Skin Antiseptic Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.39 Billion |

| Market Size (2031) | USD 5.97 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skin Antiseptic Products Market Analysis by Mordor Intelligence

The skin antiseptic products market size was valued at USD 4.13 billion in 2025 and is estimated to grow from USD 4.39 billion in 2026 to reach USD 5.97 billion by 2031, at a CAGR of 6.34% during the forecast period (2026-2031). Hospitals are intensifying infection-prevention protocols, ambulatory surgery centers are gaining volume, and outpatient care models in the Asia-Pacific and the Gulf Cooperation Council are drawing capital into single-use formats. Continuous declines in central line-associated bloodstream infections and catheter-associated urinary tract infections, coupled with 40–60% cost savings in freestanding surgery centers, encourage formulary expansions for broad-spectrum agents. Supply-chain disruptions for chlorhexidine gluconate and volatile organic compound regulations in Europe prompt diversification into iodine and alcohol-free alternatives, while antimicrobial peptide research signals future product differentiation.[1]Centers for Disease Control and Prevention, “2023 National and State Healthcare-Associated Infections Progress Report,” CDC, cdc.gov Against this backdrop, the skin antiseptic products market is poised for steady growth as infection-control mandates tighten and procedural volumes rise across both high- and middle-income economies.

Key Report Takeaways

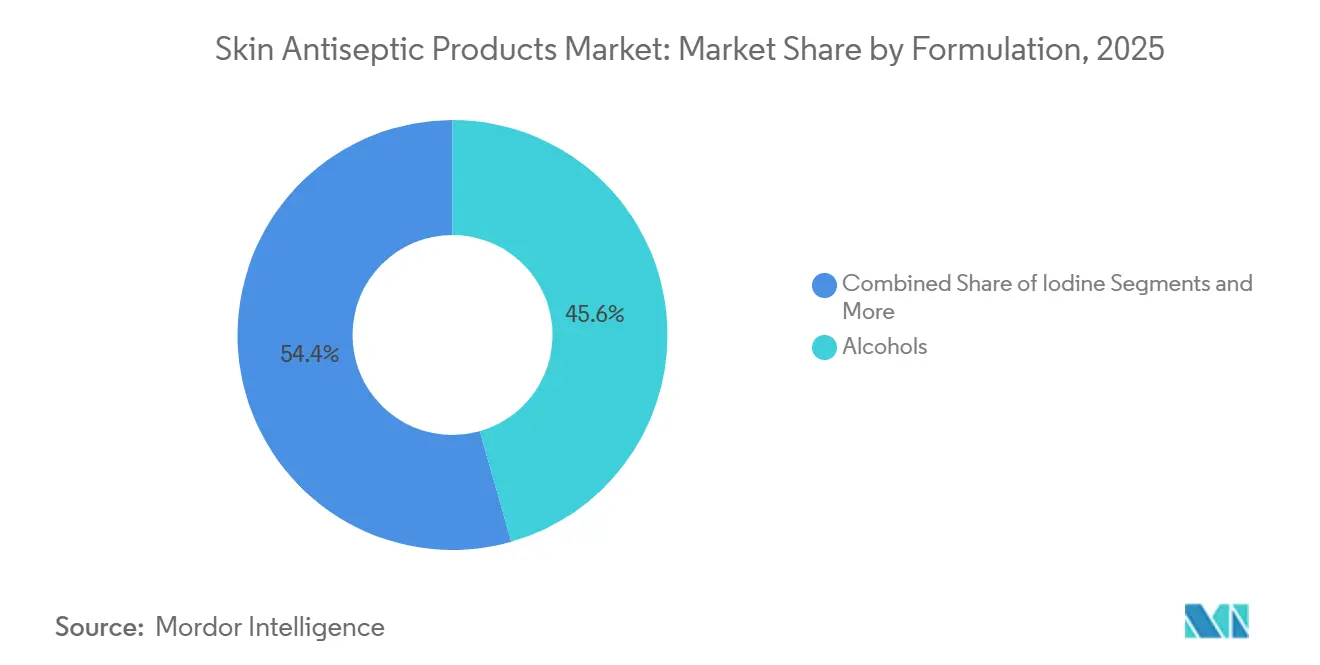

- By formulation, alcohol-based agents led with 45.59% revenue share in 2025, whereas iodine formulations are forecast to expand at a 7.21% CAGR through 2031.

- By type, solutions commanded 52.34% of 2025 revenue, while wipes are projected to grow at a 7.32% CAGR over the same horizon.

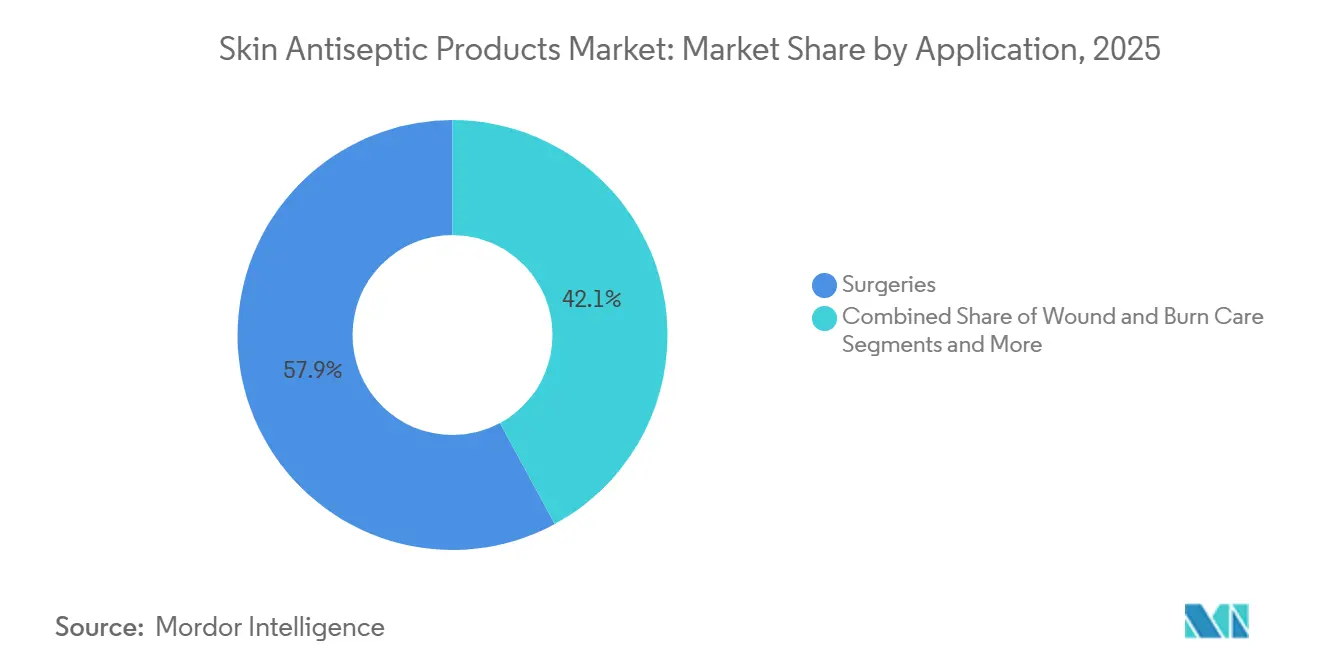

- By application, surgeries contributed 57.89% of demand in 2025, yet injection and catheter site preparation is advancing at a 7.35% CAGR to 2031.

- By end-user, hospitals held 48.44% of 2025 revenue, whereas home-care and telehealth settings are set to rise at a 7.41% CAGR.

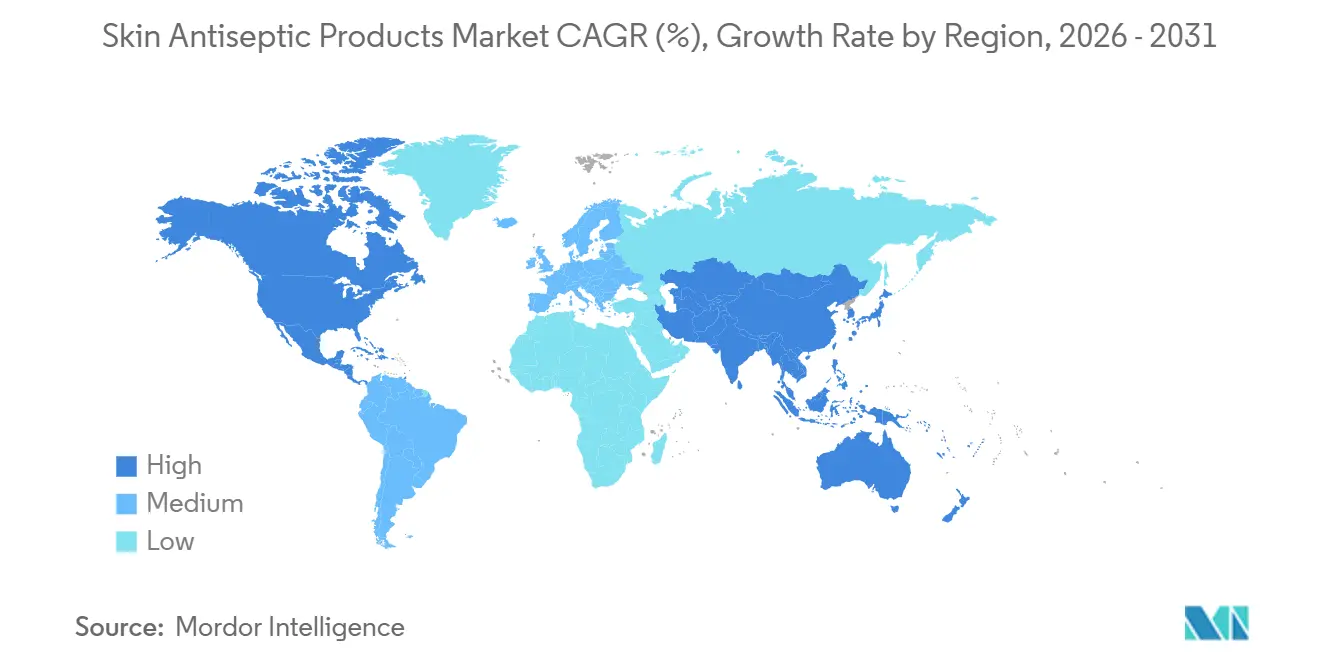

- By geography, North America accounted for 38.39% of 2025 revenue, while Asia–Pacific is expected to deliver the fastest 7.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Skin Antiseptic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hospital-acquired infections | +1.2% | Global, with acute focus in North America and Europe | Medium term (2-4 years) |

| Increasing number of surgical and minimally-invasive procedures | +1.1% | APAC core, spill-over to Middle East and Latin America | Long term (≥ 4 years) |

| Expansion of outpatient and ambulatory surgery centers in emerging markets | +0.9% | Asia-Pacific, GCC, Brazil, Argentina | Medium term (2-4 years) |

| Surge in adoption of ready-to-use single-use applicators and wipes | +0.8% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Regulatory push for alcohol-free long-acting formulations | +0.6% | Europe (EU BPR), North America (FDA guidance) | Medium term (2-4 years) |

| Development of antimicrobial-peptide and nanoparticle skin antiseptics | +0.4% | North America and Europe (R&D hubs), future global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hospital-Acquired Infections

Hospital-acquired infections cost U.S. providers USD 28.4 billion each year and still affect roughly 1 in 31 in-patients despite recent gains. Central line and catheter infection declines of 13% and 11% between 2022 and 2023 demonstrate the value of standardized skin preparation, yet multidrug-resistant organisms such as carbapenem-resistant Enterobacteriaceae and Candida auris keep pressure on antiseptic purchasing. Chlorhexidine bathing reached 90% U.S. penetration in 2024, up from 7% a decade earlier, affirming hospital commitment to broad-spectrum agents. Global antimicrobial-resistance action plans embed skin antisepsis as a front-line defense, underpinning predictable demand in the skin antiseptic products market. Financial penalties tied to infection metrics further entrench procurement in North America and Europe.

Increasing Number of Surgical and Minimally-Invasive Procedures

China carried out 65.2 million surgeries in 2023, and India’s procedural count is growing 8–10% annually as facilities expand into tier-2 cities. Laparoscopic and robotic systems require meticulous skin preparation despite smaller incisions, pushing antiseptic orders in Japan, South Korea, and the Middle East. More than 1 million reconstructive procedures were logged in 2024 by U.S. plastic surgeons, with 56% inside hospitals, underscoring the enduring role of acute-care facilities. These volumes anchor long-term expansion of the skin antiseptic products market, especially in Asia–Pacific where procedure growth outpaces GDP.

Expansion of Outpatient and Ambulatory Surgery Centers in Emerging Markets

The United States hosts over 6,100 ambulatory surgery centers that cut costs by up to 60%, a model now exported to Saudi Arabia, the United Arab Emirates, and Brazil.[2]American Hospital Association, “Ambulatory Surgery Centers: Trends and Statistics 2024,” AHA, aha.org Medicare reimbursement updates and private-equity funding accelerate center rollouts, while Vision 2030 budgets drive facility construction across the Gulf. India’s urban districts are developing day-surgery hubs even as national rules mature. Single-use wipes and applicators dominate ASC formularies, propelling short-cycle replenishment in the skin antiseptic products market.

Surge in Adoption of Ready-to-Use Single-Use Applicators and Wipes

Becton, Dickinson and Company secured multiple 510(k) clearances for ChloraPrep devices that include dye indicators to verify coverage, reducing variability during surgery. U.S. Food and Drug Administration guidance reinforces one-time-use expectations, and European institutions mirror the practice to satisfy infection audits. Hospitals report better compliance with contact-time standards when nurses use pre-filled devices. Asia–Pacific tenders increasingly specify wipes to lower cross-contamination. These dynamics produce a near-term lift for single-use segments within the skin antiseptic products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin irritation and allergic reactions to certain actives | -0.5% | Global, with heightened sensitivity reporting in North America and Europe | Short term (≤ 2 years) |

| Stricter VOC and biocide regulations limiting alcohol content | -0.4% | Europe (EU BPR, ECHA), North America (EPA, FDA) | Medium term (2-4 years) |

| Rise of antiseptic-tolerant microbial strains in ICU settings | -0.3% | Global, concentrated in high-acuity ICUs | Long term (≥ 4 years) |

| Supply-chain risk for high-purity chlorhexidine API | -0.3% | Global, with acute impact in North America due to FDA shortage notifications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skin Irritation and Allergic Reactions to Certain Actives

Chlorhexidine hypersensitivity cases reported to MedWatch climbed in 2024, including episodes of anaphylaxis after surgical prep.[3]U.S. Food and Drug Administration, “Drug Shortages: Chlorhexidine Gluconate,” FDA, accessdata.fda.gov Hospitals now screen for allergies and stock povidone-iodine as an alternative, while alcohol-based products cause dryness that hampers compliance in home care. These issues curb usage in chronic settings, nudging suppliers to create emollient-rich or alcohol-free variants. The restraint shaves near-term growth for the skin antiseptic products market but also sparks formulation innovation.

Stricter VOC and Biocide Regulations Limiting Alcohol Content

European and U.S. regulations restrict ethanol levels and demand environmental risk assessments, forcing reformulation or withdrawal of high-alcohol products. Smaller firms struggle with compliance costs, allowing multinationals to consolidate share. Portfolio rationalization is underway, trimming some legacy stock-keeping units. The regulatory squeeze is a medium-term brake on the skin antiseptic products market yet establishes a pathway for compliant, premium-priced offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Iodine Strengthens Amid Resistance Concerns

Alcohol-based agents contributed 45.59% of the skin antiseptic products market share in 2025, yet iodine agents are forecast to grow 7.21% per year through 2031 as hospitals hedge against Candida auris and chlorhexidine-tolerant strains. Povidone-iodine’s broad spectrum and minimal resistance potential attract formulary committees, and recent 510(k) clearances for iodine applicators validate safety in U.S. theaters. The skin antiseptic products market size for iodine formulations is therefore set to widen as Europe enforces volatile-organic-compound limits and Asia–Pacific diversifies supply.

Broader wound-healing compatibility positions iodine for chronic-care uptake, and its supply chain is less geographically concentrated than chlorhexidine. Benzalkonium chloride fills smaller alcohol-free niches, while hydrogen peroxide solutions appeal where non-staining properties are crucial. Collectively, these shifts indicate a balanced product mix that buffers the skin antiseptic products market against single-ingredient shortages.

By Type: Wipes Improve Compliance and Safety

Multi-dose solutions captured 52.34% of 2025 revenue, maintaining popularity in high-throughput operating rooms that prize low cost per use. However, wipes are expanding at a 7.32% CAGR, driven by audit evidence showing higher adherence to recommended contact times. The skin antiseptic products market size attributed to wipes is growing quickly inside ambulatory surgery centers that emphasize rapid turnover and sterile-barrier integrity.

Visual dye indicators on applicators and foil-pouched wipes reduce variance in technique, satisfying infection-control teams under intense scrutiny. Spray and foam dispensers fulfill large-area or self-application needs but remain niche. In home care, patients favor wipe packs for intuitive use and reduced spill risk, adding an incremental growth layer to the skin antiseptic products market.

By Application: Catheter Site Preparation Gathers Momentum

Surgical site prep accounted for 57.89% of 2025 volumes, yet catheter and injection sites are advancing 7.35% yearly as guidelines prescribe chlorhexidine-alcohol for vascular access. Medicare penalty structures sharpen focus on central line infections, expanding spend on dedicated applicators for peripheral lines as well. Catheter prep thus anchors the fastest incremental contribution to the skin antiseptic products market.

Wound and burn care benefits from iodine’s tissue-friendly profile, broadening demand outside the operating theater. Consumer personal hygiene remains a stable, lower-acuity niche. Together, these patterns ensure that skin antiseptic products market share remains skewed toward clinical procedures even as outpatient and chronic-care settings rise.

By End-User: Home Care and Telehealth Accelerate

Hospitals still represented 48.44% of 2025 revenue, but hospital-at-home programs and remote monitoring lift home-care growth to 7.41% through 2031. Telehealth platforms embed antiseptic reminders, and caregiver kits include ready-to-use wipes to offset training gaps. The skin antiseptic products market size linked to home settings is therefore widening rapidly.

Ambulatory surgery center counts keep rising, cementing procurement pipelines for single-use formats. Long-term and urgent-care facilities add steady baseline demand. End-user diversification bodes well for resilience in the skin antiseptic products market during macroeconomic swings.

Geography Analysis

North America generated 38.39% of 2025 revenue as Medicare penalties drove strict infection targets, and more than 6,100 ambulatory surgery centers ordered single-use devices to standardize practice. Active U.S. Food and Drug Administration oversight spurred rapid iteration in applicator design, while Canadian provinces added antiseptic compliance checks to surgical safety lists. Chlorhexidine shortages in 2024 triggered supplier diversification, reinforcing iodine uptake across leading hospital systems.

Europe’s skin antiseptic products market contends with Biocidal Products Regulation constraints on volatile organic compounds, pushing alcohol-free innovation. Germany, the United Kingdom, France, Italy, and Spain are early movers on benzalkonium chloride adoption, whereas Eastern European facilities weigh cost over sustainability. Environmental mandates also boost recycling-ready applicators that appeal to procurement teams under circular-economy targets. Established multinationals dominate, but niche startups address neonatal and dermatology needs with specialized blends.

Asia–Pacific posts the fastest 7.45% CAGR thanks to China’s 65.2 million annual surgeries, India’s double-digit procedure growth, and Japan’s aging population that requires chronic wound care. South Korea’s medical tourism regulations ensure Joint Commission International-aligned infection controls, and Australia’s Therapeutic Goods Administration approval pathway serves as a regional gatekeeper. Concentrated chlorhexidine production creates both cost leverage and supply vulnerability, prompting hospitals to dual-source whenever possible. Emerging Southeast Asian markets, notably Vietnam and the Philippines, gain access via new regional distribution centers, broadening addressable demand for the skin antiseptic products market.

Competitive Landscape

Global suppliers hold advantageous formulary spots, yet the skin antiseptic products market remains moderately consolidated rather than dominated by a single player. Becton, Dickinson and Company capitalizes on its ChloraPrep franchise with integrated dye applicators, reinforcing presence in high-volume operating rooms. Solventum, spun off from 3M in January 2025, directs capital exclusively toward infection-prevention lines, signaling renewed competition for surgical prep spend.

Cardinal Health and Medline compete on private-label economics, offering chlorhexidine and povidone-iodine lines at discounts for group-purchasing organizations. Ecolab bundles surface disinfection and skin prep under enterprise contracts, deepening account stickiness across hospitals and ambulatory centers. In Europe, Mölnlycke’s alcohol-free chlorhexidine applicators meet volatile-organic-compound limits and carve out share in sustainability-focused facilities.

Future white-space revolves around peptide and nanoparticle research, alcohol-free long-acting formats, and home-care-friendly packs. Mid-sized innovators such as Schülke & Mayr and PDI aim at neonatal or long-term-care niches, while digital integrations that verify application technique create new value layers. As hospital systems consolidate, suppliers able to produce real-world infection-reduction data are best positioned to hold ground in the evolving skin antiseptic products market.

Skin Antiseptic Products Industry Leaders

Becton, Dickinson & Co.

Ecolab Inc.

Johnson & Johnson (Ethicon)

Solventum

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ecolab opened additional production lines for alcohol-based antiseptics in Singapore, enhancing supply resilience for Asia Pacific customers.

- February 2025: B. Braun obtained United States Food and Drug Administration clearance for a film-forming povidone-iodine designed for regional anesthesia, expanding its procedural-specific portfolio.

- January 2025: Johnson & Johnson (Ethicon) finalized a USD 120 million acquisition of a niche antiseptic-technology firm, signaling continued convergence between device platforms and antimicrobial science.

- December 2024: BD launched an updated chlorhexidine-impregnated dressing aimed at reducing central-line infections in critical-care environments.

Global Skin Antiseptic Products Market Report Scope

As per the scope of the report, skin antiseptic products encompasses formulations designed to disinfect the skin and reduce microbial presence, primarily before surgical procedures or other medical interventions. These products aim to reduce or eliminate microorganisms on the skin, minimizing the risk of infection.

The Skin Antiseptic Products Market is segmented by Formulation (Alcohols, Chlorhexidine Gluconate, Iodine & Iodophors, Hydrogen Peroxide, Octenidine, Quaternary Ammonium Compounds, and Other Formulations), Product Type (Solutions, Swab Sticks, Wipes, Gels, Sprays & Foams, Creams & Ointments, and Bathing Kits & Applicators), Application (Pre-Operative Surgery Preparation, Injections & Venipuncture, Catheter Insertion & Maintenance, Dialysis & Blood Collection, Wound Care & First Aid, and Neonatal & Obstetric Care), End User (Hospitals, Ambulatory Surgical Centers and Emergency Medical Services (EMS), Clinics & Physician Offices, Dialysis Centers, Home-Care Settings, and Long-Term Care Facilities), Distribution Channel (Hospital Pharmacies, Retail & Drug Stores, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America).

| Alcohols |

| Chlorhexidine |

| Iodine |

| Other Formulations |

| Solutions |

| Swab Sticks |

| Wipes |

| Sprays & Foams |

| Surgeries |

| Injection and Catheter site preparation |

| Wound & Burn Care |

| Non-clinical Personal Hygiene |

| Hospitals |

| Ambulatory Surgery Centres |

| Home-care and Tele-health |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Formulation | Alcohols | |

| Chlorhexidine | ||

| Iodine | ||

| Other Formulations | ||

| By Type | Solutions | |

| Swab Sticks | ||

| Wipes | ||

| Sprays & Foams | ||

| By Application | Surgeries | |

| Injection and Catheter site preparation | ||

| Wound & Burn Care | ||

| Non-clinical Personal Hygiene | ||

| By End-User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Home-care and Tele-health | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the skin antiseptic products market?

The market was valued at USD 4.39 billion in 2026 and is forecast to rise to USD 5.97 billion by 2031.

Which formulation is expanding fastest through 2031?

Iodine-based antiseptics are projected to grow at a 7.21% CAGR due to broad antimicrobial coverage and regulatory tailwinds.

Why are wipes gaining popularity in procedural settings?

Single-use wipes improve compliance, cut cross-contamination risk, and align with audit standards in ambulatory surgery centers.

Which region is expected to log the highest growth rate?

Asia–Pacific is set to achieve a 7.45% CAGR as surgical volumes climb and outpatient infrastructure expands.

What factor most threatens supply stability for chlorhexidine products?

Quality-control failures at key API plants in China and India triggered FDA shortage notices, elevating procurement risk.

How are regulations shaping product innovation in Europe?

The Biocidal Products Regulation is driving the shift toward alcohol-free, long-acting formulations that meet volatile-organic-compound limits.

Page last updated on: