Fertility Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 39.88 Billion |

| Market Size (2030) | USD 63.36 Billion |

| Growth Rate (2025 - 2030) | 9.70% CAGR |

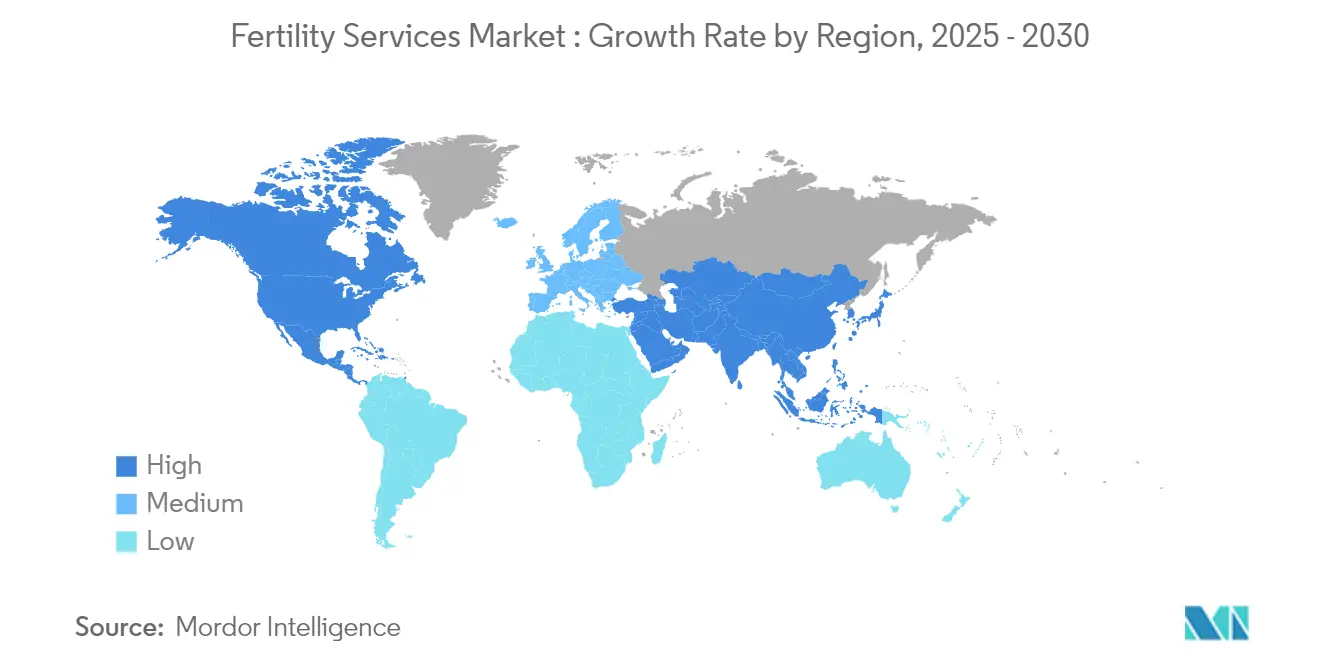

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

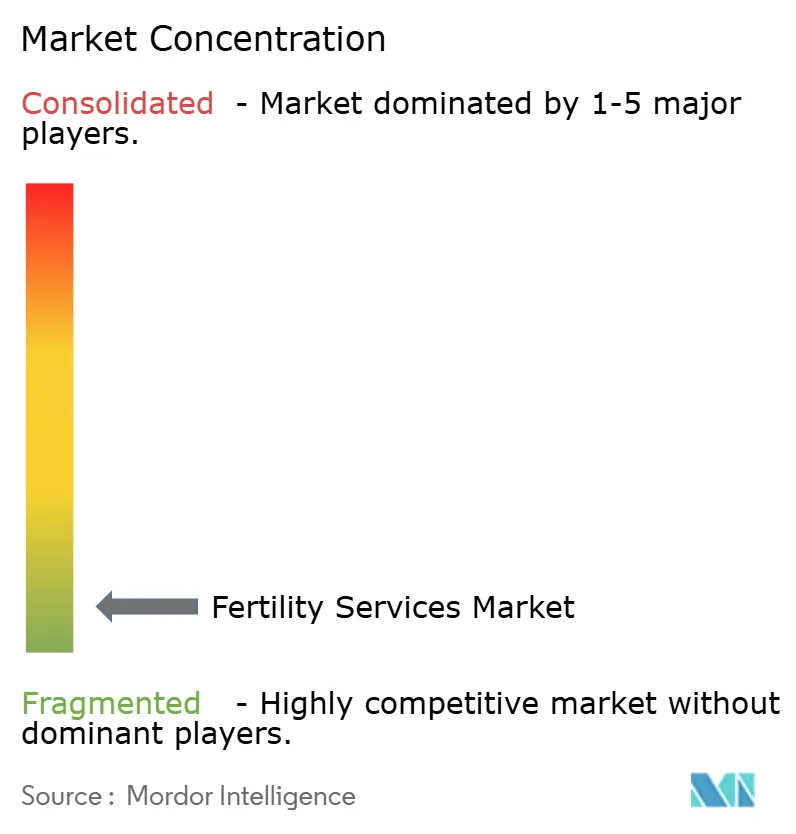

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fertility Services Market Analysis by Mordor Intelligence

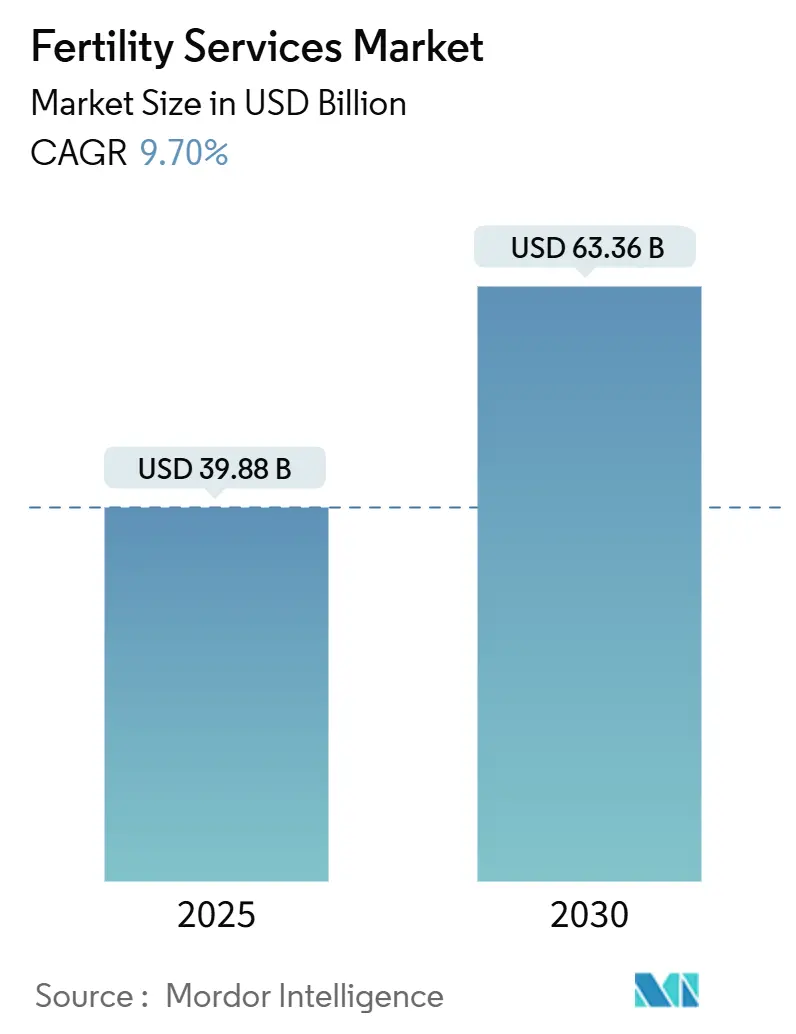

The Fertility Services Market size is estimated at USD 39.88 billion in 2025, and is expected to reach USD 63.36 billion by 2030, at a CAGR of 9.70% during the forecast period (2025-2030).

Fertility Services Market Overview

The fertility services industry is experiencing significant transformation driven by changing societal norms and demographic shifts. The increasing trend of delayed parenthood, particularly in developed nations, has created a substantial demand for reproductive assistance. According to the World Health Organization's latest estimates in 2023, approximately 17.5% of couples globally experience fertility challenges, highlighting the growing need for specialized reproductive services. The industry has also witnessed a notable shift in consumer demographics, with more single parents and LGBTQ+ individuals seeking fertility treatments. This evolving patient profile has prompted fertility clinics to expand their service offerings and adopt more inclusive treatment approaches.

The market is witnessing significant growth driven by rapid technological advancements and innovations in treatment methodologies. In May 2023, Oma Fertility expanded its operations by launching three new clinics equipped with artificial intelligence and robotics in their laboratories, while maintaining a focus on human-centered care. The company introduced its AI-powered microscope system, Oma Sperm InSight, which enables embryologists to analyze twenty to thirty times more sperm cells compared to conventional methods, thereby optimizing the selection process. The adoption of such advanced technologies has led to substantial improvements in success rates and treatment outcomes, enhancing the overall attractiveness of fertility services to potential patients.

Strategic consolidation and international expansion have become prominent features of the fertility services landscape. In January 2024, Indira IVF, one of the leading fertility clinic networks, marked its first international venture by opening a hospital in Kathmandu, Nepal, with plans to expand into Southeast Asian, European, Middle Eastern, and African markets. This expansion trend is complemented by increasing cross-border fertility tourism, as patients seek cost-effective treatment options in different countries. The industry has also witnessed a surge in strategic partnerships, with fertility clinics collaborating with biotechnology companies to enhance their technological capabilities and service offerings.

Fertility preservation services, especially egg freezing, have surged in popularity, driven by evolving lifestyle choices and heightened awareness of reproductive options. Data from Kindbody, a prominent fertility group, highlights a 50% jump in egg-freezing cycles from April 2023 to April 2024, marking a significant rise compared to prior years. This uptick has spurred the establishment of specialized clinics and programs, tailored for those aiming to safeguard their reproductive choices for future family planning. Furthermore, the industry is amplifying its focus on patient education and support, with clinics rolling out holistic programs that encompass both the medical and emotional facets of fertility treatments.

Global Fertility Services Market Trends and Insights

Increase in Infertility Rates Across the Globe

Infertility has become a critical global health issue with significant implications for healthcare systems and related industries. In 2023, the World Health Organization (WHO) reported that the Western Pacific Region experienced the highest lifetime infertility prevalence at 23.2%. High-income countries recorded a prevalence rate of 17.8%, while low- and middle-income countries reported a rate of 16.5%. This upward trend is driven by factors such as delayed parenthood decisions, environmental influences, and lifestyle changes. The increasing prevalence of conditions like Polycystic Ovary Syndrome (PCOS) has further exacerbated fertility challenges. In 2023, the global prevalence of PCOS was estimated at 6.3% based on international guidelines, while the Rotterdam criteria, which include Polycystic Ovarian Morphology (PCOM), indicated a higher prevalence of 9.8%. Additionally, male infertility factors, including declining sperm quality and count due to exposure to environmental toxins, stress, and lifestyle choices, have become increasingly significant in recent years.

The influence of modern lifestyle choices on fertility rates has become more evident, with factors such as rising stress levels, obesity, smoking, and alcohol consumption playing pivotal roles. Recent studies have highlighted that occupational exposure to specific chemicals and electromagnetic radiation has also contributed to declining fertility rates among working professionals. Furthermore, the trend of delaying marriages and pregnancies, particularly in developed economies, has led to age-related fertility challenges, driving many couples to seek medical assistance when natural conception becomes more difficult.

Advancements in Assisted Reproductive Technology (ART)

Technological advancements in Assisted Reproductive Technology (ART) have significantly transformed fertility treatments, driving improvements in success rates and expanding treatment options. In January 2025, research funded by the National Institute for Health and Care Research (NIHR) highlighted the potential of artificial intelligence (AI) to enhance the success rates of in-vitro fertilisation (IVF) procedures. The study emphasized AI's ability to accurately determine the optimal timing for targeting follicles small ovarian sacs that house eggs thereby increasing the probability of successful IVF outcomes. Additionally, advanced genetic screening techniques, such as Preimplantation Genetic Testing (PGT), have facilitated more precise identification of viable embryos while reducing the risk of genetic disorders. These innovations have improved the efficiency and accessibility of fertility treatments, simultaneously mitigating the emotional and financial challenges faced by patients.

The emergence of new laboratory techniques and equipment has also contributed to better preservation of genetic material and improved fertilization outcomes. Time-lapse imaging systems now allow continuous monitoring of embryo development without disturbing the culture environment, leading to better selection of viable embryos. Additionally, advances in cryopreservation techniques have significantly improved the viability of frozen eggs and embryos, providing more flexibility in fertility treatment timing and increasing the overall success rates of fertility procedures. The development of automated systems for embryo handling and culture has also reduced human error and improved standardization in laboratory procedures.

Rising Awareness about Reproductive Health

The increasing awareness about reproductive health has been driven by comprehensive educational initiatives and advocacy programs implemented by healthcare organizations and fertility specialists. In September 2023, a survey conducted by the Pew Research Center (PRC) highlighted that the increasing average age of first-time mothers in the United States has driven a rise in the adoption of fertility treatments. The percentage of adults utilizing these treatments has grown to 42%, compared to 33% recorded five years ago. Social media platforms and digital health resources have played a crucial role in disseminating information about fertility treatments and reproductive health, breaking down stigmas and encouraging open discussions about infertility. Healthcare providers have also expanded their educational outreach programs, offering workshops, webinars, and counseling services to help individuals make informed decisions about their reproductive health.

The shift in societal attitudes towards fertility treatments has been accompanied by improved access to information about various treatment options and success rates. Fertility clinics and healthcare providers have adopted transparent communication strategies, providing detailed information about treatment protocols, success rates, and potential risks. Support groups and online communities have emerged as valuable resources for individuals seeking emotional support and practical advice during their fertility journey. Additionally, workplace policies have evolved to accommodate fertility treatments, with many organizations now offering fertility benefits and flexible scheduling options for employees undergoing treatment.

Integration of Telemedicine in Fertility Services

The adoption of telemedicine in fertility services is revolutionizing the delivery of reproductive healthcare. For instance, in January 2025, Reproductive Medicine Associates (RMA) of New York, a prominent provider in the field, announced a strategic partnership with Conceive, a leading 24/7 fertility support platform. This collaboration aims to enhance the patient experience at RMA's locations in Manhattan, Brooklyn, and Westchester. The partnership reflects RMA of New York's strategic focus on reducing the emotional challenges associated with fertility treatments while driving improved patient outcomes. Virtual consultations have expanded the accessibility of fertility services, accommodating patients in remote areas and those with demanding schedules. Additionally, digital health platforms enable continuous monitoring and support throughout the treatment process. The integration of mobile applications and patient portals has streamlined communication between healthcare providers and patients, offering real-time tracking of treatment progress and medication schedules. These technological advancements have significantly reduced the time and travel requirements traditionally associated with fertility treatments.

The expansion of telemedicine services has also facilitated better coordination between different healthcare providers involved in fertility treatments. Digital platforms now enable seamless sharing of medical records, test results, and treatment plans among specialists, leading to more coordinated and efficient care delivery. Remote monitoring capabilities have allowed healthcare providers to track patients' responses to medications and adjust treatment protocols promptly. Furthermore, the integration of artificial intelligence in telemedicine platforms has enabled more personalized treatment approaches, with algorithms analyzing patient data to optimize treatment timing and medication dosages. This technological integration has not only improved treatment outcomes but also enhanced the overall patient experience in fertility care.

Fertility Services Market Procedures Segment Analysis

In-Vitro Fertilization (IVF) Segment in Fertility Services Market

In-vitro fertilization (IVF) maintains its position as the dominant segment in the fertility services market, commanding approximately 45% of the market share in 2024. This substantial market presence is attributed to the procedure's high success rates and continuous technological improvements in embryo cultivation and genetic testing capabilities. The segment's strength is further reinforced by increasing insurance coverage for IVF procedures in developed nations and the rising adoption of preimplantation genetic testing. The integration of artificial intelligence in embryo selection has significantly enhanced success rates, making IVF the preferred choice among healthcare providers and patients. Additionally, the growing trend of delayed parenthood in urban populations has sustained the demand for IVF services. The segment's robust performance is also supported by the establishment of specialized IVF centers and the increasing number of trained fertility specialists worldwide.

Surrogacy Segment in Fertility Services Market

The surrogacy segment is emerging as a high-growth category within the fertility services market. This growth is primarily driven by the increasing acceptance of gestational surrogacy arrangements and the expansion of legal frameworks in various countries. The segment's acceleration is particularly notable in developing nations where favorable regulations and cost-effective services are attracting international patients. Technological advancements in embryo transfer techniques and improved success rates have bolstered confidence in surrogacy arrangements. The rise of cross-border surrogacy services, coupled with growing support networks and agencies, has created a more structured and accessible market. Furthermore, the increasing recognition of surrogacy rights for same-sex couples and single parents has opened new market opportunities. The segment's growth is also supported by improved medical infrastructure and standardization of surrogacy protocols across major fertility centers.

Fertility Services Market Services Segment Analysis

Non-Donor Services Segment in Fertility Services Market

The non-donor services segment has emerged as the dominant force in the global fertility services market. This substantial market position is primarily attributed to the increasing preference for treatments using patients' own genetic material, which often aligns with personal and cultural preferences. The segment's prominence is further strengthened by extensive insurance coverage in developed nations and the growing integration of advanced reproductive technologies. Additionally, the segment has benefited from continuous technological advancements in fertility preservation techniques and genetic testing capabilities. The expansion of fertility clinic networks and the standardization of treatment protocols have also played crucial roles in maintaining this segment's market leadership. Moreover, the increasing success rates of non-donor procedures and improved patient awareness have reinforced its dominant position in the global market.

Donor Services Segment in Fertility Services Market

The donor services segment is projected to exhibit a significant growth rate in the fertility services market. This accelerated growth is driven by several factors, including the increasing acceptance of donor-assisted reproduction across various cultural contexts and the expanding legal framework supporting donor services globally. The segment is experiencing substantial momentum due to the rising demand from same-sex couples and single parents seeking fertility solutions. Technological advancements in donor screening processes and improved success rates have significantly enhanced the appeal of donor services. The segment's growth is further propelled by the development of comprehensive donor databases and the implementation of stringent quality control measures. Additionally, the increasing availability of international donor programs and cross-border fertility services has created new growth opportunities. The integration of genetic testing and counseling services has also contributed to the segment's rapid expansion, making it increasingly attractive to prospective parents seeking fertility solutions.

Fertility Services Market Service Provider Segment Analysis

Fertility Clinics Segment in Fertility Service Market

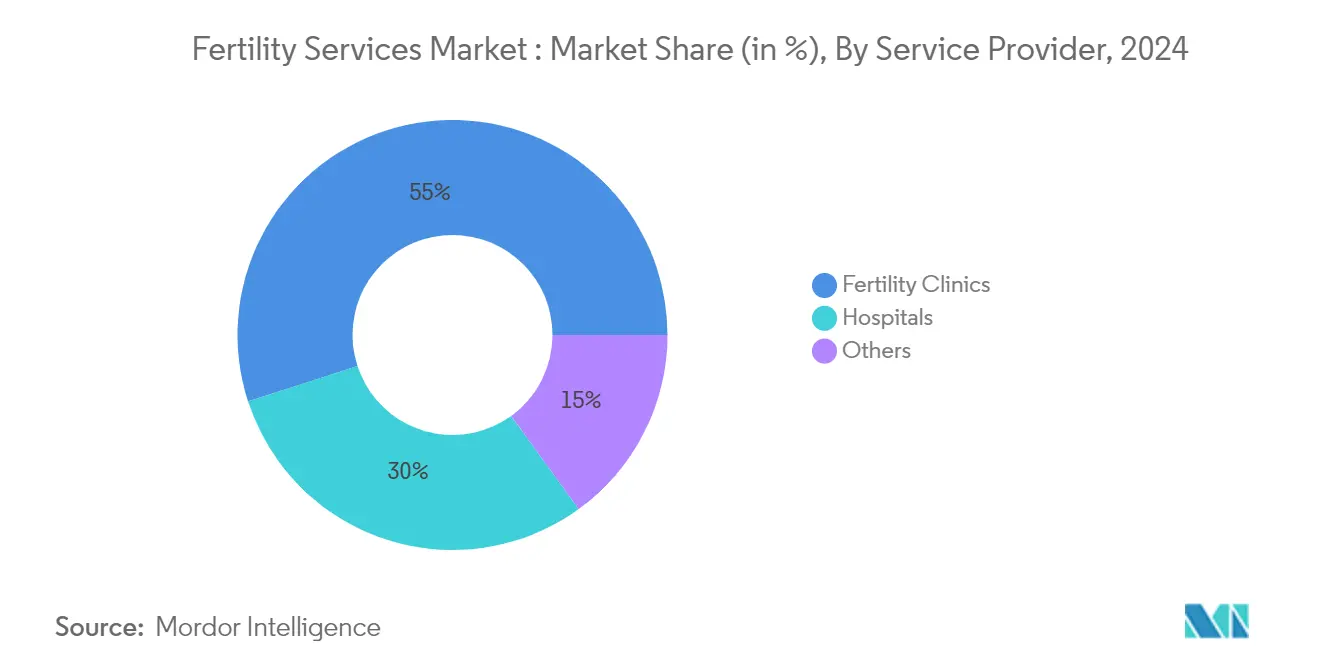

Fertility clinics have emerged as the dominant segment in the fertility services market, commanding approximately 55% of the market share in 2024. This substantial market position is attributed to their specialized focus on reproductive treatments and comprehensive fertility solutions. These dedicated facilities offer state-of-the-art equipment, specialized expertise, and personalized care protocols specifically designed for fertility treatments. The segment's prominence is further strengthened by the increasing number of standalone fertility centers worldwide, particularly in developed regions. Modern fertility clinics are incorporating advanced technologies such as time-lapse imaging, genetic testing capabilities, and automated systems for embryo handling. The preference for fertility clinics is also driven by their higher success rates, specialized staff training, and ability to offer both standard and complex fertility treatments under one roof. Additionally, many fertility clinics have established strong partnerships with sperm and egg banks, enhancing their service offerings and market position.

Hospitals Segment in Fertility Services Market

The hospitals segment is projected to experience the highest growth rate in the fertility services market, with an estimated CAGR of 11% from 2025 to 2030. This accelerated growth is primarily driven by the increasing integration of fertility departments within major hospital networks, offering patients the advantage of comprehensive medical support and emergency care facilities. Hospitals are rapidly expanding their fertility services through investments in advanced reproductive technologies and specialized fertility units. The segment's growth is further propelled by the rising trend of medical tourism for fertility treatments, with hospitals offering package deals that include accommodation and post-procedure care. The availability of insurance coverage for fertility treatments in hospital settings is also contributing to this growth trajectory. Moreover, hospitals are increasingly partnering with fertility specialists and establishing centers of excellence for reproductive medicine, enhancing their competitive position in the market. The segment is also benefiting from the growing preference for one-stop healthcare solutions among patients seeking fertility treatments.

Fertility Services Market Geography Segment Analysis

Fertility Services Market in North America

The North American fertility services market demonstrates robust growth driven by advanced healthcare infrastructure, high awareness levels, and increasing adoption of assisted reproductive technologies. The United States, Canada, and Mexico comprise the key markets in this region, with factors such as delayed pregnancies, rising infertility rates, and supportive insurance coverage contributing to market expansion. The presence of major fertility clinics, technological advancements in IVF procedures, and growing acceptance of fertility treatments further strengthen the regional market landscape.

Fertility Services Market in United States

The United States dominates the North American fertility services market, holding approximately 85% of the regional market share in 2024. The country's leadership position is attributed to its advanced healthcare system, presence of leading fertility clinics, and comprehensive fertility treatment options. The growing trend of delayed parenthood, increasing prevalence of infertility among both men and women and rising awareness about fertility preservation options drive market growth. Additionally, the integration of artificial intelligence and robotics in fertility treatments, exemplified by innovations like Oma Fertility's AI-driven sperm selection technology, showcases the market's technological advancement.

Fertility Services Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 8% from 2025 to 2030. The Canadian market is witnessing rapid expansion due to increasing health consciousness among consumers and growing awareness about preventive healthcare. The country's robust healthcare system and supportive regulatory environment have created favorable conditions for market growth. Canadian consumers are increasingly embracing natural and herbal supplements, driving demand for brain health products. The market is further strengthened by growing research activities, an increasing elderly population, and a rising focus on mental wellness among younger demographics.

Fertility Services Market in Europe

The European fertility services market showcases significant development with comprehensive coverage across Germany, France, United Kingdom, Italy, and Spain. The region benefits from advanced healthcare infrastructure, supportive regulatory frameworks, and increasing public awareness about fertility treatments. The European market is characterized by high-quality healthcare standards, innovative treatment approaches, and growing medical tourism for fertility services. The integration of cutting-edge technologies and personalized treatment protocols further enhances the region's market position.

Fertility Services Market in Germany

Germany leads the European fertility services market, commanding approximately 25% of the regional market share in 2024. The country's market leadership is supported by its robust healthcare infrastructure, advanced medical technology adoption, and comprehensive insurance coverage for fertility treatments. German fertility clinics are renowned for their high success rates, stringent quality standards, and innovative treatment approaches. The country's strong focus on research and development in reproductive medicine continues to drive market growth.

Fertility Services Market in United Kingdom

The United Kingdom demonstrates remarkable growth potential with an expected CAGR of approximately 8.5% from 2025-2030. The market's rapid expansion is driven by increasing private sector investments, growing awareness about fertility preservation options, and technological advancements in assisted reproductive technologies. The UK's fertility sector benefits from strong regulatory oversight, high-quality clinical practices, and increasing acceptance of various fertility treatment options. The country's focus on patient care excellence and continuous improvement in success rates contributes to its accelerated growth trajectory.

Fertility Services Market in Asia-Pacific

The Asia-Pacific fertility services market exhibits dynamic growth potential across China, Japan, India, and Australia. The region's market expansion is driven by improving healthcare infrastructure, rising disposable income, and growing awareness about fertility treatments. The increasing prevalence of infertility, coupled with changing lifestyle factors and delayed marriages, contributes to market growth. The region also benefits from medical tourism, technological advancements, and increasing accessibility to fertility treatments.

Fertility Services Market in China

China emerges as the dominant force in the Asia-Pacific fertility services market. The country's market leadership is attributed to its large population base, growing middle-class demographics, and increasing acceptance of assisted reproductive technologies. The Chinese market benefits from continuous improvements in healthcare infrastructure, rising investments in fertility clinics, and growing awareness about reproductive health. The government's supportive policies and increasing private sector participation further strengthen China's market position.

Fertility Services Market in India

India represents the fastest-growing market in the Asia-Pacific region. The country's rapid market expansion is driven by increasing awareness about fertility treatments, growing healthcare infrastructure, and rising disposable income. India's competitive advantage in medical tourism, coupled with the presence of skilled healthcare professionals and cost-effective treatment options, contributes to its growth momentum. The country's fertility services sector benefits from technological advancements and increasing acceptance of assisted reproductive technologies.

Fertility Services Market in the Middle East and Africa

The Middle East & Africa fertility services market, with key contributions from South Africa and the United Arab Emirates, shows promising growth prospects. The region's market development is characterized by increasing healthcare investments, growing awareness about fertility treatments, and rising medical tourism. The United Arab Emirates leads the regional market in terms of size, while South Africa demonstrates the fastest growth potential. The region's market expansion is supported by improving healthcare infrastructure, technological advancements, and increasing acceptance of assisted reproductive technologies.

Fertility Services Market in South America

South America fertility services market, primarily represented by Brazil and Argentina, demonstrates steady growth potential. The region's market development is supported by improving healthcare infrastructure, rising awareness about fertility treatments, and increasing accessibility to assisted reproductive technologies. Brazil emerges as the largest market in the region, while Argentina shows the fastest growth potential. The region's market expansion is further driven by medical tourism, technological advancements, and growing acceptance of fertility treatments among the population.

Competitive Landscape

Top Companies in the Fertility Services Market

The global fertility services market is led by key players including PFCLA, Mayo Foundation for Medical Education and Research (MFMER), Cleveland Clinic, Apricity Fertility UK Limited, King’s Fertility Limited, Dallas IVF, Midwest Fertility Specialists, Europe IVF, Care Fertility, Aspire Fertility, Virtus Health, Monash IVF Group. These companies are driving market growth through continuous product innovation, particularly in assisted reproductive technologies (ART) and genetic testing capabilities. The industry has witnessed significant strategic partnerships and collaborations aimed at expanding its geographical presence and enhancing service portfolios. Market leaders are increasingly focusing on technological integration, including AI-powered embryo selection and digital health platforms, while also expanding their clinic networks through both organic growth and acquisitions. Operational excellence initiatives have centered on standardizing protocols across clinic networks, improving success rates, and enhancing patient experience through personalized care approaches.

Market Structure Shows Growing Consolidation Trend

The fertility services market exhibits a hybrid competitive structure with both global conglomerates and specialized regional providers maintaining significant market presence. Large multinational healthcare companies have established dominant positions through extensive clinic networks and comprehensive service offerings, while specialized fertility clinics maintain a strong regional presence through deep local market knowledge and personalized care approaches. The market is experiencing accelerated consolidation as larger players acquire regional clinics to expand their geographical footprint and service capabilities.

The industry landscape is characterized by varying levels of vertical integration, with some players maintaining complete control over the entire treatment process while others focus on specific segments of the value chain. Market leaders are increasingly pursuing strategic partnerships with genetic testing laboratories, sperm banks, and technology providers to enhance their service offerings. Cross-border expansion strategies have become more prevalent, particularly in regions with favorable regulatory environments and growing demand for fertility services. The competitive dynamics are further shaped by the emergence of fertility-focused healthcare groups that combine medical expertise with modern management practices.

Innovation and Patient Care Drive Success

Success in the fertility services market increasingly depends on providers' ability to combine clinical excellence with technological innovation while maintaining cost-effectiveness. Established players are strengthening their market positions by investing in advanced laboratory equipment, expanding their range of treatment options, and developing proprietary technologies for improved success rates. Market leaders are also focusing on building strong brand recognition through quality certifications, transparent success rate reporting, and comprehensive patient support programs. The ability to attract and retain skilled fertility specialists while maintaining strong relationships with referring physicians has become crucial for sustainable growth.

Future competitive advantage will increasingly rely on providers' ability to adapt to changing patient preferences and regulatory requirements while maintaining operational efficiency. Success factors include the development of patient-centric care models, integration of digital health solutions, and establishment of robust quality management systems. Market participants must also address the growing importance of value-based care models and increasing patient demand for transparent pricing and success rates. The ability to navigate complex regulatory environments while maintaining high clinical standards will become increasingly important as markets mature and oversight increases. Providers who can effectively balance these factors while maintaining strong financial performance will be best positioned for long-term success.

Fertility Services Industry Leaders

Monash IVF Group

Virtus Health

Aspire Fertility

Europe IVF

Care Fertility

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cigna Healthcare, the health benefits division of The Cigna Group partnered with Progyny, Inc. to deliver advanced fertility and family-building solutions to a wider range of employers. This initiative enables employers to provide comprehensive coverage across the entire fertility process, from pre-conception planning to postpartum care, while also offering options for family-building services, including surrogacy and adoption.

- January 2025: NewGenIvf Group has introduced a groundbreaking lifetime egg freezing service in Asia. Dubbed the 'one charge, no worries' solution, it promises hassle-free fertility preservation. With this service, customers can pay once and enjoy unlimited egg storage duration. The initiative primarily targets working women and professionals who desire greater reproductive flexibility.

- October 2024: Ontario's health and finance ministers announced a USD 150 million allocation over the next two years to enhance access to fertility services in Canada. Finance Minister Peter Bethlenfalvy stated that this funding increase for the Ontario Fertility Program will expand eligibility for government-funded in vitro fertilization (IVF) to three times more individuals.

- August 2024: Aetna, a United States-based insurer, expanded access to fertility services by including intrauterine insemination (IUI) as a covered medical benefit across all eligible plans. This initiative demonstrated Aetna's dedication to promoting equity in family-building options for individuals from diverse backgrounds.

Global Fertility Services Market Report Scope

As per the scope of the report, fertility services encompass a range of medical treatments and procedures designed to help individuals and couples conceive and address infertility challenges. These services are typically provided by fertility clinics, hospitals, and specialized reproductive centers, supporting patients with medical, emotional, and ethical considerations throughout their journey to parenthood.

The fertility services market is segmented into procedures, services, service providers, and geography. By procedures, the market is segmented as in-vitro fertilization (IVF), artificial insemination, surrogacy, and others. By service, the market is segmented as donor services and non-donor services. By donor services, the market is further segmented as fresh donor services and frozen donor services. By non-donor services, the market is segmented as as fresh non-donor services and frozen non-donor services. By service provider, the market is segmented as fertility clinics, hospitals, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions, globally. The report offers the value (in USD) for the above-mentioned segments.

| In-Vitro Fertilization (IVF) |

| Artificial Insemination |

| Surrogacy |

| Others |

| Donor Services | Fresh Donor Services |

| Frozen Donor Services | |

| Non-Donor Services | Fresh Non-Donor Services |

| Frozen Non-Donor Services |

| Fertility Clinics |

| Hospitals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedures | In-Vitro Fertilization (IVF) | |

| Artificial Insemination | ||

| Surrogacy | ||

| Others | ||

| By Services | Donor Services | Fresh Donor Services |

| Frozen Donor Services | ||

| Non-Donor Services | Fresh Non-Donor Services | |

| Frozen Non-Donor Services | ||

| By Service Provider | Fertility Clinics | |

| Hospitals | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Fertility Services Market?

The Fertility Services Market size is expected to reach USD 39.88 billion in 2025 and grow at a CAGR of 9.70% to reach USD 63.36 billion by 2030.

What is the current Fertility Services Market size?

In 2025, the Fertility Services Market size is expected to reach USD 39.88 billion.

Which is the fastest growing region in Fertility Services Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Fertility Services Market?

In 2025, the North America accounts for the largest market share in Fertility Services Market.

What years does this Fertility Services Market cover, and what was the market size in 2024?

In 2024, the Fertility Services Market size was estimated at USD 36.01 billion. The report covers the Fertility Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Fertility Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: