Mouth Ulcer Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.09 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mouth Ulcer Treatment Market Analysis by Mordor Intelligence

mouth ulcer treatment market size in 2026 is estimated at USD 1.75 billion, growing from 2025 value of USD 1.69 billion with 2031 projections showing USD 2.09 billion, growing at 3.61% CAGR over 2026-2031. Moderate expansion reflects a maturing landscape in which well-established corticosteroid and analgesic brands face new competition from AI-guided personalization, herbal actives, and muco-adhesive films. Demand is reinforced by growing autoimmune disease prevalence, wider e-commerce access to over-the-counter (OTC) remedies, and a steady pipeline of delivery-system innovations. Market participants also contend with cost pressure as generic erosion accelerates and subscription-commerce models reset consumer expectations. While premium formulations command higher unit revenues in North America and Western Europe, emerging economies focus on affordable sprays and gels that deliver rapid pain relief and minimal systemic exposure.

Key Report Takeaways

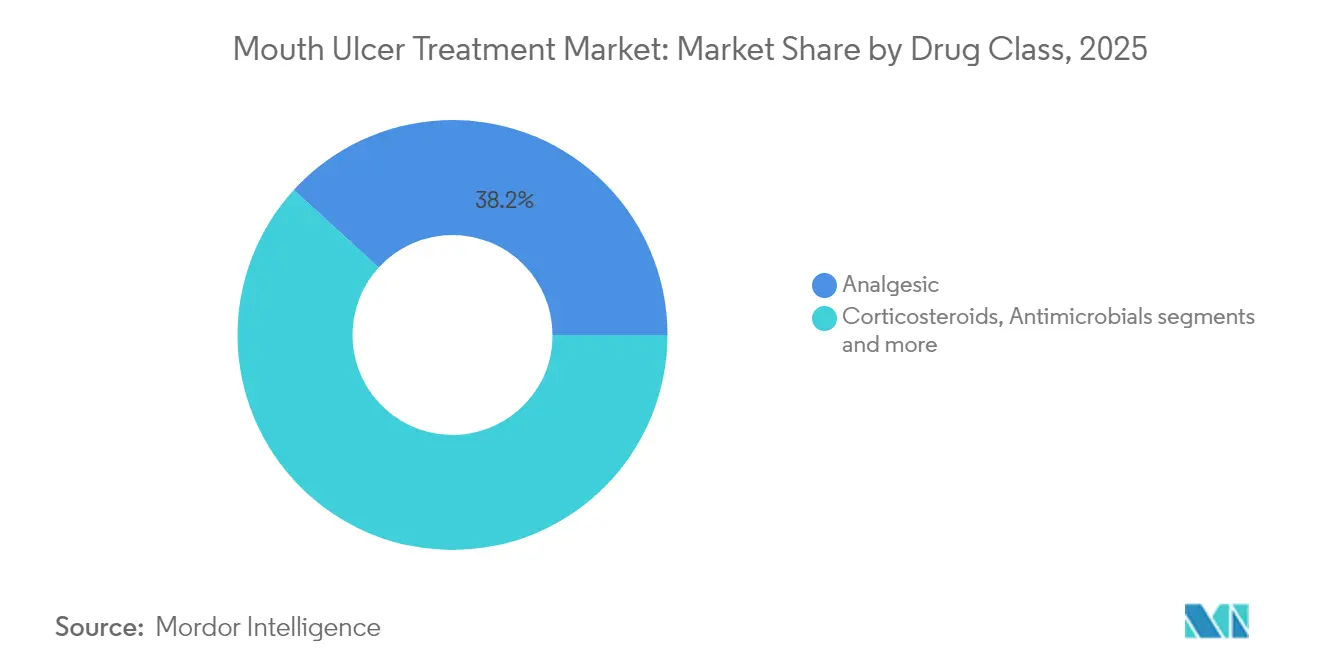

- By drug class, analgesics led with 38.22% of the mouth ulcer treatment market share in 2025, whereas anesthetics post the fastest 4.03% CAGR through 2031.

- By formulation, gels held 40.88% revenue share in 2025; sprays are projected to rise at a 4.44% CAGR to 2031.

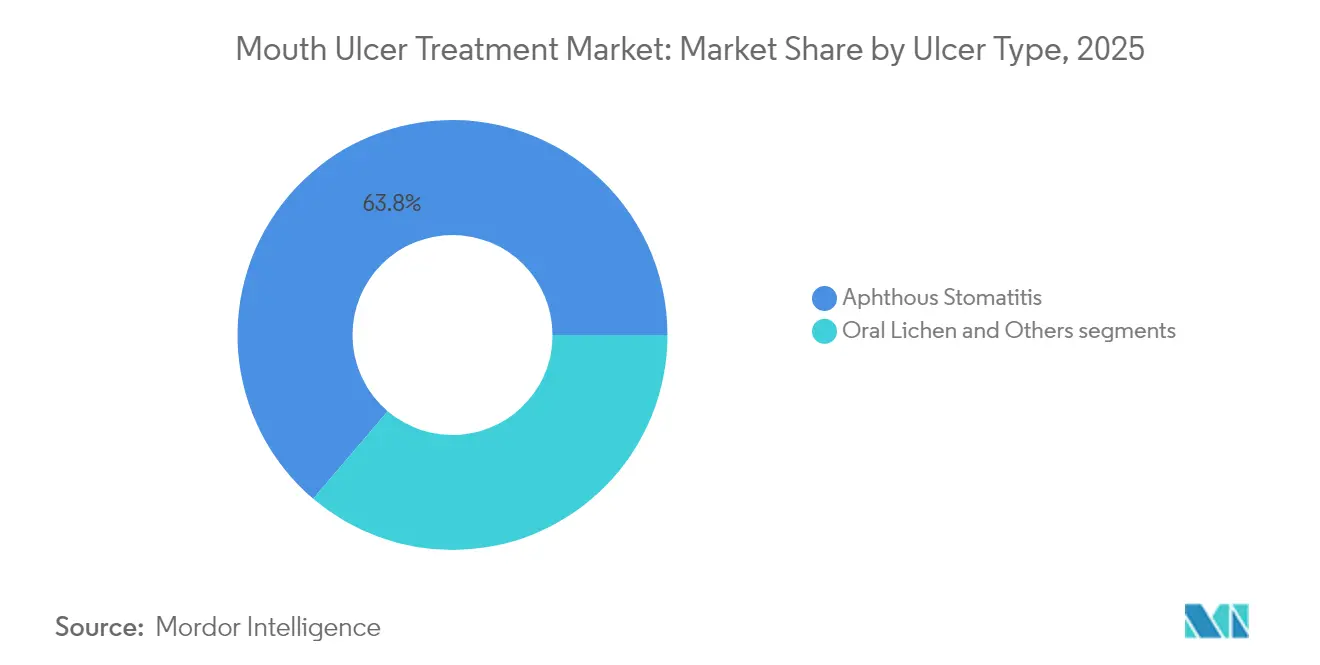

- By ulcer type, aphthous stomatitis accounted for a 63.78% share of the mouth ulcer treatment market size in 2025, while oral lichen planus records the highest 4.93% CAGR during the same period.

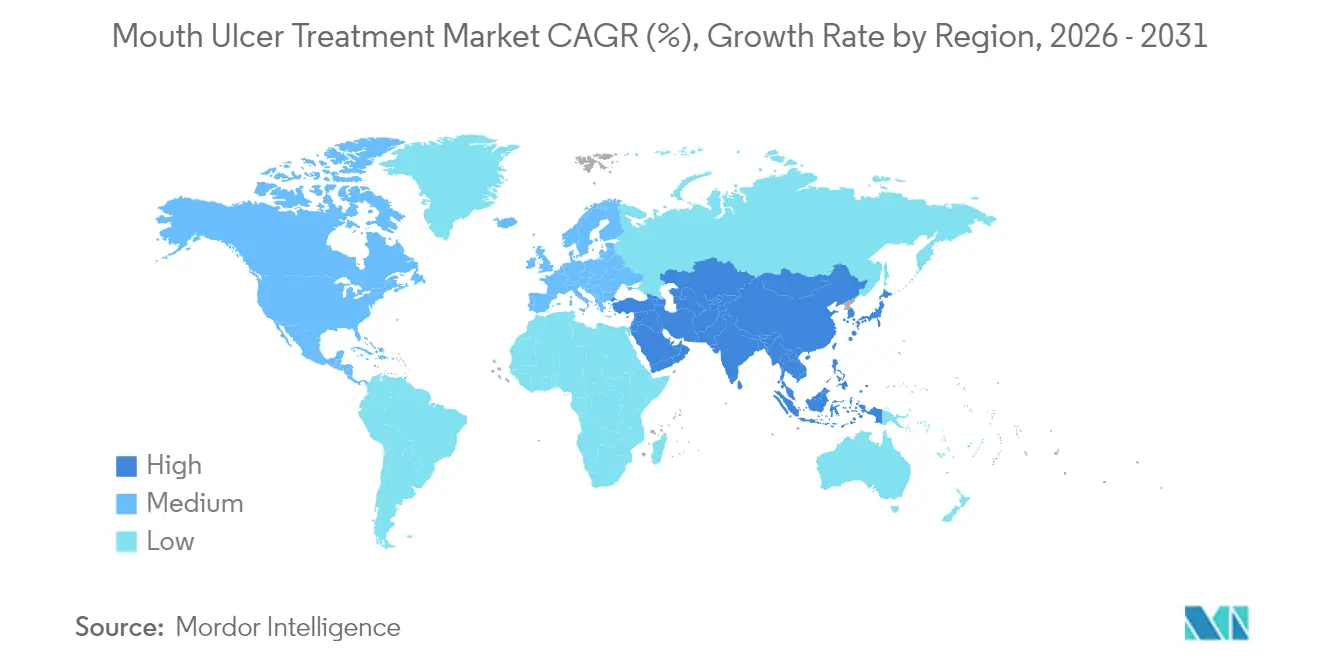

- By geography, North America captured 38.21% of 2025 sales; Asia-Pacific is advancing at a 5.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mouth Ulcer Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in sugar-free & herbal OTC gels | +0.8% | North America, Europe, expanding globally | Medium term (2-4 years) |

| Growing prevalence of autoimmune disorders | +1.2% | Developed markets with aging populations | Long term (≥ 4 years) |

| E-commerce proliferation boosting self-care | +0.9% | APAC and North America | Short term (≤ 2 years) |

| Advances in muco-adhesive drug-delivery films | +0.7% | North America, EU, APAC | Medium term (2-4 years) |

| AI-driven personalized oral-care regimens | +0.5% | North America and selected APAC markets | Long term (≥ 4 years) |

| Microbiome-targeted therapeutics pipeline | +0.4% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Sugar-Free & Herbal OTC Gels

Consumers increasingly choose plant-derived and sugar-free gels, pushing manufacturers to invest in botanical actives such as eugenol and flavonoids that pair well with modern muco-adhesive bases. Clinical validation supports efficacy, addressing regulatory and prescriber scrutiny. Market leaders differentiate through transparent labeling, clinical dossiers, and convenient packaging aligned with tele-pharmacy growth.

Growing Prevalence of Autoimmune Disorders

Enhanced and aging demographics lift autoimmune disease incidence, increasing oral lichen planus and aphthous ulcer cases. Targeted small-molecule therapies, illustrated by tofacitinib success in erosive lichen planus, shift treatment from broad anti-inflammatory regimens to precision approaches. Cross-portfolio synergies emerge as systemic immunology pipelines adapt topical formulations for oral lesion

E-commerce Proliferation Boosting Self-Medication

Healthcare e-commerce, projected to hit USD 750 billion by 2027, rewires purchase pathways and emphasizes direct-to-consumer education, loyalty programs, and subscription refill models. Digital engagement accelerates adoption of convenient sprays and films, while price transparency intensifies competition.

Advances in Muco-Adhesive Drug-Delivery Films

Next-generation films made from green-tea polyphenols or foam-actuated nano-emulgels increase residence time, reduce dosing frequency, and enhance antimicrobial activity. Intellectual-property filings around polymer matrices and nanocarriers create durable competitive barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTC product commoditization | -0.6% | Price-sensitive emerging markets | Short term (≤ 2 years) |

| Safety concerns over chronic corticosteroid use | -0.4% | Developed regions | Medium term (2-4 years) |

| Regulatory hurdles for novel biologic topicals | -0.3% | North America, EU | Long term (≥ 4 years) |

| Under-diagnosis in low-income regions | -0.2% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OTC Product Commoditization Keeps Prices Low

Patent expiries and biosimilar entry drop average selling prices by nearly 50%, limiting premium scope unless backed by clear clinical or convenience advantages. Manufacturers lengthen life-cycles through reformulations, but retailers use private-label parity to restrain shelf prices.

Safety Concerns Over Long-Term Corticosteroid Use

Meta-analyses link prolonged systemic corticosteroid exposure to gastrointestinal and infectious complications, encouraging prescribers to pivot toward cannabidiol and other non-steroidal actives . Demand shifts create room for safer, plant-based or biologic alternatives, though higher manufacturing costs require supportive reimbursement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Anesthetics Gain Momentum Amid Analgesic Dominance

Analgesics retained 38.22% of the mouth ulcer treatment market in 2025, benefiting from physician familiarity and broad OTC access. The segment’s lead, however, is challenged as anesthetics log a 4.03% CAGR, reflecting patient preference for rapid numbness that supports daily function. Combination nanofiber platforms delivering acyclovir plus clobetasol demonstrate superior lesion resolution, underlining the role of co-formulations in the mouth ulcer treatment market.

In revenue terms, anesthetic expansion translates into a rising contribution to the mouth ulcer treatment market size, propelled by dentistry partnerships and digital triage apps that advise immediate symptomatic relief. Corticosteroid brands remain indispensable for immune-mediated ulcers despite safety debate, while antimicrobial agents occupy niche use against secondary infection.

By Formulation: Sprays Challenge Gel Supremacy

Gels accounted for 40.88% of 2025 sales, leveraging strong muco-adhesion and dosing accuracy. Yet sprays are advancing at a 4.44% CAGR, lifted by non-contact comfort and compatibility with tele-consult refill protocols. The transition is visible in North America where QR-coded spray packs integrate with insurer telehealth dashboards.

The mouth ulcer treatment market size opportunity for sprays climbs as plant-derived oromucosal sprays combine antiseptic and anti-inflammatory claims. Film strips and foams add variety, but gel upgrades—such as sugar-free herbal bases—help incumbents protect share.

By Ulcer Type: Oral Lichen Planus Accelerates

Aphthous stomatitis represented 63.78% of 2025 volume, mirroring high prevalence. Diagnosis and therapeutic innovation now shift attention to oral lichen planus, which grows 4.93% annually. Phase IIa data for LP-310 and targeted kinase inhibitors indicate unmet need and commercial upside in this subset.

As specific biologic pathways become clearer, differentiated labeling and companion diagnostics will define future mouth ulcer treatment market share allocation. Other categories, including radiation-induced mucositis, benefit from muco-adhesive film innovation and oncology supportive-care funding.

Geography Analysis

North America contributed 38.21% of 2025 value through robust insurance coverage, specialist networks, and marketing scale. Retail pharmacies increasingly co-pack AI-guided consultation leaflets, reinforcing premium positioning. The United States posts the highest per-capita spend, while Canada’s reimbursement reforms encourage expanded OTC usage.

Asia-Pacific registers the top 5.44% CAGR through 2031, driven by urbanization, oral health campaigns, and regulatory streamlining in China and India. Beijing’s 2027 reform blueprint promises faster review cycles, likely accelerating innovative spray and film launches. Malaysia’s National Oral Health Strategic Plan further underscores regional policy focus on mouth ulcer prevention and early treatment. Local manufacturing hubs reduce cost, supporting volume penetration.

Europe sustains steady growth as evidence-based guidelines promote clinically proven products. Cross-border e-pharmacy directives foster online share gains, although strict advertising codes cap direct-to-consumer promotional flexibility. Market access hinges on health-technology-assessment outcomes that reward real-world evidence for novel delivery systems.

Competitive Landscape

Competition remains moderate, with large consumer-health corporations and focused biotech innovators sharing space. Colgate-Palmolive leverages OTC brand equity, while Pfizer benefits from systemic immunology expertise that informs topical pipeline extensions. Reckitt’s new OTC manufacturing facility expands supply flexibility, positioning the firm for private-label and brand output in parallel[2]Source: Reckitt, “Reckitt Opens Its Largest OTC Manufacturing Facility,” reckitt.com .

Investment themes center on AI-powered drug discovery and personalization, illustrated by Bristol Myers Squibb’s USD 400 million AI Proteins alliance. Patents covering hydrogel nanocarriers and probiotic combinations create defensible niches. Manufacturers explore partnerships with telehealth firms to embed therapy algorithms into mobile workflows, enhancing stickiness.

Price competition intensifies where generics proliferate, but innovators defend gross margins via novel actives, improved delivery, and digital support platforms. Consolidation talk persists, yet antitrust constraints and diverse pathology segments keep the mouth ulcer treatment market from tipping into high concentration.

Mouth Ulcer Treatment Industry Leaders

3M

Blistex Inc.

Colgate- Palmolive Company

Church & Dwight, Inc.

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA cleared Khindivi hydrocortisone oral solution for pediatric adrenocortical insufficiency, with commercial roll-out slated for Q3 2025

- April 2025: Sun Pharma launched fexuprazan tablets in India after 95% eight-week healing rates in Phase 3 esophagitis trials

- December 2024: Reckitt opened its largest U.S. OTC manufacturing facility to scale oral-care output

Global Mouth Ulcer Treatment Market Report Scope

As per the scope of the report, mouth ulcers are painful sores that can develop in the mucous membrane of the oral cavity and do not allow the person to chew or bite. Some mouth ulcers can be severe and need immediate medical treatment to reduce lesions and pain severity. Mouth ulcers can be prevented by avoiding tissue injury, avoiding food that causes irritation in the mouth, and maintaining oral hygiene. Besides the traditional method, various medications and ointments are used to treat mouth ulcers. The Mouth Ulcer Treatment Market is Segmented by Drug Class (Antimicrobial, Antihistamine, Analgesics, Corticosteroids, and Other Drug Classes), Formulation (Sprays, Mouthwash, Gels, and Other Formulations), Indication (Aphthous Stomatitis, Oral Lichen Planus, and Other Indications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

| Analgesics |

| Corticosteroids |

| Antimicrobials |

| Antihistamines |

| Anesthetics |

| Other Drug Classes |

| Ointments & Creams |

| Gels |

| Mouthwashes & Rinses |

| Sprays |

| Lozenges |

| Other Formulations |

| Aphthous Stomatitis |

| Oral Lichen Planus |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Drug Class | Analgesics | |

| Corticosteroids | ||

| Antimicrobials | ||

| Antihistamines | ||

| Anesthetics | ||

| Other Drug Classes | ||

| By Formulation | Ointments & Creams | |

| Gels | ||

| Mouthwashes & Rinses | ||

| Sprays | ||

| Lozenges | ||

| Other Formulations | ||

| By Ulcer Type | Aphthous Stomatitis | |

| Oral Lichen Planus | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the mouth ulcer treatment market?

The market generated USD 1.75 billion in 2026.

How fast will the mouth ulcer treatment market grow?

It is projected to expand at a 3.61% CAGR to reach USD 2.09 billion by 2031.

Which drug class is growing fastest?

Anesthetics post the highest 4.03% CAGR, reflecting demand for rapid pain relief.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 5.44% CAGR through 2031 on the back of healthcare access expansion.

Page last updated on: