Heart Failure POC And LOC Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

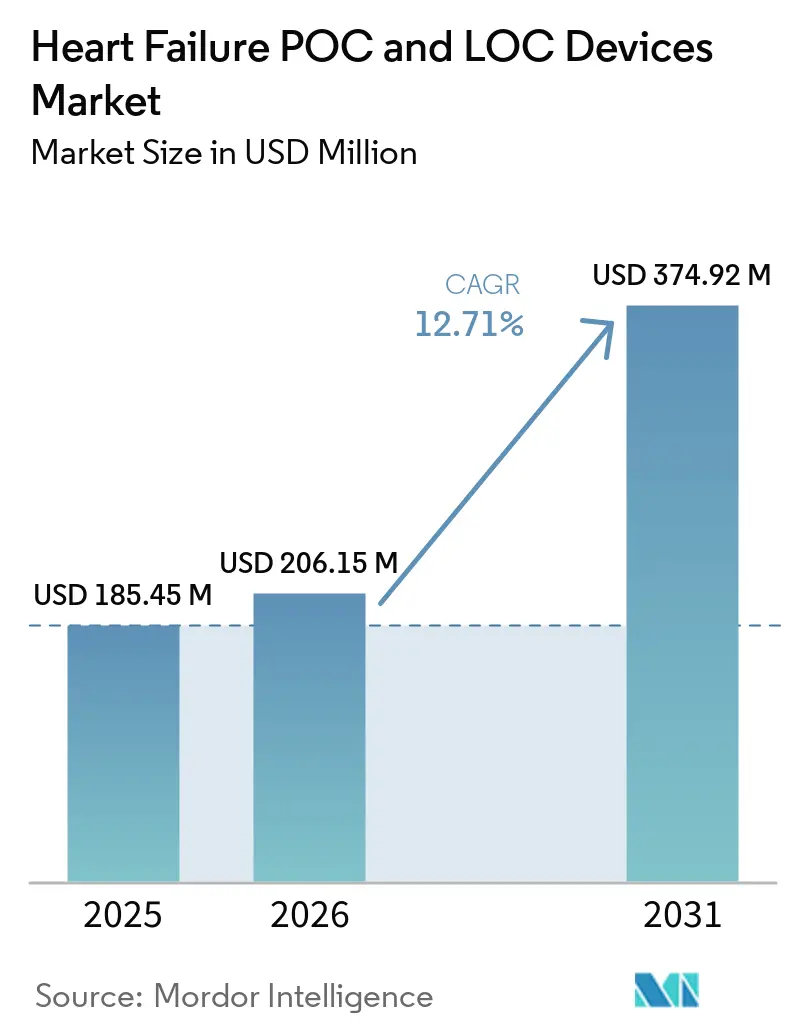

| Market Size (2026) | USD 206.15 Million |

| Market Size (2031) | USD 374.92 Million |

| Growth Rate (2026 - 2031) | 12.71% CAGR |

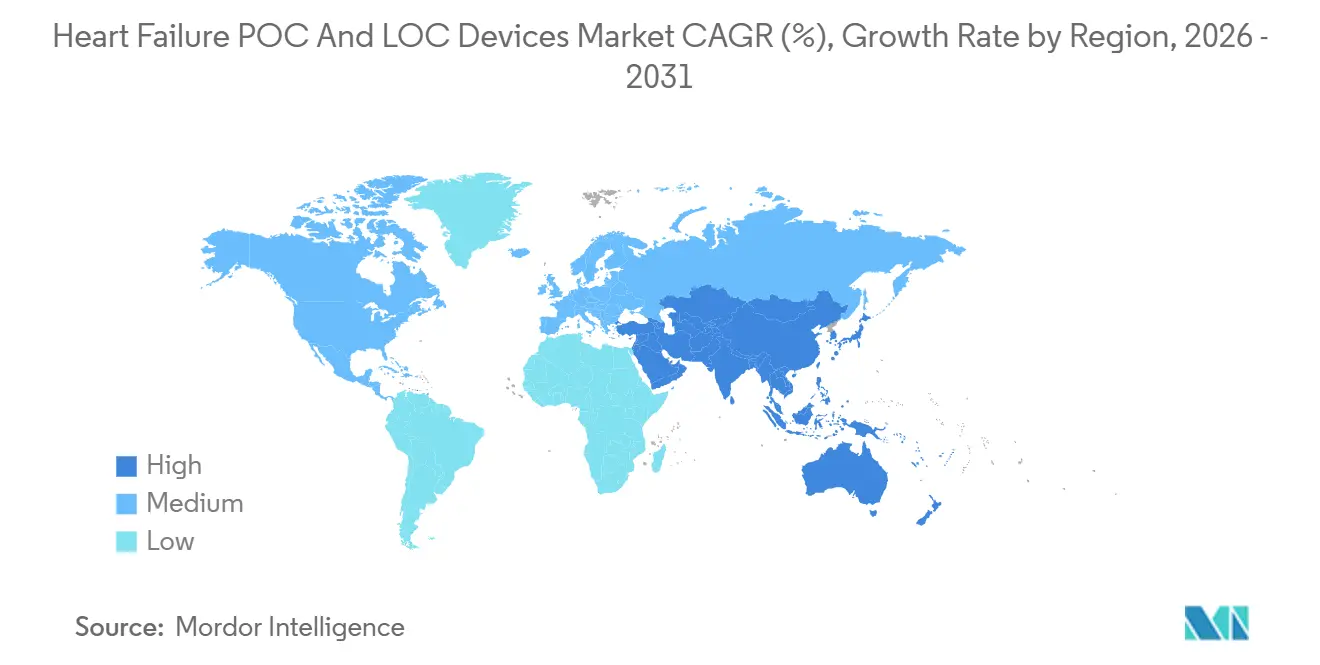

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

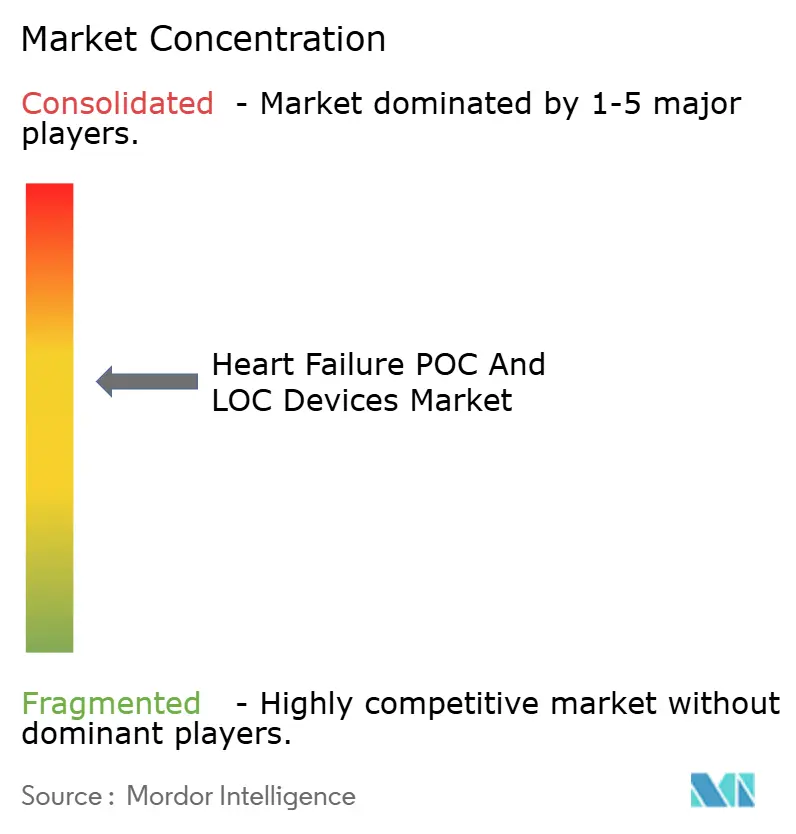

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heart Failure POC And LOC Devices Market Analysis by Mordor Intelligence

The Heart Failure POC And LOC Devices Market size is expected to grow from USD 185.45 million in 2025 to USD 206.15 million in 2026 and is forecast to reach USD 374.92 million by 2031 at 12.71% CAGR over 2026-2031.

Escalating reliance on near-patient natriuretic peptide testing in emergency and primary care settings, broader reimbursement in the United States, and guideline mandates in Europe are driving platform placements and recurring cartridge sales. Multi-marker panels that combine BNP or NT-proBNP with soluble ST2 or galectin-3 are gaining traction because they stratify risk more precisely than single-analyte assays. Finger-stick-compatible microfluidic systems are broadening the addressable base to retail clinics and rural hospitals that lack certified laboratory technologists. At the same time, hospitals are prioritizing analyzers that transmit results directly to electronic health records, because seamless data integration shortens documentation time and supports quality-metric reporting. Competitive pressure is intensifying as cloud-enabled startup platforms undercut incumbents on hardware price while bundling software interpretation algorithms.

Key Report Takeaways

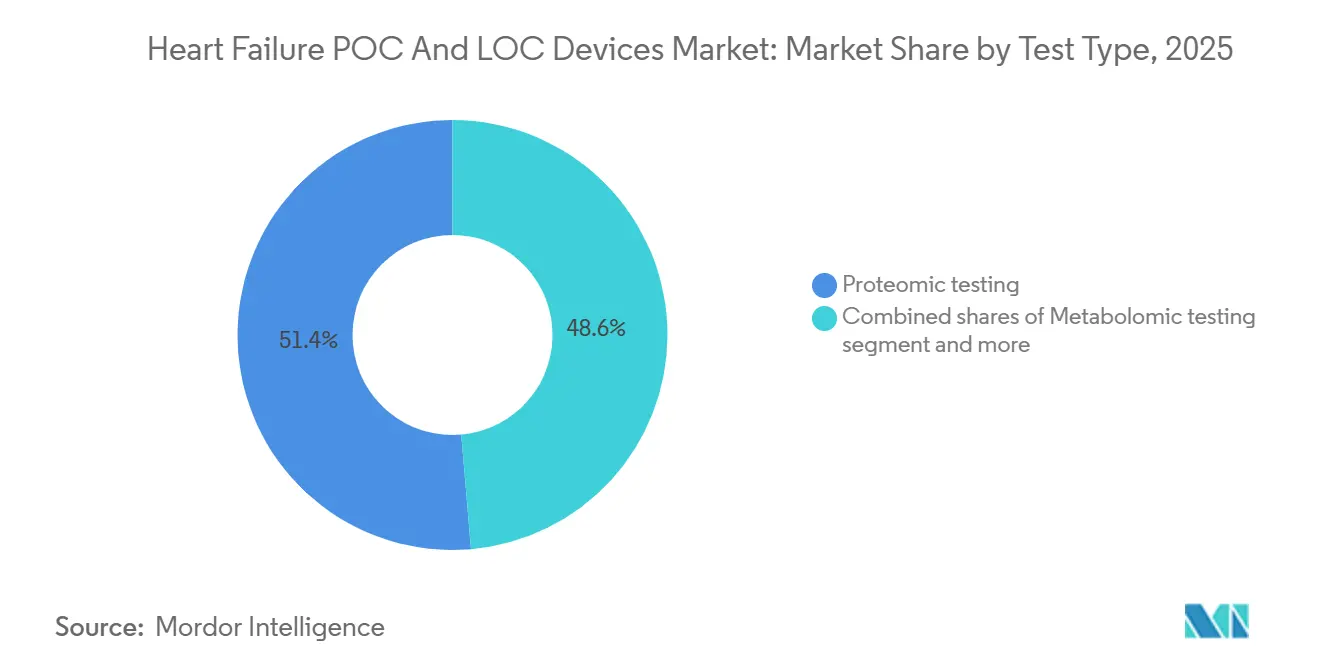

- By device type, Point-of-Care (POC) Devices led with 64.59% revenue share in 2025, and are expected to grow at 13.43% CAGR by 2031.

- By test type, proteomic assays led with 51.4% revenue share in 2025, yet metabolomic testing is forecast to advance at a 13.67% CAGR through 2031, the fastest among assay classes.

- By platform, microfluidic digital immunoassay platforms captured 46.40% of 2025, yet immunofluorescence readers are projected to record the highest platform CAGR at 13.32% over 2026-2031.

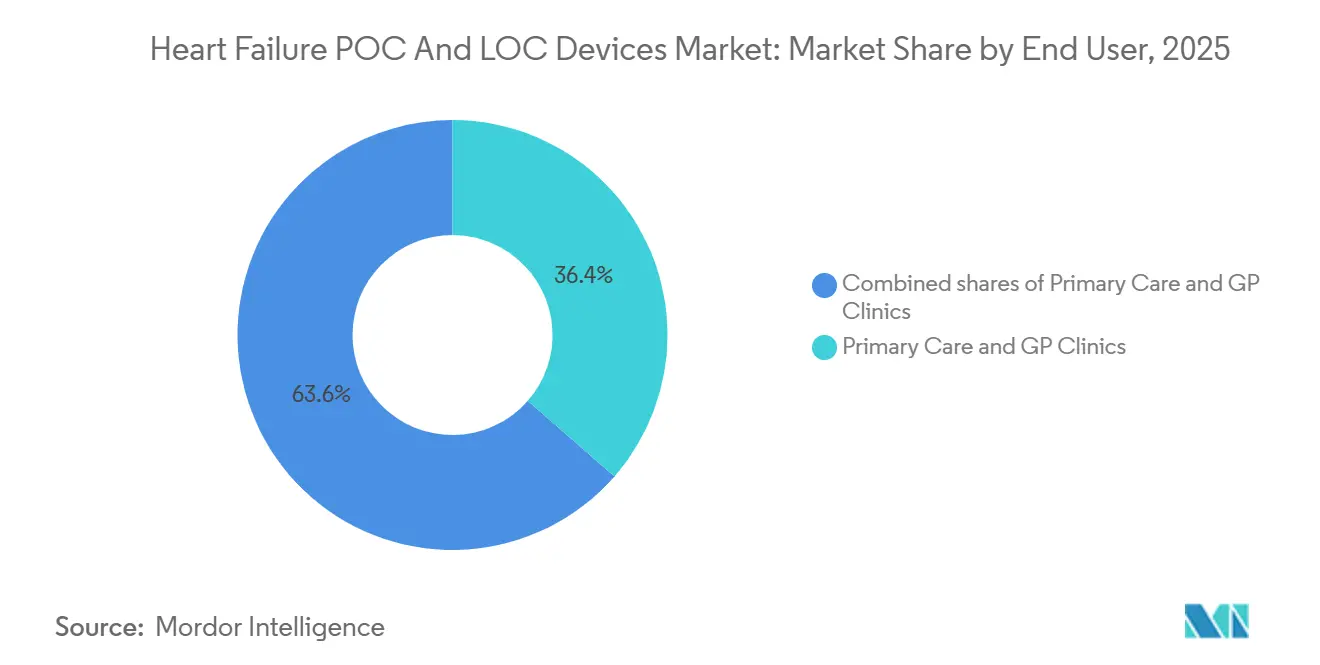

- By end users, primary-care and GP clinics held 36.43% of 2025 end-user revenue and are expected to expand at a 13.73% CAGR through 2031.

- By geography, North America accounted for 46.25% of global sales in 2025, while Asia-Pacific is poised to grow at a 13.48% regional CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heart Failure POC And LOC Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Guideline-backed natriuretic peptide testing | +2.8% | North America, Europe, global spillover | Medium term (2-4 years) |

| Operational gains from rapid NP testing | +2.3% | North America, Europe, APAC urban hubs | Short term (≤ 2 years) |

| CLIA-waived BNP availability | +1.9% | United States, Canada | Short term (≤ 2 years) |

| APAC health-system POCT investments | +2.6% | China, India, Japan, Southeast Asia | Long term (≥ 4 years) |

| Microfluidic finger-stick NT-proBNP assays | +1.7% | Global, early uptake in ambulatory and retail sites | Medium term (2-4 years) |

| Rise of multi-marker HF panels | +1.4% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Guideline-Backed Natriuretic Peptide Testing Adoption in ED and Primary Care

Diagnostic societies now require BNP or NT-proBNP results within 1 hour of patient arrival, which central laboratories rarely achieve during peak periods [1]European Society of Cardiology, “2024 ESC Guidelines for Acute and Chronic Heart Failure,” esc.org. U.S. cardiology bodies echoed this stance in 2025, effectively doubling the pool of patients eligible for testing in emergency departments. Primary-care uptake is accelerating following the United Kingdom guidance instructing general practitioners to rule out heart failure with NT-proBNP before making referrals. These policies require hospitals to relocate assays from the core lab to triage bays and encourage office-based clinicians to install handheld readers. Vendors that can certify devices to ISO 15189 and EU IVDR standards are enjoying faster market clearance and wider tender eligibility.

APAC Health-System Investments in POCT Infrastructure

Asia-Pacific governments view decentralized diagnostics as a cost-effective way to shorten referral pathways and address uneven laboratory capacity. China earmarked CNY 12 billion (USD 1.7 billion) in 2025 to outfit county hospitals with cardiac biomarker analyzers. India’s Ayushman Bharat program favors connected devices that upload results to the national health records system. Japan raised the NT-proBNP reimbursement ceiling to JPY 1,800 (USD 12) per test in 2025, halving payback periods for hospitals. South Korea matched central-lab fees for POC BNP in 2025, eliminating historical cost penalties. These incentives accelerate the distributor's focus on APAC, where device penetration still trails that of the West.

Microfluidic/Digital LOC NT-proBNP Assays Enabling Finger-Stick Workflows

Advances in single-molecule array chemistry allow quantitation from 15-microliter capillary samples, removing venipuncture and centrifugation bottlenecks. Roche secured FDA clearance for the Cobas Pulse handheld system in 2025, achieving a limit of quantitation of 10 pg/mL. Abbott followed with the i-STAT Alinity cartridge, returning NT-proBNP results in 12 minutes. Retail pharmacies are piloting these devices to offer same-day screening, a move that blurs the line between clinical diagnostics and consumer health. The finger-stick format also suits rural hospitals, EMS units, and telehealth programs that lack laboratory phlebotomists.

Operational Gains from Rapid NP Testing

A multicenter study showed that POC NT-proBNP shortened emergency-department length of stay by 47 minutes and cut observation admissions by 18%. Each avoided admission saved roughly USD 1,200 in direct costs, which offsets higher reagent prices. The American College of Emergency Physicians recognized these savings in its 2024 dyspnea policy update. Hospitals now steer low-risk patients directly to discharge, freeing beds for higher-acuity cases and improving throughput during crowding surges. Faster disposition also improves patient satisfaction scores, which influence value-based purchasing bonuses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Neutral RCT evidence on triage outcomes | -1.2% | North America, Europe | Short term (≤ 2 years) |

| Moderate-complexity status for many assays | -1.5% | United States, Canada | Medium term (2-4 years) |

| BNP/NT-proBNP variability and ARNI effects | -1.8% | Global, acute in high-ARNI markets | Long term (≥ 4 years) |

| Competition from point-of-care ultrasound | -2.1% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BNP vs NT-proBNP Assay Variability and Drug Interference Risks

Sacubitril-valsartan suppresses BNP but not NT-proBNP, generating discordant readings that can misclassify patients. Cardiology societies now favor NT-proBNP for treated patients, yet many low-cost POC platforms offer only BNP because of simpler reagent chemistry. The American Heart Association advises clinicians to record ARNI use and adjust BNP cutoffs, adding complexity that erodes time savings. Cross-platform variability of up to 20% persists despite early harmonization work by the IFCC[2]International Federation of Clinical Chemistry, “Natriuretic Peptide Harmonization,” ifcc.org. Manufacturers must recalibrate assays to emerging universal standards, a process that could stretch into 2028.

Competition from Point-of-Care Ultrasound and Integrated Care Pathways

Handheld echocardiography visualizes ventricular function without consumables, providing a rival diagnostic pathway for acute dyspnea. A European trial found similar accuracy between POC ultrasound and NT-proBNP testing, with no difference in 30-day readmissions. U.S. emergency departments have boosted ultrasound availability to 68%, up from 42% in 2022. NICE now recommends ultrasound over natriuretic peptide testing when trained operators are available. As integrated pathways merge clinical scores, imaging, and laboratory data, the incremental value of single-marker testing narrows, challenging vendors to deliver multi-marker or hybrid imaging-biomarker solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Proteomic Dominance Faces Metabolomic Disruption

Proteomic assays captured a 51.4% Heart Failure POC and LOC Devices market share in 2025, largely due to entrenched use of BNP and NT-proBNP across triage algorithms. Metabolomic panels are climbing at a 13.67% CAGR because ceramide and acylcarnitine signatures reclassify 22% of patients into higher-risk strata, prompting earlier device therapy initiation [3]Journal of the American College of Cardiology, “Ceramide Panel Improves Risk Stratification,” jacc.org. Proteomic testing still benefits from widespread reimbursement and physician familiarity, but clinicians at specialty heart-failure centers are beginning to order metabolomic panels for prognostic fine-tuning. Manufacturers are racing to combine both analyte classes on single cartridges, which could unify guideline compliance with incremental prognostic power. Genomic assays remain in pilot use because payers frequently deem them investigational, yet successful trial outcomes could unlock coverage by 2028.

Metabolomic expansion is also reshaping supplier dynamics. Startups with lipidomics expertise partner with established platform owners to secure analyzer shelf space, while hospital labs benchmark metabolomic cost per quality-adjusted life-year against implantable hemodynamics monitors. If reimbursement parity emerges, metabolomic cartridges could displace single-marker assays in advanced-care pathways. Until then, the Heart Failure POC and LOC Devices market size for proteomic testing will continue to dwarf newer segments, though its growth will trail the metabolomic curve.

By Platform: Microfluidic Systems Lead, Immunofluorescence Gains Ground

Microfluidic digital immunoassay systems accounted for 46.40% of platform revenue in 2025, demonstrating superior analytical sensitivity at low sample volumes. Hospitals deploy them to achieve sub-15-minute turnaround while minimizing nurse handling steps. Immunofluorescence readers, however, are expanding at a 13.32% CAGR because they cost less to acquire and can run a broader menu of infectious-disease tests. The Heart Failure POC and LOC Devices market size for microfluidic platforms is forecast to rise steadily but will concede share to fluorescence systems in community clinics that prioritize upfront affordability over ultralow limits of detection.

Vendor road maps reveal convergence. Siemens launched a chemiluminescence benchtop analyzer that combines 30-test hourly throughput with automatic QC. Quanterix obtained CE-IVD for a handheld reader using single-molecule arrays, pushing microfluidics into price points once reserved for fluorescence. As capital budgets tighten, platform leases bundled with cartridge minimums are replacing outright purchases, generating recurring revenue for suppliers and lower initial outlays for buyers. Integration with cloud analytics will further differentiate offers, as administrators seek dashboards that track reagent burn rates and clinical key performance indicators.

By End User: Primary Care Clinics Outpace Hospitals

Primary-care and GP clinics generated 36.43% of 2025 revenue, the highest of any setting, and are projected to post a 13.73% CAGR. Hospitals still command the largest absolute Heart Failure POC and LOC Devices market size, yet their share is slipping as payers shift diagnostics to lower-cost outpatient venues. Decentralized testing enables clinics to triage suspected heart-failure patients on the same day, cutting referral wait times and reducing unnecessary echocardiograms. Retail pharmacies are piloting similar services, bringing biomarker access closer to consumers and magnifying competitive pressure on traditional laboratories.

Diagnostic centers and EMS providers remain niche buyers. Prehospital trials in London suggested potential reductions in transport, but reagent costs and training hurdles stalled broad deployment. In contrast, chain labs in emerging markets treat POC assays as premium walk-in offerings for self-pay clients. As payer and regulator enthusiasm for community-based triage grows, the Heart Failure POC and LOC Devices industry faces a strategic question: whether to build direct-to-consumer brands or double down on institutional contracting.

By Device Type: POC Platforms Consolidate Dominance

Point-of-care (POC) systems handled 64.59% of global sales in 2025 and are on track for a 13.43% CAGR through 2031. Hospitals favor them because they cut emergency-department length of stay by roughly 45 minutes, reduce crowding, and lower observation-bed costs. The U.S. Food and Drug Administration removed the main regulatory hurdle in 2024 when it granted CLIA-waived status to several BNP assays, allowing physician offices, urgent-care clinics, and retail pharmacies to run tests without hiring certified laboratory technologists. Abbott’s i-STAT and Roche’s Cobas h 232 hold the largest installed base, but newer benchtop chemiluminescence units that process up to 30 tests an hour are challenging that lead in busy emergency departments. Government tenders in Asia-Pacific tier-2 hospitals increasingly specify a 15-minute turnaround and seamless links to national electronic health record systems, which further strengthens the appeal of POC devices.

Geography Analysis

North America accounted for 46.25% of global revenue in 2025, supported by Medicare reimbursement rising to USD 24 per test and the elimination of prior authorizations for Medicare Advantage plans. U.S. physician-office laboratories expanded BNP testing after multiple devices earned CLIA-waived status in 2024-2025. Canada pilots POC programs in rural emergency departments, though budget variability among provinces slows full rollout. Mexico’s private hospitals adopt analyzers to differentiate premium emergency services, but public-sector uptake lags because central-lab infrastructure is concentrated in urban hubs.

Asia-Pacific is the fastest-growing region and will post a 13.48% CAGR through 2031. China’s county-hospital stimulus spurs volume orders for combined cardiac and metabolic analyzers. India’s procurement rules favor cloud-connected readers that feed data into the Ayushman Bharat Digital Health network. Japan’s reimbursement hike to USD 12 per NT-proBNP test halves payback periods and unlocks capital budgets in mid-size hospitals. South Korea, Australia, and Southeast Asia replicate the pattern, emphasizing decentralized diagnostics to alleviate physician shortages and reduce patient travel distances.

Europe holds a mature but slower-growing position. ESC guidelines require BNP or NT-proBNP within 60 minutes of ED arrival, anchoring steady cartridge demand. However, compliance with the EU IVDR raises validation costs and delays launches, stretching vendor regulatory timelines. Germany leads per-capita analyzer density, while the United Kingdom aligns adoption with NHS funding cycles. Middle East & Africa and South America remain early-stage, with flagship private hospitals in the Gulf and Brazil pioneering placements, but large public tenders are scarce.

Competitive Landscape

Abbott Laboratories, Roche Diagnostics, and Siemens Healthineers together captured the majority of 2025 revenue, yet microfluidic startups and regional firms are eroding this lead. Incumbents respond with analyzer-consumable-software bundles that lock clients into multiyear subscriptions and heighten switching costs. Roche patented a hybrid cartridge integrating plasma separation to streamline ED workflows. Abbott received FDA clearance in 2026 for a multi-marker panel that combines NT-proBNP, troponin I, and soluble ST2 into a single 15-minute test. Siemens released a high-throughput benchtop system targeting crowded EDs

Startups leverage lower cost bases and agile cloud architectures. QuidelOrtho is developing a smartphone-linked reader that uses AI to adjust NT-proBNP cutoffs for age and renal function. Quanterix pushes single-molecule sensitivity into compact formats for specialty clinics. Regional manufacturers in China and India undercut global prices and pair devices with cloud portals that satisfy local data-sovereignty rules. Regulatory scrutiny favors firms with robust clinical trial datasets, nudging cash-constrained newcomers toward co-development deals with diversified conglomerates.

Success now rests on three levers: finger-stick capability, turn-around below 10 minutes, and interpretative algorithms that contextualize biomarker values. Vendors that deliver all three, while meeting IVDR and FDA expectations, will carve out durable positions even as ultrasound and integrated pathways nibble at testing volumes. The Heart Failure POC and LOC Devices market therefore remains contestable and innovation-driven, rather than locked up by any single incumbent.

Heart Failure POC And LOC Devices Industry Leaders

F. Hoffmann-La Roche Ltd

Siemens Healthineers AG

Abbott Laboratories

Becton, Dickinson and Company

Bio-Rad Laboratories, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Abbott received FDA approval for the CardioMEMS HERO reader, a next-generation pulmonary artery pressure monitor for chronic heart failure management.

- February 2026: Abbott obtained 510(k) clearance for the i-STAT Alinity Multi-Marker Cardiac Panel measuring NT-proBNP, hs-troponin I, and soluble ST2.

- January 2026: Siemens Healthineers launched the Atellica VTLi patient-side analyzer with automated QC and EHR connectivity.

Global Heart Failure POC And LOC Devices Market Report Scope

As per the scope of the report, Heart Failure (HF) management is being transformed by Point-of-Care (POC) and Lab-on-a-Chip (LOC) devices that enable rapid, decentralized testing of critical biomarkers. While POC devices are currently the primary commercially available diagnostic option, LOC technology is an emerging field that uses microfluidics to miniaturize lab functions onto a single chip, enabling even faster, more precise results.

The Heart Failure POC and LOC Devices Market is segmented by device type, test type, platform, end users, and geography. By device type, the market is segmented into point-of-care (POC) devices and lab-on-chip (LOC) devices. By test type, the market is segmented into proteomic, metabolomic, and genomic testing. By platform, the market is segmented into immunofluorescence readers, benchtop chemiluminescence POC, and microfluidic digital immunoassay. By end users, the market is segmented into hospitals & IDNs, primary care & GP clinics, diagnostic centers, EMS providers, and retail clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Point-of-Care (POC) Devices |

| Lab-on-Chip (LOC) Devices |

| Proteomic testing |

| Metabolomic testing |

| Genomic testing |

| Immunofluorescence readers |

| Benchtop chemiluminescence POC |

| Microfluidic digital immunoassay |

| Hospitals & IDNs |

| Primary Care & GP Clinics |

| Diagnostic Centers |

| EMS Providers |

| Retail Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Point-of-Care (POC) Devices | |

| Lab-on-Chip (LOC) Devices | ||

| By Test Type | Proteomic testing | |

| Metabolomic testing | ||

| Genomic testing | ||

| By Platform | Immunofluorescence readers | |

| Benchtop chemiluminescence POC | ||

| Microfluidic digital immunoassay | ||

| By End User | Hospitals & IDNs | |

| Primary Care & GP Clinics | ||

| Diagnostic Centers | ||

| EMS Providers | ||

| Retail Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Heart Failure POC and LOC Devices market by 2031?

The market is forecast to reach USD 374.92 million by 2031 on the back of a 12.71% CAGR.

Which assay type currently leads revenue?

Proteomic testing, anchored by BNP and NT-proBNP, held 51.4% share in 2025.

Why is Asia-Pacific the fastest-growing region?

Government funding, reimbursement expansion, and rising heart-failure prevalence are driving a 13.48% regional CAGR through 2031.

How are guideline changes influencing platform demand?

ESC and ACC mandates for rapid natriuretic peptide turnaround compel hospitals and clinics to adopt near-patient analyzers.

What technology trends will shape product road maps?

Finger-stick sampling, sub-10-minute turnaround, and AI-driven multi-marker interpretation are becoming must-have features

Page last updated on: