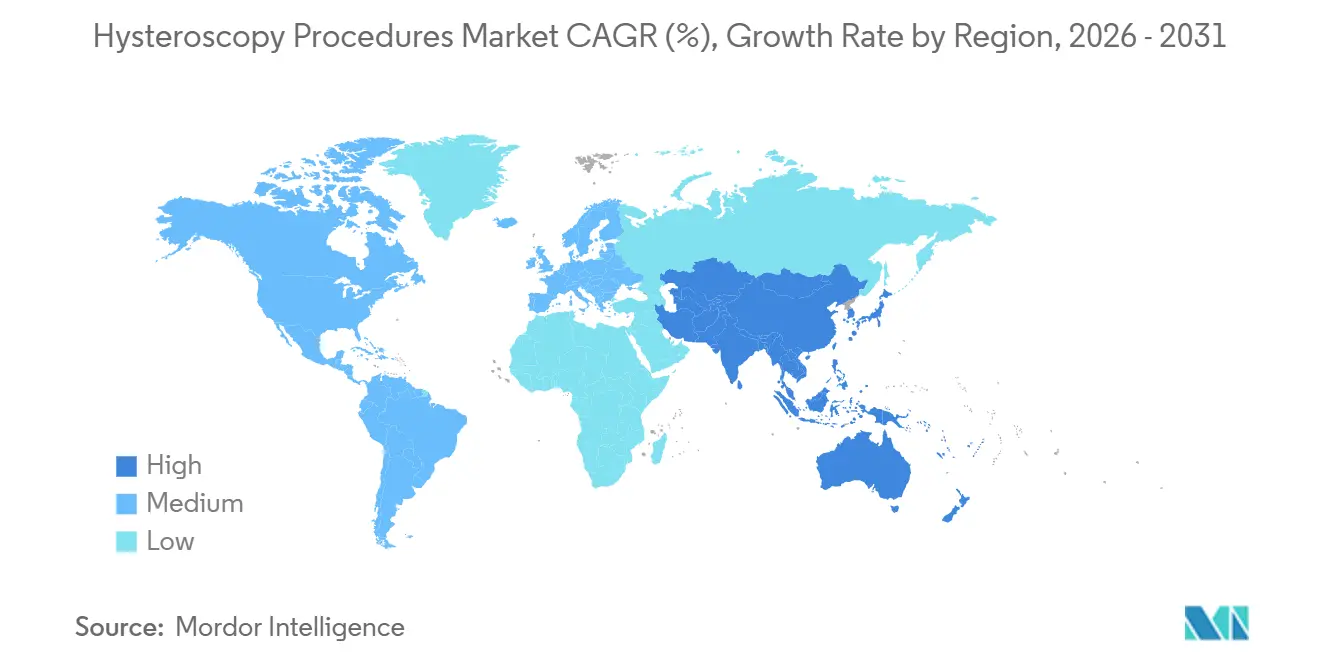

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

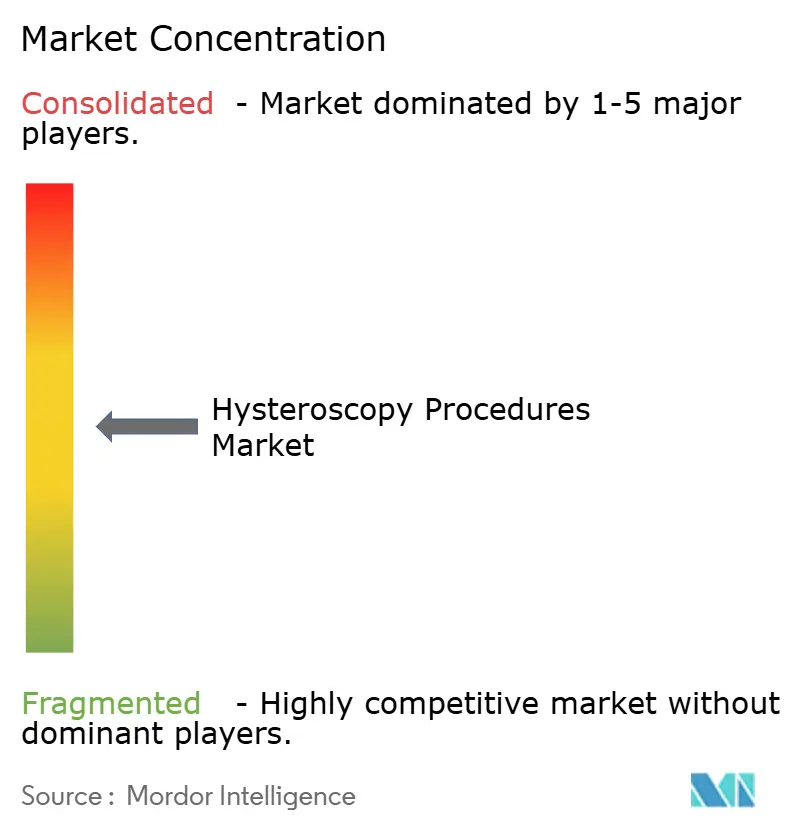

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hysteroscopy Procedures Market Analysis by Mordor Intelligence

The Hysteroscopy Procedures Market size is estimated at USD 10.69 billion in 2026, and is expected to reach USD 12.73 billion by 2031, at a CAGR of 6.25% during the forecast period (2026-2031).

Structural shifts toward outpatient and office settings, accelerating clearance of AI-enabled scopes, and wider reimbursement for single-use devices are lowering per-procedure costs, shortening patient throughput times, and creating a replacement wave for capital equipment. North American payers have already compressed hospital-outpatient fee gaps, while Asia-Pacific governments subsidize fertility services, jointly fueling procedure volumes. OEMs that bundle hysteroscopes, tissue-removal systems, and AI software now capture stickier account relationships, yet pricing pressure persists as single-use challengers undercut reusable towers by 40%. Near-shoring to Mexico and India reduces tariff risk and shortens lead times, though it introduces short-term price swings for distributors.

Key Report Takeaways

- By procedure type, diagnostic hysteroscopy commanded 53.81% of hysteroscopy procedures market share in 2025, and operative hysteroscopy is advancing at a 6.84% CAGR through 2031, outpacing diagnostic growth by 100 basis points.

- By device type, hand-held instruments led with a 41.57% share of the hysteroscopy procedures market in 2025, and resectoscopes and tissue-removal systems are projected to expand at a 7.12% CAGR through 2031.

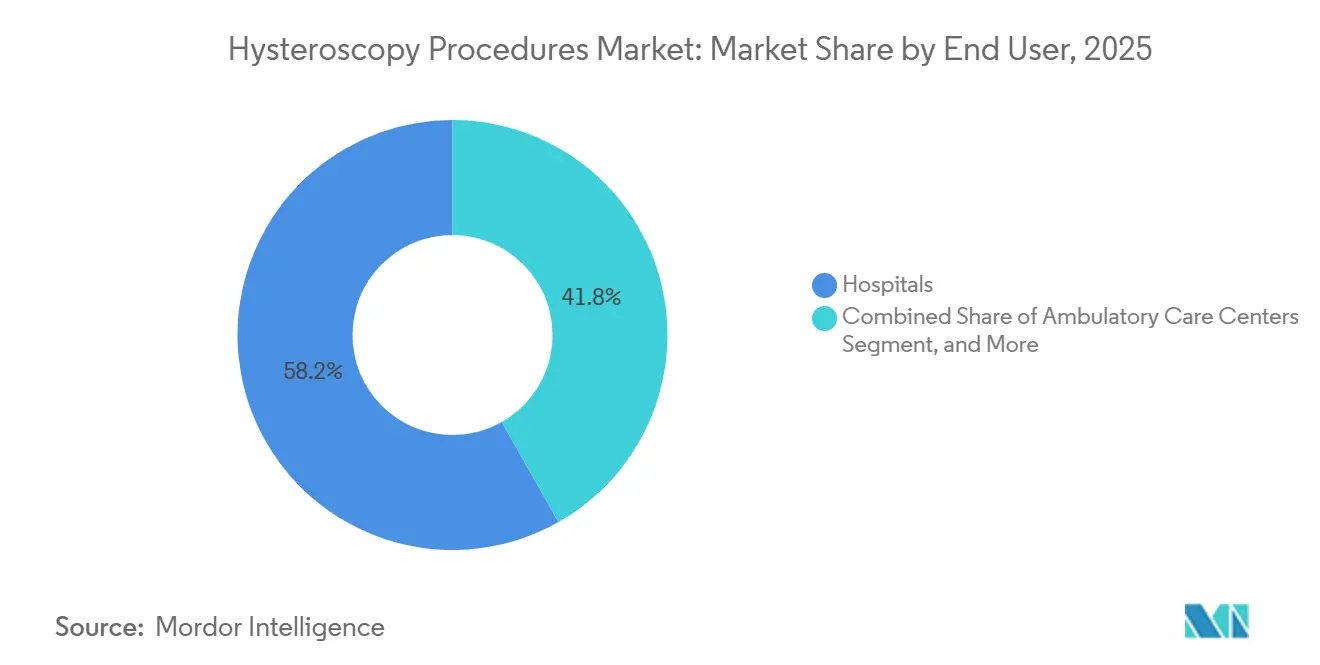

- By end user, hospitals retained 58.22% revenue share in 2025, while ambulatory surgical centers recorded the fastest 8.87% CAGR through 2031.

- By geography, North America accounted for 41.83% of 2025 sales; Asia-Pacific is the highest-growth geography, with a 9.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hysteroscopy Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to outpatient/office-based hysteroscopy | +1.2% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Rising abnormal uterine bleeding & infertility | +1.0% | Global, concentrated in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Single-use devices for infection control | +0.8% | North America, Europe, GCC, South America | Medium term (2-4 years) |

| AI-assisted imaging | +0.6% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Growth of fertility clinics | +1.1% | Asia-Pacific core, plus Middle East and South America | Medium term (2-4 years) |

| Near-shoring of scope manufacturing | +0.5% | North America (Mexico), Asia-Pacific (India, Vietnam) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Outpatient/Office-Based Hysteroscopy

Office hysteroscopy volumes are accelerating because Medicare equalized facility fees between hospital outpatient departments and ambulatory centers in 2024, trimming the cost gap from USD 1,200 to under USD 300 per case.[1]Centers for Medicare & Medicaid Services, “Physician Fee Schedule,” cms.gov Physician groups now retrofit procedure suites with vaginoscopic scopes that avoid cervical dilation, general anesthesia, and overnight stay. The Royal College of Obstetricians and Gynaecologists endorsed office hysteroscopy as first-line care in 2024, citing a 50% reduction in complications compared with operating-room settings. Ambulatory centers bundle ultrasound, biopsy, and hysteroscopy into single-visit pathways, lowering total episode cost by 35% and lifting patient satisfaction. Portable towers leased on three-year contracts defray upfront capital costs of USD 80,000-120,000, catalyzing adoption in suburban and rural markets.

Rising Prevalence of Abnormal Uterine Bleeding & Infertility Evaluations

Abnormal uterine bleeding affects up to 25% of reproductive-age women, with Asia-Pacific prevalence rising due to delayed childbearing and higher PCOS incidence.[2]World Health Organization, “Infertility Fact Sheet,” who.int Hysteroscopy provides real-time visualization and same-session therapy, eliminating the need for separate diagnostic trips. Fertility clinics in China and India expanded capacity by 18% in 2025, supported by subsidies that cover half of ART costs for couples under 40. Hysteroscopic polypectomy and adhesiolysis now form part of standard pre-IVF workups, improving implantation rates by up to 15 percentage points. Middle-Eastern liberalization of infertility insurance raised GCC hysteroscopy volumes by 22% in 2025, while telemedicine triage shaved three weeks from symptom onset to evaluation.

Adoption of Single-Use Devices for Infection Control

FDA warning letters on endoscope reprocessing in 2023 amplified interest in single-use hysteroscopes. CDC’s 2024 guidelines recommend disposables for high-risk patients.[3]Centers for Disease Control and Prevention, “Healthcare Infection Control Practices Advisory Committee,” cdc.gov Hospitals now allot up to 20% of hysteroscopy budgets to single-use scopes despite higher per-unit costs, valuing the sterility and faster turnover. Meditrina’s Aveta system offers a disposable scope with a reusable handle, reducing waste yet retaining infection-control benefits. Ambulatory centers cut room turnover from 45 minutes to under 10, enabling 6-8 cases per day. Germany added a premium for disposables to its DRG schedule in 2025, signaling alignment with reimbursement.

AI-Assisted Imaging Improving Diagnostic Accuracy

Real-time machine-learning models now detect polyps and fibroids with sensitivities above 90%, twelve points higher than unaided inspection. The Olympus VISERA ELITE III platform projects color overlays that flag suspicious tissue, slashing missed lesions by 25% and repeat visits by 15%. FDA cleared four AI-enabled systems during 2024-2025, validating software-as-a-medical-device in gynecology. Early reimbursement pilots in Japan and South Korea may catalyze broader uptake. Professional societies are crafting certification tracks because only 30% of gynecologists currently train on AI outputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced systems | -0.7% | Global, acute in low- and middle-income countries | Medium term (2-4 years) |

| Shortage of trained hysteroscopists | -0.5% | Sub-Saharan Africa, Southeast Asia, rural South America | Long term (≥ 4 years) |

| Waste-management concerns for disposables | -0.3% | Europe, North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Tariff-induced price volatility | -0.4% | North America, Europe, secondary in South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Hysteroscopic Systems

Top-tier towers with 4K imaging, AI modules, and fluid management list between USD 150,000 and USD 250,000, straining budgets outside tertiary centers. Leasing at USD 3,000-5,000 per month eases access but demands predictable cash flow. Refurbished systems sell at 40-60% discounts, yet warranty gaps slow uptake. In low-income regions, ministries allocate funds to primary care, delaying tower replacement by up to 3 years. This concentration funnels complex volumes into urban hospitals and limits market penetration in underserved geographies.

Shortage of Trained Hysteroscopists in Low-Income Regions

Fewer than 20% of obstetrician-gynecologists in Sub-Saharan Africa and Southeast Asia receive formal operative hysteroscopy training. Global fellowships cluster in the United States, Germany, and Japan, leaving emerging markets reliant on short workshops. High-fidelity simulators cost USD 20,000-40,000, curbing adoption. Remote proctoring helps but faces regulatory and liability hurdles. Brain drain intensifies shortages as trained physicians migrate to higher-paying systems. OEM-funded programs reach fewer than 500 clinicians per year, too few to close the skills gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Operative Gains on Therapeutic Demand

Operative procedures captured growing attention as the hysteroscopy procedures market size for treatment-focused cases expanded at 6.84% CAGR through 2031, outpacing diagnostic growth. Diagnostic hysteroscopy still held 35.81% hysteroscopy procedures market share in 2025, acting as the entry point for abnormal uterine bleeding and infertility workups. Surgeons now adopt single-insertion workflows that merge visualization and therapy, trimming anesthesia exposure and cutting facility time by 30%. Fertility clinics routinely perform hysteroscopic polypectomy and adhesiolysis before IVF, boosting implantation success.

Tissue-removal devices such as TruClear Elite and MyoSure allow resection of fibroids up to 4 cm in diameter under monitored fluid balance, reducing the need for conversion to laparoscopy. Handheld diagnostic units like Endosee enable point-of-care visualization in primary offices, compressing the referral cycle. Europe and North America rolled out bundled reimbursement codes that cover both diagnostic and operative sessions, encouraging same-day intervention and further tilting volume toward operative cases.

By Device Type: Resectoscopes Drive Therapeutic Innovation

Hand-held instruments accounted for 41.57% of revenue in 2025, yet resectoscopes and tissue-removal systems grew fastest at a 7.12% CAGR, reflecting surgeons' desire for single-insertion therapy. Bipolar resectoscopes mitigate electrolyte imbalances, while mechanical morcellation avoids thermal injury and supports same-day discharge.

Flexible hysteroscopes with outer diameters below 3 mm enable vaginoscopic entry without anesthesia for 70% of diagnostic cases, broadening the addressable setting. Fluid-management consoles such as Hamou Endomat provide real-time deficit alerts once 1,500 mL is reached, reducing complications. Single-use hand instruments priced at USD 150-300 appeal to ASCs looking to eliminate reprocessing overhead. Combined, these advances strengthen the position of therapeutic devices within the broader hysteroscopy procedures market.

By End User: Ambulatory Centers Capture Outpatient Shift

Hospitals held a 58.22% share in 2025, retaining complex operative cases that require anesthesia and overnight monitoring. However, ambulatory surgical centers are growing at an 8.87% CAGR as payers steer low-acuity volumes to lower-cost sites. Medicare’s site-neutral policy compressed fee gaps, spurring physician investment in office towers.

ASCs now bundle ultrasound, biopsy, and hysteroscopy into single-visit packages that lower episode cost by 35% and raise throughput. Clinics and fertility centers, especially in the Asia-Pacific region, capitalize on government ART subsidies and deliver same-day polypectomy, tightening patient retention. Hospitals continue to manage fibroids larger than 4 cm and high-risk comorbidities but face shared leakage as ASCs upgrade imaging, fluid control, and staffing.

Geography Analysis

North America accounted for 41.83% of 2025 revenue due to site-neutral reimbursement, which equalized payments and accelerated migration to ASCs. The United States accounts for 85% of regional spend due to high procedure rates and rapid adoption of single-use scopes. Canada’s provincial payers now reimburse office hysteroscopy, halving wait times in Ontario and British Columbia. Mexican plants assembled by Karl Storz and Olympus are expected to expand by 30% by 2027 under USMCA, trimming lead times and shielding against tariffs.

Asia-Pacific grows fastest at 9.39% through 2031, driven by Chinese and Indian fertility subsidies that lifted clinic registrations 18% in 2025. China now reimburses hysteroscopy within ART bundles, shaving patient costs by 40% and raising volumes by 12% annually. India’s ART Act mandates hysteroscopic evaluation for recurrent implantation failure. Japan and South Korea pilot reimbursement for AI-assisted procedures, while Australia’s private insurers drop co-pays by 25%, boosting volumes. Tele-proctored training narrows the skills gap in Southeast Asia, though formal fellowship capacity remains limited.

Europe posts steady growth as national health services favor outpatient care and disposables following the FDA warning letter on reprocessing. Germany pays a single-use premium in its DRG scheme, while the U.K. endorses office hysteroscopy as first-line, citing 50% fewer complications. France and Italy invest in regional fertility networks as birth rates fall. South America sees 15% volume growth after Brazil and Argentina liberalize infertility coverage, although capital shortages slow rural expansion. Middle Eastern investment in fertility platforms reflects confidence in long-term demand.

Competitive Landscape

The top five OEMs, Hologic, Medtronic, Karl Storz, Olympus, and Boston Scientific, command significant global revenue, yet emerging single-use suppliers disrupt on price and speed. Hologic acquired Gynesonics for USD 350 million in 2025, integrating radiofrequency fibroid ablation into its uterine health suite. Karl Storz acquired Asensus Surgical in 2024 to gain robotic IP and position for future robotic hysteroscopy.

Meditrina and UroViu offer FDA-cleared disposable scopes at 40% lower cost than reusable towers, attracting ASCs focused on infection control. CooperSurgical expanded its disposable range by buying obp Surgical in 2024. Fluid-management innovation from LiNA Medical and Maxer Endoscopy undercuts incumbents by 30% while adding automated pressure sensors. AI-enabled imaging pipelines deliver four new 510(k) clearances annually, but clinician training remains scarce, tempering immediate revenues.

White-space opportunity centers on office hysteroscopy units priced below USD 10,000, which allow primary care expansion. Boston Scientific, Smith & Nephew, and Richard Wolf invest in compact towers to address that frontier. Capital replacement cycles average 7-10 years, implying peak upgrade demand from analog systems purchased before 2020.

Hysteroscopy Procedures Industry Leaders

B. Braun Melsungen AG

Boston Scientific Corporation

CooperSurgical Inc.

Medtronic

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Blackstone and TPG agreed to acquire Hologic for USD 18.3 billion, aiming to scale AI imaging launches.

- October 2025: Medtronic began an IDE study of its Hugo robotic system for hysteroscopic myomectomy across five U.S. sites.

- January 2025: Hologic closed its USD 350 million purchase of Gynesonics, adding the Sonata fibroid ablation system.

- April 2024: Karl Storz completed its USD 0.35-per-share acquisition of Asensus Surgical, adding Senhance robotics.

- April 2024: CooperSurgical bought obp Surgical, enlarging its single-use instrument catalog.

Global Hysteroscopy Procedures Market Report Scope

The Hysteroscopy Procedures Market Report is Segmented by Procedure Type (Diagnostic, Operative), Device Type (Hysteroscopes, Hand-held Instruments, Resectoscopes & Tissue-Removal Systems, Fluid Management Systems & Accessories), End User (Hospitals, Ambulatory Surgical Centers, Clinics & Fertility Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Diagnostic |

| Operative |

| Hysteroscopes |

| Hand-held Instruments |

| Resectoscopes & Tissue-Removal Systems |

| Fluid Management Systems & Accessories |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics & Fertility Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Diagnostic | |

| Operative | ||

| By Device Type | Hysteroscopes | |

| Hand-held Instruments | ||

| Resectoscopes & Tissue-Removal Systems | ||

| Fluid Management Systems & Accessories | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics & Fertility Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hysteroscopy procedures market?

The hysteroscopy procedures market size reached USD 10.69 billion in 2026 and is forecast to rise to USD 12.73 billion by 2031.

Which procedure type is growing fastest?

Operative hysteroscopy is expanding at a 6.84% CAGR through 2031 as single-insertion workflows combine diagnosis and treatment.

Why are ambulatory surgical centers gaining share?

Medicare’s site-neutral payment cut has closed facility fee gaps, so ASCs deliver lower-cost hysteroscopy bundled with ultrasound and biopsy in a single visit.

How do single-use scopes affect adoption?

Disposable hysteroscopes remove reprocessing risk, cut turnover times to under 10 minutes, and now account for up to 20% of facility budgets.

Which region shows the highest growth rate?

Asia-Pacific posts the fastest CAGR of 9.39%, supported by government subsidies for fertility treatments in China and India.

Page last updated on: