N95 Grade Medical Protective Mask Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

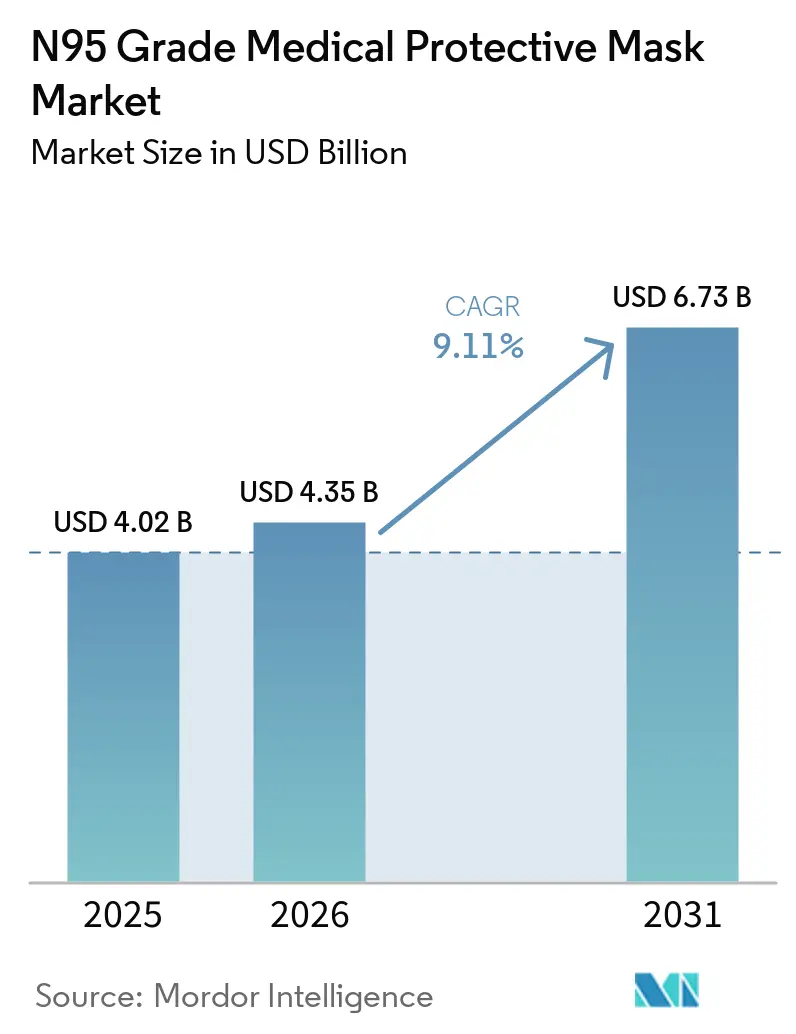

| Market Size (2026) | USD 4.35 Billion |

| Market Size (2031) | USD 6.73 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

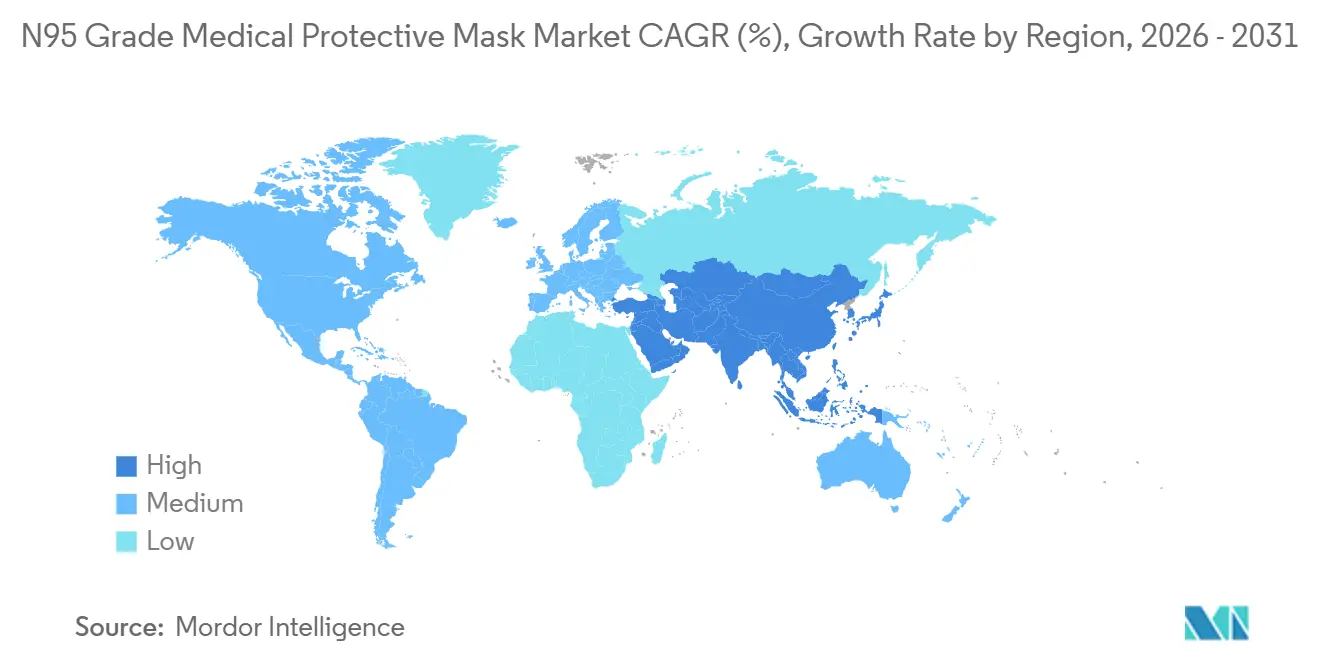

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

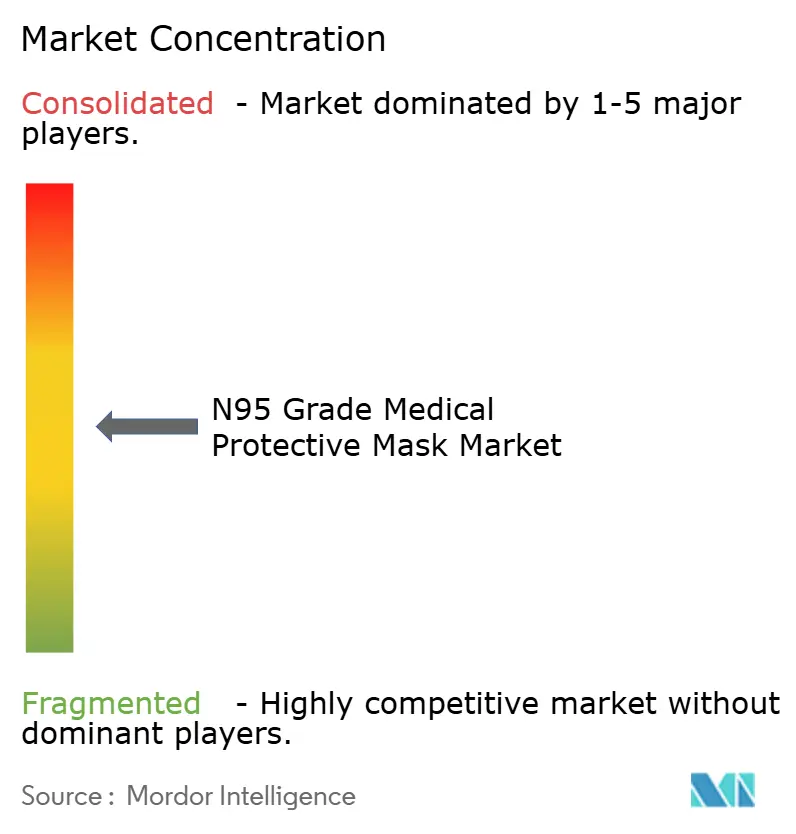

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

N95 Grade Medical Protective Mask Market Analysis by Mordor Intelligence

The N95 Grade Medical Protective Mask Market size is projected to be USD 4.02 billion in 2025, USD 4.35 billion in 2026, and reach USD 6.73 billion by 2031, growing at a CAGR of 9.11% from 2026 to 2031.

Demand in the N95 Grade Medical Protective Mask Market is being supported by a lasting move toward hospital stockpiles and stricter respiratory protection enforcement in high-exposure workplaces. Across the N95 Grade Medical Protective Mask Market, procurement is shifting away from emergency-led buying and toward multi-year supplier agreements that require certification, lot traceability, and audit readiness. This change is making revenue patterns more predictable for certified manufacturers, while also raising the penalty for sellers that cannot prove compliance across hospital and industrial channels. Margin pressure still remains a core issue because melt-blown polypropylene costs rose sharply in early 2026, which hurt manufacturers without an integrated material supply. Counterfeit leakage in online channels and overlapping rules across NIOSH, CE, FDA, and local regimes continue to raise verification costs and slow some cross-border buying decisions in the N95 grade medical protective mask market.

Key Report Takeaways

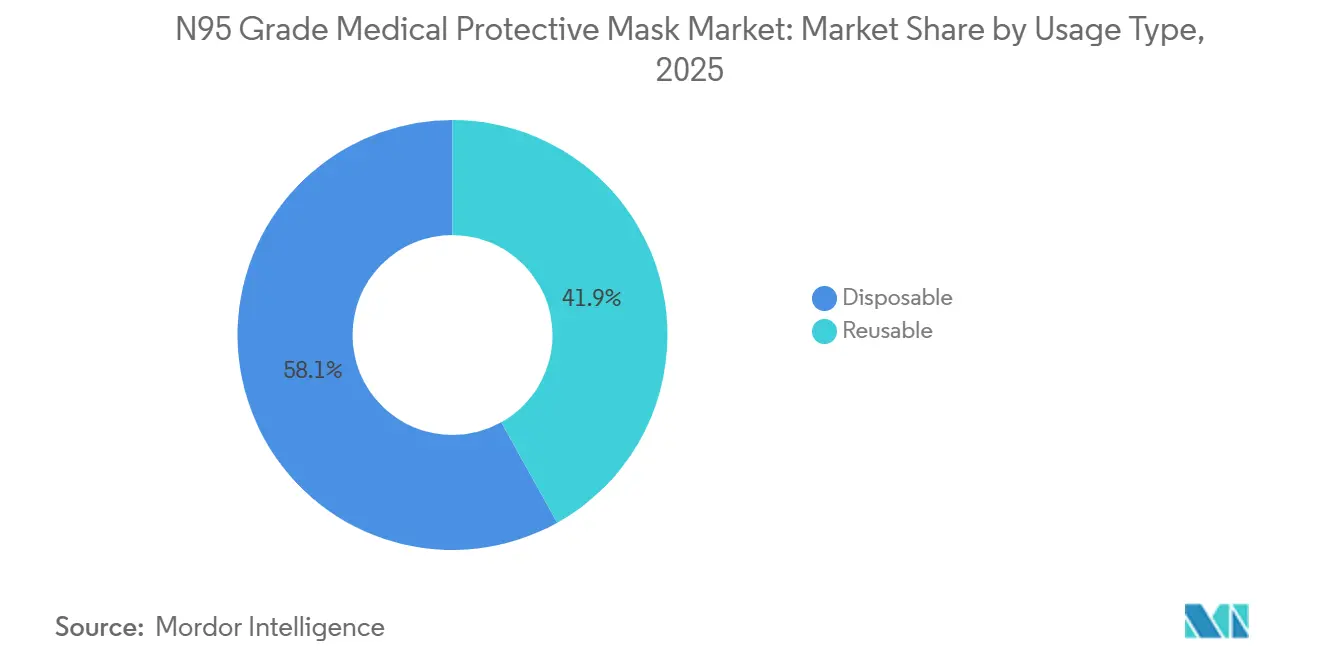

- By usage type, disposable N95 respirators led with 58.12% share in 2025, while reusable respirators are projected to expand at a 12.62% CAGR through 2031.

- By design features, non-valve N95 respirators held 71.73% share in 2025, while valve-type N95 respirators are forecast to grow at an 11.17% CAGR through 2031.

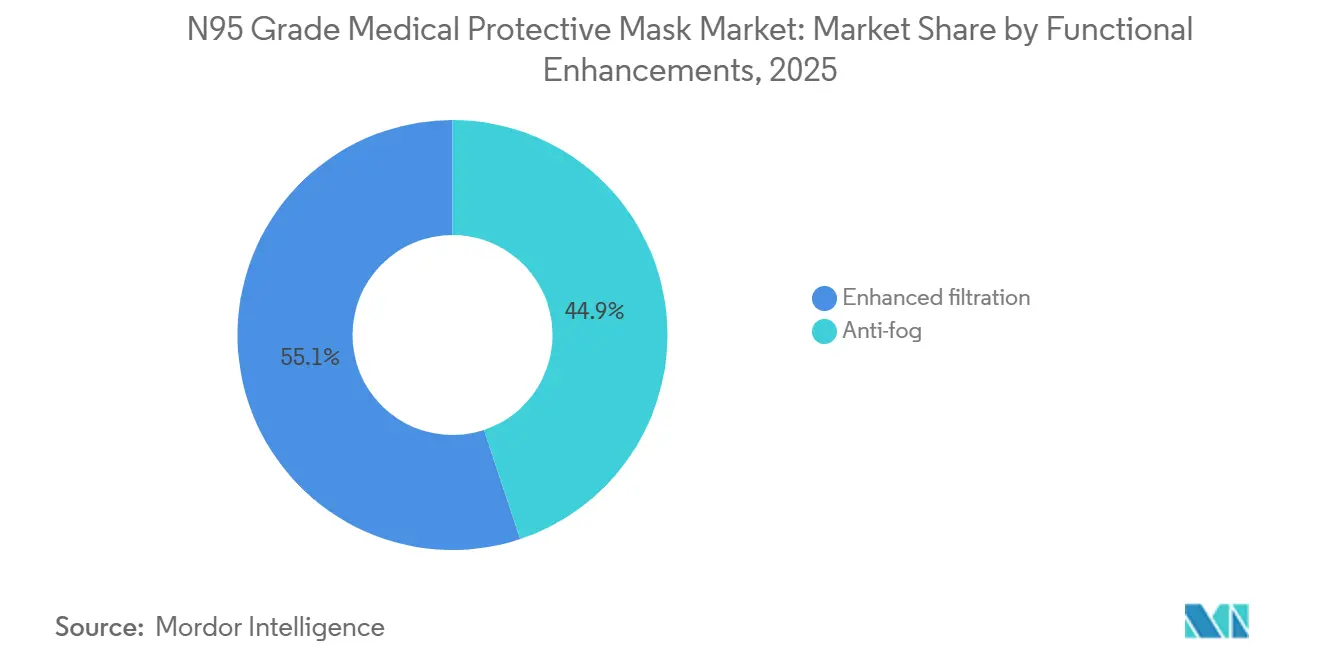

- By functional enhancements, enhanced filtration masks accounted for 55.07% share in 2025, while anti-fog masks are advancing at a 13.57% CAGR through 2031.

- By certification, NIOSH-certified masks captured 61.82% share in 2025, while no faster-growing certification sub-segment CAGR was provided in the supplied material.

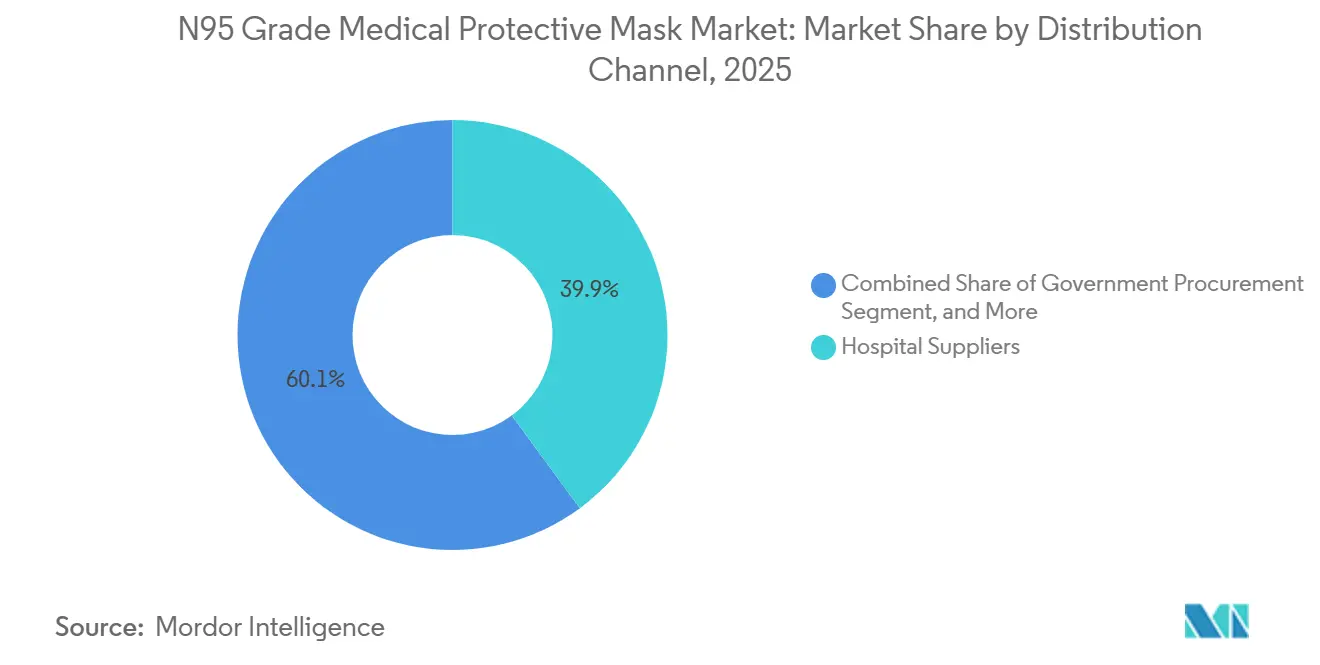

- By distribution channel, hospital suppliers held 39.87% share in 2025, while online retail is projected to expand at a 13.57% CAGR through 2031.

- By geography, North America held 37.23% share in 2025, while Asia-Pacific is forecast to grow at a 10.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global N95 Grade Medical Protective Mask Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hospital Stockpiling for Respiratory Readiness | +1.8% | North America and Europe core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Tighter Infection-Control Protocols in High-Risk Care Settings | +1.5% | Global, accelerating in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Stricter Workplace Safety Enforcement in High-Exposure Occupations | +1.2% | North America, Japan, European Union | Medium term (2-4 years) |

| Shift Toward Certified Procurement and Traceable Supply Agreements | +0.9% | Global | Medium term (2-4 years) |

| Rising Demand for Better Fit, Comfort, and Seal Performance | +0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Expansion of Certified Secondary Manufacturing Capacity Outside China | +0.7% | India, Vietnam, ASEAN, export to North America and European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hospital Stockpiling for Respiratory Readiness

Hospital respiratory readiness is moving into a standing procurement policy rather than episodic emergency planning in the N95 Grade Medical Protective Mask Market. The January 2026 CMS advance notice proposed a Secure American Medical Supplies designation and payment adjustments for hospitals that procure domestically manufactured NIOSH-approved surgical N95 respirators, which shows that supply resilience is now being tied more directly to reimbursement policy.[1]Centers for Medicare & Medicaid Services, “Medicare Program, Ensuring Safety Through Domestic Security With Made in America Personal Protective Equipment (PPE) and Essential Medicine Procurement by Medicare Participating Hospitals,” Federal Register, federalregister.gov The same notice stated that fewer than 100 U.S. hospitals reported data for the existing FY 2024 N95 payment adjustment, which means even modest simplification could widen participation and lift certified unit demand. That policy direction encourages buyers to lock in auditable supply relationships instead of rotating through short-term low-cost vendors. It also gives domestic and fully documented manufacturers a stronger position in contract renewals across the N95 Grade Medical Protective Mask Market. The result is a steadier procurement cadence that supports visibility in production planning, inventory allocation, and account retention.

Tighter Infection-Control Protocols in High-Risk Care Settings

Clinical infection-control standards are expanding N95 use beyond outbreak response and into routine care settings that carry persistent aerosol exposure risk. In April 2026, the European Health and Digital Executive Agency issued a prior information notice under the EU FAB+ program for capacity reservation contracts covering FFP2 respirators, which signaled that respiratory protection is being treated as a strategic reserve category in Europe.[2]European Health and Digital Executive Agency, “Prior Information Notice, EU FAB+ Capacity Reservation for Personal Protective Equipment,” HaDEA, hadea.ec.europa.eu This matters because reserved manufacturing capacity and vendor-managed stock requirements favor producers that can prove documentation quality and consistent output. In the N95 Grade Medical Protective Mask Market, this narrows the field to suppliers that can meet tighter qualification rules under hospital tenders and public procurement programs. CE marking, EN 149 compliance, and ISO-based quality systems are becoming less of a differentiator and more of a baseline requirement in regulated buying environments. As these requirements spread, the N95 Grade Medical Protective Mask Market should see less room for uncertified substitution in higher-risk care settings.

Stricter Workplace Safety Enforcement in High-Exposure Occupations

Industrial demand is strengthening because respiratory protection is being enforced more actively in workplaces with heavy dust, fumes, and airborne exposure. OSHA's Respiratory Protection Standard ranked fifth on the agency's FY 2025 most-cited violations list, with 1,953 violations recorded, which shows that compliance gaps remain large enough to keep enforcement pressure elevated.[3]American National Standards Institute, “OSHA 2025 Top 10 Violations,” ANSI Blog, ansi.org When violations remain persistent at that scale, employers are more likely to shift from discretionary buying toward formal respirator programs with approved products and documented fit-testing. The same pattern is visible in parts of Asia, where broader fit-testing obligations are making annual respirator replacement more predictable in industrial settings. In the N95 Grade Medical Protective Mask Market, this creates a durable demand stream that is not tied only to hospitals or infectious disease cycles. It also favors suppliers that can serve both institutional healthcare buyers and occupational safety channels with the same compliance discipline.

Shift Toward Certified Procurement and Traceable Supply Agreements

Buyer preference is moving toward verifiable certification, lot traceability, and approved sales channels across the N95 Grade Medical Protective Mask Market. NIOSH published its April 2025 fact sheet on counterfeit and misrepresented respirators to clarify that visual inspection alone cannot confirm authenticity and that TC approval number verification remains essential. The FTC's April 2024 action against Razer also showed that false N95-grade claims can lead to direct financial penalties when the product has not met or even entered the NIOSH certification process. That case raised the legal and reputational cost of casual certification claims for both brands and sellers. Procurement teams are responding by embedding TC number verification, authorized sourcing, and audit documentation into supplier qualification standards. In the N95 Grade Medical Protective Mask Market, this reduces the room for gray-market intermediaries and shifts value toward primary manufacturers with traceable production records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Dependence on Melt-Blown Polypropylene | -1.4% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Counterfeit and Uncertified Product Leakage in Online Channels | -1.1% | Global, concentrated in online retail | Medium term (2-4 years) |

| Regulatory Fragmentation Across NIOSH, CE, FDA, and Local Regimes | -0.9% | Cross-border procurement markets globally | Long term (≥ 4 years) |

| Inventory Obsolescence and Shelf-Life Management Pressure | -0.7% | North America and Europe hospital procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Dependence on Melt-Blown Polypropylene

The N95 Grade Medical Protective Mask Market remains exposed to melt-blown polypropylene because that material still anchors filtration performance in most certified products. In early 2026, nonwoven raw material prices climbed sharply as Middle East supply disruptions moved through petrochemical feedstock chains, with reported regional pressure across Asia-Pacific, North America, and Europe. This creates a difficult pricing mismatch because large hospital and government contracts often lock finished-product prices for 12 to 24 months, while resin and media costs can move much faster. Smaller producers without captive melt-blown capacity or secured offtake agreements therefore absorb more of the margin shock. The pressure is especially uneven because not all pandemic-era capacity is suited for high-grade electret filtration media. In the N95 Grade Medical Protective Mask Market, the next raw material spike could again shift share toward manufacturers that control their media supply or maintain stronger supplier contracts.

Counterfeit and Uncertified Product Leakage in Online Channels

Online sales are expanding quickly, but that same channel carries the highest authenticity risk in the N95 grade medical protective mask market. NIOSH stated in its 2025 counterfeit respirator guidance that workers and employers cannot depend on product appearance to distinguish authentic units from misrepresented ones. The FTC's action against Razer showed how polished branding and technical claims can still mislead buyers when formal certification has not been secured. Marketplace operators that do not verify TC approval numbers at the listing stage leave room for compliant and non-compliant inventory to appear side by side. Each enforcement event then weakens trust not only in the seller involved, but also in the wider channel. That channel friction slows conversion for legitimate suppliers and keeps verification costs elevated across the N95 grade medical protective mask market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage Type: Disposables Hold the Floor as Reusables Gain Institutional Footing

Disposable N95 respirators held 58.12% share in 2025, which kept them in the lead across the usage-type split. That position reflects the strong fit between single-use masks and hospital infection-control routines where contamination concerns make repeat wear operationally difficult. The N95 grade medical protective mask market still leans toward disposables because procurement teams value simple issuance, simple disposal, and fewer cleaning or storage steps. These products also fit well with surge planning because hospitals can integrate them into existing stockpile practices without changing staff workflow. In industrial settings, disposables remain useful where exposures are intermittent, crew turnover is high, or managers prefer a straightforward compliance process.

Reusable respirators are projected to grow at a 12.62% CAGR through 2031, which makes them the faster-expanding part of this segmentation. That growth shows that the N95 grade medical protective mask industry is opening more space for program-based use cases where repeated wear can reduce total unit consumption over time. Large institutions and industrial operators are more willing to evaluate reusable options when exposure duration is long and yearly replacement costs matter. Even so, the N95 grade medical protective mask market is unlikely to move fully away from disposables because healthcare settings still prioritize infection-control simplicity over lifecycle savings. The segment therefore points to a stable base for disposable demand and a growing, but still more selective, role for reusable models.

By Design Features: Valve Adoption Rises as Extended-Wear Needs Become More Important

Non-valve N95 respirators held 71.73% share in 2025, giving them a clear lead within design features. Their dominance came from healthcare and surgical environments where unfiltered exhalation into the surrounding area is not acceptable. The N95 grade medical protective mask market therefore continues to give non-valve designs a structural advantage in clinical use, where source control and wearer protection must work together. Non-valve masks also align more closely with hospital procurement habits because they fit existing infection-prevention standards without extra interpretation. That keeps them firmly positioned in large institutional contracts even as other designs gain traction in non-clinical settings.

Valve-type N95 respirators are projected to grow at an 11.17% CAGR through 2031, making them the faster-growing design sub-segment. This increase reflects conditions in laboratories, manufacturing sites, and field jobs where long wear times can make heat buildup and exhalation resistance more noticeable. Makrite highlighted this product direction in 2026 through its 9600NV model, which it described as reducing exhalation resistance versus traditional round-valve designs MAKRITE.COM. That example shows how comfort is becoming a defined purchase factor rather than a secondary benefit in the N95 grade medical protective mask market. As buyers compare worker compliance, shift duration, and thermal comfort, valved products are likely to win more discretionary demand outside clinical care.

By Functional Enhancements: Anti-Fog Demand Expands Beyond Standard Filtration Priorities

Enhanced filtration masks held 55.07% share in 2025, which kept them as the largest functional enhancement category. This lead fits the way many institutional buyers evaluate products because filtration efficiency and recognized certification remain the first screens in most procurement decisions. The N95 grade medical protective mask market still rewards clearly understood performance features, and enhanced filtration sits closest to that baseline expectation. The category also benefits from the fact that it is easy to justify in tenders and audit trails because buyers can link it directly to risk control. For that reason, enhanced filtration remains the default preference where committees want simple, defensible technical criteria.

Anti-fog masks are forecast to grow at a 13.57% CAGR through 2031, making them the fastest-growing functional enhancement sub-segment. That trajectory shows that the N95 grade medical protective mask market is responding to daily wear issues that standard filtration metrics do not fully capture. Clinicians, technicians, and laboratory staff who wear eyewear for extended periods need clear visibility, and fogging can become a more immediate operational problem than nominal differences in filtration performance. Product development in this area is moving toward engineered comfort attributes, which suggests that anti-fog performance is becoming easier to specify and compare. As this happens, the N95 grade medical protective mask market is likely to see more procurement language that treats visibility support as a functional requirement rather than a minor comfort claim.

By Certification: NIOSH Remains the Core Reference While Cross-Border Standards Stay Relevant

NIOSH-certified masks commanded 61.82% share in 2025, which made certification the most concentrated segmentation in the supplied material. In this segment, NIOSH-certified masks held 61.82% of the N95-grade medical protective mask market share in 2025 because U.S. occupational use requires approval under the NIOSH framework, and OSHA enforcement makes non-compliance costly. The N95 grade medical protective mask market also gives NIOSH certification influence outside the United States because procurement teams in other countries often use the Certified Equipment List as a quality reference. That makes certification more than a local regulatory label and turns it into a purchasing signal across borders. It also favors suppliers that can defend their approval status clearly in institutional tenders.

CE-marked and FDA-aligned medical-grade products still matter because regional regulatory structures and clinical use conditions are not identical. The N95 grade medical protective mask industry must therefore work across several approval regimes, even when NIOSH remains the most visible reference point. In Europe, conformity assessment under MDR-linked frameworks and local guidance maintains a clear quality threshold for formal medical procurement. In Germany, BfArM has also recognized that N95 masks can provide comparable protection to FFP2 masks under specific provisions, which supports practical cross-recognition in constrained settings. That balance between global reference value and regional compliance detail will keep certification strategy central in the N95 grade medical protective mask market.

By Distribution Channel: Hospital Suppliers Lead While Online Retail Expands Faster

Hospital suppliers held 39.87% share in 2025, which placed them at the front of the distribution mix. Their lead reflects their ability to aggregate certified products, support fit-testing needs, and provide the documentation that hospitals and other institutions require during audits. The N95 grade medical protective mask market still depends heavily on these structured channels because large buyers prefer suppliers that can combine product access with compliance support. Hospital suppliers also fit better with contract-driven purchasing and organized procurement systems than open-market channels do. That keeps them important even as buyers test new sourcing routes for speed and price visibility.

Online retail is projected to grow at a 13.57% CAGR through 2031, giving it the fastest expansion rate among channels. This part of the N95 grade medical protective mask market is gaining ground with individual practitioners, small clinics, and small and medium-sized enterprises that want faster ordering and clearer unit pricing. At the same time, channel risk remains higher because counterfeit listings and misrepresented approvals can weaken trust if verification is weak. Tools such as the NIOSH Certified Equipment List help reduce that risk by letting buyers confirm approval identifiers before purchase. The result is a channel mix in which hospital suppliers defend scale while online retail grows by serving speed-sensitive and price-sensitive demand.

Geography Analysis

North America held 37.23% of the N95 grade medical protective mask market share in 2025, which kept the region in the lead in terms of current revenue. The regional base is supported by hospital systems, emergency response agencies, construction employers, and manufacturing buyers that already operate under formal respiratory protection rules. The January 2026 CMS proposal for Medicare payment differentials tied to domestically manufactured NIOSH-approved surgical N95 respirators shows that U.S. policy is still reinforcing traceable local supply. The September 2024 Section 301 tariff increase on Chinese masks and respirators also pushed many procurement teams further toward domestic or nearshore options. Together, those factors keep North America central to revenue stability in the N95 Grade Medical Protective Mask Market even after pandemic-era surge buying normalized.

Asia-Pacific is projected to grow at a 10.65% CAGR through 2031, making it the fastest-expanding region in the N95 grade medical protective mask market. Growth is being supported by healthcare capacity additions, tighter workplace compliance, and certified manufacturing expansion outside China. India, Vietnam, and Malaysia are becoming more important because new certified melt-blown and respirator capacity supports both domestic procurement and export potential. Japan's broader fit-testing requirements are also tying industrial respirator use more closely to compliance cycles, which supports recurring replacement demand in higher-exposure workplaces. China still has the largest manufacturing footprint in the region, but export conditions have become more difficult as self-supply improves in Europe and trade barriers lift landed costs in the United States.

Europe remains a major consumption center in the N95 Grade Medical Protective Mask Market because public hospital procurement and industrial safety demand both depend on formal compliance. The EU FAB+ program showed in April 2026 that FFP2 capacity reservation is moving into long-term health security planning rather than temporary crisis management. Germany, the United Kingdom, and France anchor regional demand, while Italy and Spain offer room for catch-up as occupational enforcement improves. The Middle East and Africa are emerging as hospital infrastructure investment and workplace safety programs expand, especially in GCC procurement that increasingly asks for internationally recognized certification. South America, led by Brazil's large industrial base, continues to add demand where mining and manufacturing employers must align respirator purchases with formal compliance requirements.

Competitive Landscape

The N95 grade medical protective mask market remains moderately concentrated, with a small group of certified incumbents holding strong positions in hospital and government procurement. 3M continues to hold the broadest competitive position because of its large certified portfolio, established U.S. manufacturing base, and long-standing institutional relationships. Competition is now driven less by headline capacity and more by certification depth, traceability, and preferred access to large accounts. Honeywell's decision to exit direct participation changed the field when it agreed to sell its PPE business, including the North respirator brand, to Protective Industrial Products, which signaled a major redistribution of channel strength. That shift gave PIP a stronger industrial respiratory position and reduced the number of major legacy names competing independently in the N95 Grade Medical Protective Mask Market.

In March 2026, 3M entered into a definitive agreement to form a joint venture with Bain Capital that combines Scott Safety with Madison Fire & Rescue in a USD 1.95 billion transaction. That move showed that leading participants are building broader safety portfolios around respiratory protection rather than competing only on mask specifications. Prestige Ameritech also strengthened its institutional position after Premier transferred S2S Global in exchange for a combined ownership stake of 24.2%, which improved Prestige's access to healthcare purchasing channels. Smaller certified specialists continue to win where domestic production credentials, fast response commitments, or narrow product focus matter more than brand breadth. The N95-grade medical protective mask market, therefore, continues to reward companies that can combine compliance discipline with channel reliability.

Another competitive layer is forming around fit, comfort, and technology-enabled performance in the N95 Grade Medical Protective Mask Market. Traditional PPE leaders still control legacy disposable formats, but they do not hold the same lead in personalization tools, fit-monitoring systems, or advanced media concepts. Research published in 2025 showed that face morphology modeling and pressure analysis can support more personalized respirator fit, which points to future differentiation beyond filtration alone. That leaves room for new materials and digital-health entrants to influence the N95 grade medical protective mask market without matching incumbent scale in commodity production. As procurement standards keep tightening, the companies best placed to defend share will be those that pair certified supply with clear performance improvement and stronger documentation.

N95 Grade Medical Protective Mask Industry Leaders

3M

Cardinal Health, Inc.

Drägerwerk AG and Co. KGaA

Dynarex Corporation

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The European Health and Digital Executive Agency published a prior information notice under the EU FAB+ programme for manufacturing capacity reservation and vendor-managed FFP2 respirator mask stockpiles, marking the European Commission's first strategic PPE manufacturing reserve initiative outside the pharmaceutical sector.

- March 2026: 3M entered into a definitive agreement to form a joint venture with Bain Capital combining the Scott Safety business with the acquired Madison Fire & Rescue in a transaction valued at USD 1.95 billion. Under the terms, 3M contributes Scott Safety, receives USD 700 million in cash proceeds upon closing, and retains 50.1% of the new entity. The deal deepens 3M's commitment to diversified safety protection, including respiratory equipment, while accelerating integration with emergency response product lines.

- January 2026: The Centers for Medicare & Medicaid Services published an advance notice of proposed rulemaking in the Federal Register proposing a "Secure American Medical Supplies" designation and Medicare payment incentives for hospitals that procure domestically manufactured NIOSH-approved surgical N95 respirators, citing COVID-19 supply chain disruptions as a primary policy rationale.

- May 2025: Honeywell completed the divestiture of its Personal Protective Equipment business, including the North respiratory protection brand with its full N95 respirator portfolio, to Protective Industrial Products for USD 1.325 billion in an all-cash transaction. The acquisition expands PIP's global PPE footprint to 50 countries and combines 2 formerly competing distribution networks under a single ownership structure.

Global N95 Grade Medical Protective Mask Market Report Scope

The N95 Grade Medical Protective Mask Market encompasses the global industry involved in the manufacturing, distribution, and sales of high-efficiency respiratory protective devices. These devices are designed to achieve a tight facial seal and filter at least 95% of airborne particles.

The N95 Grade Medical Protective Mask Market is segmented by several key dimensions. By usage type, it is divided into Disposable and Reusable masks. By design features, the market includes Valve and Non‑valve options. By functional enhancements, products are categorized into Anti‑fog and Enhanced Filtration. By certification, masks are classified under NIOSH, CE, and FDA‑Aligned Medical Grade. By distribution channel, the market is segmented into Hospital Suppliers, Government Procurement, Industrial Distributors, Retail Pharmacies, and Online Retail.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Disposable |

| Reusable |

| Valve |

| Non-valve |

| Anti-fog |

| Enhanced filtration |

| NIOSH |

| CE |

| FDA-Aligned Medical Grade |

| Hospital Suppliers |

| Government Procurement |

| Industrial Distributors |

| Retail Pharmacies |

| Online Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Usage Type | Disposable | |

| Reusable | ||

| By Design Features | Valve | |

| Non-valve | ||

| By Functional Enhancements | Anti-fog | |

| Enhanced filtration | ||

| By Certification | NIOSH | |

| CE | ||

| FDA-Aligned Medical Grade | ||

| By Distribution Channel | Hospital Suppliers | |

| Government Procurement | ||

| Industrial Distributors | ||

| Retail Pharmacies | ||

| Online Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the N95 grade medical protective mask market by 2031?

The N95 grade medical protective mask market is projected to reach USD 6.73 billion by 2031 from USD 4.35 billion in 2026, at a 9.1% CAGR over 2026 to 2031.

Which region leads demand for N95 grade medical protective masks?

North America led with 37.23% share in 2025, supported by mature certification, healthcare procurement, and workplace compliance structures.

Which region is expanding the fastest for N95 grade medical protective masks?

Asia-Pacific is the fastest-growing region, with a projected 10.65% CAGR through 2031, supported by manufacturing expansion and supply diversification.

Why do disposable N95 respirators still lead over reusable models?

Disposable masks held 58.12% share in 2025 because hospitals and many employers prefer simpler infection-control and compliance workflows, even though reusable models are growing faster at 12.62% CAGR.

Which distribution channel is growing fastest for N95 mask sales?

Online retail is the fastest-growing channel at a 13.57% CAGR through 2031, driven by small buyers seeking speed and price visibility, though counterfeit risk remains a challenge.

What is the main competitive theme in this space right now?

Competition is centered on certification credibility, supply assurance, channel fit, and manufacturing geography, as shown by Honeywell’s PPE sale to PIP and Makrite’s Thailand-based supply positioning.

Page last updated on: