Analgesics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 54.29 Billion |

| Market Size (2031) | USD 76.87 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analgesics Market Analysis by Mordor Intelligence

The Analgesics Market size was valued at USD 50.65 billion in 2025 and is estimated to grow from USD 54.29 billion in 2026 to reach USD 76.87 billion by 2031, at a CAGR of 7.20% during the forecast period (2026-2031).

Stricter opioid regulations are driving prescribers, hospitals, and payers to adopt multimodal care and non-opioid treatment options for acute and chronic conditions. Advancements in transdermal delivery, topical systems, and targeted formulations are enhancing competition by emphasizing safety, convenience, and adherence over potency. Distribution patterns are shifting as digital pharmacy access expands self-care product availability, while hospital systems remain central to meeting higher-acuity analgesic demand. The competitive landscape now includes established OTC brands, large generic manufacturers, and specialty developers focusing on non-opioid differentiation, neuropathic pain, and institutional formularies.

Key Report Takeaways

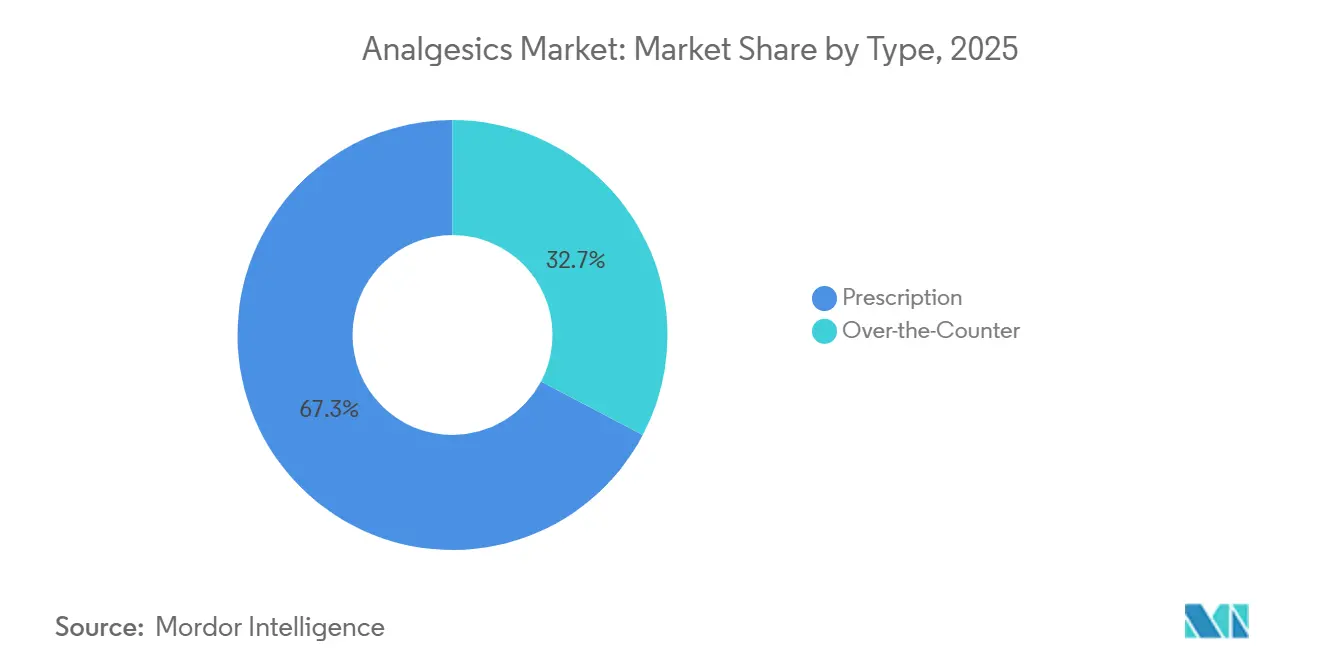

- By type, prescription analgesics held 67.29% of revenue in 2025, while OTC analgesics are projected to expand at 8.20% CAGR through 2031.

- By drug class, opioids held 54.34% of revenue in 2025, while NSAIDs are projected to advance at 9.10% CAGR through 2031.

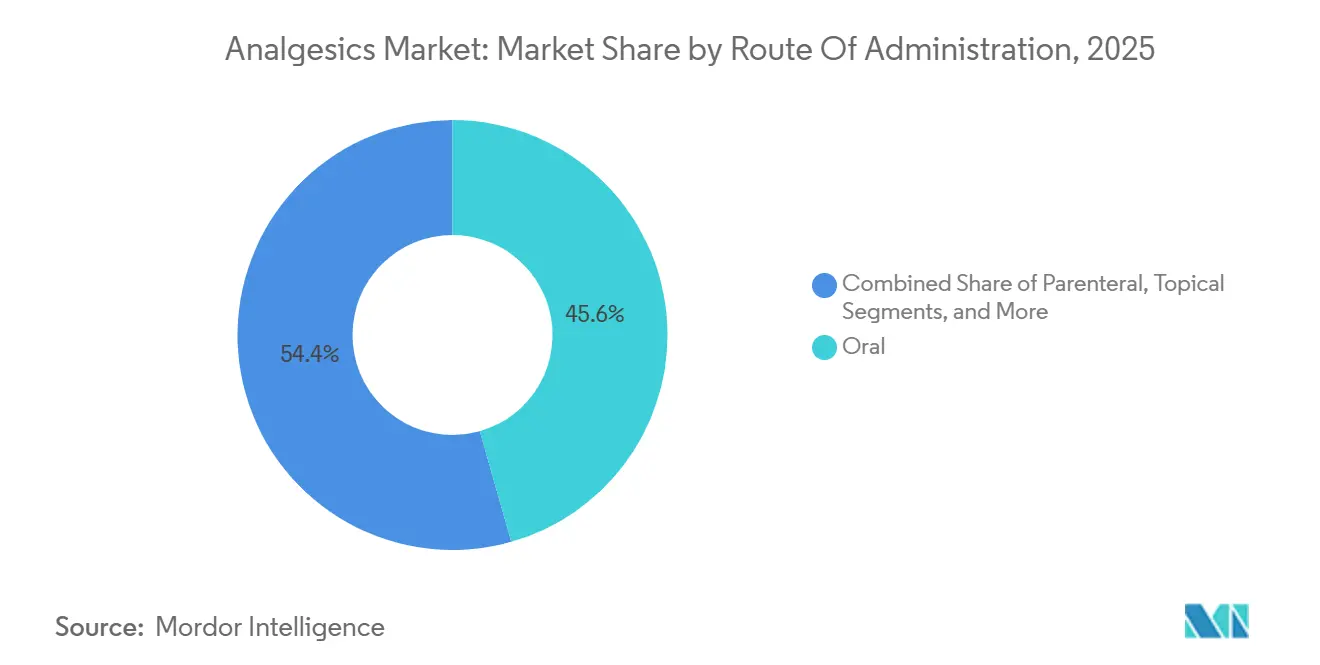

- By route of administration, oral analgesics accounted for 45.59% of revenue in 2025, while topical formulations are projected to grow at 8.85% CAGR through 2031.

- By pain type, musculoskeletal pain represented 38.89% of revenue in 2025, while neuropathic pain is projected to expand at 10.25% CAGR through 2031.

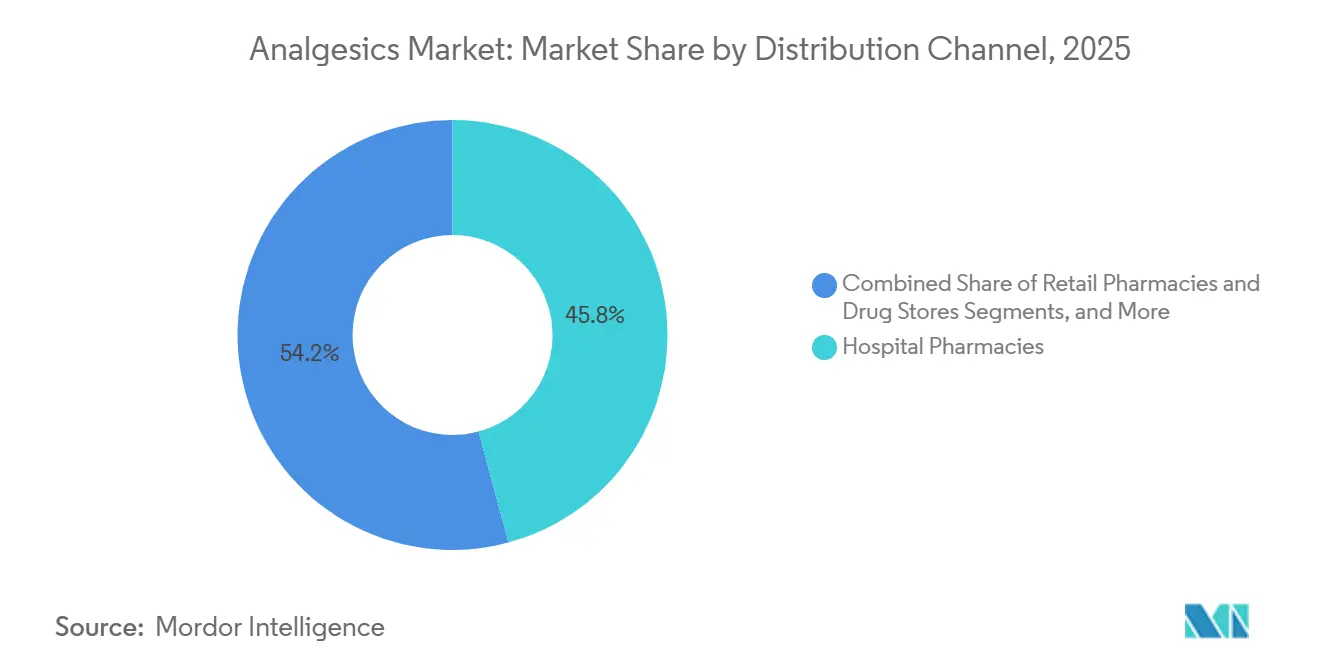

- By distribution channel, hospital pharmacies held 45.78% of revenue in 2025, while online pharmacies are projected to grow at 10.55% CAGR through 2031.

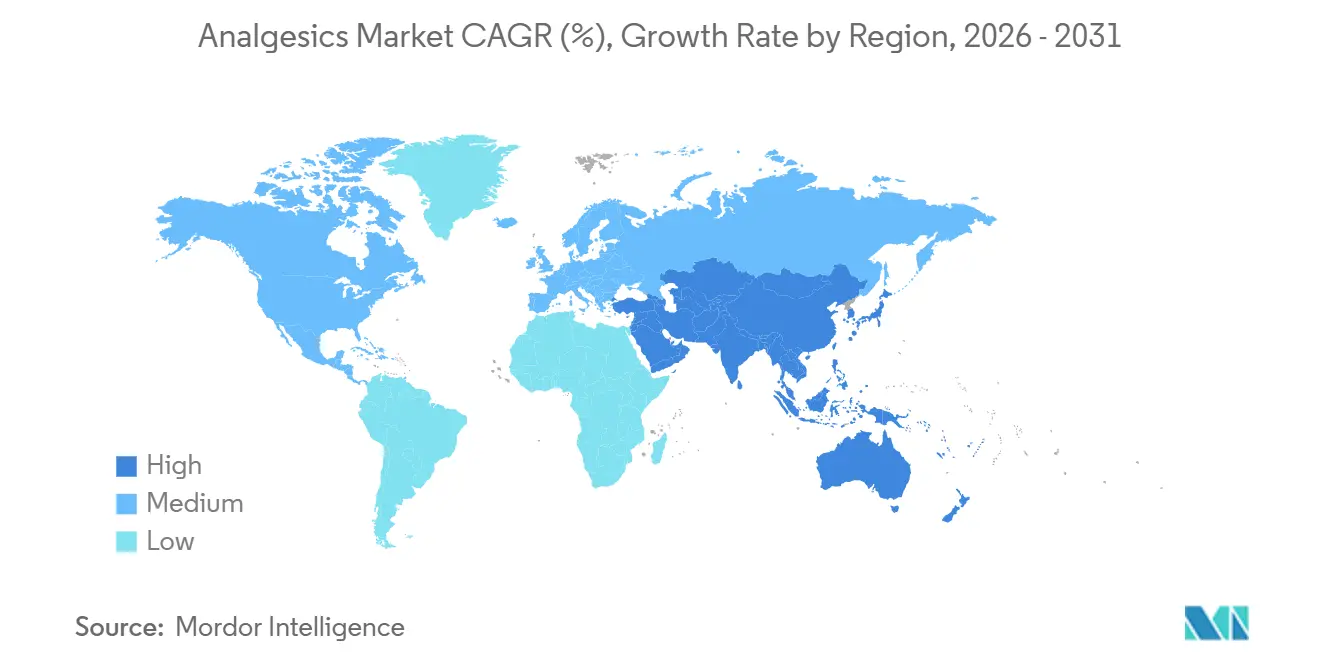

- By geography, North America held 41.67% of global revenue in 2025, while Asia-Pacific is projected to grow at 10.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Analgesics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising chronic pain and musculoskeletal burden from aging populations | +2.1% | Global, concentrated in North America, Europe, East Asia | Long term (≥ 4 years) |

| Aging-linked osteoarthritis and neuropathic pain demand increase | +1.6% | North America, Europe, APAC including Japan, South Korea, Australia | Long term (≥ 4 years) |

| Shift toward non-opioid and multimodal pain care protocols | +1.3% | North America, Europe | Medium term (2-4 years) |

| Online pharmacy expansion for OTC analgesic access | +0.9% | APAC, MEA, South America | Medium term (2-4 years) |

| IV opioid-sparing multimodal post-operative protocols | +0.7% | North America, Europe | Short term (≤ 2 years) |

| Closing opioid access gaps in LMIC palliative care | +0.5% | South America, MEA, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Pain And Musculoskeletal Burden

Chronic pain, influenced by multiple factors rather than a single disease, is a key driver of the analgesics market. Aging, obesity, sedentary lifestyles, and longer survival after major illnesses are increasing the number of patients requiring ongoing treatment for recurring pain. A 2025 study projected a rise in osteoarthritis cases among adults aged 55 and older through 2050, highlighting sustained demand for musculoskeletal pain therapies.[1]Wang Yichen et al., “Global, Regional, and National Burden of Osteoarthritis Among Middle-Aged and Older Adults, Estimates From the Global Burden of Disease Study 2021 and Projections to 2050,” Frontiers in Medicine, frontiersin.org High BMI contributes significantly to osteoarthritis-related disabilities, expanding the patient pool through aging and metabolic risks. This trend supports demand across hospitals, specialty clinics, and retail settings, while boosting the appeal of combination strategies and targeted products for long-term pain management.

Aging-Linked Osteoarthritis And Neuropathic Pain Demand Increase

The analgesics market is experiencing strong demand in regions where aging and metabolic diseases overlap, such as North America, Europe, Japan, South Korea, and urban Asia. The treated population is expanding for both joint and nerve pain. Neuropathic pain, requiring longer treatment and careful adjustments, is projected to be the fastest-growing pain category through 2031.[2]Drug Enforcement Administration, “Established Aggregate Production Quotas for Schedule I and II Controlled Substances and Assessment of Annual Needs for the List I Chemicals Ephedrine, Pseudoephedrine, and Phenylpropanolamine for 2026,” Federal Register, govinfo.gov Osteoarthritis continues to maintain a broad patient base, keeping musculoskeletal pain central to market demand. This dual demand from degenerative and neuropathic conditions is driving suppliers to diversify portfolios beyond traditional opioids and basic oral analgesics.

Shift Toward Non-Opioid And Multimodal Pain Care Protocols

The shift to non-opioid and multimodal pain management is transforming the analgesics market. In the U.S., the NOPAIN Act, effective January 2025, introduced a Medicare reimbursement pathway for non-opioid pain treatments in outpatient and ambulatory surgery centers.[3]Ahmed Nadeem-Tariq et al., “The NOPAIN Act, Implications for Opioid Use Reduction in Orthopedic Surgery,” Journal of Opioid Management, wmpllc.org This change has improved adoption conditions for hospitals and physicians. By February 2026, over 80% of surveyed facilities reported reduced opioid prescriptions post-surgery, with 52% increasing non-opioid treatment use. Perioperative care is also moving from opioid-centric to opioid-free strategies, creating opportunities for novel oral non-opioids, hospital-administered adjuncts, and specialized post-operative pain protocols.[4]Yoo Hae Kyeong, Taeyup Kim, and Ho-Jin Lee, “Recent Advances and Practical Strategies in Opioid-Free Multimodal Analgesia for Surgical Patients, A Narrative Review,” Journal of the Korean Medical Association, jkma.org

Online Pharmacy Expansion for OTC Analgesic Access

Online pharmacies are reshaping the distribution of OTC pain products, becoming a significant growth driver in the analgesics market. This channel enhances convenience, increases product visibility, and supports repeat self-care purchases without requiring physician visits. For non-prescription analgesics, brand recognition, accessibility, and purchase frequency are key factors. As online pharmacy adoption grows, the market is shifting toward a model emphasizing retail speed and digital discovery. While hospital and store-based dispensing remains important, online platforms are expanding OTC product reach, pushing branded suppliers to strengthen market share through product extensions, consumer trust, and omnichannel strategies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Opioid misuse controls and tighter prescribing frameworks | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Nsaid and acetaminophen safety liabilities from adverse event labeling | -0.7% | Global, with strongest exposure in North America and the EU | Medium term (2-4 years) |

| Api concentration and asia supply dependency | -0.5% | Global, with primary impact on North America and Europe | Medium term (2-4 years) |

| Regulatory friction in bioequivalence approvals and shortage management | -0.3% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Opioid Misuse Controls And Tighter Prescribing Frameworks

Opioid controls continue to restrict a segment of the analgesics market while creating opportunities for alternatives. The DEA has reduced oxycodone production quotas by over 6% for 2026, marking the tenth consecutive year of quota reductions for key opioids. This tighter supply environment has led to challenges in managing shortages for several Schedule II medicines, including critical hospital pain therapies. Regulatory oversight is also influencing prescriber behavior, making long-term opioid use less sustainable in routine practice. As a result, the market retains a portion of its opioid base but is shifting growth toward safer and more targeted options.

NSAID And Acetaminophen Safety Liabilities

Increased safety scrutiny on NSAIDs and acetaminophen is impacting the analgesics market across prescription and OTC segments. Despite their widespread use, stricter warning requirements are reducing prescribing confidence and increasing consumer caution. These products play a central role in pain management, positioned between controlled opioids and specialized therapies. Stricter labeling is prompting more conservative recommendations, particularly for high-risk patients or prolonged use. This trend is pressuring two major market segments while driving demand for safer formulations and delivery systems that minimize systemic exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Prescription Leadership With Faster OTC Expansion

In 2025, prescription analgesics accounted for 67.29% of market revenue, maintaining their leadership in the analgesics market. This dominance reflects the reliance on hospital-based treatments for cancer pain, post-surgical pain, neuropathic pain, and severe musculoskeletal conditions. Prescription use remains essential due to physician oversight, dosage adjustments, and access to specialized products unavailable in self-care channels. The NOPAIN Act's implementation in 2025 further supported reimbursement for non-opioid treatments, ensuring the relevance of prescription pathways despite reduced opioid volumes. OTC analgesics are projected to grow at a CAGR of 8.20% from 2026 to 2031, driven by channel expansion and brand extensions rather than shifts in clinical demand.

By Drug Class: Opioids Hold Share While NSAIDs Lead Growth

Opioids held 54.34% of the drug class segment in 2025, maintaining their leading position despite policy pressures. Their share reflects legacy use in chronic pain, palliative care, post-operative settings, and severe pain episodes where alternatives are insufficient. In regions with limited access, opioids remain critical for addressing unmet palliative care needs. The global imbalance in opioid consumption highlights the challenges of transitioning away from opioids uniformly across markets.

NSAIDs are forecast to grow at a CAGR of 9.10% through 2031, making them the fastest-growing drug class. This growth is driven by their adoption in opioid-sparing regimens and their broad application in musculoskeletal, inflammatory, and post-procedural pain management.

By Route Of Administration: Oral Products Lead While Topical Formats Accelerate

Oral analgesics accounted for 45.59% of market revenue in 2025, making them the largest route in the analgesics market. Their dominance is attributed to convenience, affordability, OTC availability, and widespread familiarity among physicians and consumers. Oral products cater to moderate pain cases and self-medication needs, maintaining demand across retail and prescription channels. While stable, their growth is expected to be steadier compared to innovation-driven formats.

Topical analgesics are projected to grow at a CAGR of 8.85% through 2031, driven by advancements in transdermal delivery systems like nanocarriers and microneedle patches. These innovations enhance site-specific delivery and align with the growing focus on safety and localized treatment, making topical products increasingly relevant for musculoskeletal pain, sports injuries, and chronic conditions.

By Pain Type: Musculoskeletal Pain Holds Volume While Neuropathic Pain Raises The Premium Mix

Musculoskeletal pain represented 38.89% of market revenue in 2025, making it the largest pain category in the analgesics market. This segment includes conditions like osteoarthritis, rheumatoid arthritis, and sports injuries, which drive recurring and episodic treatment demand. The rising burden of osteoarthritis and the impact of high BMI on disability risks further reinforce its importance. The category balances frequent OTC purchases with high-value prescription episodes, ensuring its leading position in the market.

Neuropathic pain is expected to grow at a CAGR of 10.25% through 2031, making it the fastest-growing pain category. This growth is driven by the need for longer treatment durations, therapy adjustments, and specialized care pathways, along with the increasing focus on non-opioid solutions for nerve-related pain conditions.

By Distribution Channel: Hospital Pharmacies Remain Core While Online Pharmacies Move Fastest

Hospital pharmacies accounted for 45.78% of market revenue in 2025, maintaining their leadership in the analgesics market. Their dominance stems from inpatient opioid use, post-surgical pain management, and other therapies requiring clinical oversight. Hospitals also manage supply disruptions and formulary substitutions, ensuring their central role in high-acuity demand scenarios such as surgeries and oncology treatments.

Online pharmacies are projected to grow at a CAGR of 10.55% through 2031, making them the fastest-growing distribution channel. This growth is driven by the convenience of accessing OTC products, increasing consumer acceptance of e-commerce, and the suitability of online platforms for repeat purchases of non-prescription items.

Geography Analysis

In 2025, North America accounted for 41.67% of global revenue, maintaining its position as the largest contributor to the analgesics market. The region benefits from high pharmaceutical spending, strong brand presence, and a significant chronic pain patient base. Policy changes, such as the NOPAIN Act and stricter opioid supply controls, continue to shape the market, ensuring North America's central role in value creation as treatment approaches evolve.

Asia-Pacific is projected to grow at a CAGR of 10.15% through 2031, making it the fastest-growing region in the analgesics market. The region's growth is driven by an increasing chronic disease burden, expanding urban healthcare infrastructure, and improved access to OTC and prescription pain therapies. Haleon’s acquisition of the remaining 12% equity in its China OTC joint venture in 2025 highlights the strategic focus on regional execution and market control in this key growth area.

Europe remains a mature yet active market, supported by established healthcare systems and balanced demand for prescription and OTC analgesics. Aging populations, chronic pain prevalence, and reimbursement structures sustain demand, while regulatory changes add dynamism. The Middle East and Africa, though smaller, show potential for gradual growth due to urbanization and capacity building. South America also demonstrates steady demand, driven by aging demographics and the reach of retail pharmacy networks. Together, these regions diversify the analgesics market's growth beyond its primary revenue contributors.

Competitive Landscape

The global analgesics market is moderately fragmented, with the top five players accounting for nearly the majority of revenue, and Haleon plc holding a leading 13.0% share. This structure reflects a competitive landscape where no single company dominates, but a few maintain significant scale in brand visibility, channel access, and portfolio diversity. Competition is divided between large OTC brand owners and a broad prescription base shaped by generic suppliers and specialty pain companies, creating a diverse competitive environment.

Haleon, Kenvue, Bayer, Reckitt, and Perrigo lead the OTC pain relief segment, while Teva, Viatris, Dr. Reddy's, Cipla, Lupin, Sun Pharma, and Aurobindo strengthen the generic prescription side. Haleon’s acquisition of its China OTC joint venture in 2025 enhanced its control over local distribution assets. Additionally, the NOPAIN Act improved commercial conditions for non-opioid products in U.S. hospitals, influencing post-surgery facility behavior. These developments highlight the growing importance of access strategies alongside product innovation.

Innovation in the analgesics market is focused on non-opioid science, targeted delivery, and hard-to-treat pain categories. The approval of suzetrigine in January 2025 introduced a first-in-class oral non-opioid option for acute pain, emphasizing the value of differentiated mechanisms in pain care. Grünenthal’s QUTENZA development for post-surgical neuropathic pain and Vertex Pharmaceuticals’ non-opioid pain programs targeting chronic indications demonstrate the potential for niche players to establish significant positions. Companies addressing access barriers in underserved regions may also find opportunities where pain burden is high and opioid availability is limited. This dynamic keeps the market open to both established leaders and emerging challengers.

Analgesics Industry Leaders

Bayer AG

Dr. Reddy’s Laboratories Ltd.

Cipla Limited

Teva Pharmaceutical Industries Ltd.

Sun Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Viatris Inc. announced that the U.S. Food and Drug Administration accepted the New Drug Application for MR-107A-02, a fast-acting non-opioid meloxicam for moderate-to-severe acute pain treatment.

- April 2026: Cumberland Pharmaceuticals Inc. received U.S. FDA approval for an expanded indication of Caldolor ibuprofen injection to include postoperative pain management.

- February 2026: Pacira BioSciences reported survey findings showing over 80% of hospitals reduced opioid prescriptions post-surgery after the NOPAIN Act, with 52% increasing non-opioid analgesic use.

- January 2026: The U.S. DEA finalized 2026 production quotas, reducing oxycodone supply by 6.24% and increasing morphine production by 10.5% to address shortages.

- November 2025: Bayer signed a memorandum with Alpha Pharma for local manufacturing of Aspirin Protect in Saudi Arabia, with operations planned by 2028.

Global Analgesics Market Report Scope

As per the scope of the report, an analgesic is a medication used to relieve pain without causing loss of consciousness. Unlike anesthetics, which block all sensation, analgesics specifically target pain pathways and are among the most widely used medicines worldwide.

The analgesics market is segmented by type, drug class, route of administration, pain type, and distribution channel. By type, the market includes prescription and over-the-counter analgesics. By drug class, the market is segmented into opioids, NSAIDs, acetaminophen, combination analgesics, and local anesthetics & topical analgesics. By route of administration, the market is categorized into oral, parenteral, topical, transdermal, and rectal. By pain type, the market is segmented into musculoskeletal pain, surgical and trauma pain, cancer pain, neuropathic pain, migraine and headache, dental and orofacial pain, obstetric and gynecologic pain, and pediatric pain. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and online pharmacies. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Prescription |

| Over-the-Counter |

| Opioids |

| NSAIDs |

| Acetaminophen |

| Combination Analgesics |

| Local Anesthetics and Topical Analgesics |

| Oral |

| Parenteral |

| Topical |

| Transdermal |

| Rectal |

| Musculoskeletal Pain |

| Surgical and Trauma Pain |

| Cancer Pain |

| Neuropathic Pain |

| Migraine and Headache |

| Dental and Orofacial Pain |

| Obstetric and Gynecologic Pain |

| Pediatric Pain |

| Hospital Pharmacies |

| Retail Pharmacies and Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Prescription | |

| Over-the-Counter | ||

| By Drug Class | Opioids | |

| NSAIDs | ||

| Acetaminophen | ||

| Combination Analgesics | ||

| Local Anesthetics and Topical Analgesics | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Transdermal | ||

| Rectal | ||

| By Pain Type | Musculoskeletal Pain | |

| Surgical and Trauma Pain | ||

| Cancer Pain | ||

| Neuropathic Pain | ||

| Migraine and Headache | ||

| Dental and Orofacial Pain | ||

| Obstetric and Gynecologic Pain | ||

| Pediatric Pain | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies and Drug Stores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the analgesics market in 2026 and where will it reach by 2031?

The analgesics market size stands at USD 54.29 billion in 2026 and is projected to reach USD 76.87 billion by 2031, with a 7.20% CAGR over the forecast period.

Which product type leads analgesics revenue today?

Prescription analgesics led with 67.29% of revenue in 2025, supported by hospital use, chronic pain treatment, and supervised care pathways.

Which part of analgesics is growing the fastest?

Online pharmacies are the fastest-growing distribution channel at 10.55% CAGR, while neuropathic pain is the fastest-growing pain type at 10.25% CAGR through 2031.

Why are non-opioid treatments gaining traction in pain care?

Reimbursement support under the NOPAIN Act, tighter opioid controls, and broader clinical adoption of multimodal care are pushing providers toward non-opioid options.

Which region matters most for future expansion?

Asia-Pacific is the fastest-growing region at 10.15% CAGR through 2031, while North America remained the largest region with 41.67% revenue share in 2025.

What is shaping competition among analgesics companies?

Competition is being shaped by OTC brand power, generic prescription scale, non-opioid innovation, digital channels, and regional execution, while the top 5 companies together account for nearly 35% of revenue.

Page last updated on: