Primary Care PoC Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

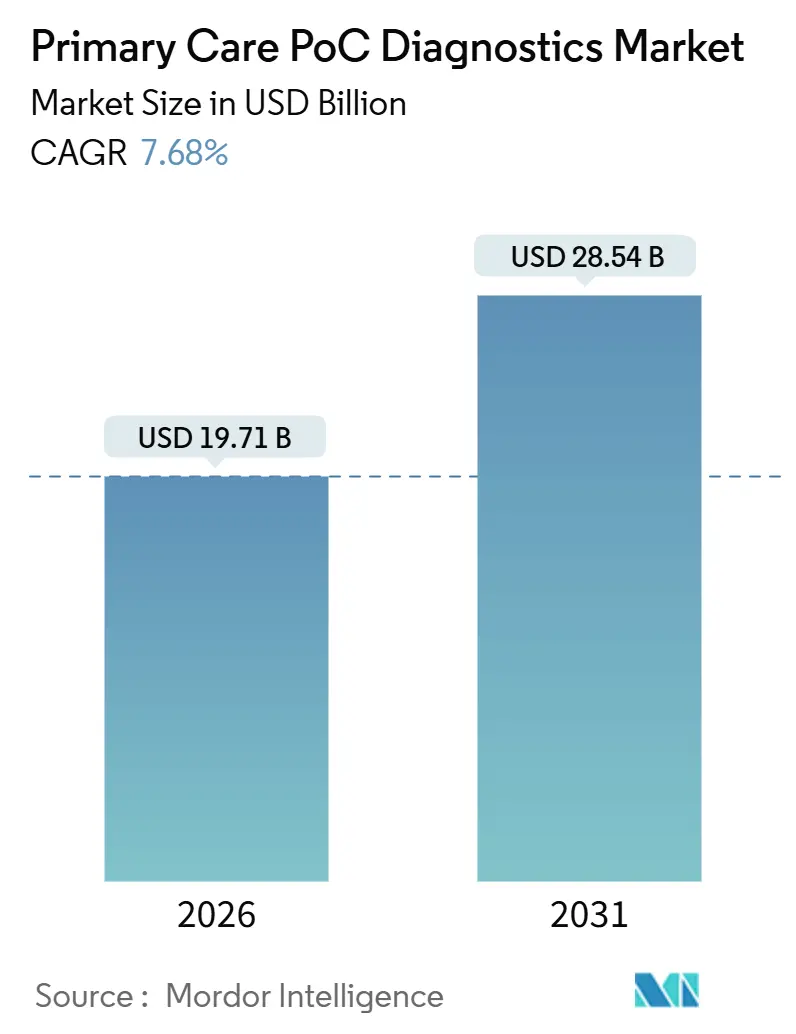

| Market Size (2026) | USD 19.71 Billion |

| Market Size (2031) | USD 28.54 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

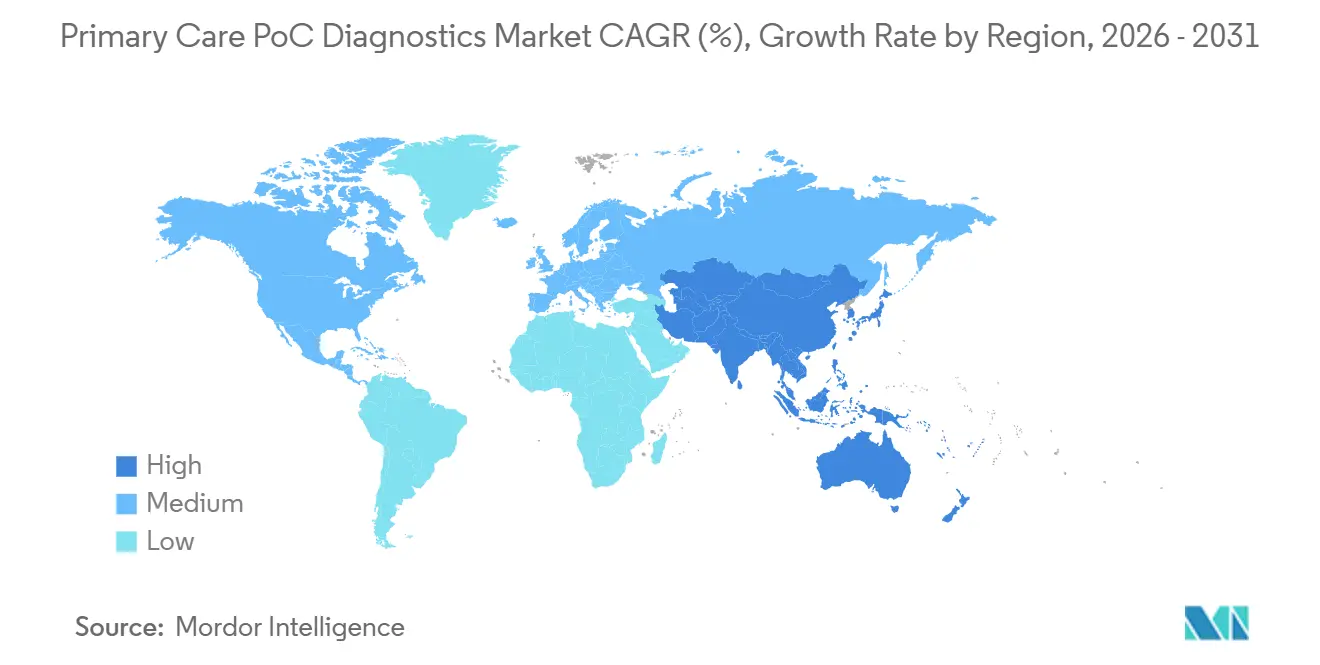

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

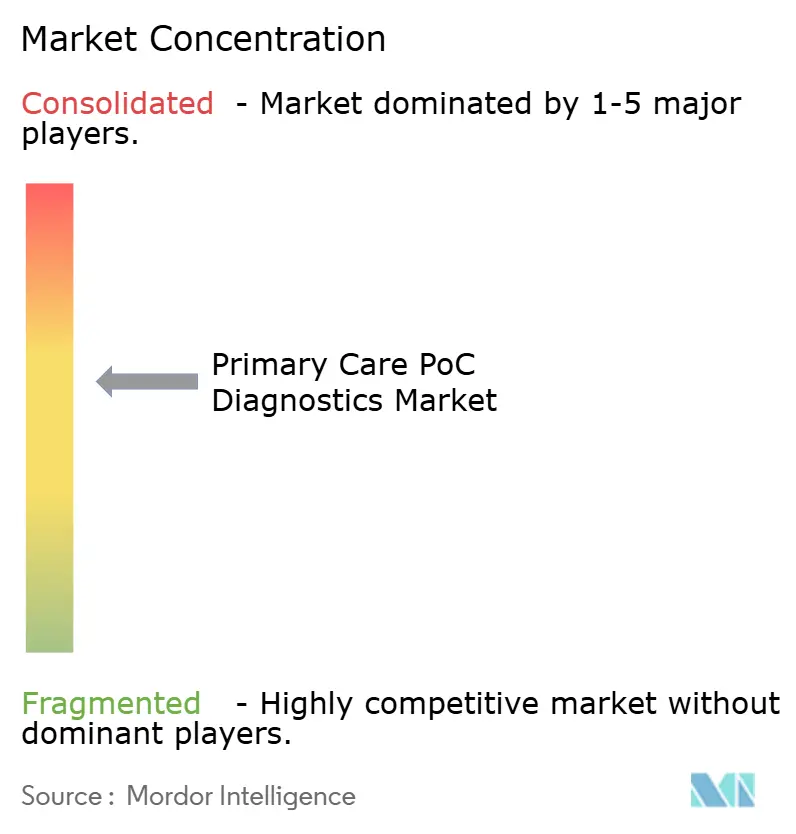

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Primary Care PoC Diagnostics Market Analysis by Mordor Intelligence

The Primary Care PoC Diagnostics Market size is estimated at USD 19.71 billion in 2026, and is expected to reach USD 28.54 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031).

Strong demand for rapid chronic-disease monitoring, infectious-disease triage, and telehealth integration is steering decision makers away from centralized laboratories toward near-patient testing in clinics, pharmacies, and homes. Industry incumbents are layering Bluetooth connectivity and cloud dashboards onto existing cartridge-based systems, which converts one-time device revenue into subscription analytics and elevates lifetime value. Retail-clinic expansion in North America, public-sector subsidies in Asia-Pacific, and relaxed over-the-counter rules for low-risk assays in several high-income nations are broadening patient access. Supply-chain bottlenecks for microfluidic cartridges, cybersecurity compliance costs for connected devices, and lingering clinician concerns about accuracy versus core labs restrain the growth pace yet are not expected to derail the medium-term outlook of the Primary Care PoC Diagnostics market.

Key Report Takeaways

- By product type, glucose monitoring led with a 29.55% revenue share in 2025; pregnancy and fertility tests are forecast to expand at an 8.25% CAGR to 2031.

- By technology platform, lateral-flow assays captured 35.53% of the 2025 Primary Care PoC Diagnostics market share; molecular diagnostics are projected to rise at an 11.85% CAGR through 2031.

- By mode of prescription, prescription-based products held 53.23% of 2025 revenue, while over-the-counter products are set to grow at a 9.15% CAGR to 2031.

- By end user, physician offices commanded 40.25% of 2025 revenue; home healthcare settings are poised to surge at a 13.21% CAGR through 2031.

- By sample type, blood specimens accounted for 65.33% of 2025 test volume; saliva-based tests are forecast to advance at an 11.05% CAGR to 2031.

- By geography, North America generated 42.15% of 2025 revenue, whereas Asia-Pacific is slated to grow at an 12.51% CAGR, the swiftest pace worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Primary Care PoC Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic-disease burden demanding rapid chair-side tests | +1.8% | Global, with highest intensity in North America and Europe | Medium term (2-4 years) |

| Growing incidence of infectious diseases requiring immediate triage | +1.5% | Global, with acute demand in Asia-Pacific and Sub-Saharan Africa | Short term (≤ 2 years) |

| Advances in microfluidics & biosensors enhancing accuracy and ease-of-use | +1.2% | North America, Europe, and Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Shift toward decentralized/retail-clinic care & telehealth models | +1.4% | North America and Europe, with emerging adoption in urban Asia-Pacific | Medium term (2-4 years) |

| AI-powered decision-support embedded in PoC devices boosting reimbursement potential | +1.0% | North America and Europe, where payer infrastructure supports algorithmic billing | Long term (≥ 4 years) |

| Single-use molecular cartridges aimed at outpatient antimicrobial stewardship | +0.8% | Global, with regulatory push in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic-Disease Burden Demanding Rapid Chair-Side Tests

Diabetes, cardiovascular disease, and chronic kidney disease together impact more than 1.5 billion adults, pushing physicians to adopt point-of-care glucose, lipid, and hemoglobin A1c assays that allow medication titration during the visit window. Abbott’s FreeStyle Libre 3 Plus, cleared in January 2025, streams glucose data to smartphones in real time and enables primary-care teams to adjust insulin before the patient leaves the clinic. Dexcom’s over-the-counter Stelo system widened continuous glucose monitoring to adults with Type 2 diabetes not using intensive insulin, a population historically underserved by episodic fingerstick meters[1]U.S. Food and Drug Administration, “FDA Clears First Over-the-Counter Continuous Glucose Monitor,” fda.gov. CMS reimbursement for continuous glucose monitors under Medicare Advantage lowered monthly out-of-pocket costs, accelerating adoption among seniors. Siemens Healthineers added troponin testing to its Atellica VTLi analyzer, delivering cardiac biomarker results in 10 minutes in urgent-care settings and preventing unnecessary emergency referrals. Continuous or on-demand measurement has compressed decision cycles, lowered readmissions, and reinforced the role of the Primary Care PoC Diagnostics market in chronic-disease management.

Growing Incidence of Infectious Diseases Requiring Immediate Triage

Recurring surges in respiratory, sexually transmitted, and vector-borne infections—especially in Asia-Pacific and Sub-Saharan Africa where laboratory infrastructure remains thin—are intensifying demand for in-visit diagnosis. Cepheid’s fingerstick hepatitis C viral-load test produces quantitative results in under 60 minutes and helps harm-reduction clinics initiate antivirals before patients leave. The BioFire Respiratory Panel 2.1 plus detects 23 pathogens from a single swab in roughly 45 minutes, guiding targeted antibiotic or antiviral therapy during the same appointment. CVS Health rolled out a 3-in-1 influenza A/B and SARS-CoV-2 test across 1,600 MinuteClinics, enabling pharmacists to prescribe antivirals on site in 13 states under test-and-treat authority. WHO’s 2024 antimicrobial-resistance guidelines explicitly promote rapid molecular assays in outpatient care, further anchoring infectious-disease panels as a key revenue stream for the Primary Care PoC Diagnostics market.

Advances in Microfluidics and Biosensors Enhancing Accuracy and Ease of Use

Disposable cartridges that embed sample preparation, amplification, and detection now allow unskilled staff to run multi-analyte panels without pipettes or cold-chain reagents. Roche’s cobas pulse handheld PCR unit runs flu, streptococcus, and SARS-CoV-2 assays in roughly 20 minutes, eliminating manual steps that once limited primary-care uptake. Siemens Healthineers’ Vivalytic respiratory panel capitalizes on digital microfluidics to reach ≥95% sensitivity for 22 targets. Abbott’s i-STAT Alinity handheld analyzer performs blood-gas and electrolyte panels in under 2 minutes and streams results to electronic records via Bluetooth. Peer-reviewed data in Clinical Chemistry and Laboratory Medicine confirm that new electrochemical biosensors now hit <3% coefficients of variation, materially closing the accuracy gap versus central laboratories. Together, these engineering leaps make the Primary Care PoC Diagnostics market increasingly competitive with core-lab precision while preserving bedside convenience.

Shift Toward Decentralized Retail-Clinic Care and Telehealth Models

U.S. retail chains operate more than 2,000 walk-in clinics that collectively manage about 5 million patient visits each year, siphoning routine care from time-constrained physicians. CVS Health plans to deepen diagnostic offerings through its Oak Street Health acquisition, while Walgreens Boots Alliance reports double-digit growth from co-located VillageMD practices. CMS interoperability rules finalized in July 2025 mandate real-time exchange of device data, knocking down technical barriers for telehealth platforms to ingest point-of-care results. FDA guidance on digital health technologies clarifies enforcement discretion for devices that merely transmit physiologic data, encouraging start-ups to pair inexpensive hardware with cloud dashboards. These regulatory tailwinds, coupled with consumer preference for shorter wait times, are channeling fresh volume into the Primary Care PoC Diagnostics market across retail clinics, pharmacies, and virtual-first care models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory & reimbursement hurdles | -0.9% | North America and Europe, where premarket approval timelines extend 12-18 months | Medium term (2-4 years) |

| Accuracy-gap concerns vs. central labs | -0.6% | Global, with heightened scrutiny in oncology and transplant monitoring | Long term (≥ 4 years) |

| Microfluidic-cartridge supply-chain fragility in rural clinics | -0.4% | Asia-Pacific, Sub-Saharan Africa, and rural North America | Short term (≤ 2 years) |

| Cyber-security liabilities from connected PoC systems | -0.3% | North America and Europe, where data-breach penalties exceed USD 50 million | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Reimbursement Hurdles

FDA’s April 2024 phase-out of enforcement discretion for laboratory-developed tests now obliges manufacturers to pursue 510(k) or pre-market approval, which lengthens timelines and lifts spending on pivotal trials beyond USD 3 million per submission. QuidelOrtho missed the 2024 flu-season launch window for its next-generation respiratory panel after extended review, trimming quarterly revenue and illustrating how clearance delays translate directly into lost sales. CMS maintains restrictive coverage of certain biomarkers, including point-of-care procalcitonin, forcing U.S. providers to absorb test costs that European peers routinely claim back from single-payer systems. Economic modeling in Health Affairs confirms that smaller innovators struggle to absorb regulatory costs, consolidating advantage among incumbents who operate large in-house clinical-study networks. Until streamlined pathways emerge, regulatory friction will keep a lid on the overall Primary Care PoC Diagnostics market growth rate.

Accuracy-Gap Concerns Vs. Central Labs

High-stakes fields such as oncology and organ-transplant monitoring demand analytical precision that many point-of-care devices still fail to demonstrate under real-world conditions. A 2024 review covering 47 glucose meters showed 22% fell short of ISO 15197 accuracy at extreme hematocrit levels, fueling clinician reluctance. The College of American Pathologists reported 30% higher coefficient of variation for point-of-care INR testing relative to core-lab coagulation analyzers, causing certain cardiology clinics to revert to venipuncture[2]College of American Pathologists, “Proficiency Testing Data 2024,” cap.org. Hologic cited hospital preference for centralized molecular oncology platforms as a headwind in its flat 2024 diagnostics revenue, underscoring market hesitation. NIH is funding multi-center trials that compare bedside troponin assays to high-sensitivity core-lab versions, but published equivalence data remain sparse. Until more rigorous head-to-head studies validate performance, segments of the Primary Care PoC Diagnostics market will face adoption drag in precision-critical disciplines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Glucose Dominance Meets Fertility Acceleration

Continuous glucose monitors secured 29.55% of 2025 revenue, giving glucose the single largest product share within the Primary Care PoC Diagnostics market size for that year. FreeStyle Libre Rio, launched at a 40% lower price point than incumbent systems, expanded access among price-sensitive payers and strengthened Abbott’s grip on follow-up sensor sales. Pregnancy and fertility tests remain a smaller pool today, yet their 8.25% forecast CAGR through 2031 indicates the fastest lane for incremental revenue, powered by connected urine-based ovulation kits that synchronize with mobile apps. Infectious-disease panels hold the second-largest slice of the Primary Care PoC Diagnostics market, riding seasonal surges and public-health investments aimed at reducing antibiotic misuse.

In cardiometabolic care, primary-care physicians increasingly turn to point-of-care troponin and natriuretic peptide assays to rule out acute myocardial events without emergency-department referral, a tactic that protects capacity during seasonal respiratory spikes. Coagulation testing, though mature, retains a loyal clinic base that manages warfarin titration; extended-interval dosing protocols for direct oral anticoagulants temper its medium-term expansion. Hematology analyzers help dialysis centers manage transfusion thresholds, while urinalysis dipsticks remain ubiquitous due to USD 0.50 reagent-strip pricing. Lipid panels face deceleration now that guidelines stretch screening intervals for low-risk adults, although high-risk patients sustain baseline volume. Niche assays—fecal occult blood, group A streptococcus, mononucleosis—populate the “others” category and resist consolidation due to low per-test reimbursements.

By Technology Platform: Lateral Flow Leads, Molecular Surges

Lateral-flow cassettes captured 35.53% of 2025 platform revenue, cementing their role as the workhorse of pregnancy, respiratory-virus, and cardiac-marker testing thanks to ambient stability and low unit cost. QuidelOrtho shipped more than 50 million QuickVue COVID-19 tests to retail outlets in the first half of 2024, underscoring the channel scalability of lateral flow. Molecular diagnostics are slated for an 11.85% CAGR, the strongest among platforms, as cartridge-based PCR and isothermal systems penetrate primary-care offices. Cepheid’s Xpert suite delivers tuberculosis, hepatitis C, and group B streptococcus results in under 60 minutes, giving outpatient clinics access to formerly hospital-only accuracy[3]Danaher, “Cepheid Revenue Highlights,” danaher.com.

Microfluidics sits in third position, embedding sample prep and multiplex detection in palm-sized chips to permit multi-analyte respiratory panels at the bedside. Electrochemical biosensors dominate glucose and lactate surveillance, embodied in Abbott’s i-STAT Alinity analyzer, which pushes electrolyte results to electronic records within 2 minutes. Immunoassays, the legacy giant, hold ground in hormone and cardiac-marker measurement, though sensitivity gains in molecular methods are starting to nibble at their share. Dipsticks remain the baseline for urinalysis, with automated strip readers gaining modest uptake among clinics seeking digital audit trails. Paper-based microfluidics and surface-plasmon platforms stay largely in pilot mode given limited reimbursement visibility.

By Mode of Prescription: OTC Gains as Rx Holds Majority

Prescription products maintained 53.23% of 2025 revenue, highlighting physician dominance over diagnostic ordering in chronic-disease and acute-symptom management. Yet over-the-counter clearances for low-risk assays are widening consumer reach. The FDA authorization of Dexcom’s Stelo OTC continuous glucose monitor in August 2024 opened direct access for an estimated 25 million adults with Type 2 diabetes not on intensive insulin. CVS Health’s 3-in-1 respiratory panel functions within CLIA-waived MinuteClinics, allowing pharmacy technicians to administer tests without an on-site physician.

Cardiometabolic, coagulation, and hematology diagnostics remain largely prescription-driven due to the clinical interpretation layer and follow-up management required, stabilizing the physician channel’s absolute revenue despite falling relative share. Meanwhile, consumers gravitate toward home pregnancy, fertility, HIV, and hepatitis assays, lured by privacy, convenience, and immediate results. This twin-track structure suggests prescription products will remain the revenue anchor of the Primary Care PoC Diagnostics market, yet incremental revenue growth will tilt toward OTC-cleared lines that extend addressable volume outside traditional clinical settings.

By End User: Physician Offices Lead, Home Healthcare Surges

Physician offices generated 40.25% of 2025 sales and continue to dominate the Primary Care PoC Diagnostics market, driven by chronic-disease monitoring that requires longitudinal patient records and follow-up visits. However, home healthcare settings are expected to log a striking 13.21% CAGR through 2031, the fastest of any end user, thanks to Medicare billing codes that pay for device setup, data transmission, and monthly interpretation. Abbott sold USD 10.6 billion of FreeStyle Libre sensors in 2024, attributing growth to Medicare Advantage coverage that cuts consumer copays below USD 40 per month.

Retail clinics and pharmacies sit in the middle ground, benefiting from foot traffic and extended hours; CVS MinuteClinics alone handle about 5 million annual visits. Ambulatory surgery centers, dialysis clinics, and occupational-health offices form the “others” category, each requiring high-frequency testing for specific patient groups, such as hemoglobin in dialysis or urinalysis in pre-employment screening. As remote monitoring platforms mature, home settings will eat into simple follow-up tests, but complex point-of-care panels—respiratory, cardiometabolic, antimicrobial stewardship—should remain anchored in professional environments.

By Sample Type: Blood Prevails, Saliva Climbs

Blood accounted for 65.33% of 2025 specimen volume, reflecting its centrality to glucose, lipid, and cardiac biomarker assays, and anchoring the Primary Care PoC Diagnostics market size for sample-driven kits. Yet saliva-based diagnostics are set to post an 11.05% CAGR, propelled by non-invasive HIV, hepatitis C, cortisol, and testosterone panels that improve screening compliance in pediatrics and geriatrics. OraSure’s OraQuick HIV and hepatitis C oral-fluid tests, now cleared for OTC sale, remove the venipuncture barrier for at-risk populations.

Urine specimens occupy second place, covering pregnancy, drug-of-abuse, and urinary-tract infection diagnostics that remain clinic mainstays due to simplicity and cost. Nasopharyngeal swabs underpin respiratory panels, stool samples power colorectal screening, and sputum aids tuberculosis detection; collectively these “other” specimens fill disease-specific niches but lack volume critical mass. Continuous innovation in saliva collection devices and stabilization buffers is expected to shrink the performance gap with serum, further diversifying specimen options available to primary-care teams.

Geography Analysis

North America produced 42.15% of 2025 revenue, making it the largest territory within the Primary Care PoC Diagnostics market. Retail chains continue to widen primary-care footprints; CVS Health and Walgreens Boots Alliance together invested heavily in clinic build-outs that integrate on-site diagnostics into pharmacy workflows. FDA’s January 2025 AI guidance spurred more than 30 AI-enabled point-of-care clearances in 2024 alone, keeping technology refresh cycles brisk. Payer policies remain supportive, with Medicare reimbursing remote patient monitoring and private insurers matching coverage for competitive parity.

Europe stands as the second-largest region. National health systems prioritize cost-effective screening, creating resilience for lateral-flow and CLIA-waived platforms across community clinics. However, reimbursement variability across member states complicates ROI calculations for high-margin molecular assays. Country-level procurement often forces tiered pricing, pressing multinational suppliers to adopt modular product lines that meet divergent funding thresholds.

Asia-Pacific is forecast to grow at a 12.51% CAGR to 2031, the quickest among regions, buoyed by Chinese, Indian, and Japanese subsidies aimed at rural access and chronic-disease management. China’s Sinocare leverages domestic scale to discount glucose meters by roughly 30% against Western brands, broadening uptake among low-income patients. India’s National Health Mission allocated USD 1.2 billion to equip 150,000 primary health centers with point-of-care devices by 2026. Japan included continuous glucose monitoring under its universal insurance in 2024, giving 7.3 million diabetes patients a new reimbursed option. Middle East and Africa lag due to cartridge supply-chain fragility; ambient-stable lateral-flow kits are prevalent. South America’s trajectory hinges on Brazil and Argentina sustaining public-health budgets that reimburse tuberculosis, HIV, and anemia assays in community clinics.

Competitive Landscape

The Primary Care PoC Diagnostics market is moderately fragmented, yet the five largest suppliers still account for a significant share of global revenue. Abbott, Roche, and Danaher use extensive hospital analyzer footprints to cross-sell cartridge refills, spare parts, and cloud-analytics subscriptions. Roche reported CHF 15.8 billion (USD 17.5 billion) in 2024 diagnostics sales as its cobas platform expanded across midsize hospitals. Abbott’s USD 10.6 billion diagnostics revenue stems largely from its FreeStyle Libre sensor ecosystem, which secures ongoing cash flow through subscription sensors rather than meters alone.

Asia-Pacific challengers such as Sinocare and Wondfo Biotech attack price-sensitive markets with lateral-flow lines priced at a 20%–40% discount versus Western brands. Retail conglomerates are vertically integrating: CVS Health acquired diagnostic kit suppliers for in-house MinuteClinic deployment, while large software firms aggregate data from multiple devices into analytics layers that hospitals buy under subscription. R&D pipelines concentrate on saliva-based endocrine tests and rapid antimicrobial-resistance panels aimed at outpatient stewardship mandates.

Connected devices face rising compliance costs after FDA’s 2024 cybersecurity guidance; Abbott allocated USD 180 million to harden its Libre cloud infrastructure. Larger firms with established quality systems absorb the financial burden more easily than start-ups, widening the capability gap. Meanwhile, smartphone-enabled microscopy and mail-in telehealth services threaten to bypass physical devices entirely, posing a disruptive flank to traditional hardware makers.

Primary Care PoC Diagnostics Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd.

Siemens Healthineers

Danaher Corporation (Beckman Coulter + Cepheid)

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: FDA cleared Roche’s Elecsys pTau181 blood test, the first biomarker indicated for Alzheimer’s assessment in routine primary-care visits.

- October 2025: Co-Diagnostics unveiled a proprietary sample-prep instrument designed to streamline its Co-Dx PCR tuberculosis test, reducing hands-on time in field clinics.

Global Primary Care PoC Diagnostics Market Report Scope

As per the scope of the report, primary care PoC Diagnostics (Point-of-Care Diagnostics) refers to medical testing conducted at or near the site of patient care, typically in a primary care setting, to quickly diagnose health conditions.

The segmentation of the primary care point-of-care (PoC) diagnostics market is categorized by product type, technology platform, mode of prescription, end user, sample type, and geography. By product type, it includes glucose monitoring devices, infectious disease testing kits, cardiometabolic testing tools, coagulation testing instruments, pregnancy & fertility test kits, hematology testing equipment, urinalysis testing kits, lipid testing instruments, and other testing products. By technology platform, it covers lateral flow assay devices, molecular diagnostic tools, microfluidic devices, electrochemical biosensor devices, immunoassay kits, dipstick test kits, and other technology platforms. By mode of prescription, it is divided into prescription-only products and over-the-counter (OTC) products. By end user, it comprises physician's offices, retail clinics & pharmacies, home healthcare settings, and other end users. By sample type, it includes blood samples, urine samples, saliva samples, and other specimen types. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Glucose Monitoring Products |

| Infectious Disease Testing Products |

| Cardiometabolic Testing Products |

| Coagulation Testing Products |

| Pregnancy & Fertility Testing Products |

| Hematology Testing Products |

| Urinalysis Testing Products |

| Lipid Testing Products |

| Others |

| Lateral Flow Assays |

| Molecular Diagnostics |

| Microfluidics |

| Electrochemical Biosensors |

| Immunoassays |

| Dipsticks |

| Others |

| Prescription-based Products |

| OTC Products |

| Physician Offices |

| Retail Clinics & Pharmacies |

| Home Healthcare Settings |

| Others |

| Blood |

| Urine |

| Saliva |

| Other Specimens |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Glucose Monitoring Products | |

| Infectious Disease Testing Products | ||

| Cardiometabolic Testing Products | ||

| Coagulation Testing Products | ||

| Pregnancy & Fertility Testing Products | ||

| Hematology Testing Products | ||

| Urinalysis Testing Products | ||

| Lipid Testing Products | ||

| Others | ||

| By Technology Platform | Lateral Flow Assays | |

| Molecular Diagnostics | ||

| Microfluidics | ||

| Electrochemical Biosensors | ||

| Immunoassays | ||

| Dipsticks | ||

| Others | ||

| By Mode of Prescription | Prescription-based Products | |

| OTC Products | ||

| By End User | Physician Offices | |

| Retail Clinics & Pharmacies | ||

| Home Healthcare Settings | ||

| Others | ||

| By Sample Type | Blood | |

| Urine | ||

| Saliva | ||

| Other Specimens | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Primary Care PoC Diagnostics market today?

The Primary Care PoC Diagnostics market size stands at USD 19.71 billion in 2026 and is projected to reach USD 28.54 billion by 2031.

Which product category dominates revenue?

Continuous glucose monitoring systems hold the largest share, accounting for 29.55% of 2025 revenue.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 12.51% CAGR to 2031, driven by public subsidies and local manufacturing scale.

What end-user segment is growing quickest?

Home healthcare settings lead growth with a 13.21% CAGR, supported by remote patient monitoring reimbursement.

Why are molecular tests gaining ground in primary care?

Cartridge-based PCR systems now deliver hospital-grade accuracy in under an hour, enabling on-site antimicrobial stewardship and rapid triage.

What is the main restraint limiting wider adoption?

Stringent FDA clearance requirements and variable reimbursement policies increase development costs and delay market entry for new devices.

Page last updated on: