Varicose Ulcer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

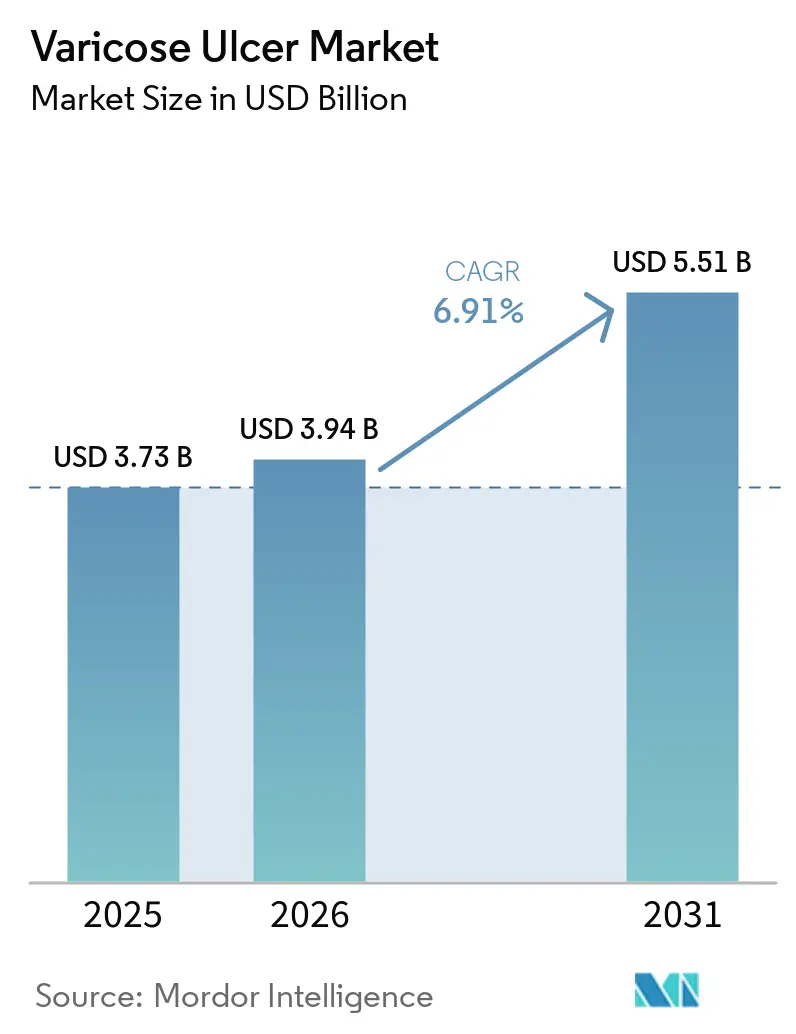

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Varicose Ulcer Market Analysis by Mordor Intelligence

The Varicose Ulcer Market size is expected to grow from USD 3.73 billion in 2025 to USD 3.94 billion in 2026 and is forecast to reach USD 5.51 billion by 2031 at 6.91% CAGR over 2026-2031.

Sustained interest in early-ablation protocols and multilayer compression sustains the core of the varicose ulcer market, while connected wound imaging and remote triage create faster escalation pathways that pull through higher-value dressings and procedural care. Digital wound assessment and care coordination solutions are expanding quickly as providers embed image analytics into routine documentation and population health workflows across home health and ambulatory settings. Despite compression therapy holding the leading share in 2025, adherence shortfalls and reimbursement boundaries curb growth, which leaves space for patient-friendly adaptive wraps and intermittent pneumatic compression to evolve in selected subpopulations. Geographic momentum splits between a volume-heavy North America and a faster-growing Asia-Pacific, where capacity build-outs and policy-led investments upgrade access to vascular interventions and standardized compression programs.

Key Report Takeaways

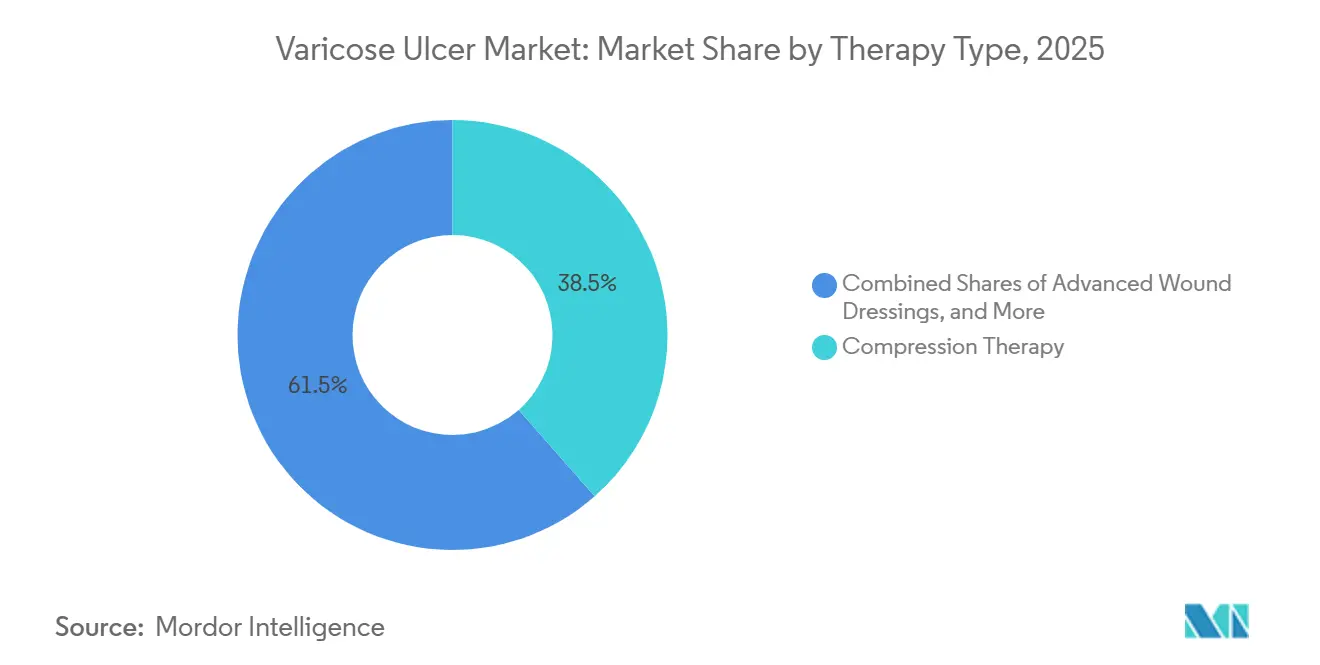

- By therapy type, compression therapy led with 38.50% of revenue in 2025, while digital wound assessment and care coordination tools are projected to expand at a 10.26% CAGR through 2031.

- By ulcer severity stage, stage 2: complicated VLU led with 43.45% in 2025, while stage 3: refractory/high risk VLU are projected to expand at a 9.56% CAGR through 2031.

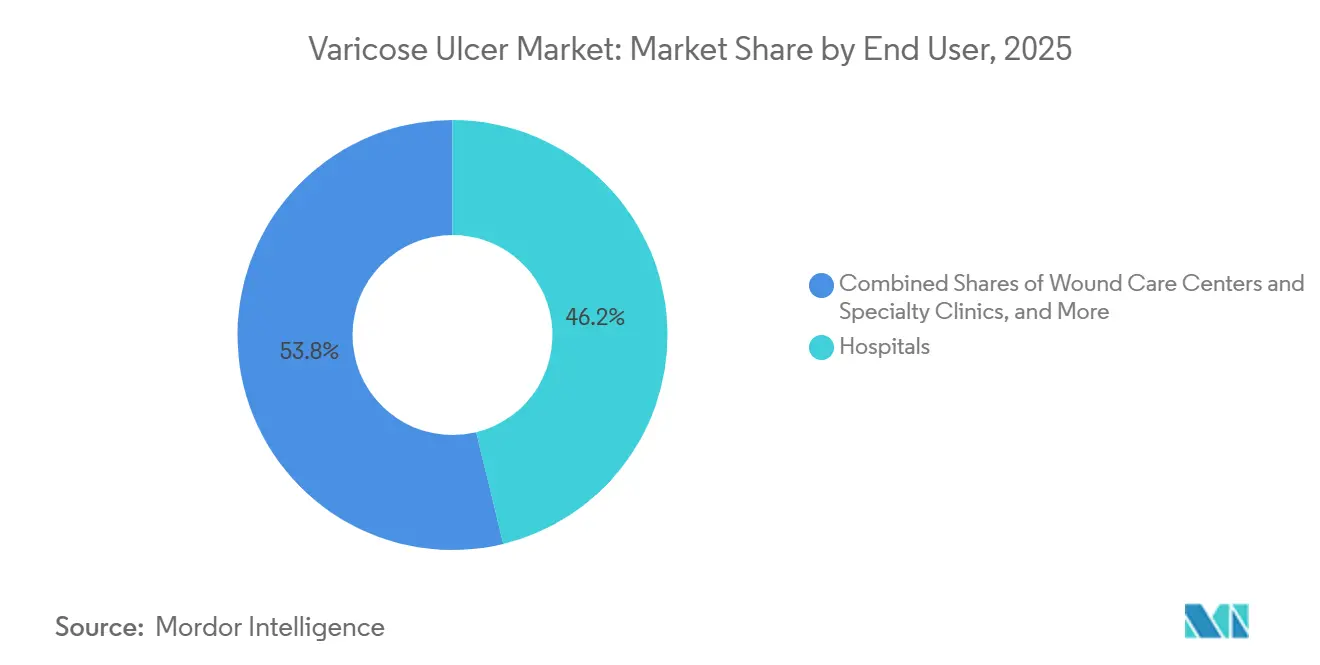

- By end user, acute-care institutions held a 46.20% share in 2025, while home healthcare and community nursing recorded the highest growth at a 9.10% rate.

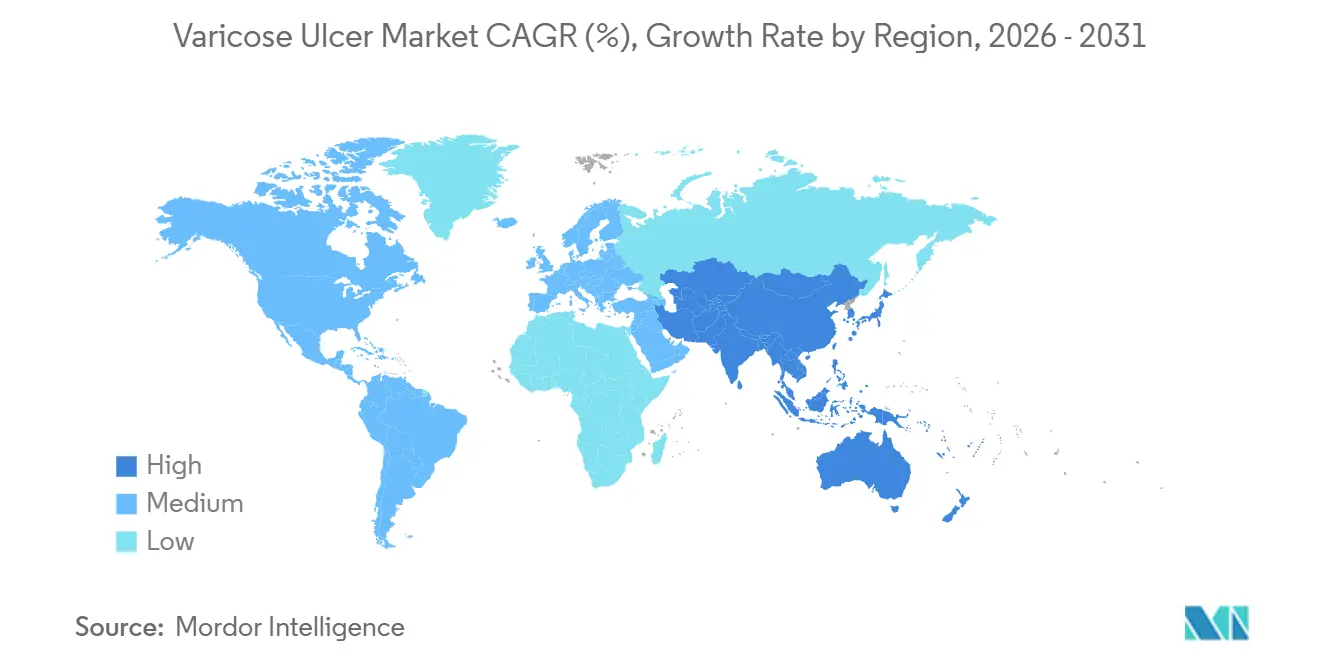

- By geography, North America accounted for 41.30% share in 2025, and Asia-Pacific is projected to grow at a 10.06% rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Varicose Ulcer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Populations With Rising Chronic Venous Disease Burden Expand VLU Caseloads | +2.1% | Global, with peak gains in North America, Europe, and APAC urban hubs (Japan, South Korea, Australia) | Long term (≥ 4 years) |

| Evidence-Based Care Pathways Endorsing Early Ablation Plus Compression Accelerate Healing (EVRA/NICE) | +1.4% | Europe & North America core, spill-over to Latin America and Middle East | Medium term (2-4 years) |

| Penetration Of Advanced Dressings And Antimicrobial Technologies For Exudate And Infection Control | +1.2% | Global | Short term (≤ 2 years) |

| Shift To Outpatient And Home-Based Wound Care Increases Addressable Treatment Volumes | +1.0% | APAC core, with early gains in Indonesia, India; Europe via NHS pathway reforms | Medium term (2-4 years) |

| Digital Wound Imaging And AI Documentation Drive Earlier Escalation And Product Uptake | +0.9% | North America and UK first-movers, APAC telehealth integration (China, Australia), EU following | Short term (≤ 2 years) |

| Expansion Of Office-Based Vein Clinics/ASCs Broadens Access To Definitive Venous Interventions | +0.7% | National (US), with emerging pilots in Canada, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Populations With Rising Chronic Venous Disease Burden Expand VLU Caseloads

Incidence and complexity of venous leg ulcers rise with age, with prevalence estimates in older cohorts far exceeding the working-age population, which places persistent demand on compression therapies, dressings, and definitive venous procedures that define the varicose ulcer market[1]Mölnlycke Health Care, “Ulcères veineux de jambe, compréhension clinique et épidémiologie,” Mölnlycke, molnlycke.com. France recorded a large diagnosed base, with hundreds of thousands of patients requiring long-term management, which underscores how the varicose ulcer market intersects with primary care and community nursing workloads. Germany’s current guidance details clinical workflows for diagnostics and treatment while highlighting resource use that includes ongoing compression, specialized dressings, and venous interventions, reflecting system-level cost pressures that favor early, evidence-based closure strategies.

Japan’s latest practice guideline emphasizes that elderly patients with limited mobility are at heightened risk because calf-muscle-pump insufficiency and venous reflux reinforce stasis, making multidisciplinary approaches more effective than stand-alone wound clinics. This demographic shift increases case volumes in both hospital and home settings, which supports the need for standardized protocols that combine timely duplex ultrasound, early reflux correction, and sustained compression in daily practice.

Evidence-Based Care Pathways Endorsing Early Ablation Plus Compression Accelerate Healing (EVRA/NICE)

Randomized evidence has moved venous intervention from late-stage rescue to early-phase standard in eligible patients, with the EVRA trial showing higher 24-week healing when ablation precedes conservative care, and the ESCHAR data documenting lower long-term recurrence when reflux is addressed instead of compression alone. Clinical guidelines in Europe now favor early treatment of superficial reflux using radiofrequency or laser thermal ablation, or newer non-thermal options, once duplex confirms pathologic reflux, which shortens overall treatment courses and reduces repeat episodes for the varicose ulcer market.

Operational capacity remains a friction point because scheduling delays erode the early-intervention advantage, as shown by NHS program data that motivated pathway redesigns to create direct referral routes from community nurses to vascular teams. A nurse-led model tested by an academic medical center consolidated visits and accelerated assessment times, improving both patient experience and clinical throughput without adding new staff. Health systems that front-load ablation costs often harvest downstream savings from fewer nursing visits, reduced dressing changes, and lower recurrence, aligning clinical and financial incentives within expanding value-based contracts for the varicose ulcer market

Penetration Of Advanced Dressings And Antimicrobial Technologies For Exudate And Infection Control

Heavy exudate and periwound skin breakdown complicate compression adherence, so absorbent foams, hydrofiber matrices, and antimicrobial dressings remain essential in day-to-day care pathways that underpin the varicose ulcer market. Newer dressings aim to address multiple complications at once, as in Smith+Nephew’s ALLEVYN COMPLETE CARE, which has a five-layer design reported to lock away more than 99% of bacteria and absorb a high proportion of mechanical energy, positioning the product to command premiums where infection control and pressure injury prevention overlap[2]Smith+Nephew, “Smith+Nephew Launches Next-Generation ALLEVYN COMPLETE CARE Foam Dressing,” Smith+Nephew, smith-nephew.com. Trial-driven differentiation remains influential, evidenced by Organogenesis reporting that PuraPly AM achieved a significant primary endpoint in randomized data, which supports positioning for complex exudative wounds that challenge standard foam dressings.

Under compression, hydrofiber dressings can maintain structure while managing high fluid loads, a practical advantage for community nurses tasked with fewer dressing changes per week in resource-constrained settings. The mix of absorbency, bacterial sequestration, and wear time continues to define procurement decisions for home health and wound centers, encouraging suppliers to pair material innovations with training on correct application and change intervals that fit local staffing realities.

Shift To Outpatient And Home-Based Wound Care Increases Addressable Treatment Volumes

Capacity constraints and value-based purchasing steer chronic VLU care toward home health and ambulatory models, where interoperable photography and AI-supported measurement help clinicians escalate cases earlier and avoid preventable visits, which supports sustainable growth for the varicose ulcer market. Digital platforms report high monthly imaging volumes across thousands of facilities and reductions in documentation time, allowing senior nurses to supervise larger caseloads and reallocate time to complex patients.[3]Swift Medical, “Home Health Digital Wound Imaging Measurement Utilization,” Swift Medical, swiftmedical.com

Home-based workflows can compress assessment-to-decision timelines, which matches the push by hospital systems to reduce emergency visits while keeping chronic wound episodes on track for timely closure. Community nursing teams continue to bear much of the VLU workload, so solutions that reduce dressing change frequency or ease self-care improve adherence to compression, which indirectly raises the return on standardized pathways for the varicose ulcer market. Many payers now accept remote documentation and photo evidence to validate progression, which aligns data capture with reimbursement logic in both public and private programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor Adherence To Compression And High Recurrence Weaken Real-World Outcomes | -1.3% | Global | Long term (≥ 4 years) |

| Reimbursement Scrutiny And Variable Coverage For Skin Substitutes/CTPs Curb Utilization | -0.9% | North America core, Europe selective, APAC fragmented | Medium term (2-4 years) |

| Community Nursing Workforce Constraints Limit Compression Changes And Complex Dressings | -0.6% | Europe & North America, APAC urban hubs (Japan, Australia) | Short term (≤ 2 years) |

| Limited High-Quality RCT Evidence For Several Adjuncts (E.G., NPWT) Hinders Broad Adoption | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Poor Adherence To Compression And High Recurrence Weaken Real-World Outcomes

Compression is the clinical foundation for healing and preventing recurrence, yet adherence often falls over time, which raises relapse risk and drives repeat treatment episodes in the varicose ulcer market. Evidence syntheses report that stronger-class stockings can reduce reulceration risk compared to lighter compression but also tend to have higher noncompliance rates, which offsets a portion of the clinical gain in everyday practice[4]Cochrane Collaboration, “Compression Therapy to Prevent Recurrence of Venous Leg Ulcers,” Cochrane, cochrane.org. Reviews for clinicians echo that recurrence can be lowered when correct pressure grades are maintained, but many patients abandon tighter garments due to donning difficulty and discomfort.

This adherence gap motivates interest in self-adjusting compression wraps and in-home pneumatic devices for selected patients who cannot tolerate stockings, although the latter are typically reserved for higher-acuity cases under durable medical equipment programs. Providers that pair education, correct sizing, and early follow-up tend to see more sustained compression use, which translates into fewer recurrences and more predictable episode costs for the varicose ulcer market.

Reimbursement Scrutiny And Variable Coverage For Skin Substitutes/CTPs Curb Utilization

U.S. Medicare policy narrowed the list of cellular and tissue-based products eligible for coverage and introduced application limits and uniform payment rates that shape case selection, encourage evidence generation, and temper short-term volume growth for the varicose ulcer market. Companies reported alignment with the final coverage determinations while highlighting the need for randomized data with standard endpoints to maintain access under the new rules.

Health systems also face administrative workload from prior-authorization requirements, which now often demand photo evidence and documentation of standard-of-care failure before approval. In Europe, coverage for biologics remains selective, and many pathways require case-by-case review or formal technology appraisals before formulary adoption, which constrains rapid scale-up and reinforces the centrality of compression and cost-effective advanced dressings. Japan’s conditional approval track supports earlier launches for regenerative products but includes multi-year real-world data obligations that add lifecycle costs and focus attention on post-market outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Multi-Front Competition Fragments Traditional Dominance

Compression therapy commanded 38.5% of 2025 revenue, anchoring the varicose ulcer market even as commoditization pressures margins and shifts differentiation toward patient education, correct application, and clinician training. Advanced dressings held the second-largest share, with hydrofiber and antimicrobial-embedded foams positioned for fewer changes and stronger exudate control under compression, which can justify premium positioning when they reduce clinician workload and complications. Digital wound assessment and care coordination tools are the fastest-growing therapy group at a 10.26% CAGR, and the varicose ulcer market size for these platforms is benefiting from SaaS models that tie revenue to documented patient volumes and outcomes within risk-bearing provider contracts. Venous interventions such as endovenous thermal ablation and non-thermal closure techniques treat reflux directly, and randomized evidence shows better healing and lower recurrence when ablation complements compression in eligible patients.

In higher-infection-risk cases, bioactive dressings may reduce nurse callbacks by controlling bioburden and safeguarding periwound skin, which supports procurement despite budget oversight in hospital and community settings. Across dressings, hydrofiber matrices maintain structural integrity when saturated under compression, preventing lateral strike-through and supporting longer wear, which is valuable in home settings with fewer scheduled visits. Foam dressings remain widely used due to ease of handling and relative affordability, but clinical differentiation narrows over time, encouraging formulary decisions that prioritize total episode value rather than brand alone. Biologic and tissue-based products offer high per-case revenue potential but now face clear evidence thresholds and application caps in the United States that push manufacturers to invest in randomized trials and health economics to sustain access.

By Ulcer Severity Stage: Refractory Cases Drive Premium Therapy Adoption

Stage 2 captured 43.45% of 2025 revenue, which reflects that many patients present with venous eczema, lipodermatosclerosis, or moderate exudate that require coordinated care beyond basic compression and generic dressings. In this cohort, escalation protocols that add antimicrobial dressings, initiate venous ablation in eligible patients, or move from Class 2 to higher compression have documented success in standard pathways, which keeps resource utilization concentrated in weekly nursing visits and duplex surveillance for the varicose ulcer market.

The varicose ulcer market size for Stage 3 is projected to expand at 9.56% as coverage frameworks now channel biologics reimbursement and advanced interventions toward refractory cases under defined criteria in the United States. This acuity shift concentrates formulary spending where randomized evidence is strongest and aligns with hospital-based wound center workflows that manage complex comorbidities and infection risk. Japan’s updated guidance reinforces compression and endorses early intervention for confirmed reflux, which helps reduce the pool of refractory cases when escalation is timely and documented.

By End User: Home Healthcare Ascendancy Reshapes Revenue Pools

Hospitals accounted for 46.2% of 2025 spending as they control access to advanced imaging, inpatient procedures, and complex wound protocols that shape purchasing in the varicose ulcer market. Wound care centers and specialty clinics manage multidisciplinary care for complicated ulcers, but bundled payment pressures encourage standardized dressings and judicious biologic use to safeguard margins.

Home healthcare and community nursing represent the fastest-growing end-user channel at a 9.10% rate as programs adopt interoperable imaging and standardized documentation to support reimbursement and quality objectives. Digital wound assessment platforms reduce documentation time and enable remote triage by senior clinicians, which expands caseload capacity without proportional staffing increases and benefits the varicose ulcer market when credentialed evidence of progression is required by payers.

Ambulatory surgical centers and office-based labs continue to draw candidates for endovenous ablation and foam sclerotherapy, offering appointments outside traditional hospital schedules and aligning with patient preference for convenience. Hospitals maintain an advantage for high-acuity cases where deep-vein imaging, surgical debridement, or inpatient negative pressure therapy is required.

Geography Analysis

North America held 41.3% of revenue in 2025, anchored by broad coverage for compression, advanced dressings, and office-based venous procedures that sustain the varicose ulcer market’s largest regional base. U.S. policy supports ablation and duplex imaging in ambulatory settings, and device makers report strong closure durability that complements compression and shortens time to healing in appropriate patients. Health systems continue to normalize remote wound monitoring within chronic care management, which assists documentation and escalation decisions without adding in-person visits. Canada’s provincial variation influences formulary breadth and pace of adoption for higher-cost options, which keeps purchasing focused on compression and cost-effective dressings in many settings.

Europe accounted for a significant global revenue, with Germany, France, and the United Kingdom representing a large share of the regional total. Germany’s guidance codifies workflows that drive high initiation rates for compression and venous procedures among diagnosed patients, reflecting an emphasis on evidence-based closure and structured follow-up to contain long-episode costs. France reports a sizable diagnosed population that absorbs community nursing resources and shapes budget planning for local health authorities. In the United Kingdom, pathway reforms have focused on direct referrals from community nurses to vascular assessment to cut wait times and consolidate appointments into single-visit workflows, improving healing rates and patient experience. Southern and Eastern European markets show cautious adoption of biologics and variable access to endovenous procedures, which keeps compression and dressings at the center of procurement decisions for the varicose ulcer market.

Asia-Pacific is projected to grow at a 10.06% rate, with policy support for reflux correction and compression programs expanding access in urban centers across high-population countries. Japan’s updated clinical practice guidelines endorse compression plus early laser treatment when indicated, and clinics report that combining compression with venous intervention increases healing compared to compression alone. Australia, South Korea, and several Southeast Asian systems are extending reimbursement for venous imaging and minimally invasive closure, which supports steady case growth in ambulatory sites and expands the accessible base for the varicose ulcer market.

Competitive Landscape

The varicose ulcer market shows moderate concentration in advanced dressings and biologics, where a small cluster of multinational manufacturers holds a sizable portion of global revenue, while compression therapy and digital platforms remain more fragmented with many regional and venture-backed entrants. Strategic moves continue to expand portfolios and tighten integration between devices, dressings, and digital tools, as seen in Solventum’s acquisition of Acera Surgical to add synthetic matrices alongside negative pressure therapy offerings. Evidence-led positioning is now essential in biologics because U.S. Medicare narrowed coverage for cellular and tissue-based products and introduced uniform payment and application caps, which concentrate demand among products with strong randomized data and robust real-world evidence.

Companies that document superiority against standard care at accepted endpoints signal higher resilience under the updated reimbursement framework, as reflected in trial updates for leading amniotic or collagen matrices. Digital-first wound platforms scale through SaaS contracts that monetize per-patient-per-month and embed into home health and ambulatory documentation, with clinical validation and imaging accuracy across diverse skin tones now central to provider due diligence in the varicose ulcer market. Overall, competition favors companies that combine evidence-backed products with workflow tools and training that lift adherence and speed to closure, which is the practical currency of value-based wound care for the varicose ulcer market.

Varicose Ulcer Industry Leaders

Essity Health & Medical

Solventum

Smith+Nephew

Mölnlycke AB

Convatec Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smith+Nephew launched the next-generation ALLEVYN COMPLETE CARE foam dressing in the United States, reporting a five-layer construction that locks more than 99% of bacteria away from the wound bed and absorbs up to 93% of mechanical energy, with claims of reduced hospital-acquired pressure injury risk and extended wear times.

- December 2025: Solventum completed the acquisition of Acera Surgical, adding the Restrata synthetic tissue matrix to its MedSurg portfolio and expanding participation in U.S. acute wound treatment through a mix of devices and bioactive matrices.

Global Varicose Ulcer Market Report Scope

As per the scope of the market, the varicose ulcer (venous leg ulcer) market encompasses products, procedures, and services used for the diagnosis, treatment, and long‑term management of chronic ulcers arising from varicose veins or chronic venous insufficiency. The market includes compression therapies, advanced wound dressings, biologics and cellular/tissue‑based products, adjunctive wound therapies, venous interventions, and digital wound assessment and care‑coordination solutions delivered across hospital, outpatient, and home‑care settings.

The varicose ulcer market is segmented by therapy type, which comprises compression therapy, including multilayer compression systems, dual-layer ulcer stocking kits, intermittent pneumatic compression devices, and advanced wound dressings, which include foam, alginate, hydrocolloid, hydrofiber/CMC, and others. Also, the therapy type segment includes biologics/cellular & tissue-based products, which incorporate living cell constructs, amniotic/chorionic membranes, xenografts, adjunctive therapies, including NPWT, enzymatic debridement, topical growth factors, venous interventions include endovenous thermal ablation, non-thermal non-tumescent (cyanoacrylate, moca), foam sclerotherapy, and lastly digital wound assessment & care coordination tools.

By ulcer severity stage includes uncomplicated VLU, complicated VLU, and refractory/high-risk VLU. Additionally, the market is further segmented into end user that comprises of hospitals, wound care centers & specialty clinics, home healthcare & community nursing, others (ASCs & office-based labs). Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Compression Therapy | Multilayer Compression Systems |

| Dual-Layer Ulcer Stocking Kits | |

| Intermittent Pneumatic Compression Devices | |

| Advanced Wound Dressings | Foam Dressings |

| Alginate Dressings | |

| Hydrocolloid Dressings | |

| Hydrofiber/CMC Dressings | |

| Others (Antimicrobial Dressing,Contact Layers And Secondary Dressings) | |

| Biologics / Cellular & Tissue-based Products (CTPs) | Living cell constructs |

| Amniotic/ Chorionic Membranes | |

| Xenografts | |

| Adjunctive Therapies | Negative Pressure Wound Therapy |

| Enzymatic Debridement Agents | |

| Topical Growth Factors | |

| Venous Interventions | Endovenous Thermal Ablation |

| Non-thermal Non-tumescent (cyanoacrylate, MOCA) Technique | |

| Foam Sclerotherapy | |

| Digital wound assessment & care coordination tools |

| Stage 1: Uncomplicated VLU |

| Stage 2: Complicated VLU |

| Stage 3: Refractory/High-risk VLU |

| Hospitals |

| Wound Care Centers & Specialty Clinics |

| Home Healthcare & Community Nursing |

| Others (Ambulatory surgical centers (ASCs) & office-based labs (OBLs/vein clinics)) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Compression Therapy | Multilayer Compression Systems |

| Dual-Layer Ulcer Stocking Kits | ||

| Intermittent Pneumatic Compression Devices | ||

| Advanced Wound Dressings | Foam Dressings | |

| Alginate Dressings | ||

| Hydrocolloid Dressings | ||

| Hydrofiber/CMC Dressings | ||

| Others (Antimicrobial Dressing,Contact Layers And Secondary Dressings) | ||

| Biologics / Cellular & Tissue-based Products (CTPs) | Living cell constructs | |

| Amniotic/ Chorionic Membranes | ||

| Xenografts | ||

| Adjunctive Therapies | Negative Pressure Wound Therapy | |

| Enzymatic Debridement Agents | ||

| Topical Growth Factors | ||

| Venous Interventions | Endovenous Thermal Ablation | |

| Non-thermal Non-tumescent (cyanoacrylate, MOCA) Technique | ||

| Foam Sclerotherapy | ||

| Digital wound assessment & care coordination tools | ||

| By Ulcer Severity Stage | Stage 1: Uncomplicated VLU | |

| Stage 2: Complicated VLU | ||

| Stage 3: Refractory/High-risk VLU | ||

| By End User | Hospitals | |

| Wound Care Centers & Specialty Clinics | ||

| Home Healthcare & Community Nursing | ||

| Others (Ambulatory surgical centers (ASCs) & office-based labs (OBLs/vein clinics)) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the varicose ulcer market?

The varicose ulcer market size was USD 3.37 billion in 2025 and is expected to reach USD 5.51 billion by 2031 at a 6.91% CAGR.

Which therapy segment leads and which grows the fastest in the varicose ulcer market?

Compression therapy led with 38.5% share in 2025, while digital wound assessment and care coordination tools are projected to grow at a 10.26% rate through 2031.

How is the end-user mix evolving within the varicose ulcer market?

Hospitals held 46.2% of revenue in 2025, but home healthcare and community nursing is the fastest riser with a 9.1% growth rate as digital documentation and remote triage scale.

Which region accounts for the largest share and which is expanding the fastest?

North America accounted for 41.3% share in 2025, and Asia-Pacific has the fastest trajectory with a 10.06% growth rate through 2031.

What clinical advances are shaping treatment pathways in the varicose ulcer market?

Early endovenous ablation plus compression improves time to healing and reduces recurrence versus compression alone in eligible patients, which is now embedded in leading guidelines.

What factors most constrain real-world outcomes?

Compression nonadherence and variable coverage for cellular and tissue-based products limit consistent healing, reinforcing the need for adherence support and stronger clinical evidence.

Page last updated on: