United States Ultomiris Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

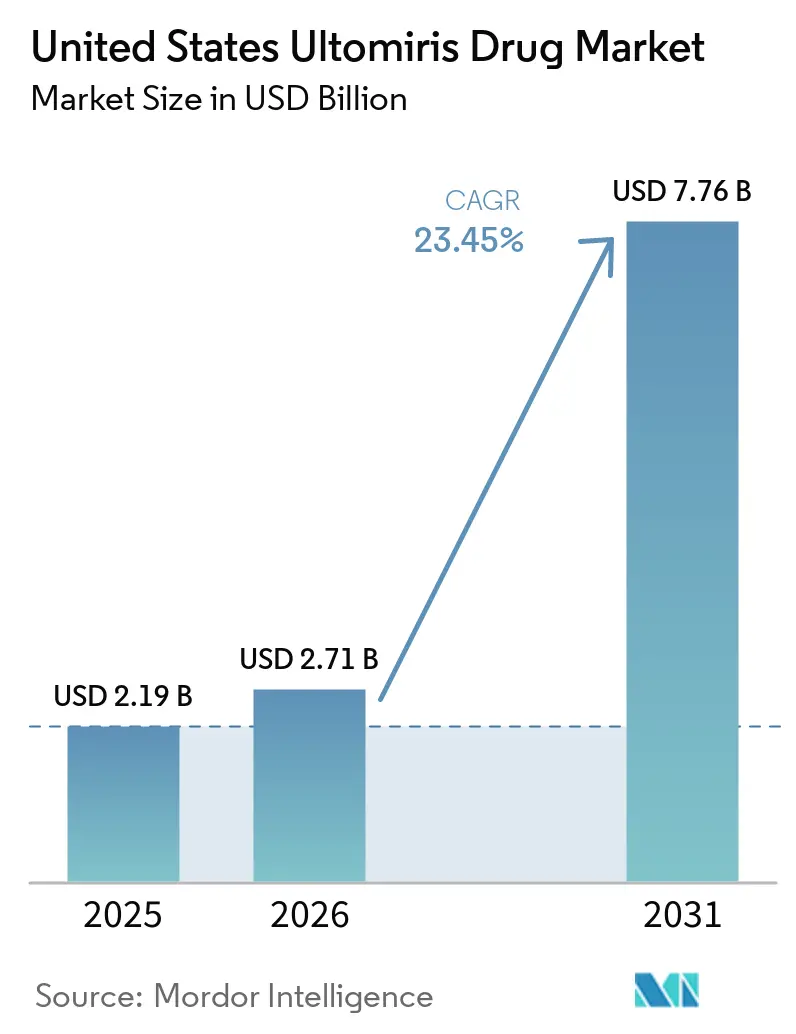

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 7.76 Billion |

| Growth Rate (2026 - 2031) | 23.45% CAGR |

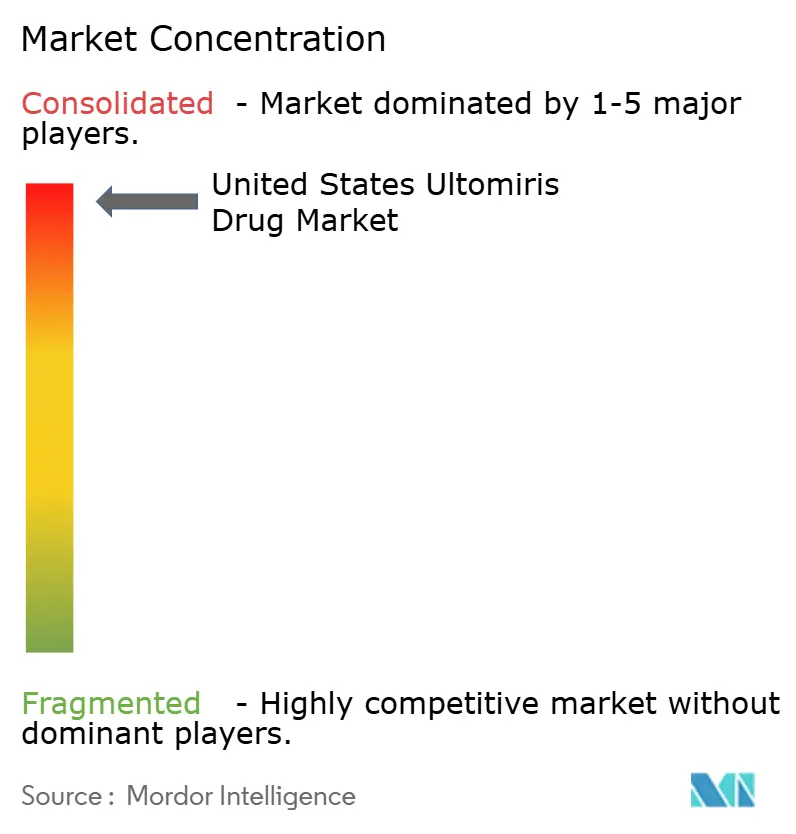

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Ultomiris Drug Market Analysis by Mordor Intelligence

The United States Ultomiris Drug Market size was valued at USD 2.19 billion in 2025 and is estimated to grow from USD 2.71 billion in 2026 to reach USD 7.76 billion by 2031, at a CAGR of 23.45% during the forecast period (2026-2031).

The market is expanding well above its earlier pace because label expansion into neurology has widened the treated base faster than underlying disease incidence can grow in these ultra-rare conditions. Its commercial position also reflects a major shift in treatment economics, because every-8-week intravenous dosing lowers infusion frequency versus eculizumab and makes long-term use easier for patients and treatment centers. The United States Ultomiris drug market continues to benefit from conversion from Soliris, and AstraZeneca reported that 2025 U.S. growth was supported by both patients new to branded therapy and switching across approved indications. At the same time, payer management is becoming tighter as commercial plans use biosimilar eculizumab products in step therapy frameworks, which can slow initiation even when demand remains intact. The United States Ultomiris drug market also remains shaped by specialist-led access, because REMS obligations and meningococcal risk monitoring keep prescribing concentrated in hematology, nephrology, and neurology settings with established rare disease workflows.

Key Report Takeaways

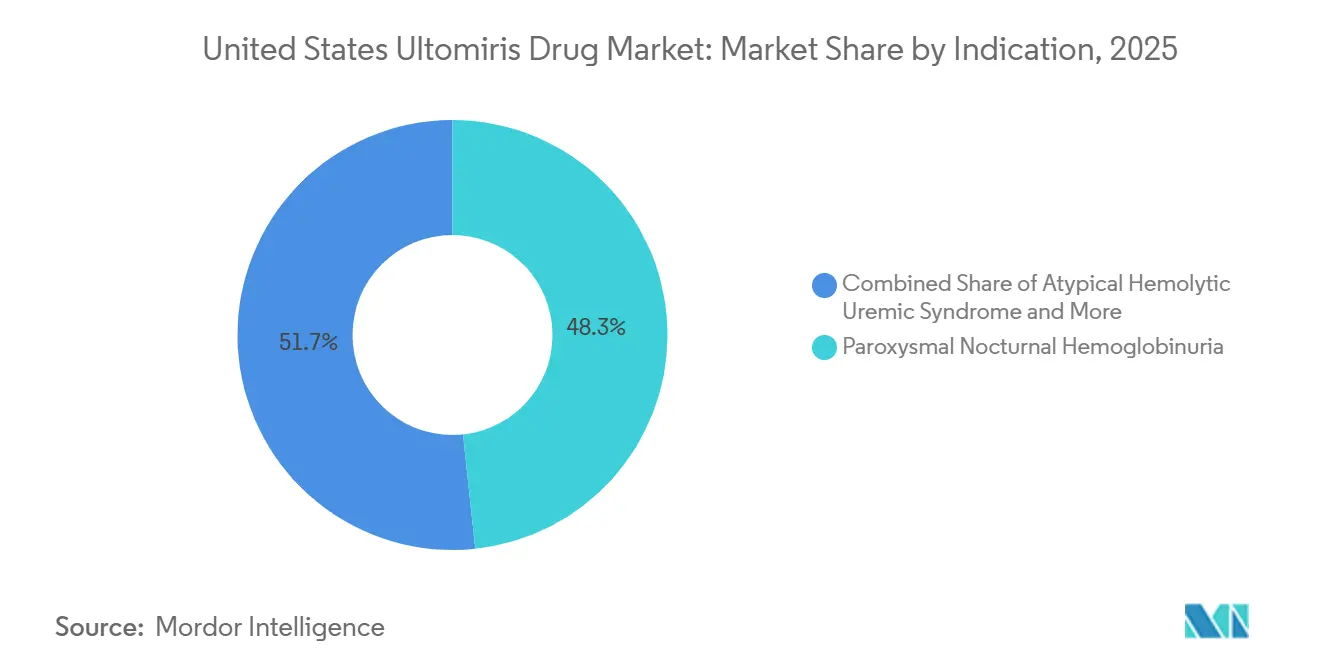

- By indication, PNH held 48.31% of the market in 2025, while gMG is forecast to expand at a 24.38% CAGR from 2026 to 2031.

- By end use, adults accounted for 61.24% of the market in 2025, while the pediatric segment is projected to grow at a 24.52% CAGR through 2031.

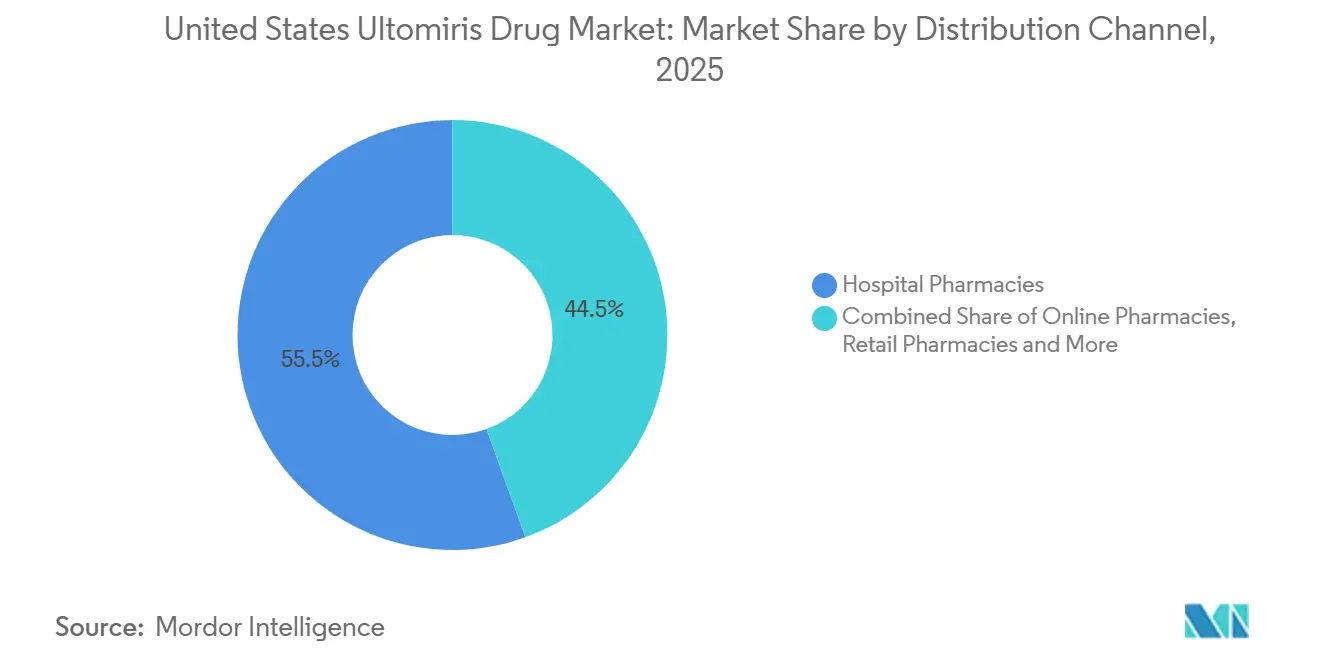

- By distribution channel, hospital pharmacies held 55.52% of the market in 2025, while online pharmacies are projected to grow at a 25.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Ultomiris Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended Dosing Interval and Lower Treatment Burden | +3.8% | National, with highest concentration in Northeast and West Coast academic medical centres | Short term (≤ 2 years) |

| Expanding Approved Indications in Hematology and Neurology | +5.5% | National | Medium term (2-4 years) |

| Conversion From Soliris to Ultomiris in Established Patients | +4.2% | National | Short term (≤ 2 years) |

| SC Self-Administration Expands Site-of-Care Flexibility | +1.6% | National, with notable gains among geographically dispersed patients in the South and Midwest | Medium term (2-4 years) |

| Broader Diagnostic Capture in Rare Complement-Mediated Diseases | +2.4% | National, with early gains concentrated in high-volume tertiary referral centres | Long term (≥ 4 years) |

| Near-Term Pipeline Readouts Could Expand Nephrology Use Cases | +2.9% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Dosing Interval and Lower Treatment Burden

The United States Ultomiris drug market benefits from ravulizumab’s every-8-week intravenous maintenance schedule, which reduces annual treatment visits to 6 to 7 compared with 26 for eculizumab under a biweekly approach. That change matters in daily practice because fewer visits reduce scheduling strain for patients, caregivers, infusion centers, and physician offices that already manage rare and complex cases. In the United States Ultomiris drug market, this lower treatment burden supports persistence, which is especially important in diseases where therapy is long term and discontinuation can have serious clinical consequences[1]U.S. Food and Drug Administration, “ULTOMIRIS (ravulizumab-cwvz) Prescribing Information,” FDA, fda.gov. The value of that convenience is stronger in working-age populations, and the claims-based U.S. analysis placed the median age for treated PNH patients at 40 years. The dosing advantage has therefore moved from being a product attribute to a practical benchmark for how new C5 therapies are judged in routine care.

Expanding Approved Indications in Hematology and Neurology

The United States Ultomiris drug market is supported by 4 active FDA-approved indications, PNH, aHUS, gMG, and NMOSD, which gives ravulizumab broader label coverage than any other single C5 inhibitor in the country. This breadth matters because growth in ultra-rare biologics depends more on moving into adjacent indications than on underlying epidemiology alone. In gMG, post-approval uptake is being reinforced by ongoing real-world registry updates that remain consistent with the durable outcomes seen in the CHAMPION MG clinical program. In NMOSD, trial results showed a 98.9% relative relapse risk reduction versus placebo, which gives prescribers and payers a strong rationale in a condition where a single relapse can cause lasting disability. Across the United States Ultomiris drug market, the combined hematology and neurology label now acts as the main engine for future patient additions.

Conversion From Soliris to Ultomiris in Established Patients

The United States Ultomiris drug market still draws major support from conversion from Soliris, even though the original conversion wave has already advanced across the installed base. AstraZeneca stated that 2025 U.S. Ultomiris growth was driven by both patients new to branded medicines and continued conversion from Soliris across indications, while Soliris declined in parallel. That pattern matters because it shows the switch has become part of standard care rather than a one-time launch event. Health systems also favor the transition because fewer administrations reduce operational steps tied to pharmacy handling, infusion throughput, and repeated claims processing. As a result, the United States Ultomiris drug market still behaves like a conversion story in hematology while neurology adds the next layer of demand.

SC Self-Administration Expands Site-of-Care Flexibility

The United States Ultomiris drug market is also broadening through the subcutaneous on-body delivery option for adult PNH patients, which adds a different care pathway to a product that was historically tied to infusion settings. This matters most in areas where infusion access is limited, because treatment can move closer to the home and reduce dependence on hospital-based outpatient centers. The benefit is especially relevant for rural and semi-rural populations in the South and Midwest, where site-of-care access can delay treatment even after diagnosis. It also supports the forecast rise in online pharmacy fulfillment, because a self-administered format is more compatible with specialty pharmacy workflows than intravenous administration. In the United States Ultomiris drug market, the channel effect from subcutaneous dosing is therefore becoming a distribution shift as well as a patient convenience shift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Annual Therapy Cost and Payer Scrutiny | -2.8% | National, with restrictive formulary management most acute in Medicaid-dependent states | Medium term (2-4 years) |

| Serious Meningococcal Infection Risk and REMS Burden | -1.2% | National | Short term (≤ 2 years) |

| Small Patient Pool Across Approved Orphan Indications | -1.5% | National | Long term (≥ 4 years) |

| Infusion and Prior Authorization Friction in Specialty Care | -1.0% | National, with highest friction in rural and community-based practices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Annual Therapy Cost and Payer Scrutiny

Cost remains a direct brake on the United States Ultomiris drug market because treated patients generate very high annual spending under both public and commercial coverage. The analysis reported total PNH-related costs of USD 660,533 in year 1 and USD 633,984 in subsequent years, which shows how drug, monitoring, and care intensity combine into a difficult payer burden. Commercial plans are responding by tightening utilization controls, and UnitedHealthcare’s 2026 complement inhibitor policy places biosimilar eculizumab products inside the decision path for new treatment starts[2]UnitedHealthcare, “Complement C5 Inhibitors, Commercial Medical Benefit Drug Policy,” UHC Provider, uhcprovider.com. That does not eliminate class demand, but it can delay therapy initiation and shift the timing of revenue recognition inside a plan year. The United States Ultomiris drug market therefore faces a ceiling from payer affordability even while underlying clinical demand remains strong.

Serious Meningococcal Infection Risk and REMS Burden

The United States Ultomiris drug market is also constrained by the safety infrastructure required for terminal complement inhibition. The CDC states that complement inhibitor use raises meningococcal disease risk by up to 2,000-fold versus the general population, which keeps vaccination and counseling requirements central to prescribing. The shared Ultomiris and Soliris REMS, modified in February 2025, requires prescriber enrollment, patient counseling, vaccination documentation, and distribution of a Patient Safety Card that remains valid for 8 months after discontinuation. Real-world ravulizumab infection rates were lower than historical eculizumab rates, but the burden of compliance remains meaningful, especially outside specialist centers. In the United States Ultomiris drug market, this keeps initiation concentrated among clinicians already familiar with REMS processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication, PNH anchors revenue while neurology drives incremental growth

PNH held 48.31% of the indication mix in 2025, which gave it the largest position in the United States Ultomiris drug market share at the indication level. That lead reflects the longest reimbursement history, the deepest prescriber familiarity, and the most established treatment workflows for complement inhibition. The analysis also described a diagnosed prevalent U.S. PNH population of 6,200 cases and noted that only 30% of insured patients had historically been captured on complement inhibitor therapy, which shows why PNH revenue remains driven by price per treated patient rather than by large patient numbers. Within the United States Ultomiris drug industry, that concentration leaves PNH commercially important but also more exposed to biosimilar-related payer pressure than newer uses.

Generalized myasthenia gravis is projected to record the fastest indication growth at a 24.38% CAGR from 2026 to 2031, and that pace reflects broader eligibility and growing neurologist familiarity after FDA approval. The United States Ultomiris drug market size for gMG is rising because real-world registry updates continue to support durable outcomes aligned with the clinical program AAN2025. NMOSD remains smaller on patient volume because treatment is limited to AQP4 antibody-positive disease, yet its clinical severity gives the product a strong value case when relapse prevention can preserve long-term function. Across the United States Ultomiris drug industry, orphan exclusivity and the lack of near-term biosimilar competition in gMG and NMOSD support continued expansion of neurology-based revenue.

By End Use, adults remain dominant while pediatric demand rises from label breadth

Adults accounted for 61.24% of the 2025 market, which represented the largest share of the United States Ultomiris drug market size by end use. This dominance reflects the fact that gMG and NMOSD are adult-only approvals, while adult PNH and aHUS populations also represent the larger treated base. The adult segment therefore remains the financial core of the product, especially because diagnosis, specialist access, and reimbursement tend to be more established in adult care settings. In the United States Ultomiris drug market, adult demand also benefits from a care model already embedded in hematology and neurology centers with experience in long-term complement inhibition.

The pediatric cohort is forecast to grow at a 24.52% CAGR through 2031, supported by label coverage that extends to patients as young as 1 month for PNH and aHUS. This makes pediatrics the faster-moving part of the United States Ultomiris drug market share trend by end use, even though it starts from a smaller base. Pediatric growth is being helped by broader recognition of complement-mediated thrombotic microangiopathy in young aHUS patients and by more routine genetic workups in pediatric nephrology. The offset is reimbursement, because Medicaid and CHIP exposure is higher in children, which can slow conversion from diagnosis to treatment even when clinical need is clear.

By Distribution Channel, hospital pharmacies retain scale while online pharmacies gain traction

Hospital pharmacies commanded 55.52% of 2025 distribution value, giving them the largest position in the United States Ultomiris drug market share by channel. That outcome was consistent with a therapy base still centered on infusion delivery, hospital-affiliated outpatient centers, and specialist oversight at treatment initiation. The hospital setting also aligns with REMS-linked workflows, vaccination verification, and the buy-and-bill structure long used for high-cost biologics in rare disease care. Retail pharmacies remain secondary because the product’s administration profile and monitoring needs still limit broad conventional pharmacy use.

Online pharmacies are projected to grow at a 25.25% CAGR from 2026 to 2031, making them the fastest-growing channel in the United States Ultomiris drug market size outlook by distribution mode. That shift is tied to the on-body subcutaneous option, which is more compatible with specialty pharmacy fulfillment and home-based care than repeated infusion visits. It also fits wider payer and provider interest in moving eligible biologic use away from hospital outpatient settings when clinical supervision needs are manageable. Over time, the United States Ultomiris drug market should therefore remain hospital-led in value while online and specialty pharmacy models claim a larger share of incremental growth.

Geography Analysis

The United States Ultomiris drug market is entirely domestic in scope, and its size reflects the country’s combination of broad label access, specialist capacity, and high-value reimbursement for rare disease biologics. The United States Ultomiris drug market growth shows how strongly the U.S. system monetizes treated orphan disease populations[3]AstraZeneca, “AstraZeneca Results, FY and Q4 2025,” AstraZeneca Investor Relations, astrazeneca.com. This scale is driven less by unusually high disease prevalence and more by reimbursement conditions that support premium biologic pricing. That same pricing structure creates long-term pressure because U.S. payers are becoming more active in comparing value and tightening access rules for complement inhibitors. As a result, national growth remains strong, but it is increasingly shaped by access management rather than by clinical demand alone.

Within the country, treatment access is concentrated in states with dense specialist networks and large academic medical centers. The Northeast, including Massachusetts, New York, and Pennsylvania, and the West Coast, including California and Washington, host a large share of hematology, nephrology, and neuromuscular expertise needed for complement inhibitor use. These geographies are better positioned to manage REMS requirements, complex reimbursement, and multidisciplinary diagnosis pathways. In contrast, rural and Medicaid-heavy parts of the South and Midwest face longer diagnostic timelines and thinner infusion infrastructure. This is why the subcutaneous option has higher practical relevance in underserved regions, where site-of-care flexibility can translate into real access gains.

State Medicaid variation adds another layer of unevenness across the United States Ultomiris drug market. States with broader rare disease coverage and clearer reimbursement pathways tend to convert eligible patients faster than states with tighter prior authorization rules. The difference is especially important in pediatric aHUS, where public coverage exposure is higher and treatment delays can follow from state-level budget constraints. Federal policy changes are starting to ease some cost pressure for Medicare beneficiaries, but state Medicaid heterogeneity remains a structural barrier to uniform national uptake. Alexion’s field reimbursement support helps reduce friction, yet it cannot fully offset restrictive local formularies or limited specialist supply.

Competitive Landscape

The United States Ultomiris drug market remains highly concentrated because AstraZeneca’s Alexion unit is the sole marketing authorization holder for ravulizumab in the country. Even so, competition is increasing at the class level as payers and rival manufacturers seek lower-cost or more flexible alternatives. UnitedHealthcare’s 2026 complement inhibitor policy shows this shift clearly, because biosimilar eculizumab products sit inside the payer decision framework for new treatment starts.

AstraZeneca’s defense in the United States Ultomiris drug market rests first on label breadth, because ravulizumab is approved across PNH, aHUS, gMG, and NMOSD. That breadth reduces dependence on any single indication and gives the company a wider clinical footprint than rivals focused on narrower use cases. The second advantage is embedded specialist workflow, since REMS familiarity and existing center experience make switching less automatic than payer spreadsheets might suggest. The third advantage is pipeline extension, and AstraZeneca’s April 2026 I CAN announcement showed that the company is actively trying to move ravulizumab into IgA nephropathy with accelerated filing plans in key markets. That pipeline move matters because renal disease would widen the opportunity base more than incremental share gains inside current labels.

Company actions since 2025 also show a strategy built around data reinforcement and access defense. AstraZeneca highlighted new rare neurology data at the 2025 AAN Annual Meeting, which supports prescriber confidence in gMG and NMOSD use after approval. Teva and Samsung Bioepis, by contrast, focused on commercial launch activity for EPYSQLI, which strengthens payer negotiating power even where ravulizumab remains clinically favored. The resulting landscape is not broad in the number of ravulizumab suppliers, but it is getting harder on access and pricing terms. The United States Ultomiris drug market should therefore remain monopolized at the product level while becoming more contested at the therapeutic class level.

United States Ultomiris Drug Industry Leaders

AstraZeneca PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AstraZeneca announced positive interim Phase III results from the I CAN trial (ALXN1210-IgAN-320) evaluating Ultomiris in adults with IgAN at risk of disease progression. AstraZeneca planned to file for accelerated approval in key regulatory markets. The primary eGFR endpoint will be assessed at week 106.

- February 2025: FDA approved a modification to the Ultomiris and Soliris REMS, updating prescriber and patient counseling requirements and implementing system-level changes to the shared REMS administration infrastructure. The modification reflects ongoing pharmacovigilance data on meningococcal infection management and consolidates both products under a unified risk management program.

United States Ultomiris Drug Market Report Scope

As per the scope of the report, Ultomiris (ravulizumab-cwvz) is a prescription drug used to treat paroxysmal nocturnal hemoglobinuria (PNH), atypical hemolytic uremic syndrome (aHUS), and others. It helps prevent blood cell destruction and organ damage associated with these conditions.

The United States Ultomiris drug market is segmented by medical condition into paroxysmal nocturnal hemoglobinuria, atypical hemolytic uremic syndrome, generalized myasthenia gravis, and neuromyelitis optica spectrum disorder. By patient age, the market is divided into adult and pediatric categories. By sales channel, it is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. For each segment, the market size and forecast are provided in terms of value (USD).

| Paroxysmal Nocturnal Hemoglobinuria |

| Atypical Hemolytic Uremic Syndrome |

| Generalized Myasthenia Gravis |

| Neuromyelitis Optica Spectrum Disorder |

| Adult |

| Pediatric |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| By Indication | Paroxysmal Nocturnal Hemoglobinuria |

| Atypical Hemolytic Uremic Syndrome | |

| Generalized Myasthenia Gravis | |

| Neuromyelitis Optica Spectrum Disorder | |

| By End Use | Adult |

| Pediatric | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the projected value of the United States Ultomiris drug market by 2031?

The United States Ultomiris drug market is projected to reach USD 7.76 billion by 2031 from USD 2.19 billion in 2025, at a 23.45% CAGR over 2026 to 2031.

Which indication contributes the most revenue for Ultomiris in the United States?

PNH held the largest indication share at 48.31% in 2025 because it has the longest reimbursement history and the deepest prescriber familiarity.

Which patient group is growing fastest for Ultomiris use?

The pediatric cohort is projected to expand at a 24.52% CAGR through 2031, supported by label coverage for patients as young as 1 month in PNH and aHUS.

Why is gMG expected to grow faster than other indications?

GMG is forecast to grow at a 24.38% CAGR through 2031 as neurologists gain more experience and real-world registry data continue to support durable treatment outcomes.

What is the biggest access challenge for Ultomiris in the United States?

High treatment cost and payer scrutiny remain the biggest access constraints, and commercial plans are increasingly using biosimilar eculizumab within step-therapy pathways for new starts.

How is the distribution model changing for Ultomiris therapy?

Hospital pharmacies still led with 55.52% of 2025 value, but online pharmacies are expected to grow at a 25.25% CAGR through 2031 as the subcutaneous option supports more specialty pharmacy and home-based fulfillment.

Page last updated on: