Structural Heart Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.07 Billion |

| Market Size (2031) | USD 23.32 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Structural Heart Devices Market Analysis by Mordor Intelligence

The structural heart devices market size in 2026 is estimated at USD 15.07 billion, growing from 2025 value of USD 13.81 billion with 2031 projections showing USD 23.32 billion, growing at 9.11% CAGR over 2026-2031. Robust demand for transcatheter aortic valve replacement (TAVR), wider reimbursement for low-risk patients, and continuous device upgrades lift near-term growth prospects. Product launches that simplify delivery systems, rising procedure volumes in ambulatory surgical centers, and the entry of polymer-free nitinol frames also widen clinical adoption. Competition is sharpening as established suppliers race to expand mitral and tricuspid portfolios, while regional players use price advantages to penetrate emerging Asian markets. Persistent shortages of skilled interventional cardiologists and high capital costs for hybrid cath-lab/OR suites temper the overall trajectory, yet the structural heart devices market remains on a solid expansion path.

Key Report Takeaways

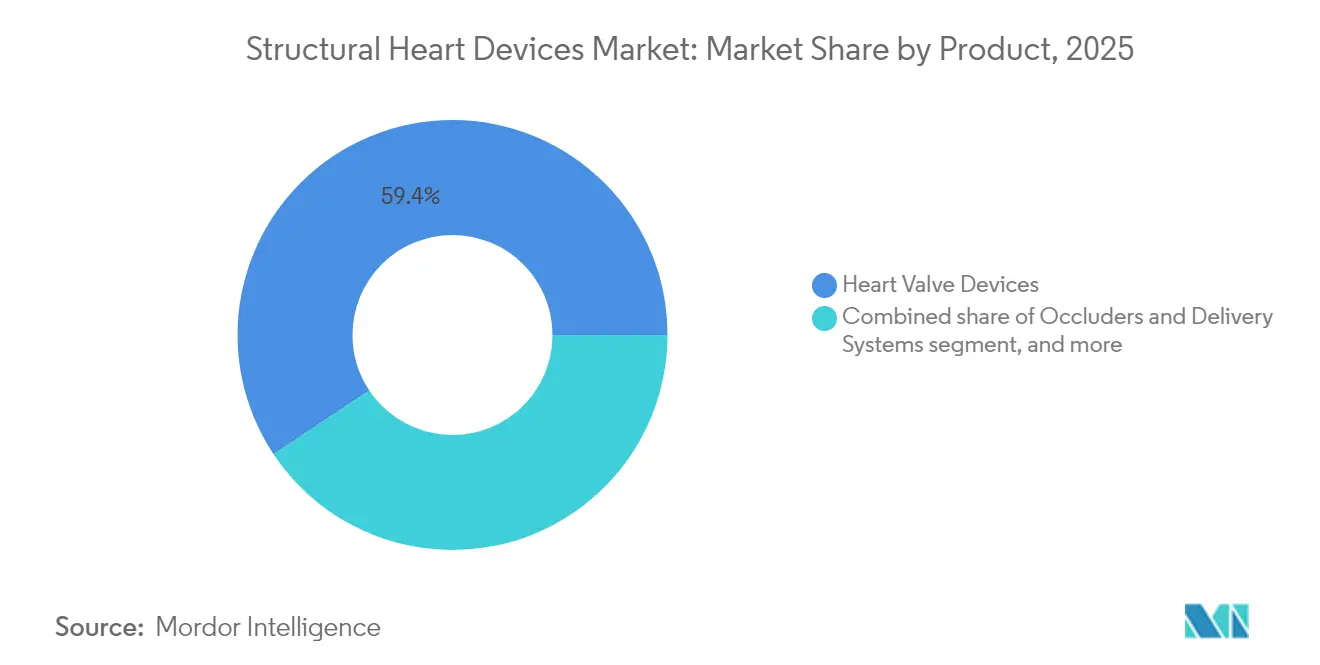

- By product category, heart valve devices led with 59.35% revenue share in 2025, while the “0ther products” segment is advancing at a double-digit CAGR of 12.55% through 2031 as firms diversify beyond valves.

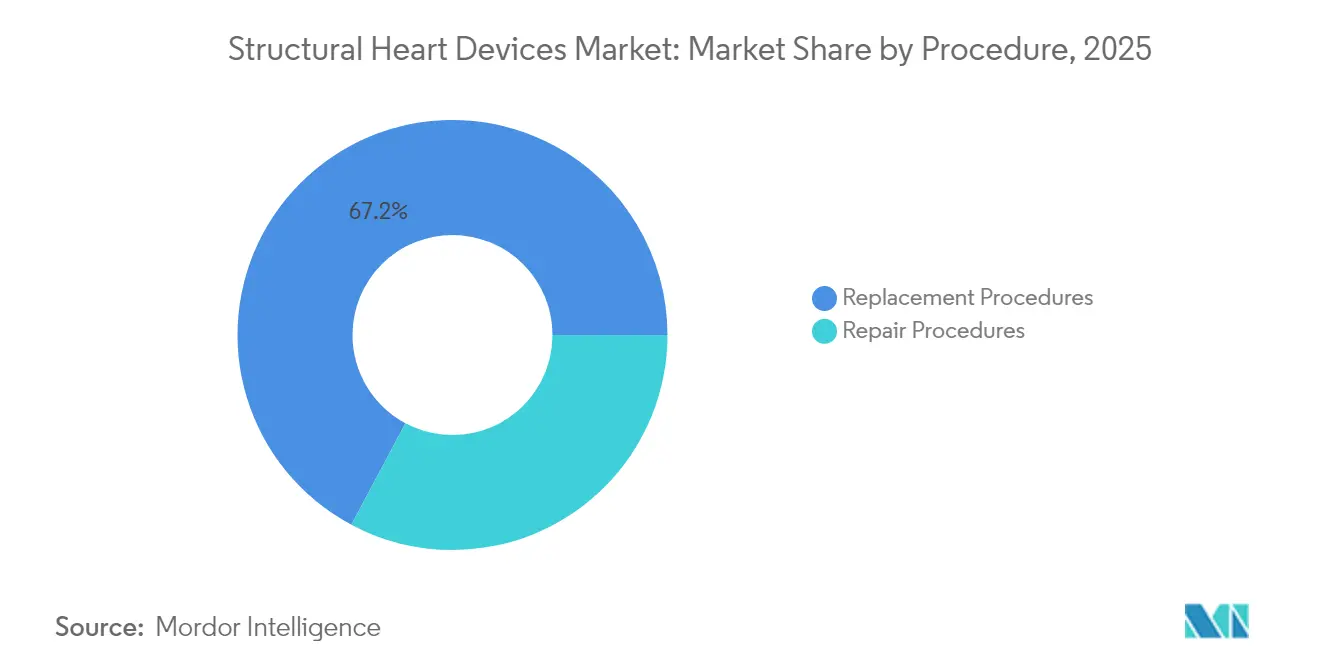

- By procedure, replacement therapies commanded 67.20% of the structural heart devices market share in 2025, whereas transcatheter repair is projected to expand at a 13.95% CAGR to 2031.

- By end user, hospitals and cardiac centers held 82.25% of 2025 revenue, yet ambulatory surgical centers show the fastest growth at 12.32% CAGR on the back of cost savings and same-day discharge models.

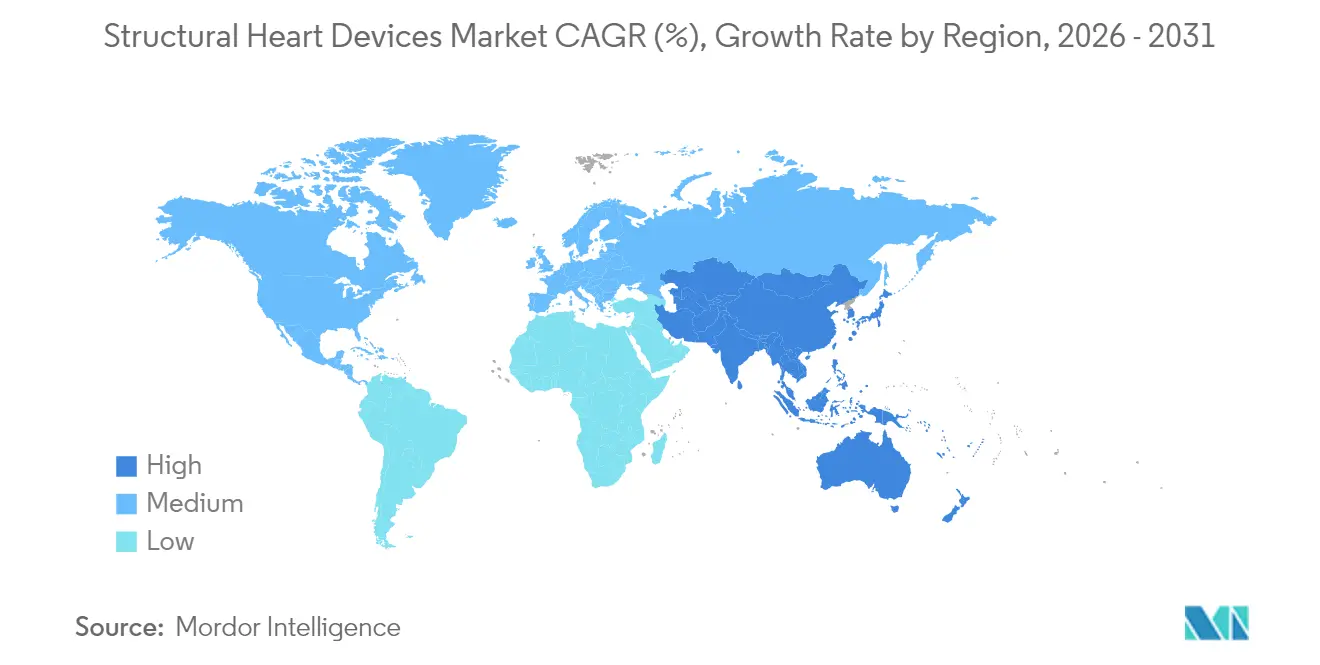

- By geography, North America accounted for 39.45% of 2025 sales, while Asia-Pacific is the fastest-growing region at 10.98% CAGR as procedure volumes rise in India and China.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Structural Heart Devices Market*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of structural heart diseases in aging populations of high-income regions | +2.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Expanding adoption of transcatheter valve therapies in low-risk patient cohorts | +2.1% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Favorable reimbursement expansion for TAVR and TMVr procedures | +1.6% | North America, Europe, select APAC | Medium term (2-4 years) |

| Rapid innovation in next-generation biomaterials and polymer-free nitinol frames | +1.2% | Global | Medium term (2-4 years) |

| Growth of ambulatory cardiac surgery centers enabling same-day discharge | +0.9% | North America, emerging in Europe | Short term (≤ 2 years) |

| Increasing strategic partnerships between device OEMs & AI-enabled imaging firms for pre-op planning | +0.6% | North America, Europe, developed APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Structural Heart Diseases In Aging Populations of High-Income Regions

Longer life expectancy in developed economies has expanded the at-risk pool for calcific aortic stenosis and functional mitral regurgitation. Recent registry updates show escalating procedure volumes in patients aged ≥75 years, reinforcing a long-run demand curve. Early-intervention evidence from the EARLY TAVR trial indicates a 20% reduction in rehospitalizations when asymptomatic severe aortic stenosis is treated before symptom onset, broadening the potential candidate base[1]Edwards Lifesciences, “2024 Annual Report,” edwards.com.

Expanding Adoption of Transcatheter Valve Therapies in Low-Risk Patient Cohorts

Five-year follow-up of low-risk patients confirms comparable all-cause mortality between TAVR and surgery, accelerating payer and clinician confidence[2]John K. Forrest et al., “5-Year Outcomes After Transcatheter or Surgical Aortic Valve Replacement in Low-Risk Patients,” Journal of the American College of Cardiology, jacc.org. Commercial focus has therefore moved to valve durability, paravalvular leak reduction, and hemodynamic performance. Edwards maintains roughly 60% share, Medtronic 28%, and newer entrants such as Abbott are gaining traction with the Navitor system, intensifying differentiation battles.

Favorable Reimbursement Expansion for TAVR And TMVr Procedures

CMS updated its National Coverage Determination to ease data-collection criteria for low-risk TAVR patients, while select European payers now reimburse transcatheter mitral repair outside tertiary centers[3]Centers for Medicare & Medicaid Services, “National Coverage Determination for Transcatheter Aortic Valve Replacement,” cms.gov. Bundled-payment experiments promote efficient device pricing, nudging OEMs toward cost-effective delivery kits and single-use accessory consolidation.

Growth Of Ambulatory Cardiac Surgery Centers Enabling Same-Day Discharge

ASCs handle an increasing mix of left atrial appendage closure and patent foramen ovale repair. Medicare analyses show stroke and mortality below 1% in ASC cohorts, supporting further migration of select valve-in-valve procedures to outpatient settings. Device makers are responding with shorter shaft catheters and simplified sealing mechanisms tailored to resource-constrained facilities.

Increasing Strategic Partnerships Between Device OEMs and AI-Enabled Imaging Firms for Pre-Op Planning

Philips and GE HealthCare have embedded automated 3D quantification into cardiovascular ultrasound, reducing assessment time for tricuspid regurgitation. Improved sizing accuracy limits paravalvular leak, prompting OEMs to bundle imaging analytics with valve systems in value-based contracts.

Restraints Impact Analysis of Structural Heart Devices Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited access to skilled interventional cardiologists in emerging Asia & Africa | −1.8% | Asia-Pacific (excluding Japan, South Korea), Africa, Latin America | Medium term (2-4 years) |

| High up-front capital expenditure for hybrid cath-lab/OR suites constraining smaller hospitals | −1.4% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| Durability concerns & re-intervention needs with certain transcatheter valves | −0.9% | Global | Long term (≥ 4 years) |

| Supply-chain volatility of medical-grade nitinol & PET raising production costs | −0.7% | Global, higher impact on smaller manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Access to Skilled Interventional Cardiologists In Emerging Asia & Africa

Rheumatic heart disease remains common in lower-income parts of Asia and Africa, yet procedure capacity is locked in metropolitan hubs. Complex transcatheter mitral replacement requires extensive proctoring that cannot be scaled quickly. Industry training collaborations are underway, but the supply gap continues to dampen adoption momentum in regions with the highest latent demand.

High Up-Front Capital Expenditure for Hybrid Cath-Lab/Or Suites Constraining Smaller Hospitals

Hospitals face negative contribution margins of roughly USD 3,380 per TAVR episode versus positive margins for surgery, discouraging uptake outside high-volume centers[4]American Heart Association Journals, “Economic Considerations in Access to Transcatheter Aortic Valve Replacement,” ahajournals.org. Financing solutions such as revenue-share models and mobile cath-lab units are emerging, yet progress remains gradual.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Structural Heart Devices Market Segment Analysis

By Product:

Heart Valve Devices Lead as Occluders AccelerateHeart valve devices captured 59.35% of 2025 revenue, confirming their anchor role in the structural heart devices market. TAVR’s worldwide revenue is approaching USD 7.0 billion, supported by 10.0% annual growth in the United States. Valve developers focus on lower profile delivery, anti-calcification leaflets, and commissural alignment technologies that improve long-term durability. The structural heart devices market size for valve platforms is projected to advance in lockstep with the rollout of next-generation systems such as Edwards SAPIEN M3, the first transfemoral mitral replacement to secure a CE Mark in 2025.

Occluders and delivery systems are witnessing rapid procedural expansion, particularly in stroke-prevention applications. Abbott’s WATCHMAN FLX portfolio continues to gain operator confidence due to pivot-ready frames and full-circumference sealing. Sales growth is amplified by favorable outpatient reimbursement, making occluders the quickest expanding sub-category within transcatheter repair solutions. New polymer-free nitinol iterations promise even shorter in-hospital stays, placing additional upward pressure on adoption curves across secondary prevention populations. Collectively, these trends maintain the structural heart devices market on its high-single-digit trajectory.

By Procedure:

Transcatheter Repair Disrupts Replacement DominanceReplacement therapies retained 67.20% share in 2025, helped by robust evidence in low-risk patients and consistent reimbursement across North America and Europe. The structural heart devices market share for TAVR alone is projected to widen further as valve-in-valve and bicuspid approvals unlock new patient cohorts. Edwards estimates 5%-7% TAVR revenue growth for 2025, reaching up to USD 4.4 billion.

Transcatheter repair, steered by clip-based mitral and tricuspid systems, is the structural heart devices market’s fastest-growing procedural class at a 13.95% CAGR. Abbott’s MitraClip generation IV shows reduced residual MR and durable symptomatic relief, underpinning more than 20 supporting trials. FDA clearance of the TriClip and the CE-marked EVOQUE tricuspid valve extend repair technology into previously untreated anatomy, rapidly diversifying manufacturer revenue. This momentum broadens the structural heart devices market size for repair solutions and repositions replacement as one of several viable options rather than the default.

By End User:

Ambulatory Centers Challenge Hospital DominanceHospitals and cardiac centers delivered 82.25% of global procedures in 2025, leveraging critical-care capability for complex multivalve interventions. Institutions with dedicated structural heart programs report procedure volume growth of 84% for TAVR/TEER during the 2020-2024 window, underscoring continued centrality of acute-care settings. Yet fixed-cost intensity fuels consolidation, and hospital operators are preparing for a future in which higher-margin elective work migrates off-campus.

Ambulatory surgical centers captured 17.75% of procedures in 2025 but are expanding at 12.32% CAGR. Medicare data show low adverse-event rates, supporting payer confidence and prompting scheduling shifts toward same-day discharge models. Device firms now tailor valve kits with shorter sheaths and pre-mounted delivery handles that can be deployed without full hybrid OR capability. The result is a structural heart devices market dynamic in which ASCs accelerate competitive pricing pressure while expanding patient access, especially for left atrial appendage and PFO closures.

Geography Analysis

North America Structural Heart Devices Market

North America generated 39.45% of global revenue in 2025, anchored by the United States, which performs more than half of all TAVR implants worldwide and maintains roughly 10.0% annual procedure growth. CMS coverage expansion and ASC penetration underpin continued double-digit growth in transcatheter repair volumes. Canadian reimbursement reforms for mitral clip procedures add incremental upside through 2027.

Europe Structural Heart Devices Market

Europe ranks second in value and adopts new technologies swiftly because of centralized procurement and pan-regional CE approvals. The April 2025 CE Mark of the SAPIEN M3 highlights the region’s role as an early commercialization hub for transfemoral mitral solutions. Hospital networks in Germany and France are broadening clip labs and triaging patients into minimally invasive pathways, helping the structural heart devices market size in Europe maintain mid-single-digit growth despite demographic plateauing.

APAC Structural Heart Devices Market

Asia-Pacific posts the fastest CAGR at 10.98% through 2031 as procedure volumes accelerate in China, Australia, and India. India’s structural heart segment, only USD 12.4 million in 2024, is on track for 31% CAGR, driven by domestic OEMs and tier-two private hospitals expanding cath-lab capacity. Diverse disease profiles create varied clinical priorities, from rheumatic-related mitral repair demand in rural areas to degenerative aortic stenosis in urban centers, requiring differentiated go-to-market strategies. Japan’s aging population continues to underpin steady TAVR growth, while South-Korean tertiary centers pilot AI-guided sizing for mitral interventions.

Regulatory Landscape

Structural heart devices are regulated as high-risk implantables in major markets, requiring robust clinical and manufacturing evidence and post-market surveillance. In the United States, the FDA typically routes transcatheter therapies through the PMA pathway, with 2025 and 2026 approvals reinforcing the pace of label expansion and new-category entry, including Abbott's FDA approval of Tendyne TMVR in May 2025 and Edwards Lifesciences' SAPIEN M3 mitral valve replacement approval in December 2025.

In Europe, structural heart implants fall under Regulation (EU) 2017/745 (MDR), with the MDR transition framework extending across device classes into the December 2027 and December 2028 deadlines. In June 2026, the European Commission published delegated regulations (EU 2026/1451 and EU 2026/1359) expanding exemptions for well-established devices, reducing specific clinical investigation and technical documentation assessment burdens for defined mature categories, influencing portfolio strategy between legacy remediation and faster-cycle updates.

Competitive Landscape

The structural heart devices market shows moderate concentration, with Abbott Laboratories, Medtronic plc, and Edwards Lifesciences Corporation accounting for slightly more than 70.0% of 2024 revenue. Abbott’s structural heart unit posted 22.6% sales growth in Q4 2024, reaching USD 2.25 billion on the back of MitraClip expansions and the Navitor aortic system. Edwards forecasts USD 500–530 million in 2025 TMTT revenue, a 50–60% jump that underscores the strategic pivot toward multivalve portfolios.

Medtronic leverages its CoreValve lineage and Evolut FX platform to capture low-profile implant share, while preparing for future Symphony mitral and Intrepid transcatheter mitral replacement programs. Boston Scientific exited TAVR after withdrawal of Acurate neo2, reallocating capital toward left atrial appendage and stroke-prevention devices.

Midsize suppliers pursue capability gaps through acquisitions. Integer Holdings spent USD 152 million on Precision Coating in 2025 to access surface-coating IP that can reduce leaflet thrombosis. OEMs also sign co-development deals with imaging vendors to lock in AI-driven sizing algorithms, weaving procedural guidance into value propositions. Clinical-evidence arms races remain critical; Abbott runs more than 20 structural heart trials, while Edwards sponsors long-term durability registries to substantiate resin-infused leaflet benefits.

Structural Heart Devices Industry Leaders

Abbott Laboratories

Medtronic plc

Edwards Lifesciences Corporation

Boston Scientific Corporation

LivaNova PLC

- *Disclaimer: Major Players sorted in no particular order

Structural Heart Devices Market Companies Covered in this Report

- Abbott Laboratories

- Medtronic

- Edward Lifesciences

- Boston Scientific

- LivaNova

- Artivion Inc. (CryoLife)

- Lepu Medical

- Venus Medtech

- JenaValve Technology

- MicroPort

- AtriCure

- NuMed

- Kephalios

- Xeltis BV

- 4C Medical Technologies

- HighLife Medical

Market Opportunities and Future Outlook

New approvals and category openings are expanding the addressable opportunity beyond classic aortic stenosis into historically undertreated anatomies and patient subsets. The regulatory actions include Edwards SAPIEN M3 approval in December 2025 for mitral replacement and JenaValve's March 2026 FDA PMA for Trilogy transcatheter heart valve system for symptomatic, severe aortic regurgitation, creating dedicated transcatheter options in segments that previously depended heavily on surgery and off-label approaches. Abbott's May 2025 FDA approval for Tendyne TMVR in severe mitral annular calcification further illustrates the shift toward therapies designed for complex, higher-risk mitral disease.

Procedure-site evolution and workflow tooling create additional whitespace across end users, particularly where outpatient models and simpler cath-lab setups are gaining traction. The market is also being shaped by clinical-evidence and imaging-driven planning needs, with OEMs and imaging platforms pushing automated quantification and sizing to reduce residual regurgitation and paravalvular leak, which supports broader adoption in hospitals and emerging ambulatory pathways. In parallel, Europe-specific MDR changes in June 2026 that broaden exemptions for defined well-established technologies can lower the regulatory friction for certain mature implantable categories, which may free manufacturer capacity to invest in next-generation mitral and tricuspid transcatheter programs and supporting training infrastructure in regions constrained by specialist availability.

Recent Industry Developments in Structural Heart Devices Market

- April 2026: Medtronic announced FDA approval and launched the Mosaic Neo mitral bioprosthesis in the United States. The system is designed for implantation through sternotomy, minimally invasive cardiac surgery, and robotic access, broadening procedure-pathway options for mitral valve replacement programs. It strengthens Medtronic's mitral franchise alongside transcatheter portfolios by aligning product design with less invasive hospital workflows.

- May 2025: Abbott received FDA approval for the Tendyne TMVR system for severe mitral annular calcification, expanding transcatheter options in complex anatomies and placing pressure on competing therapies to demonstrate robust sizing and imaging support.

- March 2024: Medtronic announced FDA approval for the Evolut FX+ TAVR system for symptomatic severe aortic stenosis. Design updates, including larger coronary access windows, address operator needs around coronary access and future interventions in a growing TAVR population. The approval supports platform refresh cycles that can influence hospital standardization and competitive positioning within replacement procedures.

Structural Heart Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers structural heart devices used to repair or replace heart valves and to close cardiac defects through surgical or transcatheter procedures. Revenue is counted for the device systems sold for these interventions across hospitals and cardiac centers.

Scope exclusions: standalone diagnostic imaging platforms, accessory imaging consoles, and ventricular assist or extracorporeal heart-pump systems are not counted in this market sizing.

Segments Covered in This Report

- By Product

- Heart Valve Devices (TAVR, TMVR, Surgical)

- Occluders & Delivery Systems (ASD, VSD, PDA, LAA)

- Annuloplasty & Support Rings

- Other Products

- By Procedure

- Replacement Procedures

- Repair Procedures

- By End User

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped set the clinical and regulatory boundaries and build the first view of procedure volumes, adoption, and pricing movement. We referenced public sources such as the US FDA device databases, the US Centers for Medicare and Medicaid Services coverage and payment files, and the US CDC and WHO cardiovascular disease statistics to understand the treated pool and care pathways.

We also used sources such as OECD health data, national health ministry publications, and peer reviewed cardiology journals to sanity check trends like valve disease prevalence and treatment rates by age group. To translate these demand signals into market value, we complemented them with company filings, investor presentations, reputable press, and paid subscriptions for company financials and patent databases. These inputs were used to track product launches and technology shifts by device category. These examples are not exhaustive, and we also referred to other public and paid sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys focused on cardiologists, interventional teams, hospital procurement stakeholders, and device channel participants, so assumptions from desk research could be tested in real settings. For a global view, we spoke across APAC, EMEA, and the Americas to validate procedure growth, typical device configurations used per case, and how pricing changes show up in contracts and tenders.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | APAC: 37% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 22% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

For sizing, a top-down approach was used where procedure demand is reconstructed from disease prevalence, diagnosis and referral rates, and the share of patients treated with surgical versus transcatheter interventions. Once the expected procedures are built by geography, they are converted into revenue using typical devices per procedure and an average selling price that reflects mix across valve types and closure systems.

To keep the totals practical, we corroborated results with selective bottom-up approximations, such as roll ups of sampled supplier revenues by device category, channel checks on hospital purchasing patterns, and ASP x volume checks for high value procedure types. Inputs in the model include the trend in valvular heart disease burden, growth in TAVR and other minimally invasive procedure volumes, average number of implants per case, reimbursement and coverage expansion signals, and the timing of new product approvals that shift the technology mix.

Forecasts were developed using scenario analysis supported by expert views on how procedure adoption and pricing will move under different reimbursement and capacity conditions. Where bottom-up data was patchy for smaller countries, we used proxy indicators like cath lab expansion and cardiology staffing growth, then adjusted shares after interview validation.

Data Validation & Update Cycle

Validation is handled through multiple checks so the final number is not driven by one assumption. We compare outputs against independent signals like procedure statistics, reimbursement changes, and company reported performance trends, and any sharp variance is reviewed before sign off.

When a material gap appears, analysts re contacted relevant respondents to confirm whether the change is coming from volume, price, or product mix, and then the model is updated with a clear audit trail. The report is refreshed annually, and interim updates are triggered when major approvals, policy shifts, or pricing resets materially alter the demand curve. Before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Structural Heart Devices Market Size Compared Against Other Published Estimates

Published market sizes for structural heart devices often differ because the market boundary and the counting logic can change from one study to another. Differences typically come from what device categories are included, how procedure volumes are derived, and whether pricing is modeled as a stable average or as a fast moving mix shift.

The table shows a spread in 2025 values, and in Mordor Intelligence's model the sizing stays limited to structural heart implants and transcatheter or surgical systems for valve repair or replacement and defect closures, with standalone imaging consoles and ventricular assist or extracorporeal pump systems kept outside the scope. Some published figures appear to add adjacent cardiovascular device revenues or apply higher ASP uplift assumptions without tying them back to procedure level checks, which can move the market total upward. Currency timing and refresh cadence also matter, because newer approval cycles and reimbursement updates can quickly change the volume outlook in fast adopting countries.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.81 B (2025) | |

| Global Consultancy A | USD 18.57 B (2025) | This estimate appears to apply a broader product grouping and a steeper growth and pricing curve for high value transcatheter procedures, with fewer visible exclusions for adjacent cardiovascular device revenue. |

| Industry Publisher B | USD 15.00 B (2025) | This figure looks closer on scope, although differences can come from how delivery systems and accessories are counted and how procedure mix is converted into ASP, especially when country level reimbursement timing is simplified. |

Looking across the three figures, most of the gap is explained by scope edges and by how procedure volume is translated into revenue through mix and pricing. By keeping the model tied to clear procedure drivers and repeatable ASP logic, our estimate remains easier to track and update when approvals, reimbursement, or adoption rates shift.

Key Questions Answered in the Report

What is the current value of the structural heart devices market?

The structural heart devices market size stands at USD 15.07 billion in 2026 and is forecast to reach USD 23.32 billion by 2031.

Which product segment generates the largest revenue?

Heart valve devices dominate with 59.35% of 2025 revenue, underpinned by sustained TAVR growth.

How fast are transcatheter repair procedures growing?

Transcatheter repair, including MitraClip and TriClip, is expanding at a 13.95% CAGR through 2031, making it the fastest-growing procedural class.

Why are ambulatory surgical centers important to future growth?

ASCs provide cost-effective, same-day discharge pathways and are growing at 12.32% CAGR, shifting demand away from traditional hospital settings.

Which region shows the highest growth potential?

Asia-Pacific leads with a 10.98% forecast CAGR, propelled by rising procedure volumes in China and India.

Who are the major players in this market?

Abbott Laboratories, Medtronic plc, Edwards Lifesciences Corporation lead with a combined share above 70.0%, supported by broad portfolios and extensive clinical evidence programs.

Page last updated on: