Ulcerative Colitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.02 Billion |

| Market Size (2031) | USD 13.59 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

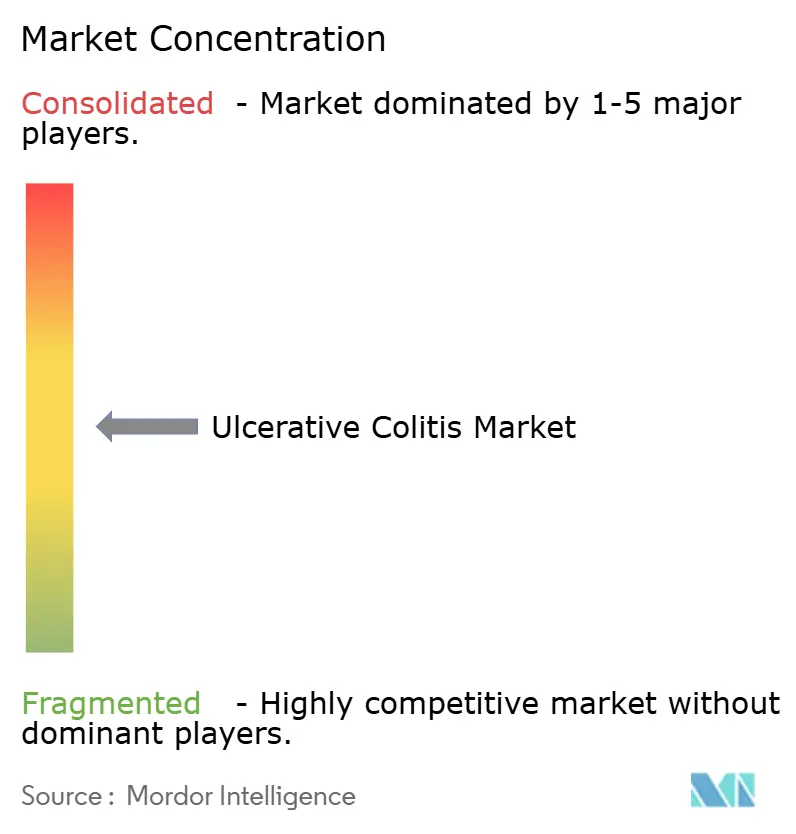

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ulcerative Colitis Market Analysis by Mordor Intelligence

The ulcerative colitis market size is expected to grow from USD 10.56 billion in 2025 to USD 11.02 billion in 2026 and is forecast to reach USD 13.59 billion by 2031 at 4.31% CAGR over 2026-2031. This steady trajectory reflects a shift from aging anti-TNF blockbusters to competitively priced biosimilars, even as premium-priced IL-23 and S1P innovations secure rapid uptake. Anti-TNF agents still provide broad clinical familiarity but now lose ground to fast-growing oral JAK inhibitors that expand treatment to ambulatory settings. Rectal formulations gain traction because targeted drug delivery improves tolerance in distal disease, while hospital pharmacies protect their dominant role through specialist oversight of cold-chain biologics. Growing patient advocacy, broader reimbursement caps in the United States, and Asia-Pacific incidence spikes create fresh volume opportunities that partially offset price pressure in mature regions.

Key Report Takeaways

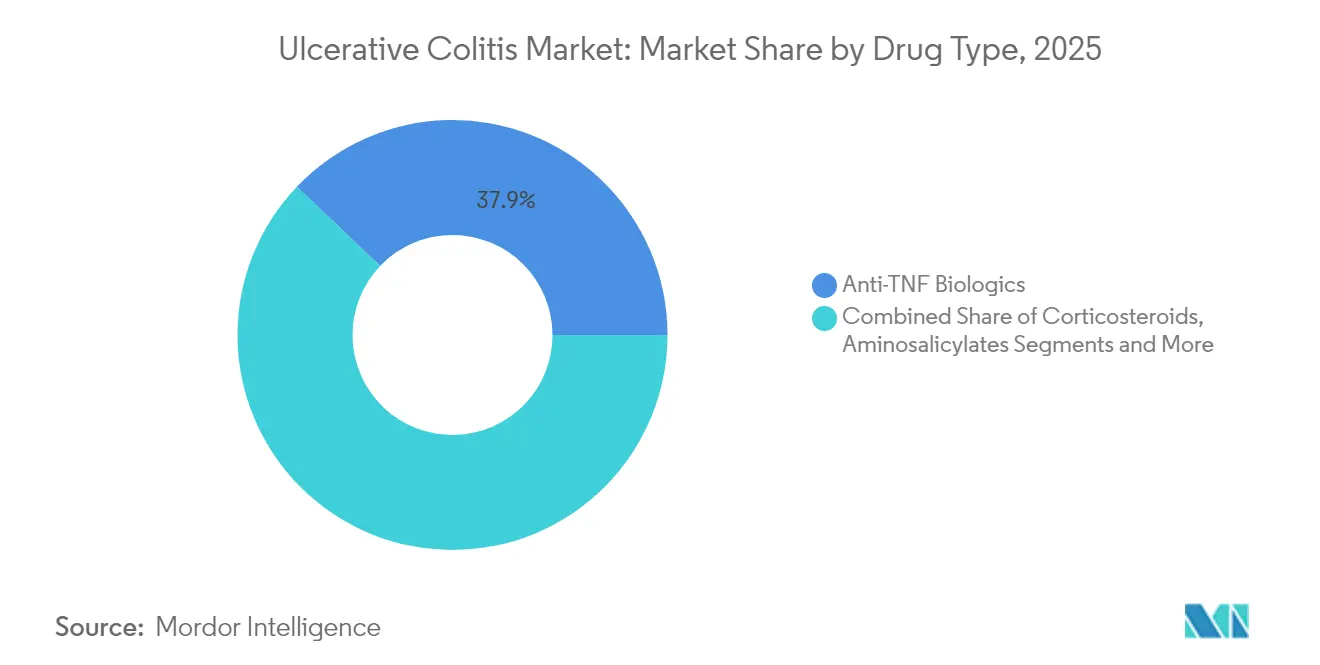

- By drug class, anti-TNF biologics led with 37.88% revenue share in 2025; JAK inhibitors are forecast to expand at a 13.68% CAGR through 2031.

- By disease type, pancolitis accounted for a 30.10% share of the ulcerative colitis market size in 2025, while fulminant colitis is advancing at an 8.41% CAGR through 2031.

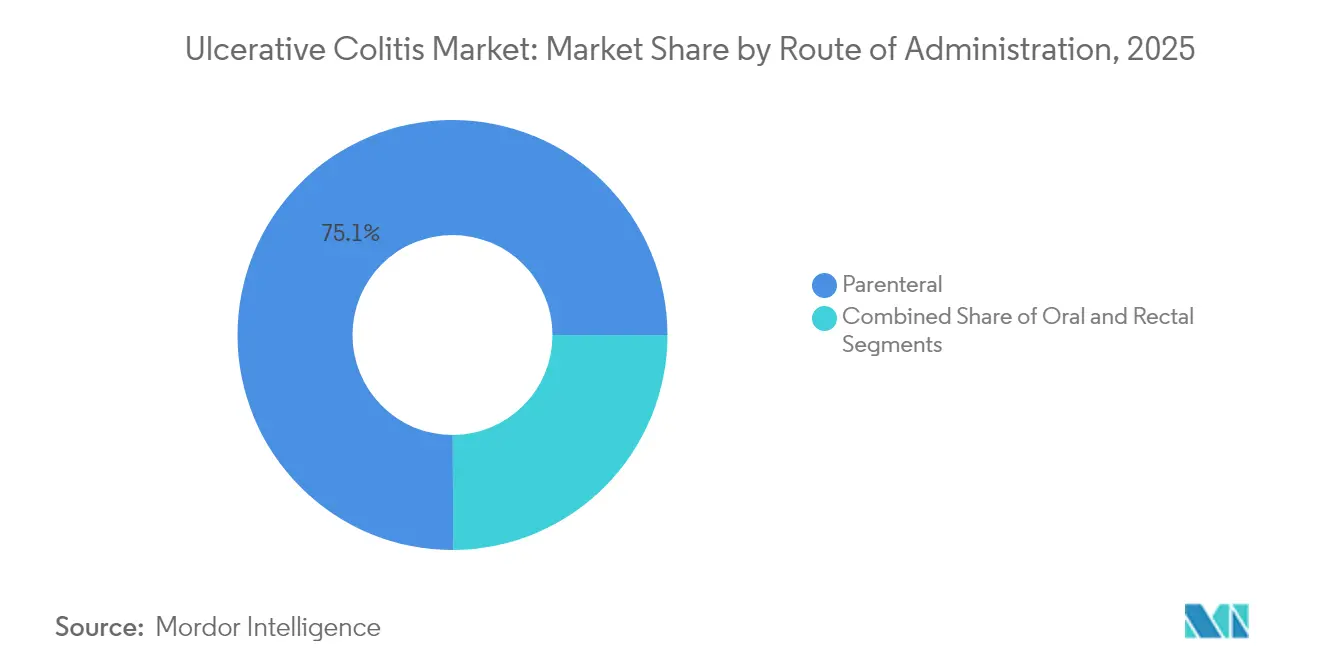

- By route of administration, parenteral products held 75.05% of ulcerative colitis market share in 2025; rectal formulations post the fastest 8.12% CAGR to 2031.

- By distribution channel, hospital pharmacies controlled 49.15% revenue in 2025, yet online pharmacies record the highest 8.79% CAGR through 2031.

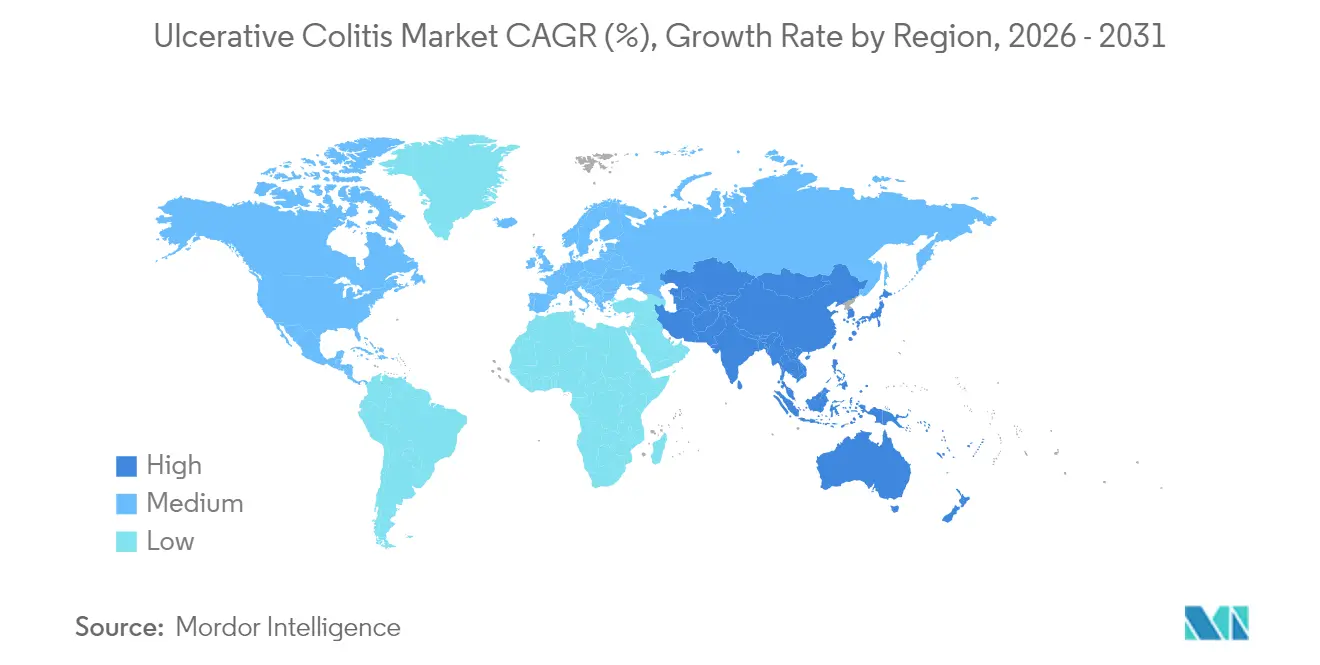

- By geography, North America commanded 43.25% of 2025 global revenue, whereas Asia-Pacific is rising at a 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ulcerative Colitis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global incidence and prevalence of UC | +1.2% | Global, highest in Asia-Pacific | Medium term (2-4 years) |

| Continuous launch of advanced biologics and small-molecule drugs | +1.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Expansion of patient-assistance and reimbursement programs | +0.9% | Global, emphasis on emerging markets | Medium term (2-4 years) |

| Growing use of tele-health and remote monitoring in IBD care | +0.6% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Rapid progress in microbiome-based therapeutics | +0.7% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continuous Launch of Advanced Biologics & Small-Molecule Drugs

IL-23 antagonists such as Tremfya, Skyrizi, and Omvoh captured 10% of advanced systemic prescriptions within 12 months, signalling clinician openness to mechanism diversification. Velsipity became the first S1P modulator to gain FDA approval, reaching 26% 12-week remission versus 11% for placebo, and reinforcing the commercial appeal of once-daily oral solutions[1]European Medicines Agency, “Velsipity,” Ema.europa.eu. Takeda tripled Entyvio output at its Japanese plant, demonstrating manufacturers’ race to secure capacity ahead of expected demand growth. Johnson & Johnson reported 63.5% clinical response in Phase 2b testing of oral icotrokinra, underlining the strong pipeline depth. Collectively, these launches raise therapeutic ceilings, shorten treatment sequences, and enlarge the ulcerative colitis market by attracting previously undertreated patients.

Rising Global Incidence & Prevalence of UC

Asia-Pacific incidence multiplied sixfold over two decades as dietary Westernization and urban stressors emerged, pushing previously low-burden countries toward parity with Western markets. Population growth and earlier diagnosis swell the addressable pool even as life-long management lengthens treatment duration. Wearables such as Apple Watch and Fitbit can pre-emptively flag flares, enabling earlier physician intervention and reducing severe hospitalization risk[2]Robert Hirten, “Wearable devices can detect and predict inflammatory bowel disease flare-ups,” Sciencedaily.com. Payers monitor these epidemiologic and technology trends to refine cost-containment strategies, yet higher caseloads still translate to incremental biologic volumes. Rising prevalence therefore enlarges both volume opportunity and healthcare resource stress, sustaining medium-term expansion of the ulcerative colitis market.

Expansion of Patient-Assistance & Reimbursement Programs

Manufacturers’ copay cards push monthly costs as low as USD 0 for eligible US patients while Medicare will cap annual out-of-pocket exposure at USD 2,000 from 2025, narrowing financial barriers. Emerging-market governments also negotiate large biologic price cuts, illustrated by Colombia’s USD 18,428 annual average versus markedly higher US invoices. These moves widen therapeutic adoption, stabilizing revenue erosion from biosimilars. Assistance programs meanwhile strengthen brand loyalty, supporting steady unit flows through hospital and specialty pharmacy channels that anchor the ulcerative colitis market.

Growing Use of Tele-Health & Remote Monitoring in IBD Care

Cleveland Clinic's integration of Ayble Health's AI platform combines nutrition, behavioral tracking, and real-time symptom feedback to sustain remission outside clinic walls. German tertiary centers posted 91.3% virtual-visit adherence, proving digital models can match in-person continuity. Pfizer's PRISM intestinal ultrasound initiative provides non-invasive disease monitoring that helps reduce colonoscopy frequency. AI systems such as EndoBRAIN-UC predict relapse via vascular healing signals, empowering proactive medication adjustments. Tele-health therefore complements physician capacity, enlarges touchpoints, and supports long-term control, indirectly lifting adherence-driven revenue in the ulcerative colitis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Serious adverse events and safety warnings limiting uptake | -1.4% | Global, stricter in EU & US | Short term (≤ 2 years) |

| High treatment costs in emerging economies | -0.8% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Loss of exclusivity for blockbuster biologics driving price erosion | -1.1% | Global, immediate in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Serious Adverse Events & Safety Warnings Limiting Uptake

The ORAL Surveillance study linked JAK inhibitors with elevated major adverse cardiac events and malignancies, triggering FDA directives to reserve the class for anti-TNF failures and prompting EMA caution in higher-risk patients. Updated guidelines emphasize risk-benefit assessment, infection screening, and dose tailoring, increasing physician workload and slowing initial uptake. EULAR data show no broad cancer spike versus biologic DMARDs except keratinocyte tumors, but regulators remain vigilant. Heightened pharmacovigilance therefore tempers near-term prescriptions despite clinical convenience advantages.

Loss of Exclusivity for Blockbuster Biologics Driving Price Erosion

Stelara’s US and EU patents expired by early 2024, enabling eight biosimilar launches at up to 90% discounts and causing 14.7% revenue drop within a year. Amgen’s Wezlana gained interchangeability status, fast-tracking formulary switches, while Medicare’s Inflation Reduction Act will negotiate further reductions from 2026. Price compression narrows absolute dollar growth even as volume persists, challenging branded revenues and shifting focus toward novel assets to sustain the ulcerative colitis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Oral Innovation Expands Treatment Choice

Anti-TNF biologics preserved leadership with 37.88% share in 2025, underpinned by a robust evidence base and physician familiarity. Yet biosimilar pressure and safety-driven laddering redirect growth to JAK inhibitors, which post a 13.68% CAGR through 2031. Upadacitinib shows rapid onset and durable remission, while tofacitinib retains a foothold despite boxed warnings. The ulcerative colitis market size for JAK inhibitors is projected to rise sharply as oral convenience appeals to both patients and payers seeking home-based regimens.

IL-23 antagonists deliver differentiated efficacy, enabling 10% advanced systemic uptake inside a year, and their less frequent dosing targets quality-of-life advantages. S1P modulators introduce a first-in-class lymphocyte egress blockade, widening oral options. Anti-integrin vedolizumab sustains gut-selective appeal, while calcineurin inhibitors remain niche rescue agents. Drug-class diversification illustrates the ulcerative colitis industry pivot to precision medicine, where biomarker-guided selection narrows responder cohorts and maximizes lifetime value per patient.

By Disease Type: Emergency Protocol Innovation Shapes Growth

Pancolitis secured 30.10% of 2025 revenue, reflecting its extensive colonic involvement that justifies early biologic escalation and combination therapy. The ulcerative colitis market size for pancolitis will expand steadily with guideline shifts endorsing proactive biologic initiation.

Fulminant colitis, though clinically uncommon, shows the fastest 8.41% CAGR as updated rescue algorithms employ high-dose steroids, infliximab, cyclosporine, and emergent JAK inhibitors to defer colectomy. International Delphi consensus on acute severe trial design accelerates new asset development, fostering specialized hospital demand. Heterogeneous disease presentation underscores why companies package portfolio breadth, ensuring each phenotype meets an optimized mechanism.

By Route of Administration: Patient Preference Drives Shifts

Parenteral biologics captured 75.05% revenue in 2025 because moderate-to-severe disease still warrants intravenous or subcutaneous delivery under clinical supervision. Yet patient convenience and distal disease prevalence boost rectal foam, enema, and suppository uptake, which show an 8.12% CAGR. The ulcerative colitis market share for rectal options therefore rises as 5-aminosalicylate optimization gains renewed focus.

Takeda’s FDA nod for subcutaneous Entyvio extends home-injection flexibility, blending parenteral potency with self-administration ease. Oral dosing growth stems from emerging JAK and S1P assets that fit tele-health oversight models. Future pipeline assets target delayed-release colonic delivery or micro-capsule biologics, indicating that administration innovation remains a core differentiator in the ulcerative colitis market.

By Distribution Channel: Digital Pathways Reshape Access

Hospital pharmacies controlled 49.15% of 2025 value by managing prior authorization, cold-chain and infusion services. Nevertheless, online specialty networks post 8.79% CAGR as they bundle copay support, adherence reminders, and same-day cold logistics. The ulcerative colitis market size within online channels will scale as insurers embrace mail-order to cut dispensing fees.

Retail chains sustain oral drug refill business but may lose share if specialty hubs dominate high-value biologics. Manufacturers now partner with digital pharmacies to preload patient onboarding and nursing coordination, reinforcing brand retention. COVID-19-induced home delivery normalised remote access, accelerating a lasting omnichannel model across the ulcerative colitis industry.

Geography Analysis

North America retained 43.25% of global revenue in 2025 due to early biologic adoption, rich specialist density, and comprehensive reimbursement ceilings that drop annual patient costs to USD 2,000 from 2025. US gastroenterologists expect near-term volume growth for Entyvio, Simponi, and infliximab biosimilars, sustaining competitive churn yet enlarging treated patient pools. FDA pediatric guidance encourages expanded trials, promising future label extensions and continued ulcerative colitis market expansion.

Asia-Pacific records a 7.23% CAGR through 2031 as incidence rises alongside economic development, healthcare spending, and IBD awareness campaigns. China’s age-standardized incidence now ranks at 2.1 per 100,000 and rising, with payer prioritization still favoring cost-effective 5-aminosalicylate pathways before biologic escalation. Regional governments negotiate volume-based procurements to widen biologic access, while private insurers proliferate in urban centers, enhancing affordability for mid-income populations. These tailwinds lift both volume and value within the ulcerative colitis market.

Europe posts stable yet moderated growth amid HTA scrutiny and rapid biosimilar rollout. EMA approved four ustekinumab biosimilars in 2024, strengthening discount pools that widen access but squeeze absolute revenue. NICE’s ongoing etrasimod appraisal underscores strict comparative-effectiveness thresholds before national uptake. Despite pressure, EU markets embrace mechanism diversity, maintaining a balanced landscape that offers predictable albeit modest expansion for the ulcerative colitis market.

Mordor Intelligence provides coverage of the ulcerative colitis market across other key regional markets. Detailed country-level analysis extends to China incorporating local coverage and market participation, as required.

Competitive Landscape

The ulcerative colitis market functions as a dynamic oligopoly. AbbVie expands beyond Humira exhaustion through Skyrizi’s UC label and a USD 1.56 billion deal for FG-M701, a TL1A antibody promising fewer doses and deeper remission. Johnson & Johnson marries Tremfya’s rapid penetration with icotrokinra’s promising oral data while seeking to soften Stelara erosion by geographic sequencing and formulation tweaks. Merck’s USD 10.8 billion Prometheus acquisition injects PRA023, offering potential first-in-class anti-TL1A synergy.

Class competition intensifies around IL-23s, where marketers pursue dosing convenience and safety messaging more than price undercutting. Sanofi and Teva’s USD 1.5 billion duvakitug alliance further crowds the pathway. Manufacturing scale becomes critical; Takeda tripled Entyvio capacity, while Resilience committed USD 225 million to support third-party biologic fill-finish, assuring supply dependability. AI-enabled drug design by Insilico Medicine heralds future entrants that could compress discovery timelines and diversify oral assets. Competitive positioning now blends pipeline velocity, real-world data generation, and integrated patient support to secure durable share inside the ulcerative colitis industry.

Ulcerative Colitis Industry Leaders

Merck & Co., Inc.,

Novartis AG

Bausch Health Companies Inc.

Johnson & Johnson

AbbVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson & Johnson announced 63.5% Phase 2b response for oral icotrokinra in ulcerative colitis.

- December 2024: Teva and Sanofi reported 47.8% remission for high-dose duvakitug in Phase IIb UC study.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global ulcerative colitis market as the annual value of prescription medicines, small molecules and biologics, plus medically necessary colectomy and related hospital, pharmacy dispensing fees for all age groups. According to Mordor Intelligence, revenue from patient-assistance programs and biosimilar uptake sits inside this boundary.

Scope exclusion: diagnostic test kits, over-the-counter supplements, wellness apps, and monitoring wearables lie outside scope.

Segmentation Overview

- By Drug Type

- Aminosalicylates

- Corticosteroids

- Immunosuppressants

- Anti-TNF Biologics

- Anti-Integrin Biologics

- JAK Inhibitors

- S1P Receptor Modulators

- Calcineurin Inhibitors

- Other Drug Types

- By Disease Type

- Ulcerative Proctitis

- Proctosigmoiditis

- Left-sided Colitis

- Pancolitis / Universal Colitis

- Fulminant Colitis

- By Route of Administration

- Oral

- Parenteral

- Rectal

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Several discussions with gastroenterologists, hospital pharmacists, payers, and procurement officers across North America, Europe, and Asia Pacific clarified real-world dosing, biosimilar discounts, and emerging surgical rates, letting us firm up desk-derived assumptions.

Desk Research

We began with epidemiology series from WHO, CDC, and the European Crohn's and Colitis Organisation, then matched them with drug-import data in UN Comtrade and price lists in NHS England and Japan NHI. Company filings disclosed branded sales, while paid assets such as D&B Hoovers and Dow Jones Factiva added triangulating revenue clues. Peer-reviewed journals and investor news outlined pipeline timing and therapy mix shifts. The sources named are illustrative, and many others informed our desk analysis.

Market-Sizing & Forecasting

We developed a top down and bottom up blended model that converts prevalence cohorts into treated patient counts and multiplies them by average annual therapy spend to reconstruct 2025 demand. Supplier roll-ups and channel price checks validate totals. Incidence drift, biologic to oral shift, biosimilar discount curves, treatment duration changes, and payer reimbursement intensity feed a multivariate regression with ARIMA overlay that extends the view to 2030. When brand sales are hidden, we impute values from shipment proxies and cost of goods disclosures.

Data Validation & Update Cycle

Outputs pass variance checks, peer reviews, and leadership sign-off. Models refresh each year, or faster when events warrant, and interim updates trigger when major approvals or reimbursement moves occur. A final sense check precedes delivery.

Why Mordor's Ulcerative Colitis Baseline Commands Reliability

Published estimates differ because teams vary scope, disease severity splits, and exchange rate cut-offs. Mordor anchors its baseline in treated patient math, keeps currency current, and refreshes it every twelve months, giving clients a balanced, transparent midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 10.56 B, 2025 | Mordor Intelligence | |

| 8.00 B, 2024 | Global Consultancy A | Drugs only, fixed 2023 FX |

| 7.39 B, 2024 | Trade Journal B | Mild cases only, uniform co-pay |

The 8 billion figure comes from a 2025 global outlook. The 7.39 billion figure is extracted from a 2025 trade snapshot. The spread shows how narrower scope and older currency weaken totals, while our disciplined variables deliver a dependable baseline for strategic calls.

Key Questions Answered in the Report

What is the current size of the ulcerative colitis market?

The market was valued at USD 11.02 billion in 2026 and is forecast to reach USD 13.59 billion by 2031.

Which drug class is growing the fastest?

JAK inhibitors post the highest 13.68% CAGR between 2026 and 2031, driven by oral convenience and rapid symptom control.

Why is Asia-Pacific the fastest-growing region?

Incidence has climbed sixfold, healthcare spending is rising, and governments are improving biologic affordability, supporting a 7.23% CAGR.

How will patent expirations affect pricing?

Stelara biosimilars launched at up to 90% discounts, and similar erosion is expected for other biologics, compressing branded revenues.

What role does tele-health play in ulcerative colitis management?

Virtual platforms maintain over 90% appointment adherence, integrate symptom monitoring, and support earlier intervention, enhancing long-term disease control.

Page last updated on: