Diabetic Foot Ulcer Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

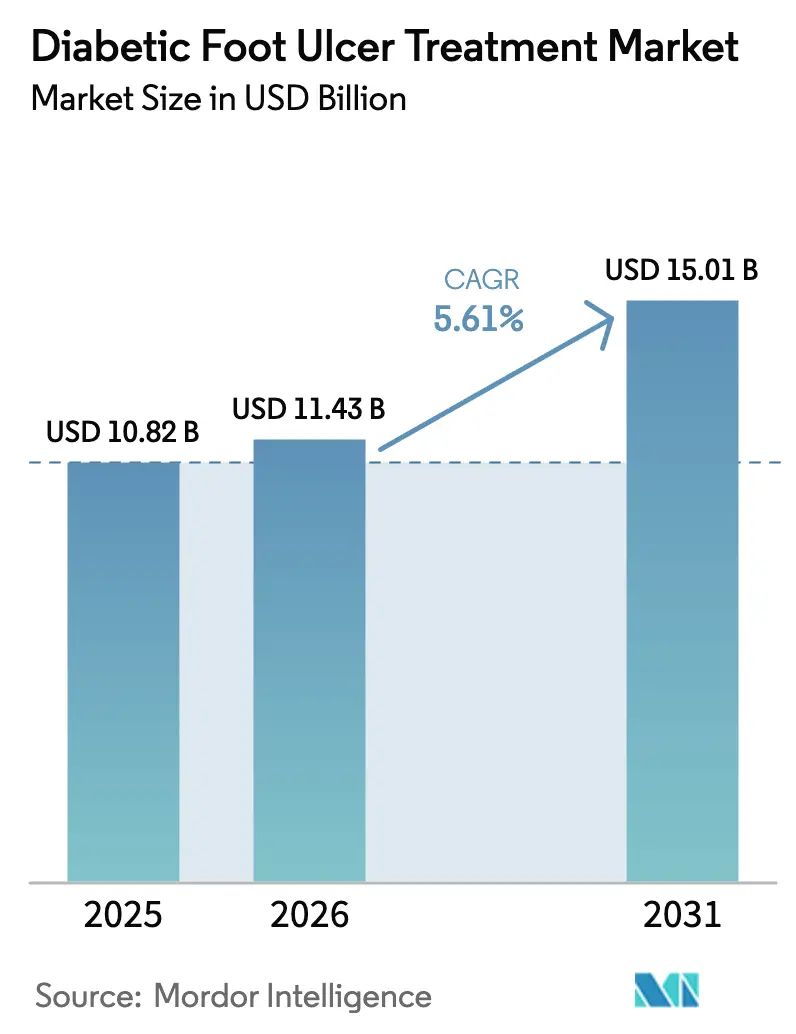

| Market Size (2026) | USD 11.43 Billion |

| Market Size (2031) | USD 15.01 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diabetic Foot Ulcer Treatment Market Analysis by Mordor Intelligence

The diabetic foot ulcer treatment market size is expected to grow from USD 10.82 billion in 2025 to USD 11.43 billion in 2026 and is forecast to reach USD 15.01 billion by 2031 at 5.61% CAGR over 2026-2031. Rising global diabetes prevalence, wider reimbursement for advanced therapies, and steady innovation in negative-pressure wound therapy (NPWT) underpin this outlook. Momentum is particularly strong in emerging economies where improving hospital infrastructure and telehealth platforms broaden access to specialist care. Smart bioactive dressings that modulate pH and glucose levels, maturing 3-D bioprinted skin substitutes, and early regulatory clarity for cellular therapies further enhance the competitive setting. Simultaneously, policy actions such as the CY 2025 Medicare Physician Fee Schedule widen coverage for caregiver training and tele-wound monitoring, adding new revenue streams for device and biologic suppliers.

Key Report Takeaways

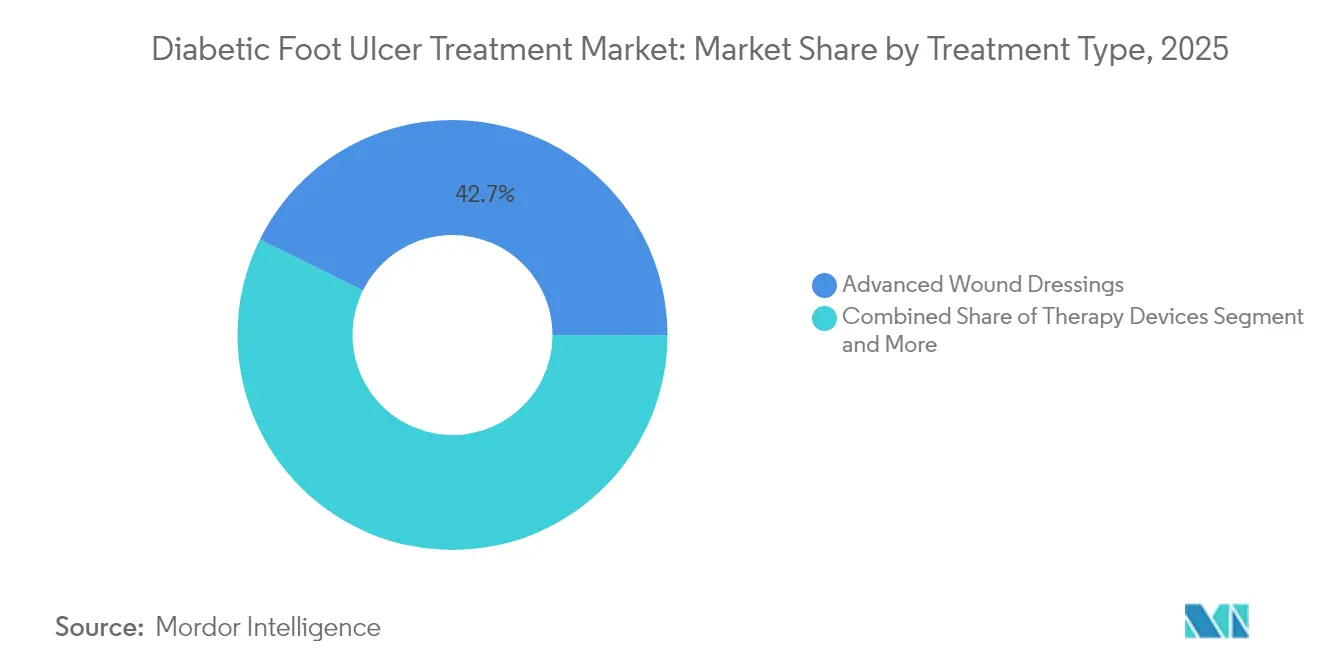

- By treatment type, advanced wound dressings led with a 42.68% revenue share in 2025, while therapy devices are forecast to grow at a 11.74% CAGR to 2031.

- By ulcer type, neuropathic ulcers held 45.10% of diabetic foot ulcer treatment market share in 2025; neuro-ischemic ulcers are projected to advance at a 9.06% CAGR through 2031.

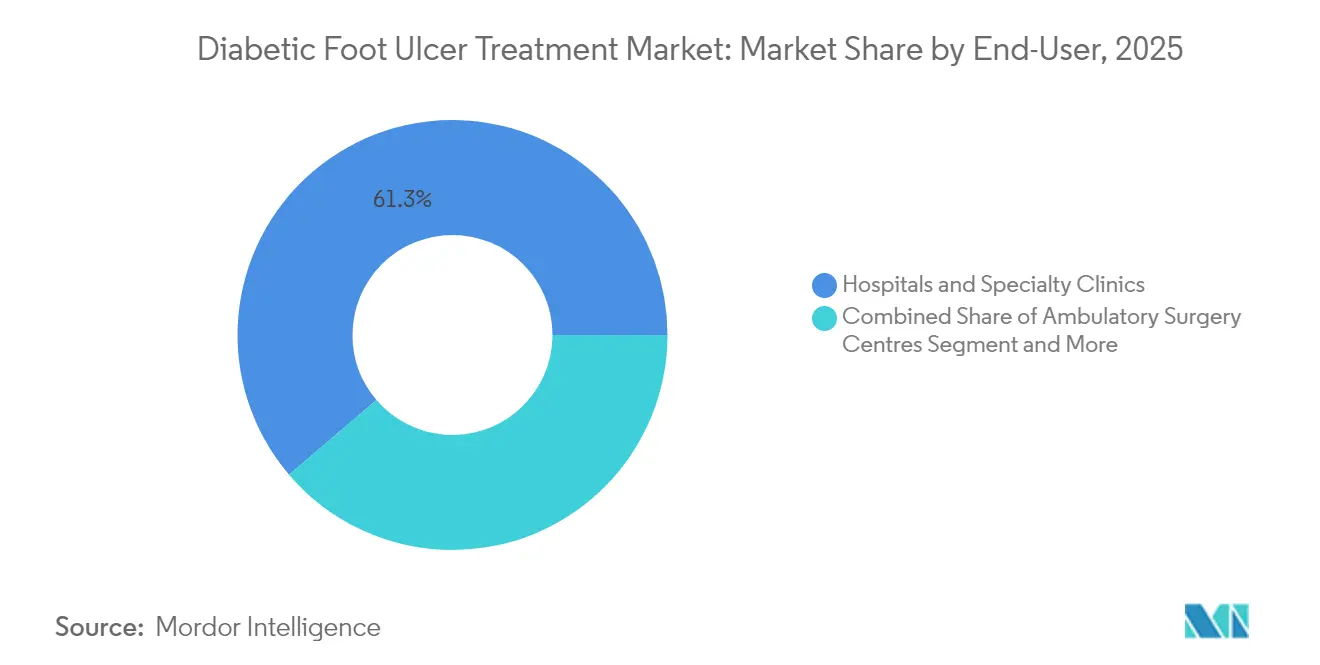

- By end-user, hospitals and specialty clinics commanded 61.25% share of the diabetic foot ulcer treatment market size in 2025, whereas home-care settings show the fastest expansion at 10.08% CAGR.

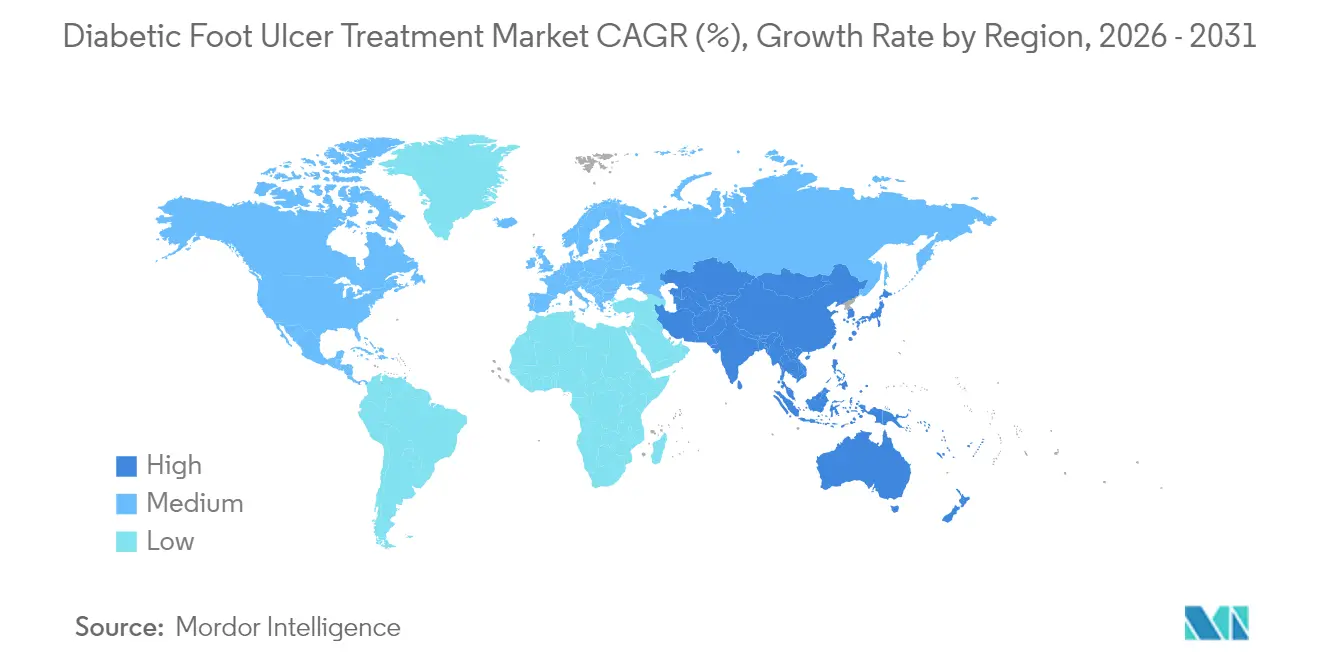

- By geography, North America accounted for 38.35% revenue share in 2025, but Asia-Pacific is expected to register a 9.41% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diabetic Foot Ulcer Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Diabetes & Obesity | +1.8% | Global, with highest impact in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Growing Adoption Of Advanced Wound Dressings and NPWT | +1.2% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| Government Reimbursement Programmes For Chronic Wounds | +0.9% | North America, EU, with gradual APAC adoption | Medium term (2-4 years) |

| 3-D Bioprinted Skin Substitutes Pipeline Maturation | +0.7% | North America & EU core markets | Long term (≥ 4 years) |

| Stem-Cell & Exosome-Based Topical Formulations | +0.5% | Global, with early clinical adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Obesity

Escalating diabetes cases add the largest absolute patient pool to the diabetic foot ulcer treatment market[1]Zhou Yu-Chang, “The National and Provincial Prevalence and Non-Fatal Burdens of Diabetes in China,” Military Medical Research, biomedcentral.com. Roughly 15–25% of adults with diabetes develop foot ulcers in their lifetime, making ulcer management a critical component of chronic-disease care. Unmet need is highest in low- and middle-income economies where 59% of diabetics remain untreated, prompting health ministries to subsidize advanced dressings and NPWT kits. Obesity intensifies wound-healing delays via systemic inflammation, pushing providers toward bioactive products that improve oxygenation. Asia-Pacific’s urban diet transitions and sedentary lifestyles fuel the fastest incremental growth in new ulcer cases through 2030, anchoring long-term demand.

Growing Adoption of Advanced Wound Dressings and NPWT

Meta-analyses confirm that NPWT shortens closure time in diabetic ulcers from a historical 29.8 days to roughly 15 days and improves infection-resolution rates from 68% to 89%. Next-generation systems such as RENASYS EDGE combine mobility-focused design with real-time pressure feedback, making them attractive for outpatient and home-care use. Smart bioactive dressings, which release antimicrobials in response to local pH or glucose changes, align with stewardship rules that aim to curb blanket antibiotic exposure. Clinical evidence shows a 61% reduction in nursing application time and 41% cost savings when next-generation NPWT kits replace older multi-component sets, reinforcing hospital ROI.

Government Reimbursement Programmes for Chronic Wounds

Medicare’s 2025 rule increased covered skin-substitute applications per episode to eight and extended treatment windows to 16 weeks, lifting utilization ceilings for high-value biologics[2]Centers for Medicare & Medicaid Services, “Skin Substitute Grafts/Cellular and Tissue-Based Products,” cms.gov. Similar reforms under NICE’s late-stage assessment of antimicrobial dressings will shape EU payer policies in 2025. Coverage now hinges on peer-reviewed evidence rather than pure regulatory approval, favoring firms with robust clinical portfolios. Still, only 15 of 200 cellular products presently meet Medicare evidence thresholds, tempering near-term uptake for emerging entrants.

3-D Bioprinted Skin Substitutes Pipeline Maturation

Clinical programs moved from preclinical phases into early human trials during 2024–2025, with CUTISS reporting sustained one-year closure outcomes for denovoSkin in complex lesions[3]CUTISS, “Positive One-Year Follow-Up Data from Phase 2 Trial of denovoSkin,” cutiss.swiss. Bioprinting addresses ischemia via pre-vascularized constructs and supports patient-specific graft geometry. Declining bioink costs, scalable printers, and refined FDA frameworks speed commercial feasibility. First-generation constructs combine growth factors with antimicrobial peptides, demonstrating quicker epithelialization and fewer infections than traditional grafts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Therapies & Patchy Coverage | -1.4% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Shortage Of Trained Wound-Care Specialists | -0.8% | Global, particularly acute in rural and underserved areas | Long term (≥ 4 years) |

| Antibiotic-Stewardship Limits On Antimicrobial Dressings | -0.6% | North America & EU primarily, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Therapies & Patchy Coverage

Hospitalization accounts for 88% of total treatment expenditure, with multicenter data placing per-patient costs near EUR 2.06 million (USD 2.37 million) for large cohorts. Out-of-pocket payments remain substantial in markets such as India, undermining adherence to optimal protocols. Medicare’s evidence-based approach further narrows access to only a fraction of available skin-substitute products, prolonging standard-care dependence and elevating amputation risk. Cost-utility analyses flag heterogenous value profiles: platelet-rich plasma shows cost-effectiveness superiority, while other cell-based options fail to meet willingness-to-pay thresholds.

Shortage of Trained Wound-Care Specialists

Certification pipelines cannot match demand as ulcer incidence climbs. Programs such as the WOCN Wound Treatment Associate course and the American Physical Therapy Association specialty pathway broaden skill sets but graduate limited cohorts each year. In Pacific Island states, multidisciplinary diabetic-foot teams are rare, forcing general practitioners to manage complex ulcers without podiatry or vascular support. Workforce gaps heighten recurrence rates, extend hospital stay lengths, and delay adoption of advanced modalities that require specialized application procedures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Bioactives Extend Efficacy Beyond Traditional Dressings

Advanced dressings held 42.68% of diabetic foot ulcer treatment market share in 2025, owing to clinical familiarity, broad-spectrum applicability, and the strong performance of foam platforms such as ALLEVYN LIFE that remain effective 1.92 times longer than gauze. Therapy devices register the fastest 11.74% CAGR as compact NPWT pumps and oxygen-diffusion patches prove compatible with home-care workflows. Regulatory scrutiny intensifies for antimicrobial coatings after the FDA proposed reclassifying certain products into higher risk classes.

Biologics and skin substitutes generate the highest revenue per case; Organogenesis advanced-wound sales rose 27% to USD 118.6 million in Q4 2024. Growth-factor gels and stem-cell suspensions post 86.41% success in Wagner II lesions, but heterogeneity across cell sources complicates broad reimbursement. Breakthrough therapy status for SkinTE, which achieved 70% closure versus 34% for standard care, signals regulatory willingness to fast-track regenerative innovations.

By Ulcer Type: Neuro-Ischemic Complexity Commands Premium Protocols

Neuropathic ulcers accounted for 45.10% of the diabetic foot ulcer treatment market in 2025, reflecting peripheral neuropathy prevalence in long-standing diabetes. These typically painless lesions respond well to off-loading devices, including pressure-alternating insoles that lowered incident ulceration risk in pilot studies. Ischemic lesions, though numerically smaller, incur greater per-patient costs due to revascularization needs.

Neuro-ischemic ulcers are set to grow at 9.06% CAGR, driven by improved diagnostics such as duplex ultrasonography that reveal mixed pathophysiology. Transcutaneous CO2 therapy achieved 67.5% healing in stubborn cases and lowered recurrence relative to conventional care. Treatment algorithms often require two-phase regimens, starting with angiogenesis-promoting biologics followed by autologous grafting, extending therapy cycles but raising reimbursement potential.

By End-User: Home-Care Modalities Propel Market Decentralization

Hospitals and specialty clinics captured 61.25% of the diabetic foot ulcer treatment market size in 2025 because multidisciplinary coordination, imaging, and surgical suites remain essential for severe Wagner III-IV ulcers. Local Coverage Determinations create clearer billing pathways for facility-based skin-substitute procedures, cementing institutional dominance.

Home-care settings will expand at 10.08% CAGR as portable NPWT systems like the V.A.C. Peel and Place Dressing achieve 7-day wear time and 61% application-time savings, enhancing caregiver efficiency. Medicare’s new caregiver-training codes encourage remote supervision, while tele-wound apps transmit images for clinician review, driving decentralization. Ambulatory surgery centers and long-term care facilities occupy niche roles, handling debridement and chronic post-acute care, respectively.

Geography Analysis

North America retained leadership with 38.35% revenue share in 2025. Extensive Medicare and private-payer coverage, early FDA breakthrough designations, and military contracts such as the USD 75 million Department of Defense award to Smith+Nephew prove the region’s high purchasing power. The United States treats roughly 8.2 million chronic-wound patients annually, translating into a USD 33 billion burden that keeps advanced therapies in demand.

Asia-Pacific is forecast to rise at a 9.41% CAGR through 2031, propelled by China’s 233 million diabetics and rapid telehealth adoption. Integrated digital-health pilots in Tianjin cut post-prandial glucose by 3.4% and improved adherence, indirectly reducing ulcer incidence. Yet reimbursement disparities persist; many provincial schemes cap the number of NPWT dressings reimbursed per episode, steering clinicians toward lower-cost standard care for modest lesions.

Europe shows steady expansion under strict health-technology-assessment paradigms. NICE’s late-stage review of topical antimicrobials will influence 2025 procurement and could shift formulary choices toward evidence-backed products. Middle East and Africa record rising diabetes rates but limited specialized staff, fostering opportunities for mobile wound-care hubs. South America remains an intermediate market; Brazil’s public system funds basic dressings yet leans on private insurers for biologics, compelling manufacturers to craft tiered pricing.

Competitive Landscape

The diabetic foot ulcer treatment market is moderately fragmented yet tightening as large firms integrate vertically. Smith+Nephew’s acquisition pipeline pairs dressings, NPWT hardware, and cellular scaffolds, letting hospitals source complete protocols from a single vendor. Organogenesis leverages its Dermagraft and Apligraf portfolios to report a 27% sales jump year-over-year, validating regenerative-medicine demand. Solventum focuses on workflow simplification, cutting procedure time and cost with its extended-wear NPWT kit.

White-space opportunities reside in home-based service models. Start-ups offering AI-guided wound-analysis apps link clinicians to in-home caregivers, boosting therapy adherence. Disruptors pushing exosome topical gels or 3-D bioprinted autografts court premium price points but navigate evidence-threshold hurdles. Patent activity clusters around antimicrobial peptides and sensor-enabled dressings that monitor pH, temperature, and glucose, signaling future differentiation vectors. Firms with clear payer-evidence narratives and digital-platform partnerships are best placed to secure formulary wins.

Diabetic Foot Ulcer Treatment Industry Leaders

Solventum Corporation

Smith+Nephew

Coloplast

Convatec

Molnlycke Health Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smith+Nephew secured a USD 75 million Department of Defense contract for advanced wound therapy systems, expanding its footprint beyond civilian healthcare.

- February 2025: FDA granted breakthrough-therapy designation to SkinTE for Wagner grade 1 ulcers after Phase 2 trials showed 70% closure versus 34% in controls.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the diabetic foot ulcer (DFU) treatment market as the global sales value of advanced wound dressings, therapy devices such as negative-pressure and oxygen systems, biologic skin substitutes, topical agents, and adjunct off-loading products that are used to heal chronic ulcers arising in people with type 1 or type 2 diabetes.

Scope exclusion: cosmetic foot care, over-the-counter emollients, and generic systemic antibiotics not billed under a DFU indication are outside this analysis.

Segmentation Overview

- By Treatment Type

- Advanced Wound Dressings

- Foam Dressings

- Hydrocolloid Dressings

- Alginate Dressings

- Hydrogel Dressings

- Film Dressings

- Antimicrobial/Active Dressings

- Therapy Devices

- Negative-Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Therapy

- Electrical / Ultrasound Stimulation

- Light & Laser Therapy

- Biologics & Skin Substitutes

- Growth-Factor Therapies

- Tissue-Engineered Skin & Grafts

- Stem-cell & Acellular Therapies

- Others (Debridement, Dressings Fixation, etc.)

- Advanced Wound Dressings

- By Ulcer Type

- Neuropathic Ulcers

- Ischemic Ulcers

- Neuro-Ischemic Ulcers

- By End-User

- Hospitals & Specialty Clinics

- Ambulatory Surgery Centres

- Home-Care Settings

- Long-Term Care Facilities

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We conducted structured interviews with wound-care nurses, podiatrists, procurement heads, and payors across North America, Europe, and Asia-Pacific. Insights on average selling prices, adoption hurdles, and therapy-device utilization helped refine model coefficients and stress-test secondary findings.

Desk Research

We start by mapping prevalence, incidence, amputation rates, and average healing times using open datasets from bodies such as the International Diabetes Federation, the World Health Organization, and national health ministries. Trade associations like the European Wound Management Association and peer-reviewed journals (e.g., Diabetes Care) provide wound-healing outcomes, while import-export logs accessed through Volza clarify cross-border device flows. Our analysts complement these with company 10-Ks, investor decks, and clinical-trial registries, then validate cost benchmarks and product mix trends through D&B Hoovers and Dow Jones Factiva snapshots. The sources cited above illustrate the range; many additional publications inform data extraction and validation.

Market-Sizing & Forecasting

Our model blends top-down and bottom-up logic. Global diabetic population pools are intersected with DFU prevalence, treated-case ratios, and average spend per treated ulcer to create a demand curve, which is then cross-checked with sampled supplier revenues and channel checks for sanity. Key variables include diabetes incidence, biologic graft penetration, therapy-device installed base, reimbursement tariff shifts, seasonal wound-clinic volumes, and currency movements. A multivariate regression with lagged macro indicators forecasts each driver, while ARIMA smooths short-term shocks before results are reconciled across geographies.

Data Validation & Update Cycle

We run variance screens against hospital procurement statistics and customs receipts, escalate anomalies for senior review, and rerun the model whenever tariff, clinical-guideline, or currency shifts exceed predefined thresholds. Reports refresh annually, with interim flashes for material events, so clients receive the newest calibrated view.

Why Mordor's Diabetic Foot Ulcer Treatment Market Baseline Earns Trust

Our team acknowledges that published DFU figures vary because providers pick different product baskets, patient cohorts, and forecast cadences.

Mordor analysts find the largest gaps stem from whether biologic grafts and capital-intensive oxygen systems are counted, how aggressively price erosion is assumed, and whether regional currency conversions are frozen at early-year rates. Our discipline in aligning scope with real clinical practice and revisiting inputs each year drives the difference.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.82 billion (2025) | Mordor Intelligence | - |

| USD 8.83 billion (2024) | Global Consultancy A | Excludes therapy devices, applies single uniform ASP, older base year |

| USD 5.47 billion (2024) | Industry Journal B | Focuses on dressings only, limited primary validation, static currency basis |

We believe these contrasts show how Mordor's carefully scoped variables, yearly refresh, and transparent assumptions deliver a balanced, repeatable baseline clients can rely on for confident decision-making.

Key Questions Answered in the Report

What is the current size of the diabetic foot ulcer treatment market?

The market generated USD 11.43 billion in 2026 and is projected to reach USD 15.01 billion by 2031, reflecting a 5.61% CAGR.

Which segment is growing the fastest?

Therapy devices, particularly negative-pressure wound therapy systems, are expected to expand at a 11.74% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

China’s large diabetic population, coupled with expanding digital-health platforms and improving reimbursement frameworks, drives a 9.41% regional CAGR.

How do reimbursement policies influence adoption of advanced therapies?

Medicare’s 2025 rule allows up to eight skin-substitute applications over 16 weeks and covers caregiver training, significantly widening access to high-value treatments.

What are the main barriers to treatment expansion?

High therapy costs and a global shortage of trained wound-care specialists limit penetration, especially in emerging economies.

Which emerging technologies could transform care by 2031?

3-D bioprinted skin substitutes, smart bioactive dressings with real-time sensors, and exosome-based topical formulations are the leading innovation fronts.

Page last updated on: