Congestive Heart Failure (CHF) Treatment Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

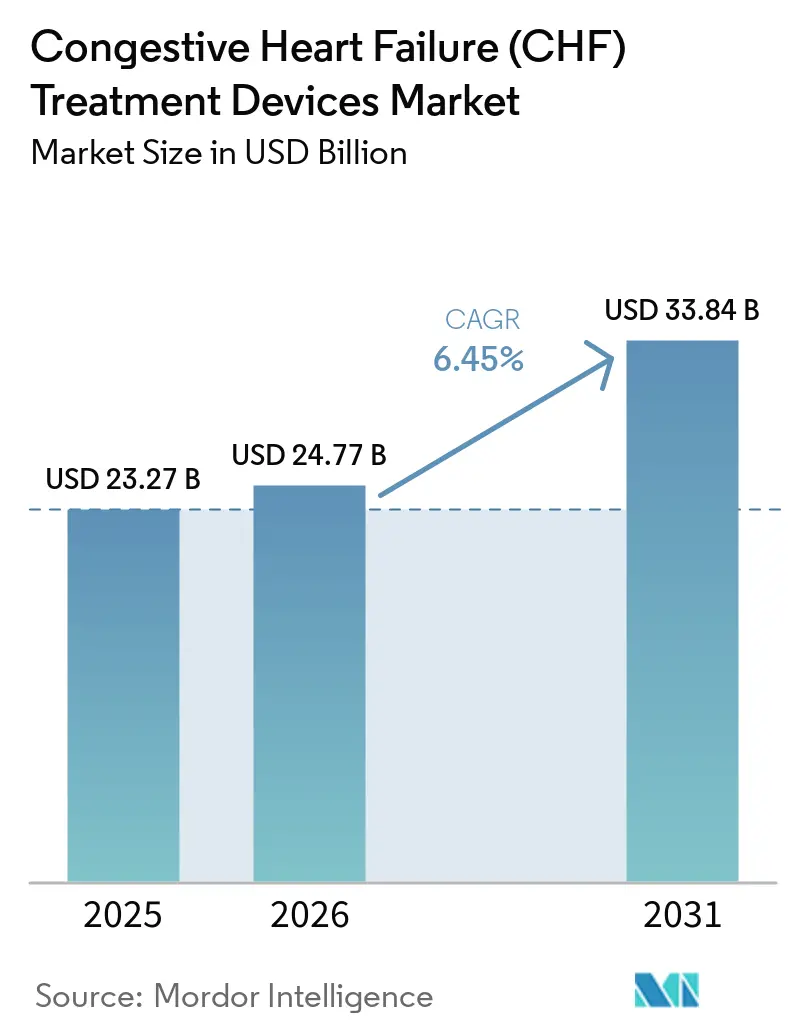

| Market Size (2026) | USD 24.77 Billion |

| Market Size (2031) | USD 33.84 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

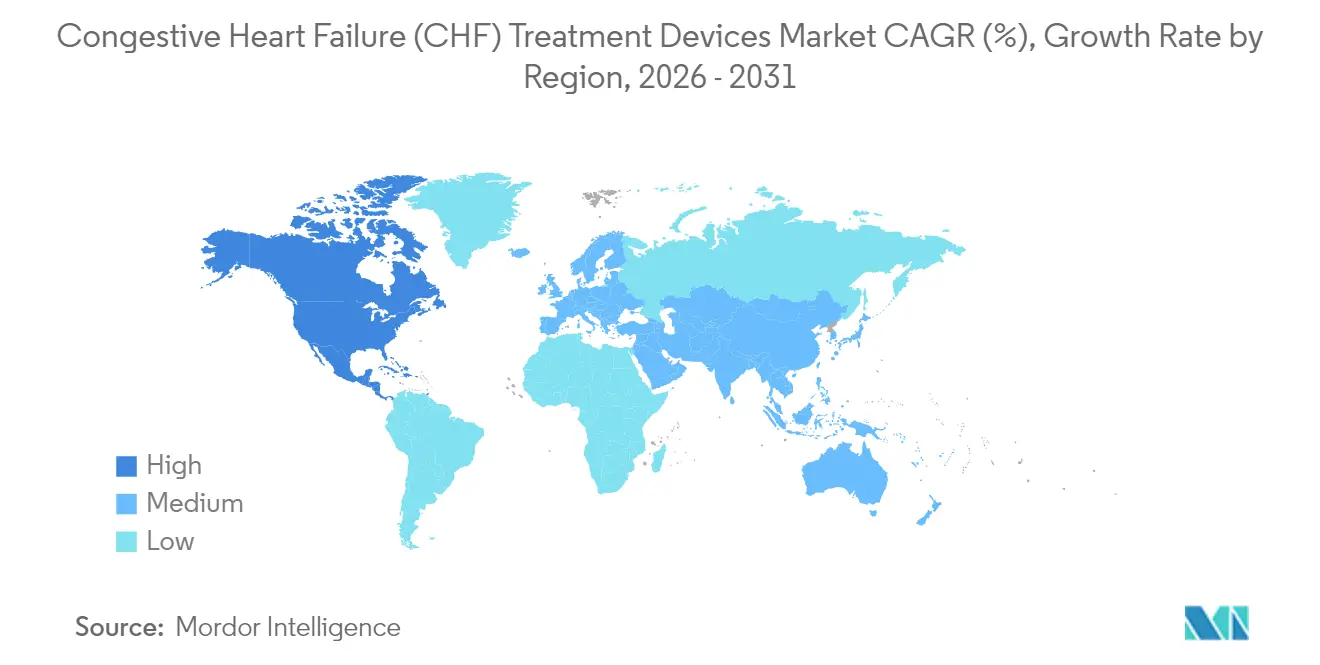

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Congestive Heart Failure (CHF) Treatment Devices Market Analysis by Mordor Intelligence

The congestive heart failure (CHF) treatment devices market size is expected to grow from USD 23.27 billion in 2025 to USD 24.77 billion in 2026 and is forecast to reach USD 33.84 billion by 2031 at 6.45% CAGR over 2026-2031. Sustained demand arises from the convergence of demographic aging, higher chronic heart failure prevalence, and rapid device innovation. Third-generation continuous-flow ventricular assist devices (VADs) are lengthening patient survival while lowering complication rates, and leadless cardiac resynchronization therapy (CRT) systems are opening new therapeutic windows. Reimbursement stability in high-income countries, coupled with frontier research pipelines moving through the U.S. FDA Breakthrough Device Program, is shortening commercialization cycles. Emerging economies are simultaneously modernizing cardiac care infrastructure, shifting device volumes toward Asia-Pacific even as North America maintains value leadership. Competitive momentum is favoring firms that blend mechanical circulatory support portfolios with digital health platforms for remote monitoring.

Key Report Takeaways

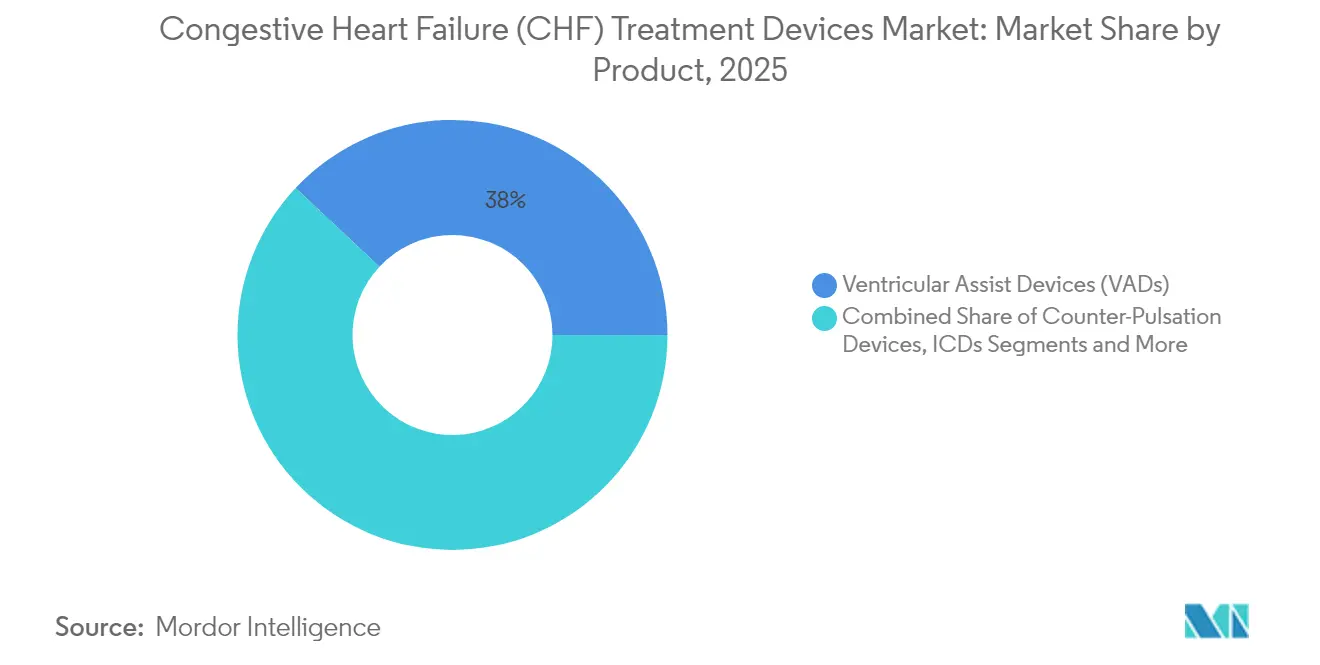

- By product type, ventricular assist devices captured 38.02% of the congestive heart failure (CHF) treatment devices market share in 2025 whereas cardiac resynchronization therapy is advancing at a 7.15% CAGR through 2031.

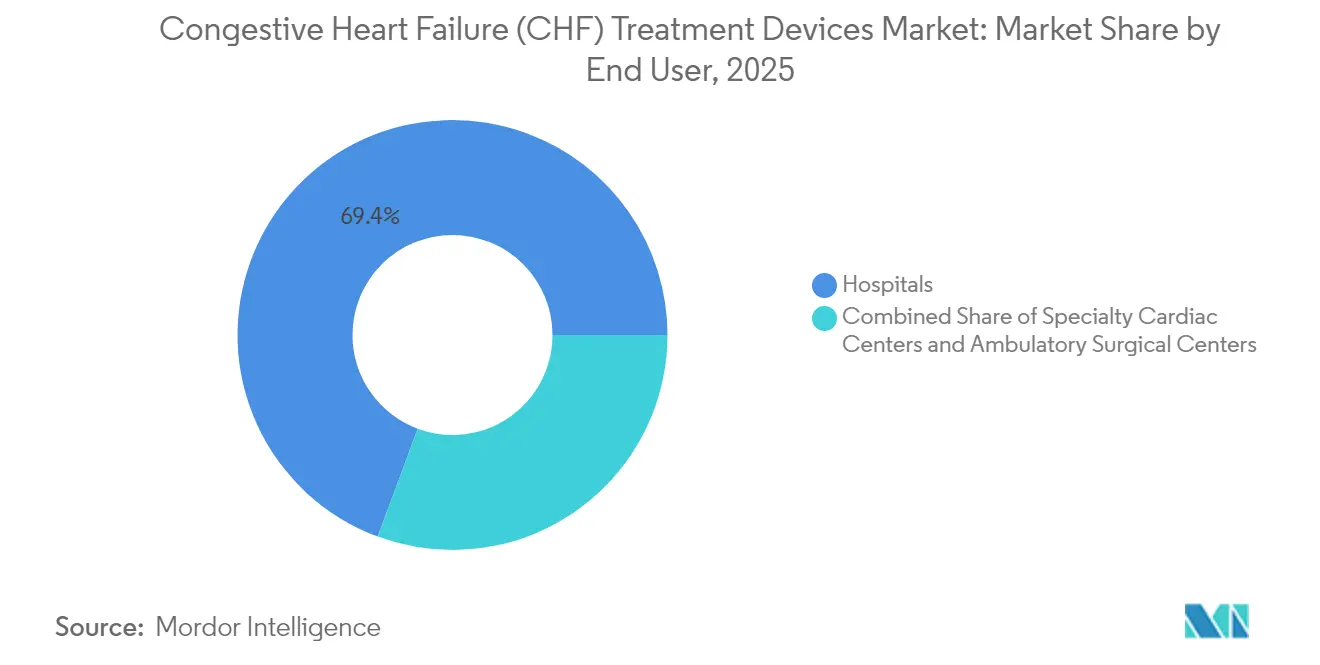

- By end user, hospitals held 69.35% share of the congestive heart failure (CHF) treatment devices market size in 2025. Specialty cardiac centers are projected to expand at a 7.38% CAGR between 2026-2031.

- By geography, North America commanded 43.02% revenue share of the congestive heart failure (CHF) treatment devices market in 2025 whereas Asia-Pacific is forecast to post the fastest 7.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Congestive Heart Failure (CHF) Treatment Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence escalation of CHF & co-morbid CVDs | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Aging population fueling device-eligible patients | +1.0% | North America, Europe | Long term (≥ 4 years) |

| Third-generation continuous-flow LVAD innovations | +0.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Regulatory fast-track for leadless CRT & CCM implants | +0.7% | North America, Europe | Short term (≤ 2 years) |

| AI-based remote monitoring platforms for implanted devices | +0.6% | Global | Medium term (2-4 years) |

| Additive-manufactured pump components lowering custom-build time | +0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence Escalation of CHF & Co-Morbid CVDs

Rising incidence of chronic heart failure is redefining baseline demand for device therapy. U.S. cases are expected to climb to 11.4 million by 2050, up from 6.7 million patients in 2025. Asia mirrors this trajectory; age-standardized prevalence surpassed 722.45 per 100,000 population by 2022. Comorbidity clusters involving diabetes, hypertension, and coronary artery disease are boosting utilization of multi-component solutions such as combined CRT-defibrillator systems. Expanded clinical criteria now allow CRT for ejection fractions up to 45%, enlarging the candidate pool. Payers are responding with value-based pathways that reward reductions in rehospitalization, reinforcing device adoption.

Aging Population Fueling Device-Eligible Patients

Nearly one-quarter of U.S. citizens will be 65 or older by 2060. Geriatric cohorts exhibit higher severity heart failure and lower medical therapy tolerance, prompting earlier consideration of mechanical circulatory support. Destination therapy now represents 73% of VAD implants, a reversal from bridge-to-transplant dominance a decade earlier [1]Duke University Medical Center, “Duke VAD Program Reaches 1,500th Implant Milestone,” dukehealth.org. Miniaturized LVAD pumps and fully percutaneous leadless pacemakers are facilitating procedures in frail patients. Hospitals have started dedicated geriatric cardiac programs to manage peri-operative risks and support post-implant rehabilitation.

Third-Generation Continuous-Flow LVAD Innovations

Magnetically levitated impellers in systems such as HeartMate 3 have lowered pump thrombosis to 2.3% at 2-years versus 8.8% with earlier designs. Superior hemocompatibility translates to longer device life and fewer exchanges, shrinking total cost of ownership despite high upfront pricing. Biventricular concepts like BiVACOR’s Total Artificial Heart extend applicability to patients with bi-ventricular failure and recently secured FDA Breakthrough Device status. Additive manufacturing is enabling bespoke conduits and housings, compressing production timelines and aligning hardware to varied anatomical profiles.

Regulatory Fast-Track for Leadless CRT & CCM Implants

The FDA Breakthrough Device Program had logged 1,041 designations by September 2024, a quarter of which involve cardiac technologies. Abbott’s AVEIR DR dual-chamber leadless pacemaker reached European clearance within 24 months of first-in-human data. Accelerated pathways shorten payback periods for R&D and encourage mid-cap entrants. Contractility modulation devices are similarly benefiting, now indicated for left ventricular ejection fractions between 25-45%, widening therapy windows.

AI-Based Remote Monitoring Platforms for Implanted Devices

Integrating cloud-connected sensors with machine-learning algorithms is transforming post-implant follow-up. Predictive analytics flag deviation in pump speed parameters or thoracic impedance, prompting pre-emptive interventions that reduce heart-failure admissions. Developed markets are piloting reimbursement for remote device checks, furthering clinical acceptance. Vendors are embedding security-hardened firmware to comply with tightening cybersecurity mandates.

Additive-Manufactured Pump Components Lowering Custom-Build Time

Three-dimensional printing is shifting inventory models from stock to order-on-demand for outflow grafts and pump housings. Turnaround can drop from 10 weeks to 14 days, accelerating surgery scheduling and tailoring geometries to complex anatomies. Early adopters in the U.S. and Europe report reduced sterilization waste and better fit, though regulatory validation of printing processes adds cost overhead.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device & procedure costs | -0.9% | Global | Long term (≥ 4 years) |

| Reimbursement gaps in emerging markets | -0.7% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Device-related infection & thrombosis risk | -0.6% | Global | Medium term (2-4 years) |

| Shortage of advanced HF surgeons & VAD coordinators | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device & Procedure Costs

LVAD systems list between USD 150,000-200,000, exclusive of surgery and long-term anticoagulation, pricing out many centers in low-income regions. India’s drug market shows branded-to-generic cost spreads of 3.27 times, implying similar disparities for devices. Payers in developed nations cover implants but balk at funding the specialized staffing models required for continuous ambulatory support. Adoption of bundled payments is slow, leaving hospitals to shoulder capital budgeting risk.

Device-Related Infection & Thrombosis Risk

Despite design progress, driveline infections occur in 10-52% of LVAD recipients while pump thrombosis still affects 10.6%. The ensuing device exchange or intravenous antibiotics raise inpatient costs and deter patient referrals. Abbott’s 2024 HeartMate recall following 70 injuries highlighted lingering safety concerns. Coatings with antimicrobial peptides and automated anticoagulation algorithms are under trial, yet widespread uptake hinges on long-term registry data.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Triumph of VADs and Acceleration of CRT

The ventricular assist device segment retained a 38.02% revenue share in 2025, underscoring its pivotal place in advanced therapy. Continuous-flow systems like HeartMate 3 coupled with total artificial heart concepts are lifting survival rates and widening indication boundaries. Intra-aortic balloon pumps, once ubiquitous, are encountering diminished utility after randomized studies questioned routine deployment in cardiogenic shock.

Cardiac resynchronization therapy is the quickest climber at a 7.15% CAGR to 2031. Regulatory expansion to higher ejection fractions and leadless form factors is propelling penetration. Subcutaneous implantable cardioverter-defibrillators and leadless pacemakers are eroding leads-based device segments through fewer pocket infections and simpler procedures. Artificial intelligence features for automatic vector optimization are further differentiating new CRT models.

By End User: Hospital Dominance and Specialty Center Upswing

Hospitals delivered 69.35% of 2025 revenues on the strength of high-acuity ICUs and cardiac surgery theaters essential for heart failure device implantation. Integration with transplant programs consolidates complex case volumes under one roof. Yet specialty cardiac centers are rising at 7.38% CAGR as procedure complexity and follow-up demands reward concentrated expertise. Dedicated VAD coordinators at such centers improve anticoagulation adherence, cutting driveline infection rates and readmissions. Ambulatory surgical centers, though nascent, benefit from miniaturized CRT implants completed under conscious sedation, signaling further site-of-care migration.

Geography Analysis

North America’s 43.02% congestive heart failure (CHF) treatment devices market share in 2025 stems from Medicare coverage, abundant fellowship-trained surgeons, and 1,041 FDA breakthrough device designations fostering rapid tech turnover. Canada’s single-payer model ensures equitable access, while Mexico’s private insurers target affluent urban populations with CRT and ICD offerings.

Europe follows as a mature adopter anchored by Germany’s high procedural volumes and the EU’s Medical Device Regulation establishing uniform conformity protocols. The United Kingdom’s National Health Service secures population-wide coverage even as post-Brexit supply chains recalibrate. France, Italy, and Spain supplement growth with robust investigator-initiated trials that provide real-world evidence for CRT efficacy.

Asia-Pacific records the fastest 7.99% CAGR to 2031. Japan, facing rapid demographic aging, is a lead adopter of dual-chamber leadless pacemakers. India’s medical device sector targets USD 50 billion size by 2025, and government initiatives are streamlining local manufacturing . South Korea’s national health insurance now reimburses LVAD implants, while Australia offers a developed market entry point for U.S. and European manufacturers.

Competitive Landscape

The congestive heart failure (CHF) treatment devices market is moderately consolidated. Abbott, Medtronic, and Boston Scientific headline value share through broad device franchises and aggressive R&D. Medtronic’s fiscal-year 2025 finish highlighted pipeline momentum in mechanical circulatory support and extracorporeal life support.

Johnson & Johnson’s USD 16.6 billion Abiomed acquisition underscored the strategic importance of mechanical circulatory support niches. Boston Scientific enjoyed 26.2% cardiovascular segment expansion in Q1 2025 on the strength of FARAPULSE pulsed-field ablation plus CRT upgrades.

Nimble innovators are leveraging the Breakthrough Device pathway to punch above their weight. BiVACOR’s magnetically levitated Total Artificial Heart and Magenta Medical’s advanced percutaneous axial pumps illustrate the shift. AI-driven remote monitoring firms partner with OEMs to augment service portfolios, intensifying competition beyond hardware features toward outcome-based ecosystems.

Congestive Heart Failure (CHF) Treatment Devices Industry Leaders

Boston Scientific Corporation

Abbott Laboratories

Biotronik SE & Co. KG

Jarvik Heart Inc.

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BioCardia will seek an FDA meeting to map approval for its CardiAMP autologous cell therapy system for ischemic heart failure.

- July 2025: Restore Medical closed a USD 23 million Series B round co-led by Pitango HealthTech and a global strategic healthcare partner to accelerate transcatheter therapies for heart failure.

- September 2024: Astellas listed DIGITIVA, a Class I software device for non-invasive heart failure management, with the U.S. FDA.

Global Congestive Heart Failure (CHF) Treatment Devices Market Report Scope

As per the scope of the report, congestive heart failure (CHF) is a chronic progressive condition that affects the pumping power of the heart muscle. Left-sided CHF is the most common type of CHF. It occurs when the left ventricle does not properly pump blood out to the body. The Congestive Heart Failure (CHF) Treatment Devices Market is Segmented by Product (Ventricular Assist Devices, Counter Pulsation Devices, Implantable Cardioverter Defibrillators, Pacemakers, and Cardiac Resynchronization Therapy [Cardiac Resynchronization Therapy-Defibrillators (CRT-D) and Cardiac Resynchronization Therapy-Pacemakers (CRT-P)) and Geography (North America, Europe, Asia Pacific, Middle East, and Africa, and South America). The report offers the value (in USD billion) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments. The report offers the value (in USD billion) for the above segments.

| Ventricular Assist Devices (VADs) | LVAD |

| RVAD | |

| BiVAD | |

| Counter-Pulsation Devices | |

| Implantable Cardioverter-Defibrillators (ICD) | Transvenous ICD |

| Subcutaneous ICD | |

| Pacemakers | Implantable |

| External | |

| Cardiac Resynchronization Therapy (CRT) | CRT-D |

| CRT-P |

| Hospitals |

| Specialty Cardiac Centers |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Ventricular Assist Devices (VADs) | LVAD |

| RVAD | ||

| BiVAD | ||

| Counter-Pulsation Devices | ||

| Implantable Cardioverter-Defibrillators (ICD) | Transvenous ICD | |

| Subcutaneous ICD | ||

| Pacemakers | Implantable | |

| External | ||

| Cardiac Resynchronization Therapy (CRT) | CRT-D | |

| CRT-P | ||

| By End-user | Hospitals | |

| Specialty Cardiac Centers | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Congestive Heart Failure (CHF) Treatment Devices Market?

The Congestive Heart Failure (CHF) Treatment Devices Market size is expected to reach USD 24.77 billion in 2026 and grow at a CAGR of 6.45% to reach USD 33.84 billion by 2031.

Which product category currently leads global sales?

Ventricular assist devices led with 38.02% share of 2025 revenues.

Who are the key players in Congestive Heart Failure (CHF) Treatment Devices Market?

Boston Scientific Corporation, Abbott Laboratories, Biotronik SE & Co. KG, Jarvik Heart Inc. and Medtronic PLC are the major companies operating in the Congestive Heart Failure (CHF) Treatment Devices Market.

Which is the fastest growing region in Congestive Heart Failure (CHF) Treatment Devices Market?

Asia-Pacific is expanding at an 7.99% CAGR through 2031 on rising disease prevalence and healthcare modernization.

Which region has the biggest share in Congestive Heart Failure (CHF) Treatment Devices Market?

In 2025, the North America accounts for the largest market share in Congestive Heart Failure (CHF) Treatment Devices Market.

Page last updated on: