Peptic Ulcer Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.33 Billion |

| Market Size (2030) | USD 6.22 Billion |

| Growth Rate (2025 - 2030) | 5.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

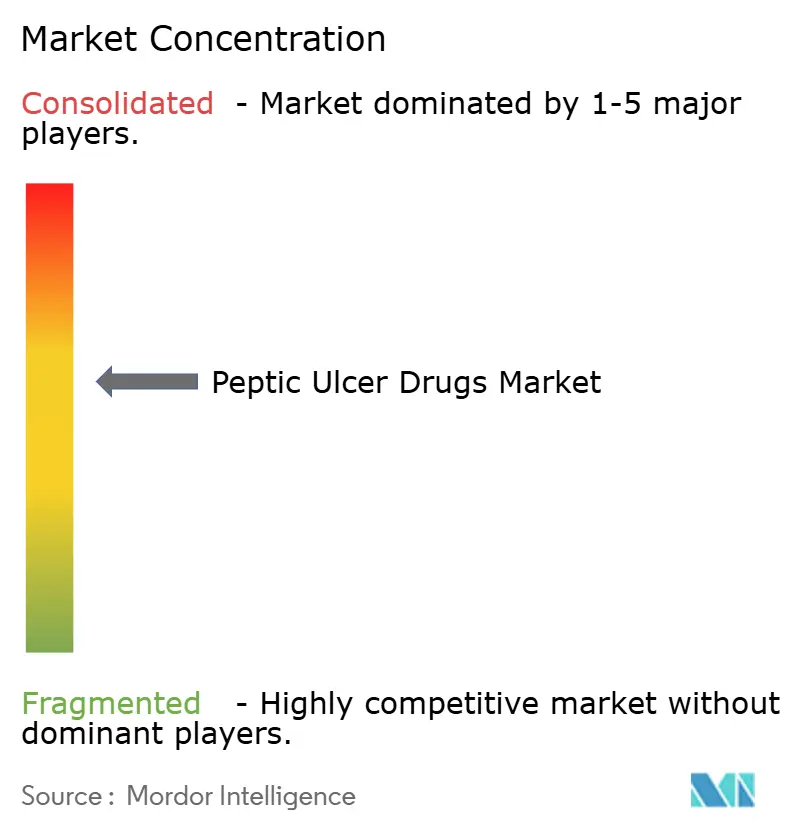

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peptic Ulcer Drugs Market Analysis by Mordor Intelligence

The peptic ulcer drugs market size reached USD 5.33 billion in 2025 and is forecast to climb to USD 6.22 billion by 2030, expanding at a 5.1% CAGR. Across the forecast horizon, premium uptake of potassium-competitive acid blockers (PCABs) offsets slowing proton pump inhibitor (PPI) volumes as prescribers move toward therapies with faster onset, fewer food-timing limitations, and improved long-term safety. Regulatory focus on cardiovascular and oncologic risks linked to chronic PPI exposure accelerates this therapeutic pivot and heightens competition in the peptic ulcer drugs market. Emerging combination regimens for Helicobacter pylori eradication, wider deployment of H. pylori screening programs, and the rapid growth of e-commerce dispensing channels further support topline expansion. At the same time, aggressive generic entry following imminent PPI patent cliffs restrains overall pricing power and intensifies portfolio diversification pressure.

Key Report Takeaways

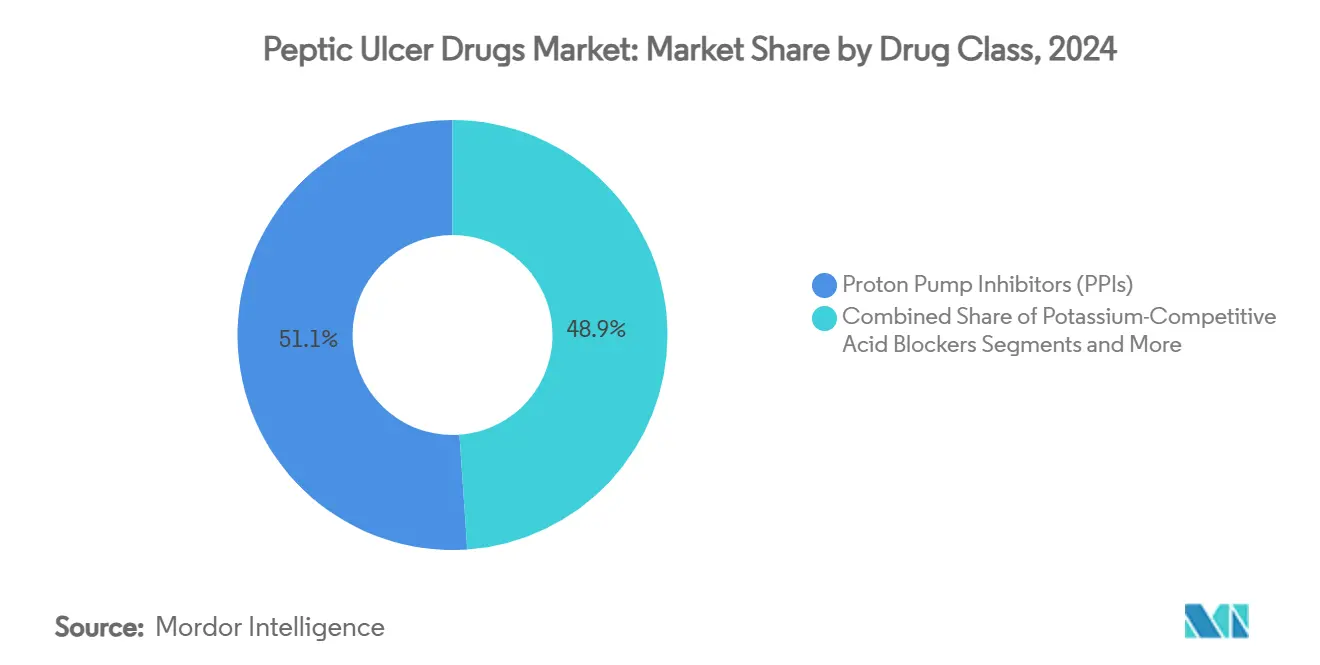

- By drug class, proton pump inhibitors retained 51.1% of the peptic ulcer drugs market share in 2024, while PCABs are projected to post the fastest 10.57% CAGR to 2030.

- By distribution channel, hospital pharmacies led with 43.3% revenue contribution in 2024; online pharmacies and e-commerce are set to surge at a 12.50% CAGR through 2030.

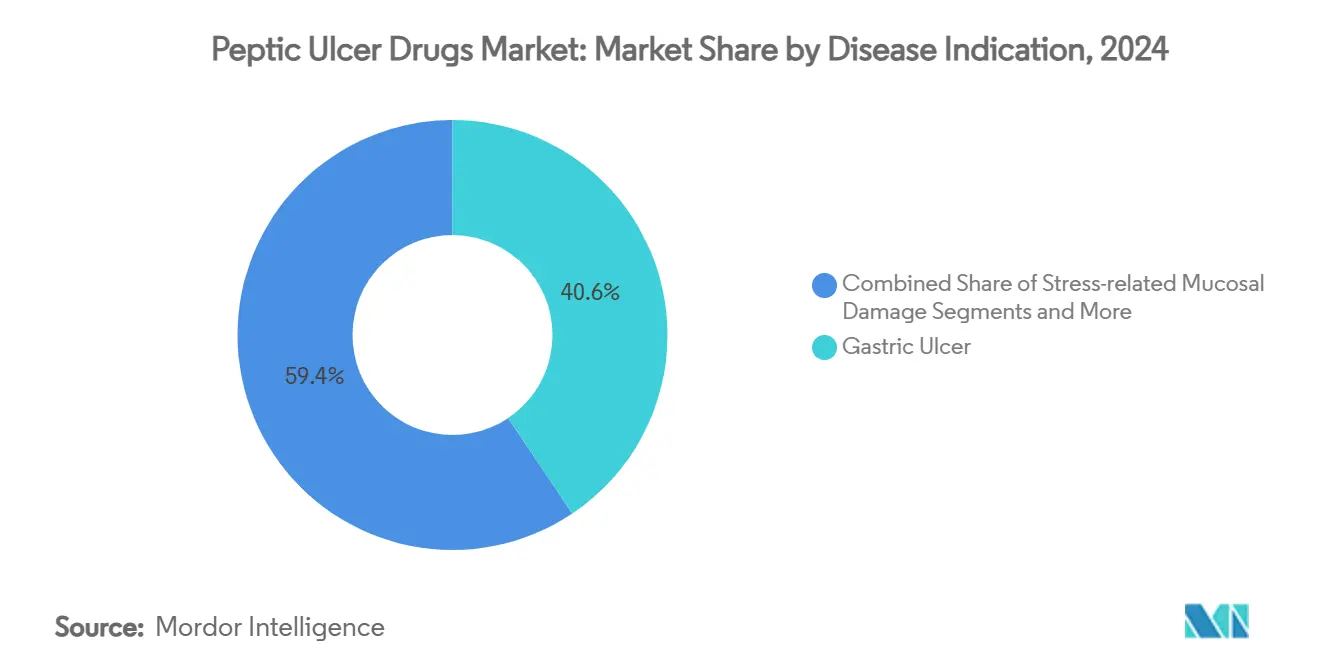

- By disease indication, gastric ulcers accounted for a 40.6% share of the peptic ulcer drugs market size in 2024, whereas stress-related mucosal damage is advancing at a 7.83% CAGR over the same period.

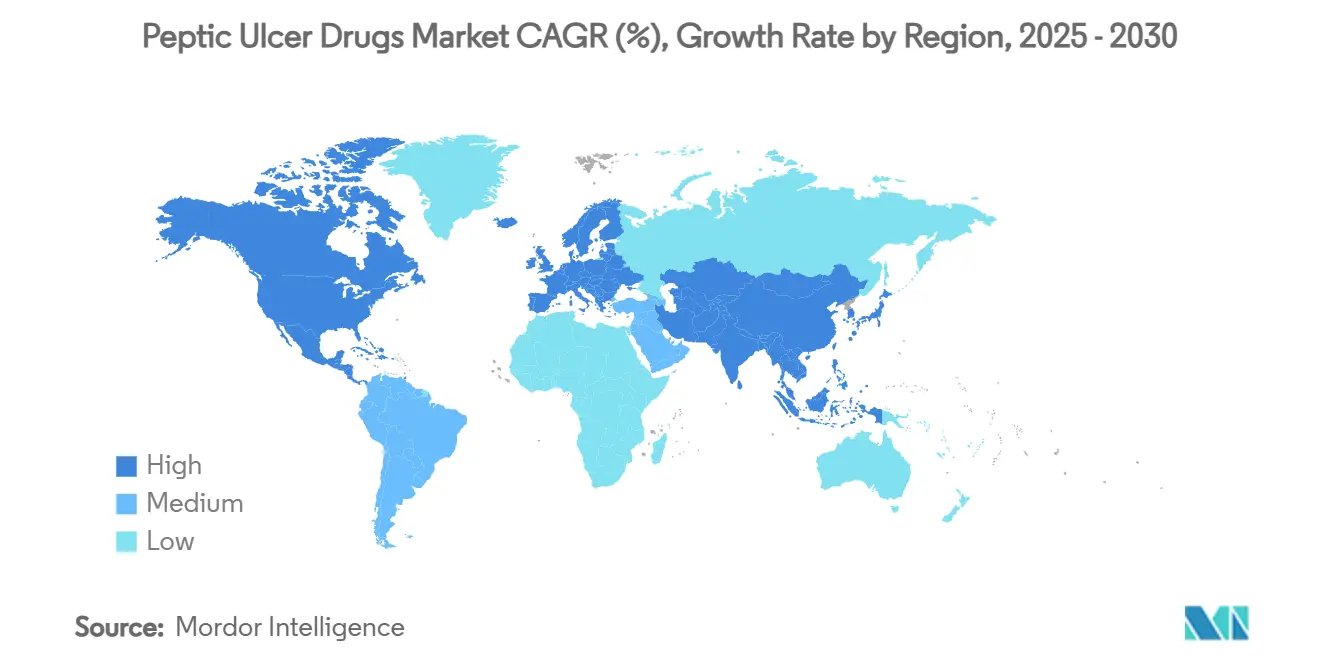

- By geography, North America commanded 30.2% of 2024 revenue, yet Asia Pacific is forecast to record the highest 5.17% CAGR to 2030.

Global Peptic Ulcer Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Helicobacter Pylori Infections In Emerging Markets | +1.20% | Asia Pacific, Middle East & Africa | Medium term (2-4 years) |

| Growing Geriatric Population And NSAID Usage | +0.80% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Advancements In Next-Generation Acid-Suppression Therapies (PCABs) | +1.50% | Global, early adoption in North America & Japan | Short term (≤ 2 years) |

| Increasing Adoption Of Combination H. Pylori Eradication Therapies | +0.70% | Global, particularly Asia Pacific | Medium term (2-4 years) |

| Expansion Of E-Commerce Pharmacies In LMICs | +0.60% | Asia Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| AI-Driven Drug-Repurposing For Gastro-Protective Agents | +0.30% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Helicobacter Pylori Infections in Emerging Markets

H. pylori infection persists at 57.1% among peptic ulcer patients and at 76.4% among individuals diagnosed with peptic ulcer disease across many Asia Pacific countries, perpetuating a sizeable treatment pool. Economic development has not yet produced parallel sanitation improvements in several lower-middle-income economies, so absolute case numbers remain elevated.[1]T. Ueda, “Prevalence of H. pylori Infection in Asia,” BMC Gastroenterology, bmcgastroenterol.biomedcentral.comGovernment-sponsored screening campaigns in China, Japan, and South Korea have increased early diagnosis rates, leading to higher prescription volumes for eradication regimens that frequently pair PCABs with multi-antibiotic combinations. The 2024 American College of Gastroenterology (ACG) guideline shift toward mandatory bismuth quadruple therapy further multiplies drug units dispensed per patient, which benefits manufacturers with broad antibiotic and gastro-protective portfolios. As emerging markets continue to urbanize, growing disposable incomes bolster adherence rates, preserving demand momentum in the peptic ulcer drugs market.

Growing Geriatric Population and NSAID Usage

A rapidly aging population intensifies gastric mucosal vulnerability while simultaneously driving chronic NSAID consumption for osteoarthritis and other degenerative disorders. Epidemiological evidence shows that elderly individuals experience triple the incidence of ulcers in younger cohorts.[2]American College of Gastroenterology, “Clinical Guideline: H. pylori Infection,” American Journal of Gastroenterology, journals.lww.com In North America and Europe, clinicians frequently co-prescribe gastro-protective agents with long-term NSAIDs, creating predictable, high-frequency refill cycles. Because seniors display heightened sensitivity to adverse renal and skeletal events attributed to long-term PPI exposure, prescribers gravitate toward PCABs, which exhibit superior acid control without meal-timing constraints. Premium, geriatric-tailored formulations consequently secure above-average margins and reinforce brand loyalty within the peptic ulcer drugs market.

Advances in Next-Generation Acid-Suppression Therapies (PCABs)

Vonoprazan delivered 93% healing versus 85% for lansoprazole in head-to-head erosive esophagitis trials while offering a notably faster onset and 24-hour pH control.[3]NEJM Journal Watch, “Vonoprazan vs PPIs in Erosive Esophagitis,” nejmjournalwatch.org The FDA’s July 2024 approval of VOQUEZNA marked the first new acid-suppression class in three decades and validated the mechanistic advantage of competitive potassium binding. Tegoprazan has since reported Phase 3 non-inferiority with a cleaner safety profile, and fexuprazan achieved >95% healing in Asian post-marketing surveillance. These data points catalyze formulary inclusion at premium price bands, redirecting prescribing away from commoditized PPIs and lifting overall revenue per prescription across the peptic ulcer drugs market.

Increasing Adoption of Combination H. Pylori Eradication Therapies

The 2024 ACG update discourages clarithromycin-based triple therapy in regions with >15% resistance, mandating bismuth quadruple therapy instead. Quadruple regimens require four active ingredients—often including a PCAB—over 10-14 days, raising the course cost and complexity. Pharmaceutical companies offering fixed-dose combinations or high-convenience blister packs record elevated uptake, particularly in Asia Pacific, where eradication drives gastric cancer prevention efforts. Vonoprazan-based quadruple therapy achieved 90.6% eradication compared with 85.2% for lansoprazole-based comparators, reinforcing PCAB positioning as the preferred acid-suppressive backbone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent Expiries Driving Generic Price Erosion | -1.80% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Long-Term PPI Safety Concerns Triggering Regulatory Scrutiny | -1.10% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Rising H. Pylori Antimicrobial Resistance | -0.70% | Global, particularly Asia Pacific | Medium term (2-4 years) |

| Consumer Shift To Herbal / Natural Ulcer Remedies | -0.40% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries Driving Generic Price Erosion

Pantoprazole loses exclusivity in December 2026, and esomeprazole faces remaining secondary expirations in 2025 across major European jurisdictions, exposing more than USD 350 billion in aggregate branded sales to rapid 80-90% price compression. Multinational firms front-load promotional spend to maximize value pre-expiry, then pivot toward PCAB launches, over-the-counter switches, or emerging-market penetration. The manoeuvre cushions top-line decline but cannot fully offset the volume-driven margin squeeze now spreading across the peptic ulcer drugs market.

Long-Term PPI Safety Concerns Triggering Regulatory Scrutiny

A 2024 pharmacovigilance review cataloged 3,133 tumor events linked to PPIs, with gastric cancer representing 19.05% of reports; nearly 30% of those cases were fatal. Prompted by such findings, the FDA and EMA expanded label warnings for fracture, C. difficile infection and chronic kidney disease. Clinicians increasingly limit courses to 8-12 weeks, creating space for PCABs and H2 receptor antagonists positioned as safer long-term maintenance options, thereby reshaping demand patterns inside the peptic ulcer drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: PCABs Challenge PPI Dominance

PPIs generated 51.1% of global revenue in 2024, yet their hold on the peptic ulcer drugs market is thinning as PCABs post a 10.57% CAGR to 2030. Vonoprazan’s U.S. approval validated PCAB pharmacology, while Japan, South Korea, and, more recently, India have embraced local launches at premium list prices. Several health-technology-assessment bodies now rate PCABs as cost-effective when factoring in higher healing rates and lower retreatment costs. Histamine-2 receptor antagonists retain a role in nocturnal symptom control for cost-sensitive patients, whereas antacids function mainly as adjunctive over-the-counter aids.

Pipeline diversity broadens defensive strategies. AstraZeneca’s esomeprazole magnesium delayed-release sachets cater to pediatrics, Takeda advances tegoprazan plus antibiotic fixed-dose combinations, and Pfizer explores AI-guided reformulations aimed at once-weekly dosing. These projects seek to maintain relevance as the peptic ulcer drugs market migrates toward differentiated acid suppressors and multi-mechanistic eradication packs.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies captured a 43.3% share of 2024 sales due to the complexity of acute bleeding management and quadruple-therapy induction that mandates inpatient monitoring. Nevertheless, online channels are accelerating at a 12.50% CAGR, outpacing retail outlets and siphoning volume from traditional brick-and-mortar chains. Digital pharmacies embed e-prescription verification, automated refill reminders, and doorstep delivery, features that resonate strongly with chronic gastritis and GERD patients who demand convenience and cost transparency. In response, leading chains in the United States and Germany have rolled out hybrid omnichannel models that combine tele-consultations with same-day pick-up, a tactic that preserves foot traffic while capturing digital share in the peptic ulcer drugs market.

By Disease Indication: Stress-Related Damage Emerges

Gastric ulcers remained the largest indication at 40.6% of global prescriptions in 2024, yet stress-related mucosal damage is expanding fastest at 7.83% CAGR. Rising workplace stress, senior-citizen polypharmacy and widespread NSAID usage drive this uptick. Clinical protocols now endorse prophylactic PCAB co-therapy for high-risk cardiovascular patients receiving dual antiplatelets, thereby broadening prophylaxis beyond classic ulcer cohorts. Duodenal ulcers and Zollinger-Ellison syndrome form niche segments, but their high treatment intensity sustains double-digit per-patient revenues. Preventive positioning aligns with evolving payer incentives that reward reduced hospitalization for upper-GI bleeding, reinforcing demand for potent, rapid-acting agents inside the peptic ulcer drugs market.

Geography Analysis

North America held 30.2% of 2024 revenue, aided by premium reimbursement for novel PCABs, timely H. pylori diagnostics, and a mature biologics supply chain. Vonoprazan’s swift formulary adoption and impending tegoprazan application have energized competition, mitigating volume loss from PPI patent expiry. Price erosion remains pronounced once generics enter, yet manufacturers offset erosion via patient-assistance programs that foster brand retention.

Europe ranked second by size but registered tempered growth due to austerity-driven price caps and aggressive tendering that favor generics. EMA pharmacovigilance demands elevate trial costs, slowing SME entry yet benefiting multinationals with robust compliance infrastructure. National health systems widely reimburse bismuth quadruple therapy, encouraging procurement of bundled packs that dovetail with antimicrobial-resistance stewardship.

Asia Pacific posted the swiftest 5.17% CAGR, propelled by China’s Healthy Stomach initiative, Japan’s entrenched PCAB heritage, and India’s fast-growing middle class that values branded generics. Government-led screening campaigns boost H. pylori detection, translating to elevated eradication therapy volumes. Local manufacturing incentives, such as India’s Production-Linked Incentive scheme, reduce unit costs and improve accessibility, accelerating patient conversion within the peptic ulcer drugs market. Middle East & Africa and South America contribute smaller shares but show rising urban adoption of e-commerce pharmacies, a trend expected to lift therapy penetration despite macroeconomic volatility.

Competitive Landscape

The peptic ulcer drugs market displays moderate fragmentation. The combined share for the five largest companies sits near 45%, leaving room for specialized entrants. AstraZeneca, Takeda, and Pfizer defend legacy PPI franchises while reinvesting in PCAB expansion. Phathom Pharmaceuticals leveraged orphan-drug-style exclusivity to secure rapid VOQUEZNA uptake. Sun Pharma’s domestic launch of fexuprazan in India and Sebela’s forthcoming U.S. filing for tegoprazan illustrate regional scaling of the PCAB class.

Strategic themes include fixed-dose combination innovation, AI-enabled molecule scouting, and omnichannel patient engagement. Larger firms invest in companion-diagnostic algorithms that match eradication regimens to local resistance patterns, thereby boosting success rates and justifying premium pricing. In parallel, digital adherence platforms collect real-world evidence that feeds post-marketing safety databases, supporting favorable formulary renewal. White-space opportunities encompass pediatric chewables, geriatric low-dose sprinkle capsules, and stress-ulcer prevention kits for intensive-care settings, each segment promising differentiated revenue pools within the peptic ulcer drugs market.

Peptic Ulcer Drugs Industry Leaders

Takeda Pharmaceutical

AstraZeneca

Pfizer

Dr. Reddy’s Laboratories

GlaxoSmithKline

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sebela Pharmaceuticals announced positive Phase 3 TRIUMpH data for tegoprazan, setting up a planned Q4 2025 FDA submission.

- April 2025: Sun Pharmaceutical introduced fexuprazan 40 mg tablets in India under the brand name Fexuclue, achieving the first PCAB entry in the country.

- March 2025: Phathom Pharmaceuticals launched a VOQUEZNA awareness campaign featuring actor Kenan Thompson to enhance patient engagement for GERD treatment.

- February 2025: Takeda entered a non-exclusive patent license with Lupin to commercialize vonoprazan in India, opening a high-volume emerging market.

Global Peptic Ulcer Drugs Market Report Scope

| Proton Pump Inhibitors (PPIs) |

| Potassium-Competitive Acid Blockers (PCABs) |

| Histamine-2 Receptor Antagonists (H2RAs) |

| Antacids |

| Antibiotics |

| Ulcer-Protective Agents |

| Gastric Ulcer |

| Duodenal Ulcer |

| Stress-related Mucosal Damage |

| Others |

| Hospital Pharmacies |

| Retail/Drug Stores |

| Online Pharmacies & E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Proton Pump Inhibitors (PPIs) | |

| Potassium-Competitive Acid Blockers (PCABs) | ||

| Histamine-2 Receptor Antagonists (H2RAs) | ||

| Antacids | ||

| Antibiotics | ||

| Ulcer-Protective Agents | ||

| By Disease Indication | Gastric Ulcer | |

| Duodenal Ulcer | ||

| Stress-related Mucosal Damage | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail/Drug Stores | ||

| Online Pharmacies & E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the peptic ulcer drugs market?

The peptic ulcer drugs market size reached USD 5.33 billion in 2025 and is projected to grow to USD 6.22 billion by 2030 at a 5.1% CAGR.

Which drug class is growing fastest within the peptic ulcer drugs market?

Potassium-competitive acid blockers are expanding at a 10.57% CAGR, outpacing traditional proton pump inhibitors.

Why are PCABs preferred over PPIs for long-term therapy?

PCABs offer faster acid suppression, flexible dosing without meal timing and fewer long-term safety concerns associated with cardiovascular and oncologic risks.

Which region will show the highest growth in the peptic ulcer drugs market through 2030?

Asia Pacific is forecast to post the fastest 5.17% CAGR due to expanding middle-class populations, higher NSAID usage and proactive H. pylori screening programs.

How will patent expiries influence competitive dynamics?

Expiring pantoprazole and esomeprazole patents will trigger generic price erosion, compelling originators to accelerate PCAB launches and explore fixed-dose combinations.

What distribution channel is gaining importance for chronic gastrointestinal therapies?

Online pharmacies and e-commerce platforms are growing at a 12.50% CAGR, driven by convenience, price transparency and automated refill services for maintenance therapy.

Page last updated on: