Pressure Ulcers Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

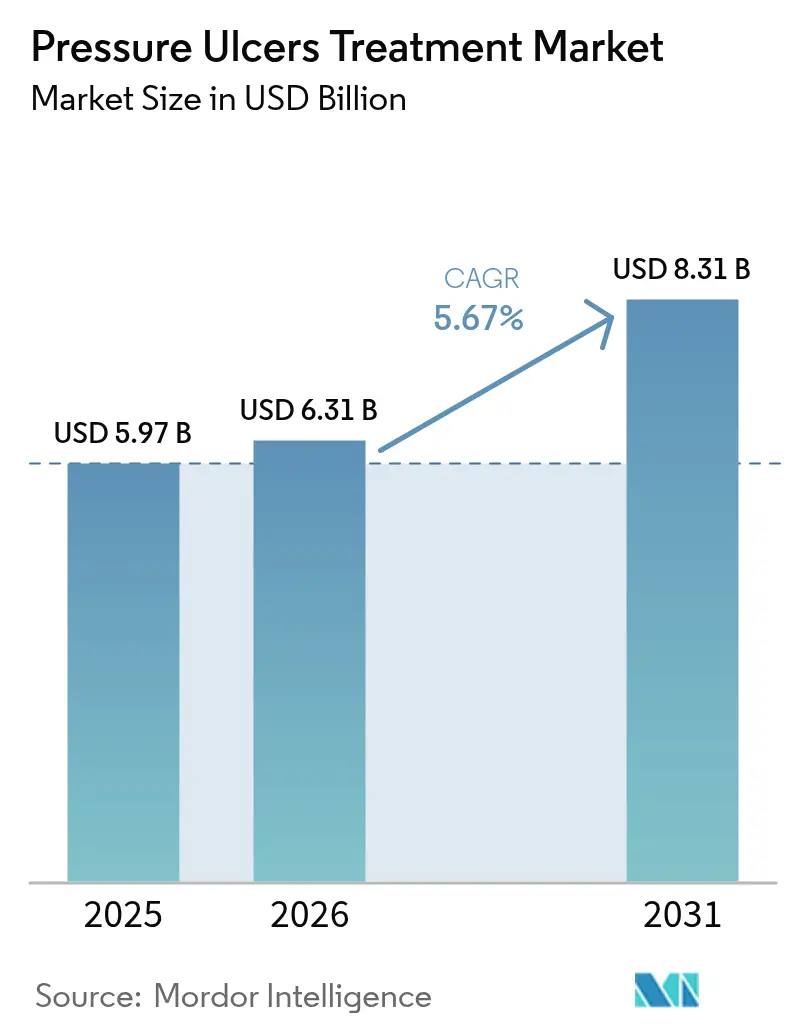

| Market Size (2026) | USD 6.31 Billion |

| Market Size (2031) | USD 8.31 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

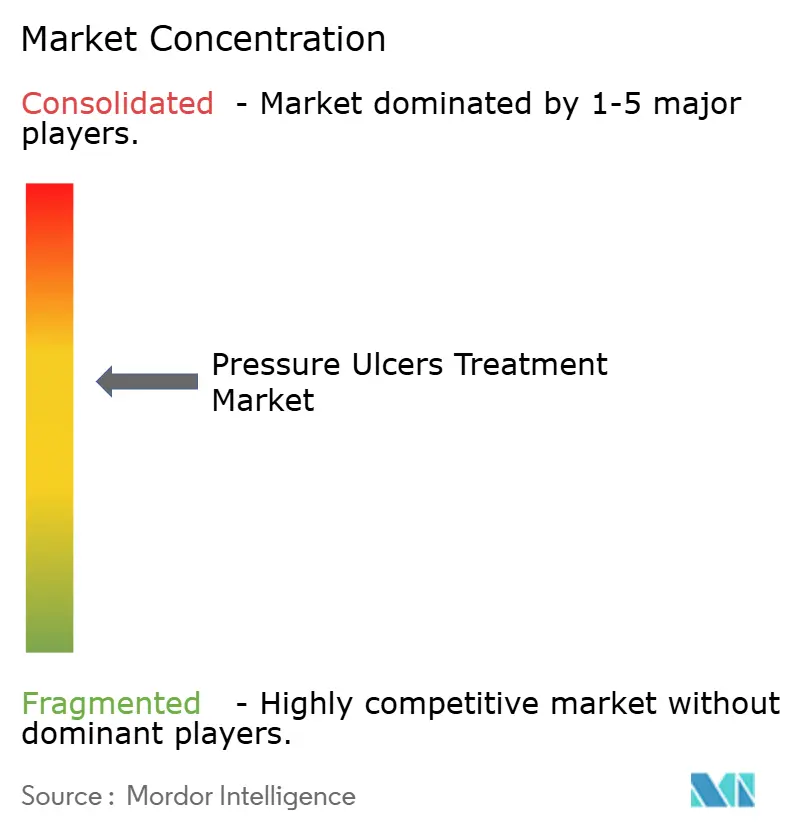

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pressure Ulcers Treatment Market Analysis by Mordor Intelligence

The pressure ulcer treatment market size in 2026 is estimated at USD 6.31 billion, growing from 2025 value of USD 5.97 billion with 2031 projections showing USD 8.31 billion, growing at 5.67% CAGR over 2026-2031. Growth is underpinned by accelerating demographic aging, surging chronic-disease prevalence, and value-based reimbursement policies that reward prevention while penalizing hospital-acquired injuries. Real-time AI pressure-mapping beds now achieve 94.2% accuracy in patient-position detection, enabling proactive repositioning and driving a structural pivot from reactive care to predictive prevention. Negative pressure wound therapy (NPWT) systems have become more portable and cost-efficient, supporting outpatient and home-care use while broadening the addressable patient base. Collectively, these factors are reshaping provider economics, pushing decision-makers toward technologies that shorten healing time, minimize readmissions, and reduce total cost of care.

Key Report Takeaways

- By product type, active wound-care therapies held 21.37% of the pressure ulcer treatment market share in 2025, while NPWT recorded the fastest growth at an 8.02% CAGR through 2031.

- By ulcer stage, Stage II ulcers accounted for 33.18% of treatment cases in 2025, whereas Stage IV ulcers are expanding at a 7.61% CAGR to 2031.

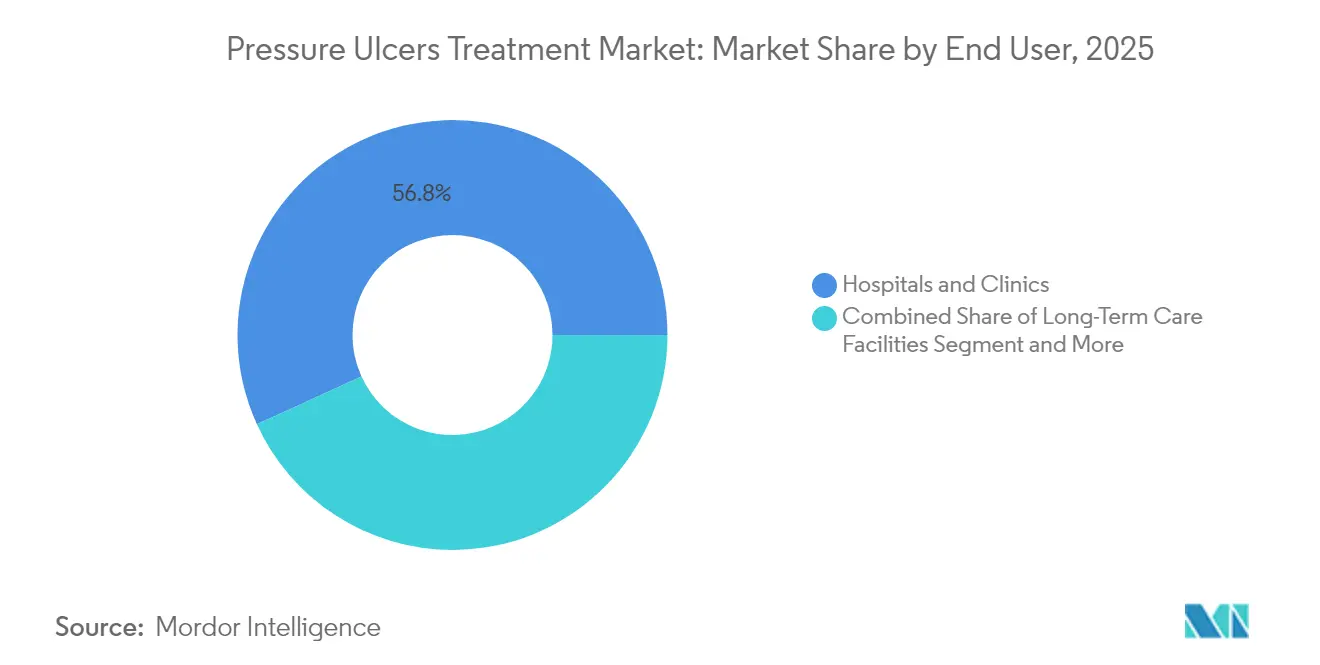

- By end user, hospitals and clinics controlled 56.81% of the pressure ulcer treatment market share in 2025, yet home-care settings are advancing at an 7.95% CAGR to 2031.

- By geography, North America captured 45.12% revenue share in 2025; Asia-Pacific is forecast to post the highest regional CAGR at 8.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pressure Ulcers Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic-disease burden | +1.2% | North America, Europe, global spillover | Long term (≥ 4 years) |

| Faster wound closure & early discharge | +0.8% | North America, Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Rising surgical volumes & trauma incidence | +0.9% | Global, highest growth in Asia-Pacific | Medium term (2-4 years) |

| Adoption of NPWT | +1.1% | North America, Europe, emerging markets | Short term (≤ 2 years) |

| AI pressure-mapping beds | +0.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Value-based reimbursement penalties | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Prevalence of Chronic Diseases

Global life expectancy gains are producing a larger cohort of immobile, comorbid patients who remain susceptible to pressure injuries. World-wide, diabetes prevalence among surgical candidates reached 15.3% in 2024, intensifying tissue-repair complexity[1]Frontiers in Public Health, “Global, Regional and National Burden of Decubitus Ulcers,” frontiersin.org. Hospitals are therefore scaling investment in biologically active dressings that deliver epidermal growth factor, a modality shown to accelerate re-epithelialization in chronic wounds. In mature health systems, reimbursement codes already cover a spectrum of growth-factor therapies, encouraging clinicians to adopt premium products that shorten healing time. Emerging markets, meanwhile, are adopting simplified, lower-cost bioactive solutions to manage the same demographic pressures. The differential adoption framing is creating a tiered global opportunity for suppliers able to flex pricing and product complexity according to local capacity.

Rising Demand for Faster Wound Closure & Early Discharge

Provider payment reforms now link compensation to length-of-stay metrics, prompting an operational focus on closing wounds quickly without compromising outcomes. Electric bandage prototypes have demonstrated 30% faster healing versus conventional approaches, signalling commercial potential for energy-based therapies that can be monitored remotely. Biologic dressings impregnated with viable cells further boost granulation tissue formation, enabling same-week discharge for selected pressure-ulcer patients. Smart bandages equipped with micro-sensors transmit moisture and pH data to clinicians, cutting unnecessary dressing changes and nurse workload. These advances dovetail with payer objectives to reallocate inpatient resources toward high-acuity care. Consequently, device makers that integrate real-time analytics into cost-effective consumables stand to gain rapid formulary access across integrated delivery networks.

Higher Surgical Volumes and Trauma Incidence Worldwide

Elective and trauma-related surgical procedures rose sharply in 2024 as health systems cleared pandemic backlogs and emerging economies expanded operating-room capacity. Greater procedural throughput has increased the absolute population at risk of peri-operative pressure injury, particularly among patients with body-mass indices above the normal range. Longer anesthesia times and prone-position surgeries raise sustained skin-compression risk, intensifying demand for intra-operative support surfaces. Hospitals in Asia-Pacific, where surgical volume growth outpaces workforce expansion, are procuring automated pressure-redistribution tables to mitigate ulcer formation during lengthy interventions. Such purchases directly lower penalty exposure under national quality-reporting programs, reinforcing procurement justification even where capital budgets are constrained.

Increasing Adoption of Negative Pressure Wound Therapy (NPWT)

NPWT systems evolved quickly after 2024, propelled by single-use canister-free cartridges that trim dressing-change time by 61% and cut supply costs by 41%. Clinical guidelines now recommend NPWT as first-line therapy for Stage III and Stage IV ulcers that fail moisture-retentive dressings, a recognition formalized by major commercial insurers in 2025. Recent designs integrate antimicrobial instillation cycles, improving bioburden control while preserving granulation tissue integrity. Growing Medicare coverage for disposable NPWT kits has also catalyzed adoption in home-care settings, especially among mobility-restricted seniors. These reimbursement tailwinds are expected to strengthen over the next two years as payers evaluate real-world data linking NPWT use to lower readmission rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced wound products | -0.8% | Global, sharper in emerging markets | Medium term (2-4 years) |

| Uneven reimbursement in emerging economies | -0.6% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Silver-dressing raw-material volatility | -0.3% | Global production hubs | Short term (≤ 2 years) |

| Home-care skill gap in device usage | -0.4% | Global, acute in rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Wound Products

Cellular tissue products can exceed USD 1,500 per application, a hurdle for hospitals operating under fixed-payment bundles. The Centers for Medicare & Medicaid Services (CMS) pruned its covered-skin-substitute list to 17 products in 2025, narrowing the reimbursable field and forcing clinicians to ration premium therapies[2]Relias, “Navigating New CMS Skin Substitute Updates,” relias.com. Capital-intensive NPWT consoles likewise demand justification through multi-year value analyses, delaying adoption in cash-constrained facilities. Suppliers are countering by introducing subscription-based pricing and repackaged single-use kits that lower per-episode spending. Nonetheless, the economic hurdle remains a significant dampener on rapid penetration in low-resource settings.

Uneven Reimbursement Coverage in Emerging Economies

Public insurance programs in parts of Asia-Pacific and Latin America classify advanced wound care as elective, shifting costs to patients and limiting demand elasticity. Fragmented payer systems complicate manufacturer listing strategies, extending negotiation timelines and inflating market-entry costs. Multinational suppliers therefore pursue tiered portfolios, pairing premium bioengineered dressings with locally manufactured hydrocolloid alternatives to secure broader formulary acceptance. Over the long term, broader universal-coverage reforms could ease this restraint, but immediate commercial plans must accommodate reimbursement heterogeneity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Active Modalities Sustain Market Leadership

Active wound-care therapies accounted for 21.37% of the pressure ulcer treatment market size in 2025, reflecting strong clinical preference for biologically active solutions that modulate inflammation and stimulate tissue regrowth. Growth factors, platelet-rich plasma, and cell-seeded matrices headline this category and command premium pricing across integrated delivery networks. Manufacturers are scaling production of allogeneic cell therapies, leveraging regulatory fast tracks that shorten commercialization timelines. Negative pressure wound therapy continues to outpace all other modalities at an 8.02% CAGR, buoyed by single-use platforms that allow rapid deployment in outpatient and home-care environments. Meanwhile, conventional foam and hydrogel dressings undergo iterative improvements—such as moisture-responding polymers and antimicrobial nanoparticles—to sustain relevance as cost-effective adjuncts. Over the forecast horizon, suppliers that pair active biologics with sensor-enabled delivery systems stand best positioned to capture incremental hospital spend.

Negative pressure wound therapy leads innovation pipelines, with next-generation systems combining instillation cycles and ionic-silver meshes to suppress biofilm formation while maintaining sub-atmospheric pressure. The FDA’s 2025 clearance of a peel-and-place drape reduced setup time to under five minutes, widening nursing adoption. Film dressings and collagen pads retain niche roles in early-stage or superficial ulcers, providing cost-conscious providers with clinically validated options. As pricing pressure intensifies, vendors will differentiate through outcomes-based contracts that tie reimbursement to documented reductions in healing time, mirroring trends in the broader pressure ulcer treatment market.

By Ulcer Stage: Severity Mix Drives Resource Allocation

Stage II ulcers represented 33.18% of treated cases in 2025, underlining the prevalence of moderate-severity injuries that benefit from early intervention protocols. Hospitals deploy moisture-retentive dressings and periodic off-loading strategies to accelerate epithelial recovery at this stage. In contrast, Stage IV lesions are expanding at a 7.61% CAGR, consuming disproportionate clinical resources and spurring demand for advanced biologics and NPWT systems. The pressure ulcer treatment market size associated with Stage IV care is forecast to climb sharply as aging populations and multimorbidity raise complexity levels within inpatient cohorts.

Across stages, precision-diagnostic platforms employing multispectral imaging and machine-learning algorithms now achieve 74% accuracy in predicting ulcer progression risk. This capability enables earlier deployment of high-value therapies, potentially flattening Stage IV growth beyond 2031. Deep-tissue injuries and unstageable wounds remain assessment challenges, catalyzing R&D investment in biomarkers capable of delineating ischemia depth. As more granular staging tools gain regulatory clearance, payers are expected to embed stage-based reimbursement modifiers, further linking economic incentives to accurate classification.

By End User: Home-Care Expansion Redefines Service Models

Hospitals and clinics retained 56.81% of the pressure ulcer treatment market share in 2025, driven by the concentration of complex wounds requiring surgical debridement or advanced biologics. Nevertheless, home-care settings are growing at an 7.95% CAGR, reflecting payer directives to treat stable wounds outside acute facilities and capitalize on lower per-diem costs. CMS expanded telehealth coverage for wound-management consults in 2025, enabling remote follow-up protocols that reduce in-person visits while preserving outcome quality. Integrated wound-monitoring apps guide caregivers through dressing changes and automatically alert clinicians to deviations in wound exudate volume, bridging the skill-gap restraint discussed earlier.

Long-term-care facilities maintain steady demand due to resident immobility and chronic comorbidities, yet budget constraints favor cost-effective foam and hydrofiber dressings. Ambulatory surgical centers are emerging as middle-ground venues for Stage I and Stage II interventions, particularly when NPWT initiation is required post-debridement. Collectively, these shifts are fragmenting care pathways, compelling device makers to tailor training resources and format options to diverse provider environments within the wider pressure ulcer treatment industry.

Geography Analysis

North America led the pressure ulcer treatment market with 45.12% revenue share in 2025, supported by robust reimbursement schemes, high adoption of AI-enabled preventive technologies, and favorable regulatory pathways. Hospitals in the United States accelerated capital outlays for smart support surfaces following a USD 26.8 billion penalty burden tied to hospital-acquired pressure injuries. Canada followed with province-level funding earmarked for NPWT kits in home-care programs, further broadening patient access.

In Europe, budgeting frameworks require cost-effectiveness dossiers, motivating suppliers to sponsor pragmatic trials that demonstrate resource-adjusted benefits. Countries such as Germany and the Netherlands now reimburse NPWT under DRG add-on payments, while the United Kingdom’s NICE validated single-use NPWT for surgical sites in 2024. The region’s embrace of evidence-based procurement sustains moderate growth despite mature penetration levels.

Asia-Pacific is the fastest-growing territory, projected at an 8.34% CAGR, fueled by health-insurance expansion in China and India and rising orthopedic and cardiovascular surgery volumes. Regional ministries are launching wound-management guidelines that prioritize infection control and rapid mobilization, stimulating imports of silver-impregnated foam and portable NPWT systems. Local contract manufacturers are entering licensing deals with multinational suppliers, lowering final-product costs and facilitating wider adoption. The Middle East & Africa and South America collectively account for a smaller share but present high unmet need; multilateral development programs are funding pilot deployments of AI-enabled pressure-mapping beds in tertiary hospitals, potentially seeding demand for broader rollouts by 2027.

Competitive Landscape

The pressure ulcer treatment market exhibits moderate concentration, with the top players—Smith+Nephew, Integra LifeSciences, and Mölnlycke Health Care—collectively holding significant revenue share in 2024. Incumbents leverage broad portfolios spanning dressings, biologics, and digital solutions, allowing hospitals to standardize procurement under multi-year supply agreements. Smith+Nephew’s integration of its PICO single-use NPWT line with the real-time WoundVision Scout imaging system exemplifies a shift toward data-enabled ecosystems that lock in customers through software stickiness.

Strategic partnerships dominate competitive moves. In early 2025, Solventum partnered with a cloud-analytics firm to embed predictive-healing algorithms into its NPWT controller, promising to cut therapy duration by predicting optimal pressure cycles. Integra LifeSciences acquired a South-Korean collagen-matrix manufacturer to localize supply and hedge against currency volatility. Meanwhile, start-ups specializing in bioelectronic bandages and oxygen-diffusion dressings are attracting venture capital, aiming to address niche applications unserved by mainstream portfolios.

Regulatory developments are also reshaping rivalry. The FDA’s 2025 down-classification of bacterial-protease detectors to Class II lowered entry barriers for diagnostic-focused companies. Larger incumbents responded by licensing sensor technologies rather than building in-house, accelerating time-to-market and broadening platform scope. Competitive success increasingly hinges on offering integrated product-service bundles that guarantee measurable reductions in pressure-injury incidence, aligning supplier incentives with hospital quality scores across the global pressure ulcer treatment market.

Pressure Ulcers Treatment Industry Leaders

Molnlycke Health Care AB

Cardinal Health Inc.

Essity AB

Integra LifeSciences Holdings Corp.

Smith & Nephew PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Provider priorities are shifting from episodic wound closure to prevention and earlier, protocolized escalation, creating whitespace for integrated bundles that combine support surfaces, repositioning aids, and digitally enabled monitoring. The 2025 fourth edition of the International Guideline (NPIAP/EPUAP/PPPIA) reinforced specific prevention practices (such as 30-degree lateral positioning and use of reactive foam surfaces), strengthening procurement justification for turnkey turning and positioning systems that standardize compliance in hospitals, long-term care facilities, and home-care pathways.

On the treatment side, recent US regulatory activity broadens the competitive set across NPWT, advanced dressings, and debridement options used in pressure ulcer care. In 2026, FDA 510(k) clearances covered new NPWT platforms, including Bechtel Medicals Wound Geni NPWT system and Smith+Nephews RENASYS EDGE, as well as wound-management dressings cleared under established pathways, for example MatriDerm. Another whitespace area is differentiated debridement and infection-management approaches for complex chronic wounds, highlighted by Cuprina Holdings FDA 510(k) clearance in June 2026 for MEDIFLY Maggots (Lucilia cuprina).

Recent Industry Developments

- July 2026: Mölnlycke Health Care accelerated its US wound care push with three launches: Granudacyn Wound Wash Solution, the Tortoise Lite Turning and Positioning System, and the Mepi Press 2 and Mepi Press Lite Compression System. The mix links prevention and care pathway execution (positioning and cleansing) with adjunctive compression, supporting broader facility standardization around pressure-injury prevention and wound management.

- May 2026: Mölnlycke Health Care announced a joint venture in China with Zhende Medical to expand and integrate wound care portfolios locally. The structure strengthens access to a high-growth geography and supports localization benefits that can reduce lead times and improve availability across hospital and community care channels.

- September 2024: Solventum launched the V.A.C. Peel and Place Dressing system for NPWT, designed to shorten application time, reduce costs, and extend wear time. Faster, simpler NPWT setup increases feasibility in outpatient and home-care workflows and supports wider protocol adoption beyond specialized inpatient teams.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers products and therapies used to treat pressure ulcers (also called pressure sores or bedsores) across care settings, with values tracked as the spend linked to clinical management of these wounds.

Scope exclusions: We exclude purely preventive-only items and general skincare products that are not used as part of a documented pressure ulcer treatment pathway.

Segmentation Overview

- By Product Type

- Wound-Care Dressings

- Film Dressings

- Foam Dressings

- Hydrogel Dressings

- Collagen Dressings

- Active Wound-Care Therapies

- Skin Substitutes

- Growth Factors & Biologics

- Wound-Care Devices

- Negative Pressure Wound Therapy

- Hyperbaric Oxygen Equipment

- Pressure-Relieving Devices

- Other Devices

- By Ulcer Stage

- Stage I

- Stage II

- Stage III

- Stage IV

- Unstageable / Deep-Tissue Injury

- By End User

- Hospitals & Clinics

- Long-Term Care Facilities

- Home-Care Settings

- Ambulatory Surgical Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear clinical and payment context, because pressure ulcer treatment use is closely linked to care setting and patient risk. We refer to public sources such as the US Centers for Medicare and Medicaid Services (quality reporting and reimbursement signals), CDC materials on healthcare associated conditions, and OECD health statistics for long term care capacity and aging trends.

To size the supply and utilization side, we also review sources such as the US FDA device databases and safety communications, published clinical guidelines and peer reviewed wound care journals, and trade and customs statistics where relevant for wound care device and dressing flows. Company annual reports, investor presentations, and press releases are used to map product ranges and typical price movements, and then a paid subscription for company financials and news helps cross-check revenue direction and major portfolio changes. The sources listed here are illustrative and not exhaustive, and many other references were also consulted to collect data, validate assumptions, and clarify the final analysis.

Primary Interviews and Surveys

Primary work is used to test what desk research cannot fully answer, mainly around real world adoption, pricing bands, and how the treatment mix shifts by ulcer stage and care setting. We speak with a mix of clinical stakeholders and procurement facing respondents, plus distributors and manufacturer side product specialists, covering major regions so geography assumptions can be adjusted and then rechecked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 18% | APAC: 51% |

| Mid tier: 55% | Functional/Unit leaders: 24% | EMEA: 29% |

| Smaller Players: 20% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where prevalence and treated patient pools are converted into demand by care setting, and then converted to value using typical treatment pathways and pricing. We map the treated pool by ulcer stage mix and setting of care (acute hospitals, long term care, and home care), and then apply usage patterns for dressings, devices, and active therapies, which are valued using average selling price ranges.

To keep totals realistic, results are corroborated using selective bottom-up checks such as supplier revenue direction, channel feedback on unit movement, and sampled volume times ASP for key categories like dressings and negative pressure systems. Inputs that matter in the model include aging population trends, long term care bed capacity, pressure ulcer incidence and length of stay signals, adoption of advanced dressings and adjunct therapies, and ASP changes driven by product upgrades and tender cycles. Forecasting uses scenario analysis supported by expert views on adoption and reimbursement pressure, with gap handling done through conservative assumptions where category level public data is thin and then revalidated in follow up calls.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as procedure volumes, facility capacity trends, and reported wound care spending patterns, and then outliers are investigated before sign off. When a mismatch is seen, we revisit assumptions like stage mix, utilization per patient, and pricing ranges, and then recontact sources if the variance is material.

Each dataset and calculation is reviewed in steps, starting from unit logic and moving to value logic, so errors do not get carried forward. The report is refreshed annually, and interim updates are triggered when major regulatory, reimbursement, or product availability events change the treatment mix. Before delivery, a final update pass is completed so clients receive the latest view based on newly available public releases and confirmed expert inputs.

Mordor Intelligence's Pressure Ulcers Treatment Market Size Versus Other Published Estimates

Published market sizes for pressure ulcer treatment often differ because studies do not always line up on what is counted, which year is treated as the base, and how prices are carried forward in the forecast. Differences also come from whether values reflect manufacturer level pricing or downstream margins, and whether adjacent wound categories are mixed into the total.

A big swing factor is the update timing, because currency conversion points and annual price revisions can change the reported total even when underlying patient volumes look similar. This is controlled through scheduled refresh checks and repeated ASP validation in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.31 B (2026) | |

| Trade Publisher A | USD 5.38 B (2024) | Uses an earlier base year and emphasizes manufacturer level (factory gate) value, and it also appears to include a wider set of related goods and services such as pressure relieving mattresses and ancillary therapies, which can shift the total depending on what is counted. |

| Industry Tracker B | USD 7.00 B (2025) | Uses a different base year and longer forecast horizon, and it groups product and treatment types more broadly, which can raise totals if advanced and traditional categories are combined without consistent price normalization across regions. |

The spread in the table is mainly explained by base year selection, what is included around adjacent wound care goods, and how pricing is normalized over time. By keeping the scope linked to treatment use and then rechecking adoption and pricing inputs during reviews, we arrive at a balanced number that can be traced back to clear demand and price drivers.

Key Questions Answered in the Report

What is the current size of the pressure ulcer treatment market?

The pressure ulcer treatment market size is USD 6.31 billion in 2026 and is forecast to reach USD 8.31 billion by 2031, growing at a 5.67% CAGR.

Which product segment is growing fastest?

Negative pressure wound therapy is expanding most rapidly at an 8.02% CAGR through 2031, driven by portable single-use systems and favorable reimbursement.

Why is Asia-Pacific showing the highest regional growth?

Asia-Pacific’s 8.34% CAGR reflects rising surgical volumes, expanding insurance coverage, and accelerated adoption of advanced wound-care technologies.

How are value-based reimbursement models influencing purchasing decisions?

Hospitals face significant penalties for hospital-acquired pressure injuries, prompting investments in predictive technologies and active therapies that reduce incidence rates.

What is the outlook for home-based pressure ulcer care?

Home-care settings are forecast to grow at an 7.95% CAGR as telehealth, remote-monitoring platforms, and portable NPWT devices enable effective treatment outside hospitals.

Page last updated on: