Fertility Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

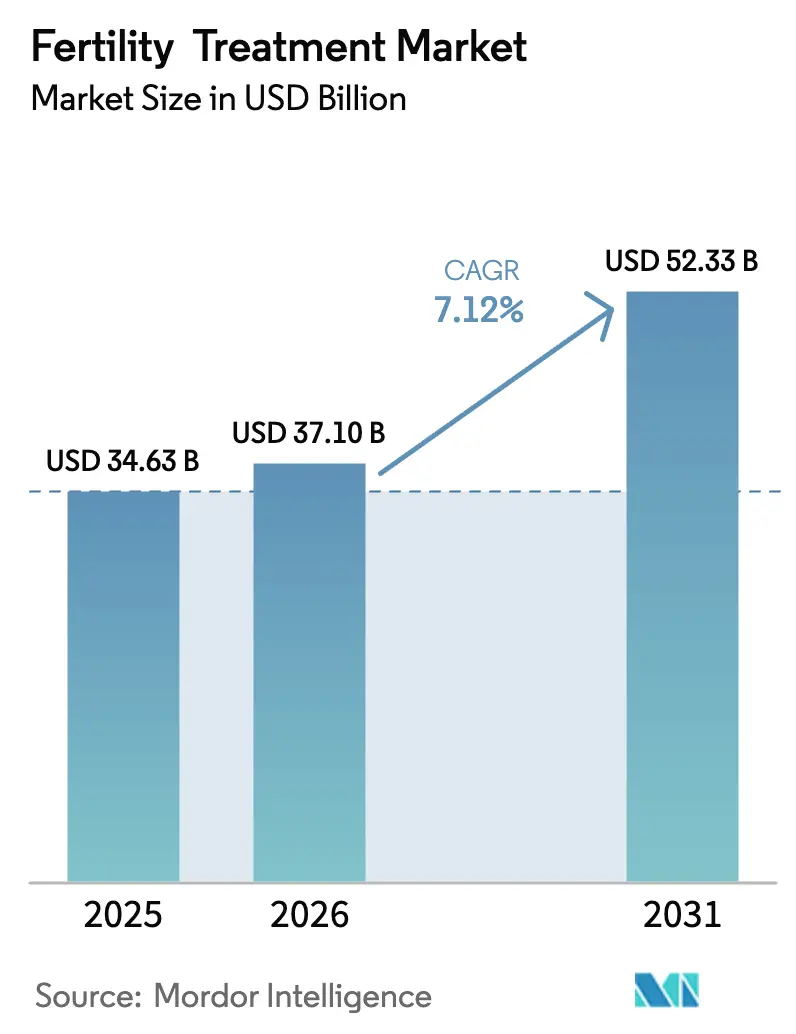

| Market Size (2026) | USD 37.10 Billion |

| Market Size (2031) | USD 52.33 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

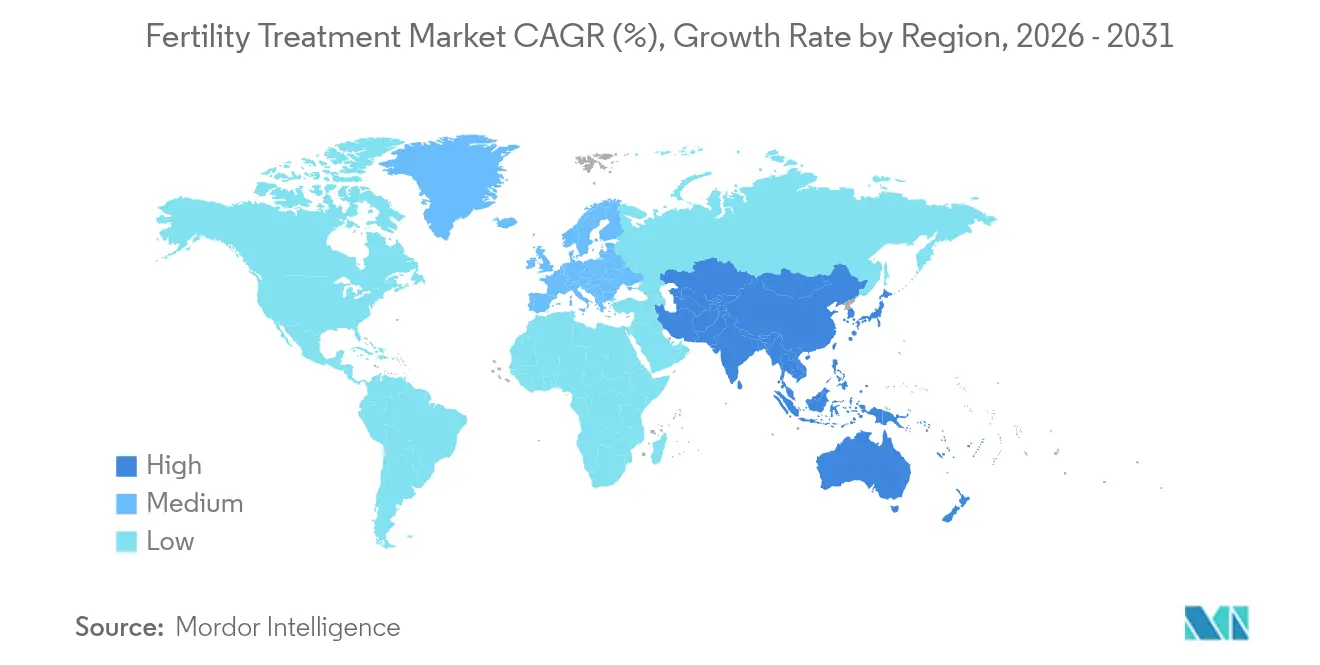

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fertility Treatment Market Analysis by Mordor Intelligence

Fertility treatment market size in 2026 is estimated at USD 37.1 billion, growing from 2025 value of USD 34.63 billion with 2031 projections showing USD 52.33 billion, growing at 7.12% CAGR over 2026-2031. Rising infertility prevalence, delayed parenthood, and rapid adoption of artificial intelligence (AI) for embryo assessment are accelerating demand. Cross-border reproductive care is widening patient pools as couples travel to jurisdictions with lower costs or more liberal laws. Regulatory momentum—such as mandatory U.S. insurance coverage for multiple in-vitro fertilization (IVF) cycles—couples with breakthroughs like stem-cell-matured oocytes that shorten stimulation protocols. Consolidation among chain clinics is improving live-birth outcomes and lifting the fertility treatment market’s overall service quality, while private equity capital continues to pour into automation and male infertility solutions.

Key Report Takeaways

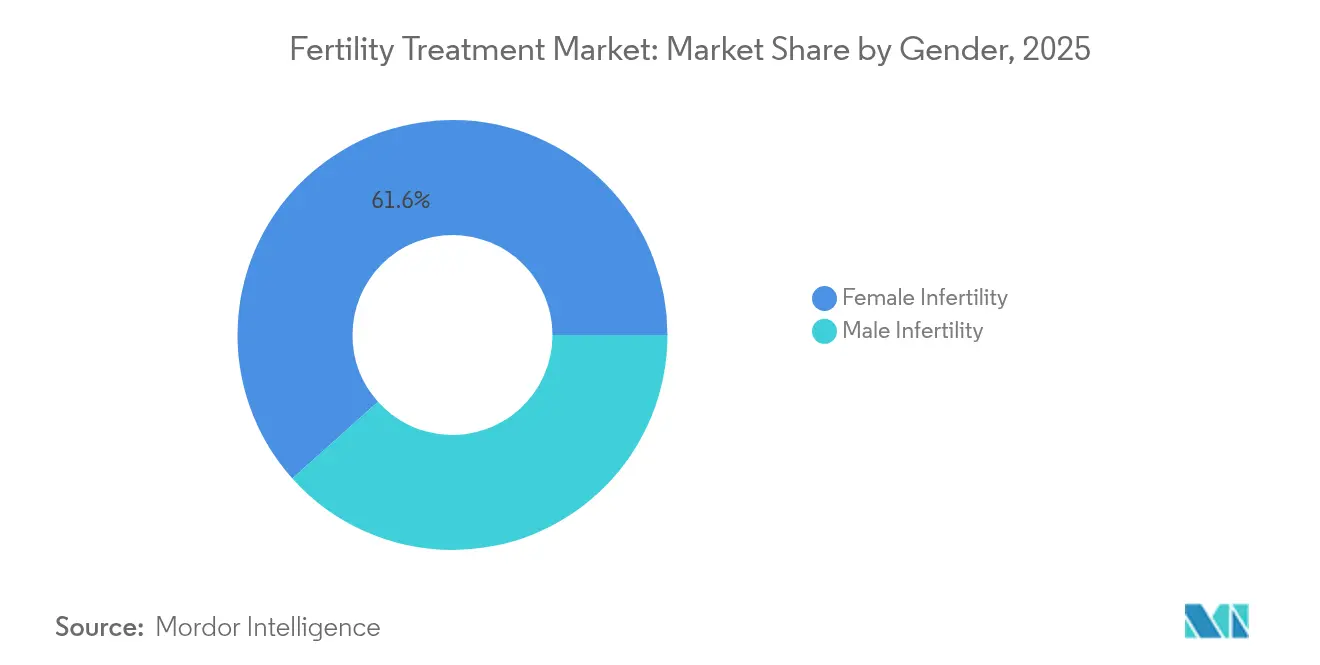

- By gender, female infertility held 61.62% of fertility treatment market share in 2025, whereas male infertility is set to grow fastest at a 9.16% CAGR to 2031.

- By treatment type, in-vitro fertilization led with 46.58% revenue share in 2025; intracytoplasmic sperm injection is projected to climb at a 9.63% CAGR through 2031.

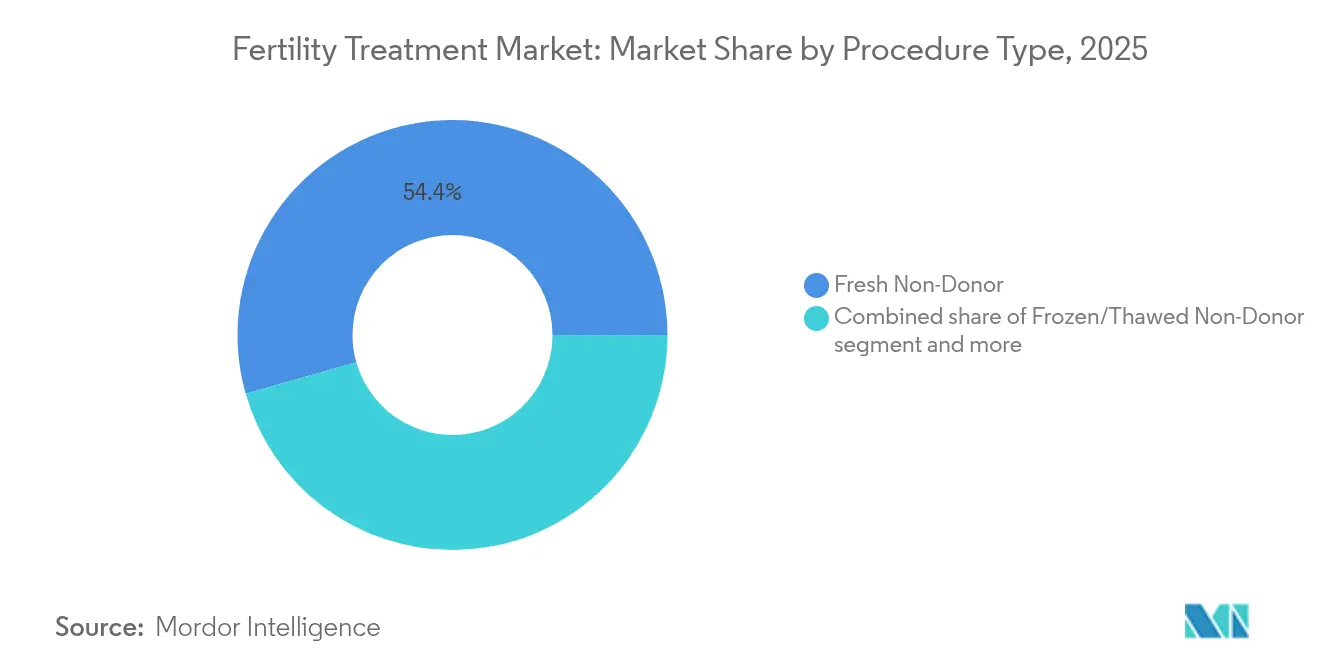

- By procedure type, fresh non-donor cycles captured 54.41% of the fertility treatment market size in 2025, while frozen/thawed non-donor cycles are expanding at 9.28% CAGR.

- By service provider, fertility clinics and ART centers commanded 67.62% of 2025 revenue; tele-fertility platforms record the highest forecast CAGR at 10.15% through 2031.

- By region, North America accounted for 38.11% of global revenue in 2025; Asia-Pacific is advancing at an 8.12% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fertility Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Infertility Incidence | +1.8% | Global, highest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Delayed Childbearing Trends | +1.5% | North America and Europe; spreading to urban Asia-Pacific | Medium term (2-4 years) |

| Technological Advancements In Assisted Reproductive Technologies | +1.2% | North America and Europe; rapidly diffusing worldwide | Short term (≤ 2 years) |

| Expansion Of Cross-Border Fertility Tourism | +0.8% | Key corridors: North-South America, intra-Europe, intra-Asia | Medium term (2-4 years) |

| Employer-Sponsored Fertility Benefit Programs | +0.7% | United States, Canada, Western Europe; emerging uptake in Asia-Pacific multinationals | Short–medium term (≤ 3 years) |

| Integration Of Artificial Intelligence In Embryo Selection | +0.6% | Early adoption in North America and Europe; pilot programs in Asia-Pacific clinics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Infertility Incidence

Roughly 186 million people now experience infertility, translating to 17.5% of the adult populatio. Asia-Pacific shows the sharpest rise, with secondary female infertility climbing faster than primary cases between 1990 and 2021[1]Wang Yajuan, “Trends in Secondary Infertility 1990-2021,” China CDC Weekly, weekly.chinacdc.cn. Polycystic ovary syndrome and lifestyle factors intensify demand, and in the Philippines one in four couples seek medical help[2]Inhorn Marcia, “Cross-Border Reproductive Care Networks,” Frontiers in Sociology, frontiersin.org. Developed economies face sub-replacement fertility, so government incentives and insurance mandates are widening access. These epidemiological stresses create lasting tailwinds for the fertility treatment market.

Delayed Childbearing Trends

Average maternal age at first birth continues to rise, and egg-freezing cycles for non-medical reasons increased 30% year-over-year at leading clinics. Employers now add fertility benefits to retain talent, with 31% covering preservation services and 30% reimbursing IVF. Women recognize the biologic clock yet lack awareness of age-related decline, spurring uptake of oocyte-cryopreservation packages. This postponement expands the fertility treatment market while encouraging bundled benefit models that lower out-of-pocket costs.

Technological Advancements in Assisted Reproductive Technologies

AI algorithms achieve predictive embryo-viability accuracies of up to 97% versus 65-70% for human grading[3]NewYork-Presbyterian, “AI Algorithm Improves Embryo Selection,” NYP News, nyp.org. Time-lapse incubators paired with deep learning allow continuous monitoring, raising implantation forecasts without invasive biopsies. Research centers collect lab-environment data every 10 minutes to tweak conditions and close the success-rate gap, which today averages 30-50%. Digital decision-support tools are therefore standardizing embryology workflows and elevating overall fertility treatment market performance.

Expansion of Cross-Border Fertility Tourism

Differences in law and cost spur patients to travel: an IVF cycle costs USD 2,700 in India versus USD 10,200 in Singapore. Oocyte-vitrification lets donor eggs traverse multiple European borders before implantation in Brazil, illustrating an emergent “reproductive silk route”. Canadian patients form the largest non-U.S. user base in American clinics, with 42.6% utilizing egg donation because Canada bans paid donors. Thailand and Malaysia are positioning as hubs to capture Chinese medical tourists, underlining how travel flows support fertility treatment market growth.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs And Limited Reimbursement | -1.4% | Most severe in North America, Latin America and emerging Asian markets | Medium term (2-4 years) |

| Ethical And Religious Constraints | -0.9% | Middle East, parts of Asia-Pacific, conservative regions in Europe and North America | Long term (≥ 4 years) |

| Declining Availability Of Donor Gametes | -0.6% | Europe (due to stricter family limits), Canada, selected Asia-Pacific countries | Medium term (2-4 years) |

| Environmental Sustainability Pressures On IVF Laboratories | -0.3% | Europe (ESG mandates), Australia, corporate-funded U.S. clinics | Short–medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Limited Reimbursement

In the United States, a single IVF cycle runs USD 12,000–30,000, and patients usually need 2.5 cycles to succeed. Only one-quarter of employers cover IVF, leaving many households to finance treatments via high-interest specialty loans. Disruptors such as Pozitivf Fertility trimmed cycle prices to USD 7,900 by streamlining lab protocols. While U.S. state mandates and California’s 2025 insurance law may ease access, reimbursement gaps still slow the fertility treatment market’s expansion.

Ethical and Religious Constraints

Surrogacy remains illegal in mainland China and tightly restricted in parts of Europe and the Middle East, complicating parentage rights and custody disputes. The Philippines lacks a national ART framework, so personal moral beliefs dictate practice standards, restraining uptake. Preimplantation genetic testing for polygenic disorders raises concerns about eugenics, and evidence on long-term child outcomes is scarce. These ethical debates generate regulatory uncertainty that tempers fertility treatment market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gender: Male Infertility Gains Clinical Recognition

In 2025, female infertility accounted for 61.62% of the fertility treatment market. The male infertility segment, however, is forecast to register a 9.16% CAGR from 2026 to 2031 as clinicians acknowledge that men contribute to up to half of infertility cases. Artificial-intelligence-driven semen-analysis devices and smartphone-based diagnostics are improving accuracy and accessibility. Ferring Pharmaceuticals and Posterity Health launched a digital Male Fertility program that provides confidential assessments and personalized guidance, reducing diagnostic delays.

Growing social acceptance and targeted investment are enabling simultaneous testing of both partners, cutting unnecessary costs. Lifestyle modification apps, hormonal therapies, and micro-surgical interventions enlarge the therapeutic toolkit. As insurers gradually expand coverage for male diagnostic workups, the fertility treatment market gains a new revenue stream that complements the dominant female-focused services.

By Treatment Type: ICSI Emerges as Growth Leader

In-vitro fertilization retained 46.58% revenue share in 2025, yet intracytoplasmic sperm injection (ICSI) is projected to grow at a 9.63% CAGR, making it the fastest-rising modality. ICSI’s precision suits severe male-factor or previously failed IVF cases, and its adoption reflects wider awareness of male contributions to infertility. As genetic screening becomes cheaper, the share of IVF cycles using preimplantation genetic testing is expected to rise to about 25% in coming years.

Adjunct innovations, including platelet-rich plasma therapy and mitochondrial transfer, aim to boost oocyte quality, though regulators now tighten oversight of stem-cell-based clinics. These layered treatment options diversify revenue and fuel the fertility treatment market. Medication protocols and surgical adjuncts still underpin all cycles, but automation and AI are reducing manual variability.

By Procedure Type: Frozen Embryo Transfers Gain Momentum

Fresh non-donor cycles represented 54.41% of the fertility treatment market size in 2025, yet frozen/thawed non-donor cycles are expanding at a 9.28% CAGR thanks to improved vitrification and higher implantation success. Chain clinics report 93% single-embryo transfer adoption, curbing multiples and maternal complications.

Donor gamete cycles grow in parallel as cross-border patients seek egg or sperm unavailable at home. Regulatory caps on donor family limits vary dramatically, with some European banks allowing donations to 75 families versus the United Kingdom’s limit of 10. Such disparities sustain cross-border transport of vitrified embryos and reinforce the international nature of the fertility treatment market.

By Service Provider: Tele-Fertility Platforms Disrupt Traditional Care

Fertility clinics and ART centers delivered 67.62% of 2025 revenue, yet tele-fertility services exhibit a 10.15% forecast CAGR. Remote platforms handle initial consults, monitoring, and medication management, widening access in underserved areas. Conceivable Life Sciences’ fully automated AURA laboratory in Mexico City processes 2,000 annual cycles with minimal staff, illustrating how robotics lower costs and address embryologist shortages.

Maven Clinic’s 24/7 virtual coaching model achieved a 98% singleton pregnancy rate after IVF while lowering overall costs by up to 30%. Tele-fertility further aligns with employer benefit plans, improving uptake and reinforcing digital-first care pathways inside the fertility treatment market.

Geography Analysis

North America commanded 38.11% of global revenue in 2025, anchored by advanced clinical infrastructure, higher disposable income, and state-level insurance mandates that now cover up to three IVF cycles for millions of residents. The United States also draws Canadian and Caribbean patients, benefiting from well-established donor registries and genetic laboratories. Private equity funding into clinic chains accelerates market consolidation and technology adoption, keeping the region at the forefront of the fertility treatment market.

Asia-Pacific is the fastest-growing geography with an 8.12% CAGR forecast through 2031. India opens 60-70 IVF centers each year, and organized networks now perform 35-40% of national cycles compared with negligible levels a decade ago. China’s large unmet need and evolving reimbursement guidelines hold substantial promise, even though commercial surrogacy remains banned. Thailand and Malaysia leverage medical-tourism incentives to attract Chinese, Australian, and Middle-Eastern clients, thereby strengthening the regional fertility treatment market.

Europe maintains a robust position under supportive legislation in Spain, Denmark, and the Czech Republic, where public funding and liberal donor rules stimulate procedure volumes. Following Poland’s recent policy shift, all 27 EU members now fund IVF in some form, yet only five grant full financing for up to six cycles. Latin America performs roughly 107,000 IVF cycles annually, led by Brazil, Argentina, and Mexico. The Middle East and Africa remain nascent but show rising demand in Gulf Cooperation Council states where expatriate populations commonly delay childbearing.

Competitive Landscape

The fertility treatment market is moderately consolidated. Chain clinics expanded their collective share from 5% in 2004 to 20% in 2018 and now conduct more than 40% of all IVF cycles, reporting 14% higher live-birth rates than independent centers. Private equity fuels this shift: KKR acquired IVIRMA for USD 3.8 billion and BPEA EQT bought Indira IVF for USD 656.6 million, signaling confidence in scalable, tech-enabled care models.

Technology investment is the new battleground. Vitrolife took a lead stake in AutoIVF, while Astorg merged Hamilton Thorne with Cook Medical’s IVF arm after a USD 228 million deal to integrate equipment and consumables. Emerging players such as Gameto and Overture Life channel venture funding into stem-cell maturation and lab automation, respectively, pushing the fertility treatment market toward standardized, high-throughput operations.

White-space opportunities persist in male fertility diagnostics, preservation services, and underserved geographies. Companies are adding genetic counseling, mental-health support, and financing options to improve patient experience and retention. As regulatory frameworks harmonize and tele-fertility scales, competition will hinge on outcome transparency and cost efficiency rather than geographic exclusivity.

Fertility Treatment Industry Leaders

CooperSurgical Inc.

Vitrolife AB

Merck KGaA (EMD Serono)

Ferring Holdings SA

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ReproNovo raised USD 65 million Series A led by Jeito Capital to advance Phase 2 trials of RPN-001 for male infertility and RPN-002 for adenomyosis and embryo implantation enhancement.

- April 2025: Overture Life secured USD 20.6 million to accelerate IVF-lab automation and expand global access.

- February 2025: Posterity Health closed USD 13 million Series A financing aimed at comprehensive male fertility care.

- February 2025: Organon licensed Bao Pharmaceutical’s SJ02, a long-acting FSH in a Chinese BLA process, broadening its ART portfoli.

- January 2025: Gameto received FDA clearance for a Phase 3 trial of Fertilo, which cuts hormone injections by 80% and reduces cycle length to three days.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fertility treatment market as all fee-based medical interventions and prescription drugs used to overcome biological infertility and help intended parents achieve a live birth. It captures assisted reproductive procedures (IVF, ICSI, IUI, cryopreservation, donor cycles, genetic testing), related surgical corrections, and the therapeutic drug regimens prescribed for male or female factor cases.

Scope Exclusions: Contraceptives, home pregnancy or ovulation test kits, and over-the-counter fertility supplements lie outside this assessment.

Segmentation Overview

- By Gender

- Female Infertility

- Male Infertility

- By Treatment Type

- In-Vitro Fertilization (IVF)

- Intracytoplasmic Sperm Injection (ICSI)

- Intrauterine Insemination (IUI)

- Fertility Medications

- Surgery & Other ART

- Cryopreservation Services

- Genetic Testing & PGD/PGT-A

- Adjunct Therapies (PRP, Stem Cell, Mito Transfer)

- By Procedure / Cycle Type

- Fresh Non-Donor

- Frozen / Thawed Non-Donor

- Donor Egg / Embryo

- Surrogacy Cycles

- By Service Provider

- Fertility Clinics & ART Centres

- Hospitals & Surgical Centres

- Cryobanks & Genetic Labs

- Tele-Fertility Platforms

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts supplement desk work with structured discussions involving reproductive endocrinologists, embryologists, clinic finance managers, and ART equipment distributors across North America, Europe, Asia-Pacific, and the GCC. These interviews validate treatment volumes, average selling prices (ASPs), reimbursement shifts, and emerging techniques that secondary data alone cannot fully surface.

Desk Research

We start by mapping publicly available data from tier-1 health sources such as WHO infertility prevalence tables, CDC and ESHRE ART cycle registries, national vital-statistics offices, and trade bodies like the American Society for Reproductive Medicine. Filings from listed clinic groups, insurer reimbursement schedules, and patent activity on embryo-selection AI provide additional context. Select paid databases, D&B Hoovers for clinic revenues and Questel for device patents, supply financial and innovation clues. This list is illustrative; many further sources underpin our evidence stack.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort model estimates the global candidate pool before clinic utilization rates, average cycle multiples, and ASPs translate cases into value terms. Select bottom-up checks, sampled IVF laboratory roll-ups and drug channel audits, help us recalibrate totals. Key drivers in the model include national infertility prevalence, average ART success rates, cross-border treatment flows, insurance coverage uptake, regulatory caps on embryo transfers, and median cycle pricing. Multivariate regression combined with scenario analysis projects each driver to 2030, while expert consensus moderates extremes and fills data gaps.

Data Validation & Update Cycle

Outputs pass two-level variance checks against historic clinic revenues and shipment trends, followed by peer review and senior analyst sign-off. Reports refresh annually; any major regulatory, technological, or reimbursement event triggers an interim update, ensuring clients receive an up-to-date view.

Why Mordor's Fertility Treatment Baseline Commands Confidence

Published estimates frequently diverge because firms choose different service scopes, pricing ladders, and refresh cadences.

Key gap drivers include whether drugs and surgical adjuncts are counted, how donor cycles are treated, ASP inflation assumptions, and the width of geographic coverage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 34.63 B (2025) | Mordor Intelligence | - |

| USD 36.53 B (2024) | Global Consultancy A | Combines contraceptive services and wider women's health revenues, inflating the baseline |

| USD 1.89 B (2024) | Regional Consultancy B | Counts only laboratory equipment sales in select nations, omitting drug and service income |

Taken together, the comparison shows that our disciplined scope selection, dual-path modeling, and yearly refresh create a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the fertility treatment market?

The fertility treatment market stands at USD 37.1 billion in 2026 and is projected to hit USD 52.33 billion by 2031.

Which segment is growing fastest within the market?

Intracytoplasmic sperm injection leads growth with a 9.63% CAGR forecast for 2026-2031.

Why is Asia-Pacific considered the most dynamic region?

Large populations, rising infertility awareness, and rapid clinic expansion push Asia-Pacific’s CAGR to 8.12% through 2031.

Which is the fastest growing region in Global Fertility Treatment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What are the major cost barriers for patients?

In the United States, IVF costs USD 12,000–30,000 per cycle, and limited insurance coverage means many couples self-fund multiple attempts.

How consolidated is the competitive landscape?

Private-equity-backed chains now manage over 40% of IVF cycles, but independent clinics remain significant, giving the market a moderate concentration score.

Page last updated on: