United States Heart Failure POC and LOC Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

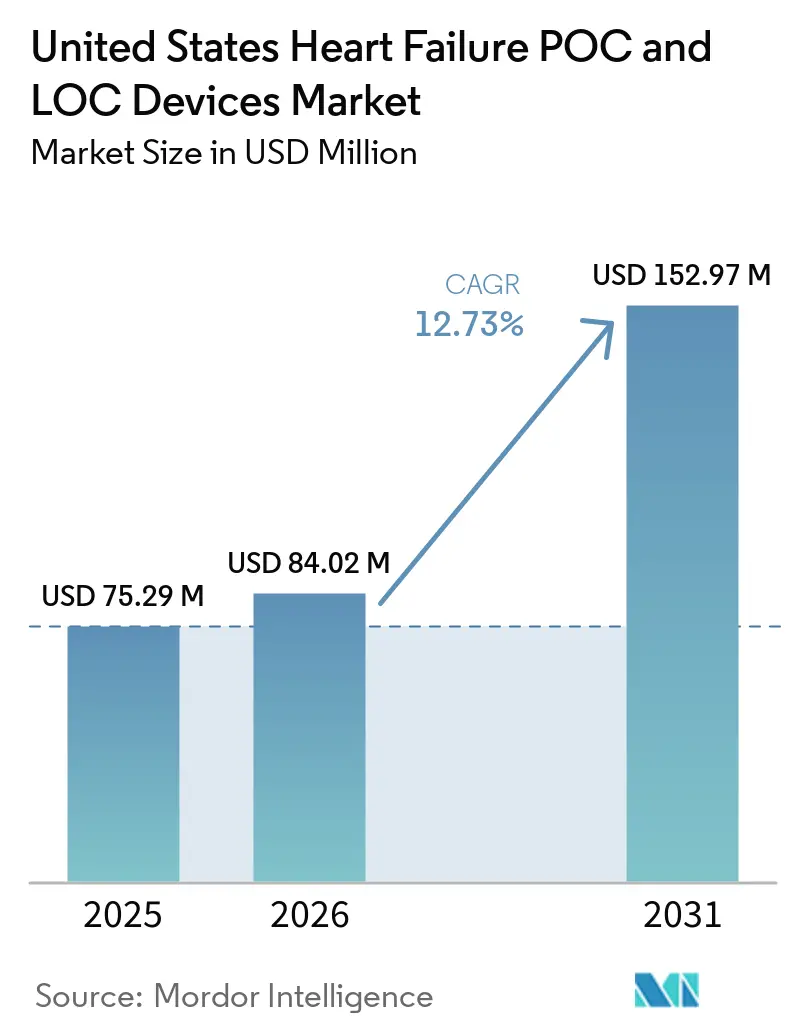

| Base Year Market Size (2025) | USD 75.29 Million |

| Market Size (2026) | USD 84.02 Million |

| Market Size (2031) | USD 152.97 Million |

| Growth Rate (2026 - 2031) | 12.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Heart Failure POC and LOC Devices Market Analysis by Mordor Intelligence

The United States Heart Failure POC And LOC Devices Market size is projected to expand from USD 75.29 million in 2025 and USD 84.02 million in 2026 to USD 152.97 million by 2031, registering a CAGR of 12.73% between 2026 to 2031.

The growth pattern in the heart failure POC and LOC devices market reflects a larger elderly patient pool, rising heart failure burden, and stronger reimbursement support for near-patient natriuretic peptide testing in the United States. It also reflects the steady improvement of cartridge-based microfluidic platforms that now produce fast results at the bedside, in physician offices, and in other decentralized care settings. Demand is also being supported by the delayed diagnosis backlog that followed pandemic-era care disruption, wider CLIA-waived access for BNP assays, and a payment environment that rewards earlier triage and tighter post-discharge follow-up. Competition remains moderate rather than fully fragmented because large vendors still benefit from analyzer, consumable, and software bundles, while newer entrants are gaining ground through lower-cost platforms and cloud-native workflows in settings that were previously less served.

Key Report Takeaways

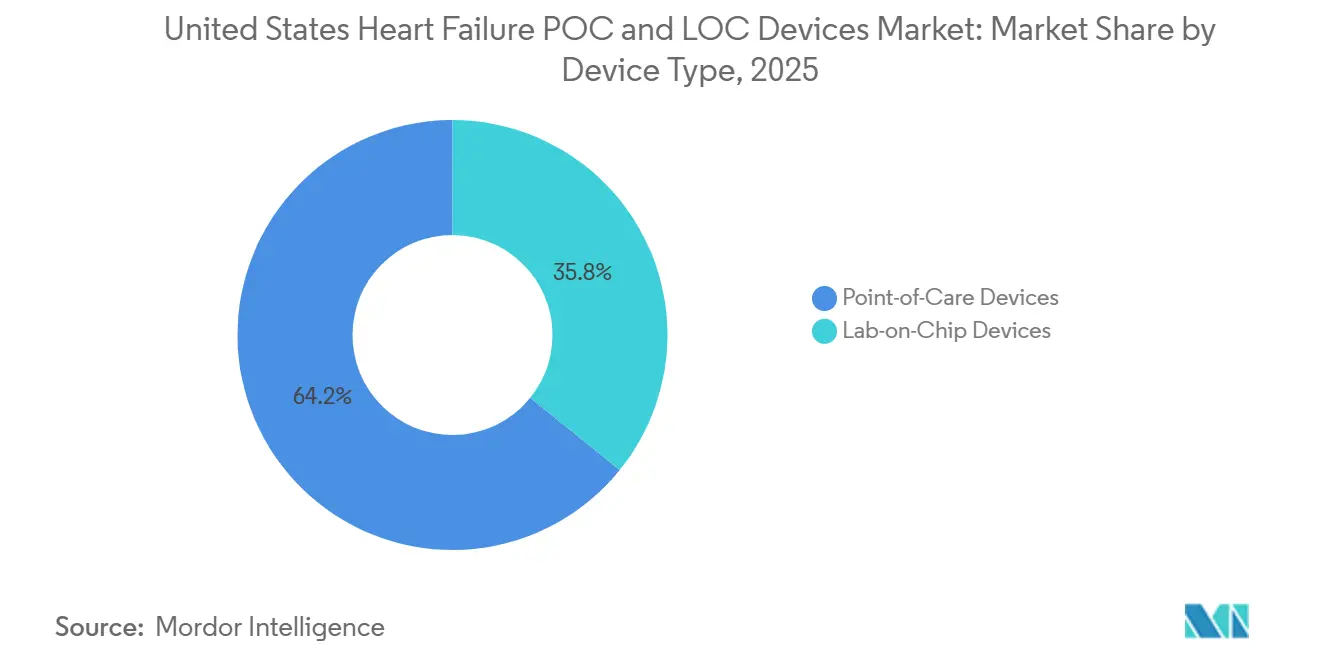

- By device type, point-of-care devices held 64.23% of revenue in 2025, while lab-on-chip devices are projected to expand at a 13.25% CAGR through 2031 in the heart failure POC and LOC devices market.

- By test type, proteomic testing accounted for 51.23% of revenue in 2025, while metabolomic testing is forecast to grow at a 15.97% CAGR through 2031.

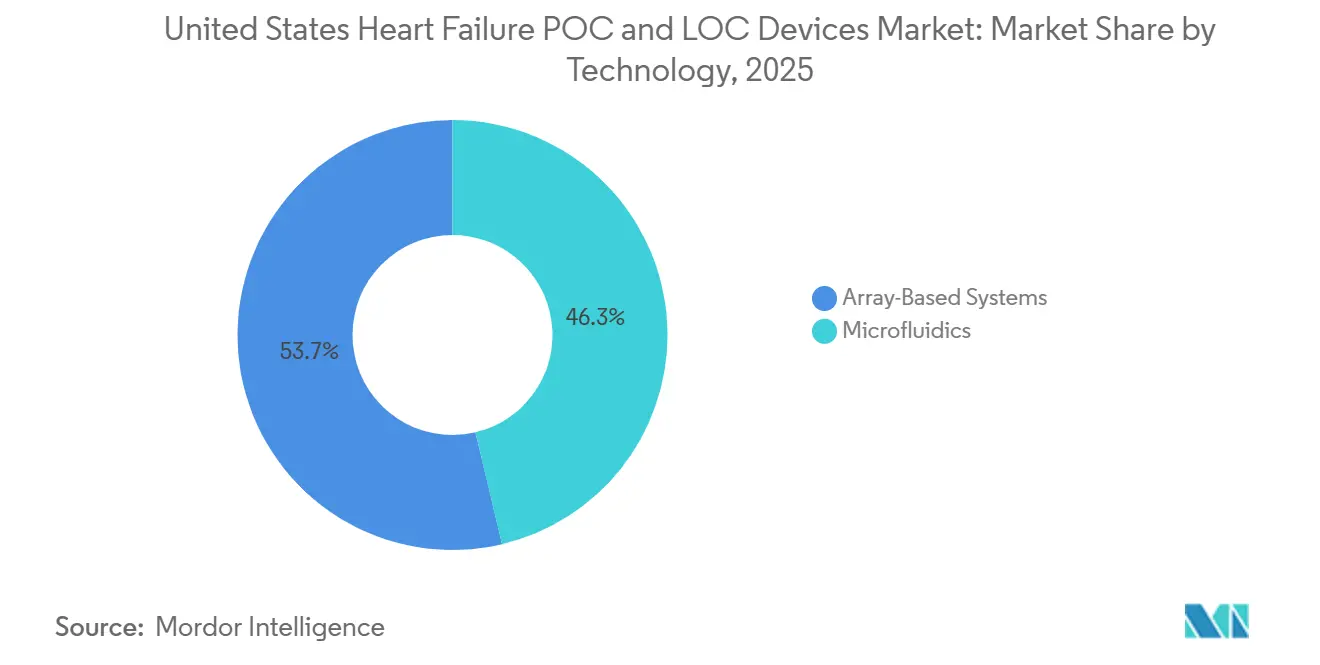

- By technology, microfluidics captured 46.32% of platform revenue in 2025, while array-based systems are expected to advance at a 14.35% CAGR through 2031.

- By biomarker, NT-proBNP and BNP held 58.62% of biomarker revenue in 2025, while multi-biomarker panels are projected to grow at a 14.82% CAGR through 2031.

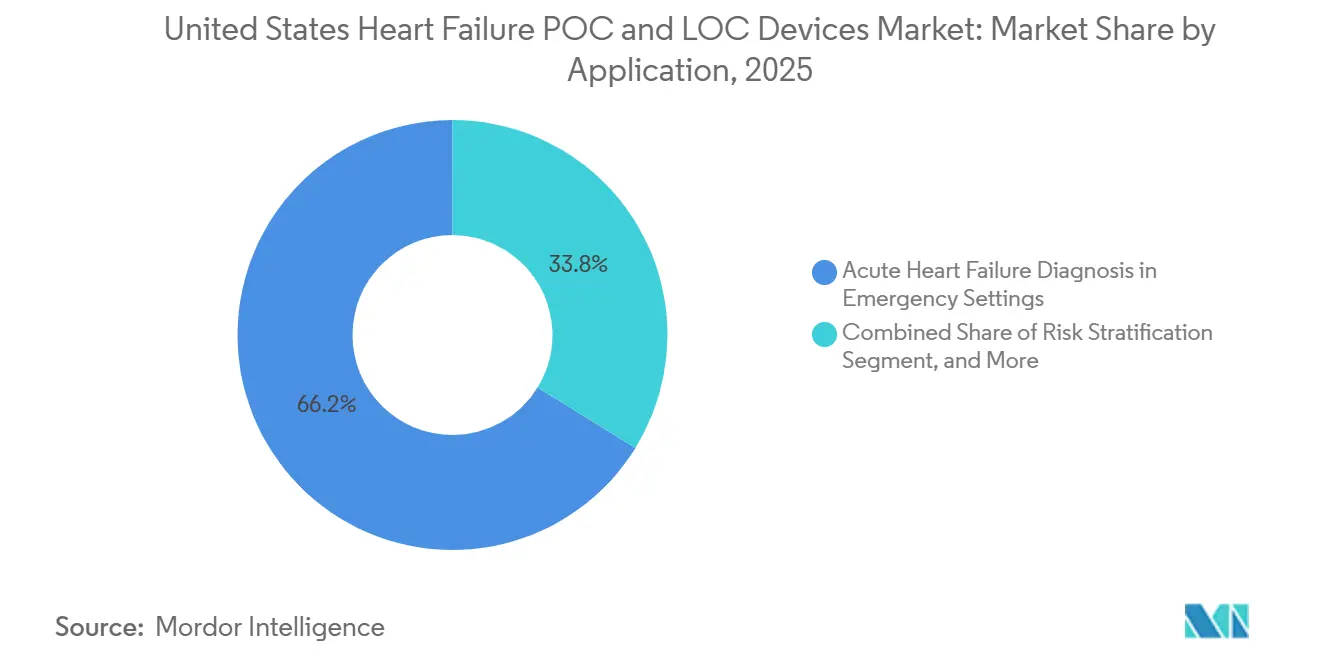

- By application, acute heart failure diagnosis in emergency settings accounted for 66.23% of revenue in 2025, while chronic heart failure monitoring and therapy optimization is forecast to expand at a 13.02% CAGR through 2031.

- By end user, hospitals and clinics held 45.89% of revenue in 2025, while homecare and remote patient monitoring programs are projected to grow at a 13.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Heart Failure POC and LOC Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Medicare Coverage for Near-Patient Natriuretic Peptide Testing | +2.1% | National, concentrated gains in Medicare Advantage-heavy states including Florida, Texas, and California | Short term (≤ 2 years) |

| CLIA-Waived Decentralization of BNP Assays in Physician Offices and Urgent Care | +1.8% | National, early gains in Sun Belt and rural markets with limited laboratory infrastructure | Short term (≤ 2 years) |

| Rising Need to Reduce Emergency Department Length of Stay Through Rapid Triage | +2.3% | National, disproportionate impact in high-ED-volume urban systems in the Northeast and West Coast | Medium term (2-4 years) |

| Adoption of Connected Multi-Marker Panels for Earlier Heart Failure Risk Stratification | +1.9% | National, concentrated in large integrated health systems with EHR interoperability capacity | Medium term (2-4 years) |

| AI-Enabled Interpretation of BNP, NT-proBNP, and Cardiac Biomarker Outputs | +1.5% | National, fastest adoption in academic medical centers and tertiary care networks | Long term (≥ 4 years) |

| Fingerstick-Compatible Microfluidic Platforms Extending Testing Beyond Traditional Labs | +2.0% | National, priority impact in rural and community care settings lacking lab infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Medicare Coverage for Near-Patient Natriuretic Peptide Testing

Medicare’s revised LCD L34410, effective February 15, 2026, combines Part A and Part B coverage for BNP and NT-proBNP into one clearer framework for acute dyspnea evaluation, severity assessment, and risk stratification in emergency and outpatient settings.[1]Centers for Medicare & Medicaid Services, “Article - Response to Comments: B-type Natriuretic Peptide (BNP) Testing (A60382),” CMS Medicare Coverage Database, cms.gov That change matters for the heart failure POC and LOC devices market because it reduces billing ambiguity for providers that operate across hospital and outpatient sites under the same health system structure. The CMS raised reimbursement for near-patient BNP testing to USD 24 per test and removed prior authorization requirements for Medicare Advantage plans, which improves the revenue case for physician offices and urgent care use. The direct beneficiary is the CLIA-waived whole blood BNP format because it avoids plasma preparation and lowers staffing needs at lower-acuity sites, a profile that aligns with the QuidelOrtho Triage BNP Test. This is especially relevant for the large physician office-based in the United States, where clinical demand existed before, but reimbursement clarity had remained inconsistent across settings. The result is a sharper commercial path for decentralized testing sites that need fast cardiac rule-in and rule-out support without a full laboratory buildout.

CLIA-Waived Decentralization of BNP Assays in Physician Offices and Urgent Care

The FDA’s waived test list shows that selected BNP platforms obtained CLIA-waived status, which changed the staffing and deployment economics for natriuretic peptide testing outside traditional laboratories. That development supports the heart failure POC and LOC devices market because it allows testing in physician offices, urgent care centers, and retail-linked care sites that cannot support higher-complexity operations. The practical impact is that primary care physicians can receive BNP results during the visit instead of sending patients into a slower referral pathway before treatment decisions begin. The fingerstick BNP and NT-proBNP workflows in retail and community settings create a channel outside hospital procurement and widen access points for earlier evaluation. A 2026 ICare-FASTER preprint described analytical advances that support very small capillary sample volumes, which is important because small sample requirements make decentralized fingerstick workflows more realistic at scale.[2]Martin Than, “Improving Care by FAster risk-STratification through use of high sensitivity point-of-care troponin in patients presenting with possible acute coronary syndrome in the Emergency department (ICare-FASTER): a stepped-wedge cluster randomized trial,” medRxiv, medrxiv.org The waiver framework, therefore, does more than simplify compliance; it also shapes product design priorities by rewarding devices that keep performance high while making the operating process simpler.

Rising Need to Reduce Emergency Department Length of Stay Through Rapid Triage

Emergency departments in the United States continue to manage high acute heart failure volume while facing pressure to reduce wait times, shorten observation periods, and avoid unnecessary admissions in a payment environment tied to outcomes. The ICare-FASTER stepped-wedge cluster randomized trial posted in April 2026 showed that use of the Siemens Atellica VTLi high-sensitivity troponin I point-of-care pathway reduced emergency department length of stay by 13%, or 47 minutes, across 59,980 presentations without worsening 30-day safety outcomes. That finding is important because the gain came from faster turnaround rather than from looser protocols, which suggests that many sites still have room to improve throughput through faster biomarker access alone. Kaiser Permanente Northern California added another practical example in January 2025 when it deployed the STRIDE-HF risk tool across 21 emergency departments and identified 11.4% of acute heart failure patients as very low risk.[3]Kaiser Permanente Division of Research, “Risk Tool Improves Emergency Department Care for Patients With Heart Failure,” Kaiser Permanente, divisionofresearch.kaiserpermanente.org In the heart failure POC and LOC devices market, that kind of structured triage raises the value of analyzers that can deliver rapid data directly into decision workflows instead of only producing stand-alone results. The link between readmission penalties and heart failure outcomes also gives hospital leadership a direct financial reason to invest in triage tools that improve discharge decisions earlier in the care episode.

Adoption of Connected Multi-Marker Panels for Earlier Heart Failure Risk Stratification

Single-marker testing remains important, but it does not fully address the biological diversity seen across heart failure presentations, especially in HFpEF, where one simple confirmatory marker has remained elusive. Multi-marker panels that combine NT-proBNP with soluble ST2, galectin-3, troponin, or metabolic signals offer a broader view of fibrosis, inflammation, injury, and volume overload in one workflow. Abbott received 2026 clearance for an i-STAT Alinity multi-marker cardiac panel that brings NT-proBNP, high-sensitivity troponin I, and soluble ST2 into one bedside cartridge, which highlights the commercial move toward wider panel content in the heart failure POC and LOC devices market. A 2025 proteomic biomarker study also found that blood-based markers improved differentiation between HFpEF and HFrEF when used alongside BNP, which supports a more subtype-aware diagnostic approach. Scientific Reports and the International Journal of Molecular Sciences each added support for metabolomic signatures that can help classify heart failure phenotypes more precisely than natriuretic peptides alone. Adoption is moving faster in large integrated systems because connected outputs fit better with EHR-based care pathways and with contracting models that place value on earlier risk identification rather than on isolated test volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Moderate-Complexity Classification Limits Broad Decentralized Deployment | -1.3% | National, amplified in rural and community settings lacking lab infrastructure | Short term (≤ 2 years) |

| Reimbursement Friction for Multi-Test Cartridges and Advanced Panel Bundles | -1.0% | National, most acute in Medicare and Medicaid-dominant payer markets | Medium term (2-4 years) |

| High Clinical Validation Burden for Novel LOC Biomarker Combinations | -0.8% | National, especially affects academic medical center adoption timelines | Long term (≥ 4 years) |

| Installed Base Resistance From Central Laboratory Workflow Preferences | -1.1% | National, most pronounced in large academic and community hospital systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Moderate-Complexity Classification Limits Broad Decentralized Deployment

CLIA waiver has helped some BNP formats, but many of the strongest-performing NT-proBNP assays still remain outside waived status and require higher oversight before they can be used in decentralized care settings. This creates a practical mismatch in the heart failure POC and LOC devices market because the sites with the biggest access gaps are often the same sites that lack moderate-complexity infrastructure. 75% of U.S. urgent care centers do not have the certification framework needed to run these assays without additional staffing and compliance investment, which directly limits adoption beyond hospital-linked networks. That barrier is more manageable for hospital-owned urgent care sites because they already operate within existing quality systems and oversight arrangements. Independent chains and community providers face a harder choice because they must either upgrade certification or accept lower-performance testing options. The result is a slower move toward broad decentralization than the analytical performance of the devices alone would suggest.

Reimbursement Friction for Multi-Test Cartridges and Advanced Panel Bundles

Multi-biomarker cartridges fit clinical logic well, but reimbursement still tends to follow single-analyte coding, which makes panel adoption slower than the underlying medical need would imply. Medicare guidance for BNP testing does not automatically extend to bundled panels, so providers often need separate code submissions and medical necessity documentation for each additional marker. The general frequency ceiling of 4 BNP tests per patient per year under current coverage logic does not align well with the monitoring cadence often needed in chronic management. Because many private payers use CMS logic as a benchmark, that friction carries into a wide share of the payer mix, not just into fee-for-service Medicare. Manufacturers, therefore, need a stronger payer strategy, including outcomes evidence and health technology assessment support, before panel revenue can scale in a consistent way. This issue does not block growth, but it slows the shift from single-marker testing toward higher-value bundled cartridges in routine use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Lab-on-Chip Accelerates as POC Platforms Defend Installed Base

Point-of-Care devices held 64.23% of the heart failure POC and LOC devices market share in 2025, which reflects their long-established role in emergency departments and acute care workflows, where BNP and troponin testing already fit validated reimbursement and protocol structures. These systems remain difficult to displace because hospitals have already invested in analyzers, reagent agreements, staff training, and EHR connectivity that are tied to routine cardiac testing. Siemens, QuidelOrtho, and Radiometer benefit from this installed base effect because device replacement requires operational change rather than just a product swap. In practice, the point-of-care segment still dominates higher-acuity settings where speed, familiarity, and audit-ready workflows matter more than full miniaturization. The device type mix, therefore, reflects both clinical performance and the cost of changing existing hospital operations within the heart failure POC and LOC devices industry.

Lab-on-Chip devices are projected to expand at a 13.25% CAGR through 2031, which makes them the fastest-growing device class in the heart failure POC and LOC devices market. Their main advantage is not immediate displacement of hospital analyzers, but entry into physician offices, urgent care, discharge follow-up, and home-linked monitoring pathways where legacy systems have a weaker reach. Nature’s 2026 study on dual-mode multiplexed optical sensing showed how miniaturized platforms are moving toward very high analytical sensitivity in compact formats, which supports the credibility of LOC expansion. Abbott’s i-STAT Alinity cartridge and Siemens’ Atellica VTLi show how commercial products are already closing the gap between compact design and clinically acceptable turnaround time. As performance parity improves, LOC devices are more likely to win incremental demand in greenfield settings first and then compete more directly in emergency care later in the forecast period.

By Test Type: Proteomics Anchors Revenue as Metabolomics Opens a New Diagnostic Frontier

Proteomic testing accounted for 51.23% of test-type revenue in 2025, which made it the largest test segment in the heart failure POC and LOC devices market size because BNP, NT-proBNP, and troponin assays already have clinical precedent, reimbursement pathways, and broad analyzer compatibility. This segment remains the revenue anchor because hospitals, payers, and accreditation bodies are more comfortable with assays that already carry established thresholds and long clinical use histories. FDA-cleared proteomic assays are especially valuable in clinical operations because they support defensible documentation during audit, utilization review, and treatment escalation decisions. The depth of outcome evidence behind natriuretic peptides also keeps this segment central even as new test formats arrive. For these reasons, proteomics is likely to remain the commercial core of the heart failure POC and LOC devices industry through the medium term.

Metabolomic testing is projected to grow at a 15.97% CAGR through 2031, making it the fastest-growing test category in the heart failure POC and LOC devices market. Scientific Reports in 2025 showed that plasma metabolic signatures can differentiate heart failure phenotypes with high model accuracy, which gives this segment a clearer clinical role than it had only a few years ago. The International Journal of Molecular Sciences also linked ADMA, TMAO, and acylcarnitines to HFpEF in hypertensive patients, which is especially relevant because HFpEF has lacked a simple confirmatory point-of-care marker. That makes metabolomics valuable not only for diagnosis, but also for subtype refinement and therapy response tracking, where conventional natriuretic peptides may not be enough on their own. Genomic testing remains more limited and is still largely concentrated in academic settings, so its commercial contribution is expected to stay small relative to proteomic and metabolomic formats through 2031.

By Technology: Microfluidics Leads While Array-Based Systems Close the Performance Gap

Microfluidics captured 46.32% of platform revenue in 2025, which gave it the largest technology position in the heart failure POC and LOC devices market size across both POC and LOC device formats. The technology is widely favored because it handles small sample volumes well, supports whole blood workflows, and can deliver near-laboratory sensitivity within compact disposable cartridges. It also fits the current commercial model of analyzer plus consumable revenue, which makes it attractive to large vendors with manufacturing scale and existing hospital relationships. As a result, microfluidics remains the default platform for many near-patient cardiac assays already in active use. The segment’s leadership reflects a combination of analytical strength, established production capability, and compatibility with current clinical workflow expectations.

Array-based systems are forecast to grow at a 14.35% CAGR through 2031, which makes them the fastest-expanding technology class in the heart failure POC and LOC devices market. Nature’s 2026 paper showed that array-like multiplexed sensing combined with deep learning can quantify NT-proBNP, cTnI, and CK-MB from a compact paper-based format, which demonstrates how multiplex capability is improving in smaller systems. The commercial attraction is that array-based systems can expand panel breadth without repeating the full manufacturing complexity associated with every separate immunoassay cartridge. That can lower the entry barrier for mid-tier firms that want to compete on multiplex breadth, especially as electrochemical and photolithographic fabrication methods mature. The technology is still behind microfluidics in installed base, but its cost structure and panel flexibility make it a credible growth challenger over the next several years.

By Biomarker: NT-proBNP and BNP Anchor Demand While Multi-Panel Combinations Gain Ground

NT-proBNP and BNP held 58.62% of biomarker revenue in 2025, which made them the leading biomarker class in the heart failure POC and LOC devices market share because they remain central to diagnosis, prognosis, and triage pathways. Their position is reinforced by ACC and AHA guideline familiarity, by legal testing designations for waived whole blood formats in selected configurations, and by broad clinician comfort with threshold-based interpretation. Troponin plays a complementary role because it helps identify concurrent myocardial injury and adds value in mixed cardiac presentations seen in emergency departments. Siemens’ 2025 FDA-cleared Atellica IM high-sensitivity troponin I claim for longer-term prognostic use also widened the commercial relevance of troponin beyond acute rule-in and rule-out use. Even with broader biomarker interest, natriuretic peptides still define the base demand profile for this category.

Multi-biomarker panels are forecast to expand at a 14.82% CAGR through 2031, which makes them the fastest-growing biomarker segment in the heart failure POC and LOC devices market. JACC Basic to Translational Science described metabolomics-based precision strategies as capable of subclassifying heart failure phenotypes in ways that can influence treatment direction, which supports broader panel adoption. Combining NT-proBNP with soluble ST2, galectin-3, or metabolic markers gives clinicians a broader mechanistic view of fibrosis, inflammation, and hemodynamic stress within one test run. The UCLA-linked 2026 optical sensing work also points toward cartridge and chip architectures that can support this type of multiplex co-detection at very high sensitivity. As reimbursement and validation mature, panel formats are likely to take a larger share of incremental growth even if BNP and NT-proBNP remain the largest individual biomarker category.

By Application: Emergency Diagnosis Dominates While Chronic Monitoring Deepens

Acute heart failure diagnosis in emergency settings accounted for 66.23% of application revenue in 2025, which gave it the largest application position in the heart failure POC and LOC devices market size because dyspnea triage remains the most established use case for BNP and NT-proBNP. CMS coverage language specifically supports near-patient BNP use for differentiating cardiogenic from non-cardiogenic dyspnea, which makes the emergency setting a strong reimbursement-backed demand center. The role of age-stratified rule-out thresholds also helps standardize interpretation across busy emergency care environments. This application remains dominant because the clinical consequence of delayed triage is high, while the operational value of rapid results is immediate. Risk stratification and readmission prevention add another layer of demand, but emergency diagnosis still carries the strongest volume concentration today.

Chronic heart failure monitoring and therapy optimization is projected to grow at a 13.02% CAGR through 2031, which shows that the fastest new opportunity is moving beyond one-time triage toward ongoing patient management. JACC Heart Failure reported in 2025 that HeartLogic-capable implantable devices detected worsening heart failure earlier than symptom-based monitoring, which supports wider use of connected monitoring frameworks. JACC Basic to Translational Science also described the HF Monitor wearable molecular device as a proof-of-concept route toward multi-day ambulatory biomarker tracking without repeated blood draws. These developments matter because they move biomarker use into post-discharge care, medication optimization, and earlier detection of worsening status in outpatient settings. As remote physiologic monitoring reimbursement becomes more established, this application is positioned to capture a larger share of forecast growth even if emergency care remains the main revenue base.

By End User: Hospitals Lead While Homecare Programs Expand Fastest

Hospitals and clinics held 45.89% of end-user revenue in 2025, which made them the leading demand center in the heart failure POC and LOC devices market because they combine high patient volume, skilled staff, validated protocols, and direct access to analyzer networks. These sites are where acute diagnostic demand is concentrated, so they naturally hold the largest installed base for BNP and troponin testing. Specialty centers remain important secondary users because they support structured risk stratification and outpatient disease management in cardiology-led programs. Primary care and urgent care sites are expanding their role, but share gains remain tempered by classification barriers and reimbursement friction for more advanced panels. The end-user mix, therefore, still leans toward higher-acuity care settings even as decentralization gradually expands.

Homecare and remote patient monitoring programs are expected to grow at a 13.77% CAGR through 2031, which makes them the fastest-growing end-user segment in the heart failure POC and LOC devices market. This growth is being supported by post-discharge management programs, remote physiologic monitoring reimbursement, and patient preference for care pathways that reduce repeated facility visits. A 2025 cost-effectiveness study found that a home-based heart failure management system reduced mean per-patient care costs by USD 6,723 over 5 years and lowered readmissions by 10.5%, which strengthens the economic case for broader remote deployment. Even so, broad home use still depends on whether near-patient LOC systems can combine analytical reliability, simple patient operation, and durable reimbursement support in everyday practice. That means the segment has strong momentum, but its full long-term opportunity will depend on product design and payment alignment as much as on clinical need.

Geography Analysis

The United States is the largest single geography within the heart failure POC and LOC devices market and the main launch market for meaningful commercial platform clearances. Its position is strengthened by a reimbursement framework that is more structured than most comparable markets, even when that same framework also places limits on serial inpatient monitoring. Demand is especially concentrated in states such as Florida, California, Texas, and Pennsylvania, where Medicare-heavy demographics support higher use of near-patient cardiac testing. This makes regulatory literacy and payer navigation central commercial capabilities for any company competing in the heart failure POC and LOC devices market in the United States.

Within the country, the urban-rural divide remains a major structural issue because many rural communities lack the laboratory infrastructure needed for more complex cardiac immunoassay operations. CLIA-waived whole blood BNP platforms address part of that access gap by allowing smaller community sites to screen for heart failure without building a full moderate-complexity laboratory capability. Kaiser Permanente Northern California’s 2025 rollout of STRIDE-HF across 21 emergency departments also shows how large integrated systems can scale biomarker-supported triage models quickly when data systems are aligned. Sun Belt markets are emerging as strong volume centers because heart failure prevalence is being reinforced by obesity, hypertension, and type 2 diabetes burden, while retail-linked screening models open new channels outside hospitals.

The market is also benefiting from a post-pandemic restoration of outpatient cardiology and diagnostic activity that had been delayed earlier in the decade. Global manufacturers continue to prioritize U.S. commercialization, as shown by Roche, Abbott, Siemens, Beckman Coulter, and others receiving meaningful U.S.-focused regulatory or launch milestones between 2024 and 2026. A 2025 U.S. cost-effectiveness model found that connected heart failure monitoring systems can lower 5-year care costs by USD 6,723 per patient, which supports wider adoption under value-based care logic. Taken together, these conditions give the United States a commercial profile that is both high growth and highly shaped by regulatory detail within the heart failure POC and LOC devices market.

Competitive Landscape

The heart failure POC and LOC devices market in the United States is moderately concentrated, with Abbott Laboratories, Roche Diagnostics, and Siemens Healthineers controlling the majority of 2025 revenue through analyzer, consumable, and software bundles that reinforce recurring sales. Their advantage comes not only from assay breadth, but also from connectivity, service contracts, validation history, and the operational cost of switching away from entrenched systems. Abbott strengthened its position with the 2026 CardioMEMS HERO reader approval and i-STAT Alinity multi-marker cardiac panel clearance, both of which extend its reach across monitoring and near-patient diagnosis. Siemens has focused on workflow depth, with Atellica VTLi combining fingerstick speed with Wi-Fi and Ethernet links into its POC Ecosystem Solution for centralized oversight of decentralized sites. Roche has continued to invest in cardiac biomarker accuracy and forward product positioning, as shown by its 2025 sixth-generation troponin T update and the broader push to secure a U.S. follow-on commercial opportunity.

Large central laboratory vendors are also defending adjacent territory rather than surrendering it to POC-native firms. Beckman Coulter’s 2024 Access NT-proBNP clearance and 2026 Access BNP II clearance show a strategy focused on faster, more competitive cardiac testing inside the lab environment itself. QuidelOrtho retains an important niche because its Triage BNP Test remains the only CLIA-waived whole blood BNP option identified, which gives it a distinct role in physician office and urgent care decentralization. The result is a competitive field where incumbents still hold scale advantages, but targeted product positioning can create meaningful openings for challengers.

Mid-tier and emerging companies are mostly using wedge strategies rather than broad platform competition across the full care pathway. Quanterix is pushing ultra-sensitive single-molecule detection toward more compact formats, while lower-cost and cloud-native vendors are targeting smaller hospitals and community-based sites that value simpler deployment. The clearest white spaces remain home biomarker monitoring and clinically validated metabolomic panel deployment, where need is visible but product, reimbursement, and regulatory readiness are still forming. Compliance expectations such as ISO 22870 and CLSI analytical performance verification still shape procurement decisions, which means technical performance alone is not enough to win formulary adoption in the heart failure POC and LOC devices market.

United States Heart Failure POC and LOC Devices Industry Leaders

Abbott Laboratories

Bio-Rad Laboratories, Inc.

bioMérieux S.A.

Danaher Corporation

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Abbott received FDA approval for the CardioMEMS HERO reader, a next-generation pulmonary artery pressure monitoring device for NYHA Class III heart failure patients, featuring a redesigned smaller form factor. The HERO reader generates daily PA pressure and vital signs data transmitted from home to care teams, advancing continuous connected remote monitoring for chronic HF management.

- February 2026: Abbott received FDA approval for the CardioMEMS HERO reader, a next-generation pulmonary artery pressure monitoring device for NYHA Class III heart failure patients, featuring a redesigned smaller form factor. The HERO reader generates daily PA pressure and vital signs data transmitted from home to care teams, advancing continuous connected remote monitoring for chronic HF management.

- September 2025: Roche announced primary results from the TSIX Study Program at ESC Congress 2025, demonstrating high AMI diagnostic precision for the Elecsys Troponin T hs Gen 6 test. The sixth-generation test received CE Mark approval, with US regulatory filing anticipated to follow.

United States Heart Failure POC and LOC Devices Market Report Scope

The United States Heart Failure POC (Point-of-Care) and LOC (Lab-on-a-Chip) Devices Market is a specialized healthcare segment focused on rapid, decentralized cardiovascular diagnostics.

The United States Heart Failure POC (Point-of-Care) and LOC (Lab-on-a-Chip) Devices Market is segmented across several dimensions. By Device Type, it includes Point-of-Care Devices and Lab-on-Chip Devices. By test type, the market is divided into Proteomic Testing, Metabolomic Testing, and Genomic Testing. By Technology, segmentation covers Microfluidics and Array-Based Systems. By Biomarker, the market is categorized into NT-proBNP and BNP, Troponin, and Multi-Biomarker Panels. By Application, it includes Acute Heart Failure Diagnosis in Emergency Settings, Chronic Heart Failure Monitoring and Therapy Optimization, and Risk Stratification and Readmission Prevention. By End User, the market is segmented into Hospitals and Clinics, Specialty Centers, Homecare and Remote Patient Monitoring Programs, and Primary Care and Urgent Care Centers.

| Point-of-Care Devices |

| Lab-on-Chip Devices |

| Proteomic Testing |

| Metabolomic Testing |

| Genomic Testing |

| Microfluidics |

| Array-Based Systems |

| NT-proBNP and BNP |

| Troponin |

| Multi-Biomarker Panels |

| Acute Heart Failure Diagnosis in Emergency Settings |

| Chronic Heart Failure Monitoring and Therapy Optimization |

| Risk Stratification and Readmission Prevention |

| Hospitals and Clinics |

| Specialty Centers |

| Homecare and Remote Patient Monitoring Programs |

| Primary Care and Urgent Care Centers |

| By Device Type | Point-of-Care Devices |

| Lab-on-Chip Devices | |

| By Test Type | Proteomic Testing |

| Metabolomic Testing | |

| Genomic Testing | |

| By Technology | Microfluidics |

| Array-Based Systems | |

| By Biomarker | NT-proBNP and BNP |

| Troponin | |

| Multi-Biomarker Panels | |

| By Application | Acute Heart Failure Diagnosis in Emergency Settings |

| Chronic Heart Failure Monitoring and Therapy Optimization | |

| Risk Stratification and Readmission Prevention | |

| By End User | Hospitals and Clinics |

| Specialty Centers | |

| Homecare and Remote Patient Monitoring Programs | |

| Primary Care and Urgent Care Centers |

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for heart failure POC and LOC devices in the United States?

The United States heart failure POC and LOC devices market is expected to rise from USD 84.02 million in 2026 to USD 152.97 million by 2031 at a 12.73% CAGR, supported by aging patient populations, reimbursement support, and faster decentralized testing formats.

Which device format currently leads revenue in U.S. heart failure testing?

Point-of-Care devices led with 64.23% of revenue in 2025 because they are already embedded in emergency and acute care workflows, while Lab-on-Chip systems are growing faster as they expand into physician office, urgent care, and post-discharge settings.

Why are BNP and NT-proBNP still central in near-patient heart failure diagnostics?

BNP and NT-proBNP held 58.62% of biomarker revenue in 2025 because they have strong clinical acceptance, recognized threshold frameworks, and reimbursement support for key triage use cases in emergency and outpatient care.

What is driving faster adoption of homecare and remote monitoring programs for heart failure?

Homecare and remote patient monitoring programs are projected to grow at a 13.77% CAGR through 2031, helped by post-discharge optimization efforts, remote physiologic monitoring reimbursement, and evidence that connected care can reduce costs and readmissions.

How are multi-marker panels changing the heart failure testing landscape in the United States?

Multi-biomarker panels are forecast to grow at a 14.82% CAGR through 2031 because they combine markers for volume overload, injury, fibrosis, and inflammation, which improves stratification potential beyond single-marker workflows in selected settings.

Page last updated on: