U.S. Medical Device Manufacturers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

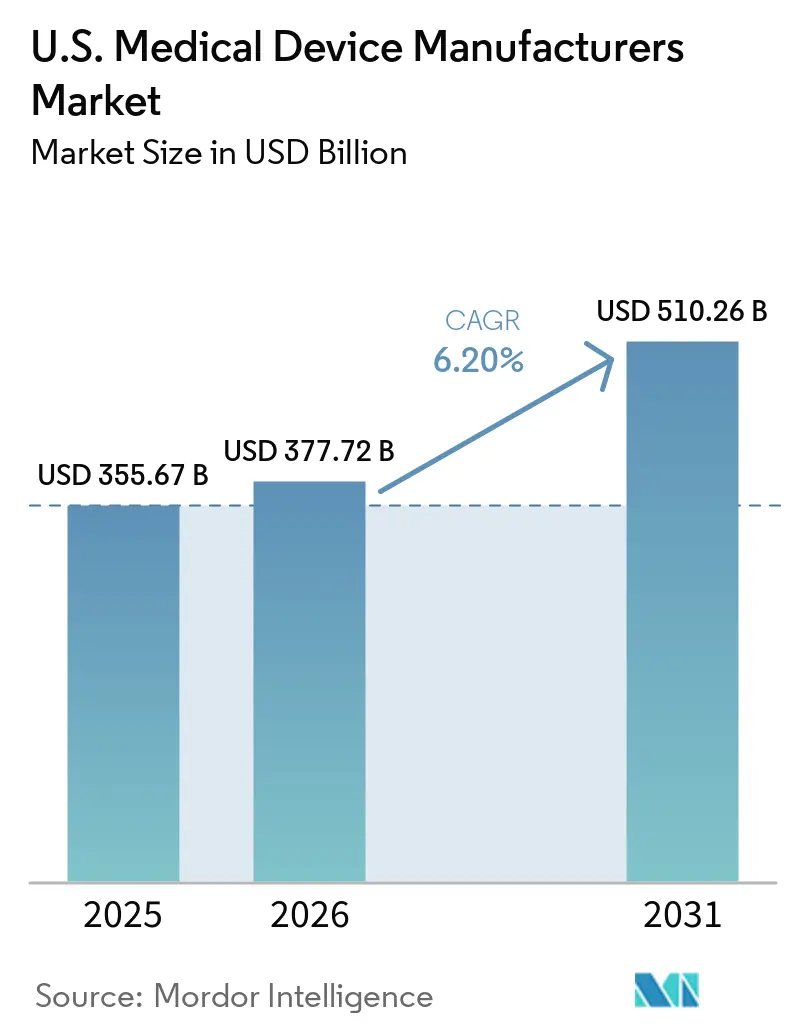

| Base Year Market Size (2025) | USD 355.67 Billion |

| Market Size (2026) | USD 377.72 Billion |

| Market Size (2031) | USD 510.26 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

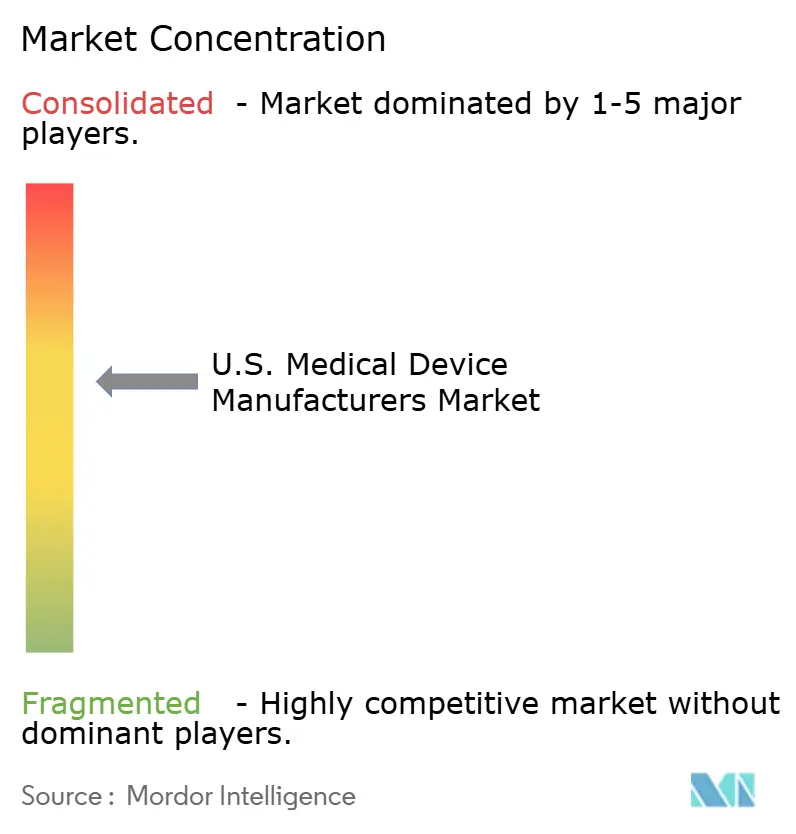

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Medical Device Manufacturers Market Analysis by Mordor Intelligence

The U.S. Medical Device Manufacturers Market size is expected to increase from USD 355.67 billion in 2025 to USD 377.72 billion in 2026 and reach USD 510.26 billion by 2031, growing at a CAGR of 6.20% over 2026-2031.

Medical device manufacturers in the United States are supported by hospital capital refresh programs focusing on imaging, monitoring, IT-linked equipment, and robotics after years of aging infrastructure. Reimbursement changes are driving the adoption of remote patient monitoring and telehealth devices, expanding their use beyond hospital settings. Manufacturers are prioritizing connected systems, workflow efficiency, and compact designs for ambulatory and home use. Larger companies are using acquisitions and platform upgrades to maintain their position in high-growth categories. The market's core demand remains strong, with significant growth in software-linked diagnostics, smart materials, neuromodulation, remote monitoring, and outpatient-focused devices.

Key Report Takeaways

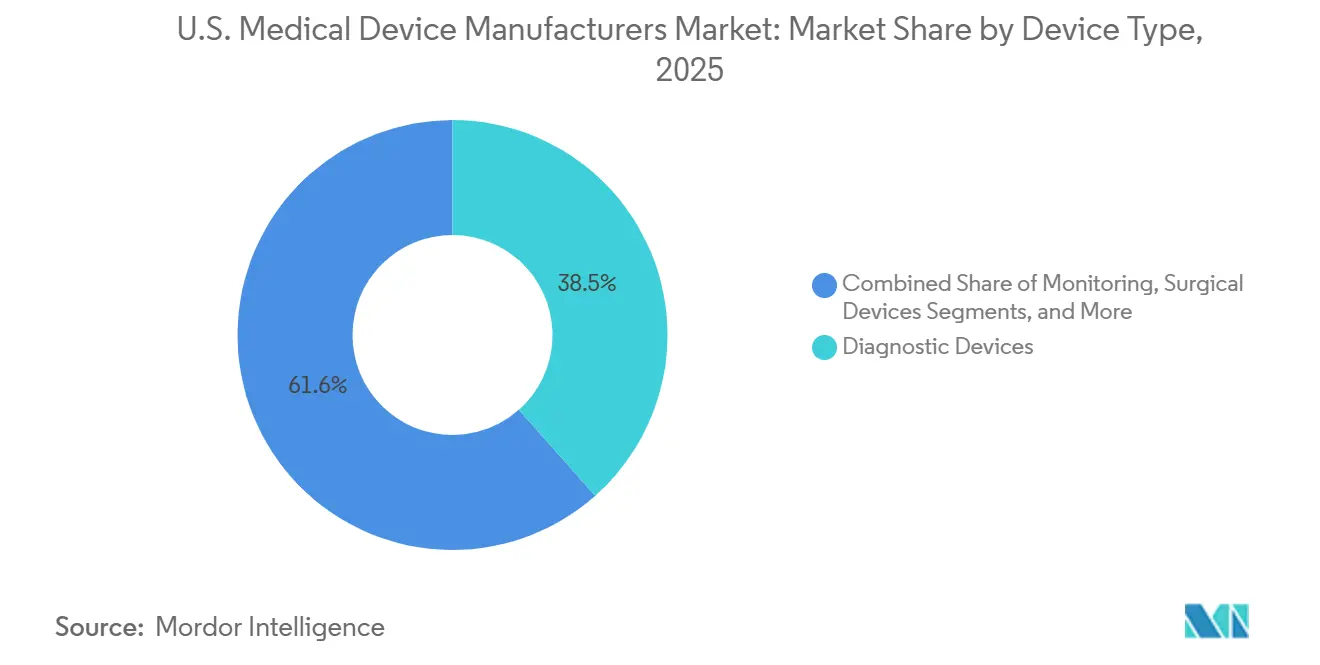

- By device type, diagnostic devices led with 38.45% of U.S. medical device manufacturers' market share in 2025, while monitoring devices are projected to expand at a 7.23% CAGR through 2031.

- By technology platform, conventional electro-mechanical and disposable solutions accounted for 55.9% share of the U.S. medical device manufacturers market size in 2025, while nanotechnology and smart materials are projected to grow at an 8.11% CAGR through 2031.

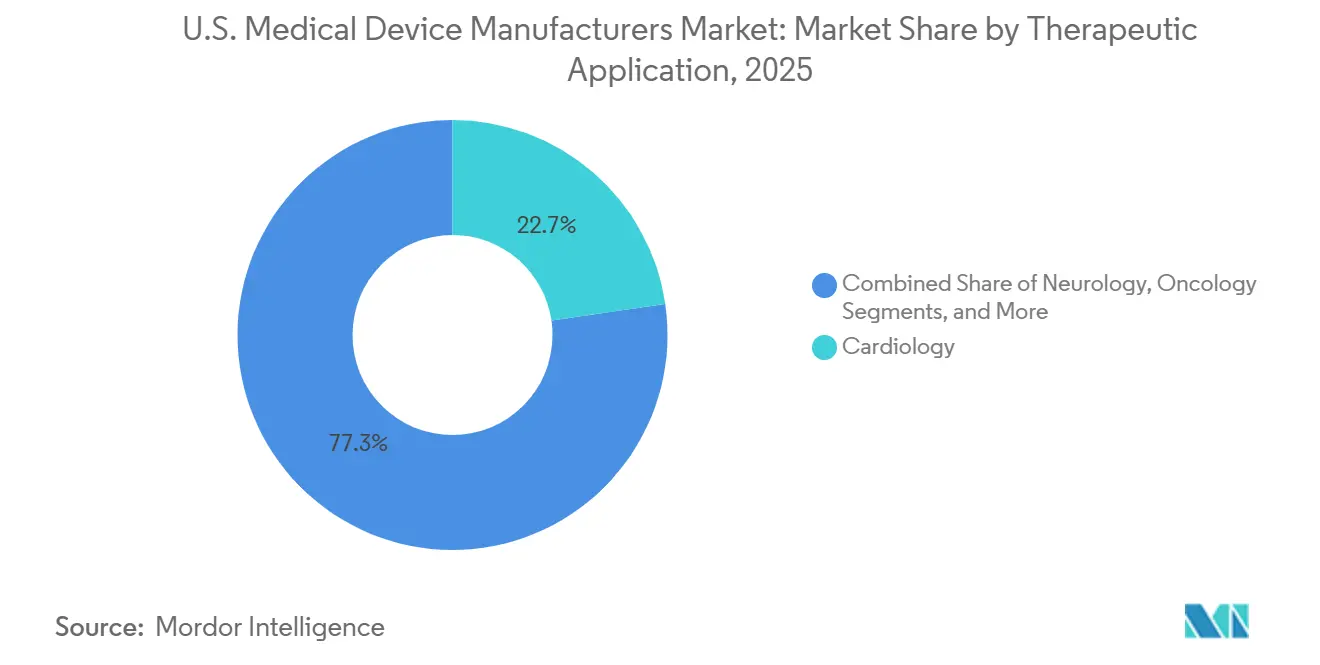

- By therapeutic application, cardiology held 22.70% of the U.S. medical device manufacturers' market share in 2025, while neurology is expected to record the fastest growth at a 7.63% CAGR through 2031.

- By end user, hospitals captured 65.45% share of the U.S. medical device manufacturers market size in 2025, while ambulatory surgery centers will likely post the highest growth at a 7.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Medical Device Manufacturers Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| aging population and chronic disease burden | +1.8% | National, with concentrated intensity in Sun Belt states and Midwest aging corridors | Long term (≥ 4 years) |

| shift toward minimally invasive and image-guided procedures | +1.2% | National, accelerated in urban academic medical centers and high-volume ASC clusters | Medium term (2-4 years) |

| hospital capital refresh for imaging, monitoring, and robotics | +0.9% | National, highest in the Southeast and West Coast where health system consolidation is active | Medium term (2-4 years) |

| expansion of outpatient and home-monitoring pathways | +1.1% | National, with early gains in states that removed certificate-of-need restrictions | Short term (≤ 2 years) |

| CMS pass-through pathway lift for breakthrough devices | +0.6% | National, concentrated in hospital outpatient departments and ASC settings | Medium term (2-4 years) |

| stabilizing EtO sterilization capacity for single-use devices | +0.4% | National supply chain, with operating centers in Illinois, Georgia, and New Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic Disease: Structural Foundation for Demand

The United States medical device manufacturers market benefits from a strong demand base driven by chronic conditions requiring ongoing diagnostics, therapeutic interventions, and monitoring. This demand is particularly significant among older populations managing multiple conditions, increasing the use of imaging, cardiac support devices, orthopedic implants, and monitoring systems. Multimorbid patients necessitate broader procurement, supporting both capital equipment and consumables, while chronic disease care remains less impacted by economic fluctuations compared to elective spending.

Shift Toward Minimally Invasive and Image-Guided Procedures

The shift to robotic-assisted and image-guided procedures is transforming demand across device categories. Hospitals adopting robotic systems have increased minimally invasive surgery rates from 60.5% to 65.8%, expanding procedure mixes. This trend drives demand for energy devices, visualization tools, navigation systems, and intraoperative imaging, while integrated operating room ecosystems enhance throughput and recovery times.[1]Healthcare Financial Management Association, “Hospital Capital Expenditures Aging Facilities,” HFMA, hfma.org Companies offering comprehensive portfolios are better positioned than those with standalone products.

Hospital Capital Refresh for Imaging, Monitoring, and Robotics

The United States medical device manufacturers market is experiencing a robust hospital capital refresh cycle. In FY2024, the average hospital plant age reached 12.7 years, and the capex-to-depreciation ratio rose to 123.4%, reflecting modernization efforts. Investments in imaging, monitoring, and robotics align with facility upgrades and IT modernization. Hospitals are increasingly prioritizing AI-driven tools, with spending intent rising from 19% to 57%, favoring manufacturers offering integrated solutions over standalone equipment.

Expansion of Outpatient and Home-Monitoring Pathways

The United States medical device manufacturers market is shaped by the shift toward outpatient and home care. Medicare payments for remote patient monitoring exceeded USD 500 million in 2024, supported by policy changes in the 2026 physician fee schedule.[2]Centers for Medicare & Medicaid Services, “Telehealth & Remote Monitoring,” Centers for Medicare & Medicaid Services, cms.gov This trend drives demand for compact, easy-to-use devices suited for ambulatory and home settings, accelerating refresh cycles for wearable and wireless formats while increasing the need for connected systems that integrate with clinical workflows.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent FDA evidence, quality, and post-market burden | -1.1% | National, disproportionately affecting smaller manufacturers with limited regulatory infrastructure | Long term (≥ 4 years) |

| Recall, cybersecurity, and remediation costs | -0.7% | National, concentrated in connected device manufacturers with networked hospital deployments | Medium term (2-4 years) |

| Medicare coverage lag after FDA authorization | -0.5% | National, with earliest adoption in health systems with stronger payer leverage | Medium term (2-4 years) |

| QMSR transition compliance burden | -0.4% | National, with smaller and mid-size manufacturers more affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent FDA Evidence, Quality, and Post-Market Burden

Regulatory scrutiny is tightening for medical device manufacturers, with deeper focus on quality systems and supplier controls. In FY2025, 38 out of 44 device warning letters cited Part 820, and over 100 QMSR inspections were conducted within 75 days of the February 2026 effective date. This increases fixed costs for smaller manufacturers, requiring investments in risk files, CAPA systems, and ongoing surveillance.[3]Centers for Medicare & Medicaid Services, “CMS and FDA Announce RAPID Coverage Pathway to Accelerate Patient Access to Life-Changing Medical Devices,” Centers for Medicare & Medicaid Services, cms.gov Larger firms in the United States medical device manufacturers market are better positioned to use compliance as a competitive advantage, while smaller players face challenges balancing growth and regulatory readiness.

Recall, Cybersecurity, and Remediation Costs

Cybersecurity has become a critical operational risk for connected device manufacturers, alongside product quality. In June 2025, the FDA mandated cybersecurity documentation for devices in the 510(k) pathway, including software and vulnerability details. Failures, such as Abiomed's October 2025 correction for network vulnerabilities, highlight the costs of non-compliance. Hospitals now prioritize vendors with robust lifecycle security management and support practices. The United States medical device manufacturers market increasingly favors companies integrating cybersecurity into design and post-market services rather than treating it as a compliance afterthought.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Devices Outpace as Diagnostics Anchor Revenue

In 2025, Diagnostic Devices accounted for 38.45% of the United States medical device manufacturers market, driven by consistent imaging demand, in-vitro diagnostics, and image-guided workflows in hospitals and outpatient centers. These systems are integral to care pathways in cardiology, oncology, neurology, and routine monitoring, with procurement influenced by throughput, workflow efficiency, and software integration.

Monitoring Devices are projected to grow at a 7.23% CAGR from 2026 to 2031, making them the fastest-growing segment in the United States medical device market. Growth is fueled by remote patient monitoring adoption, expanded use in ambulatory settings, and the shift toward wireless, compact systems like Sibel Health's ANNE Maternal platform.

By Technology Platform: Conventional Backbone Persists as Nanotechnology Accelerates

In 2025, Conventional Electro-mechanical and Disposable platforms represented 55.9% of the technology mix in the United States medical device market, reflecting reliance on high-volume consumables and standard equipment. This segment thrives on volume, reliability, and uninterrupted supply, as seen in BD's investment in U.S. manufacturing and expansion of its Nebraska syringe plant.

Nanotechnology and Smart Materials are expected to grow at an 8.11% CAGR from 2026 to 2031, driven by a shift from passive devices to systems enhancing precision and reducing tissue burden. Innovations in responsive systems and material-enabled performance are advancing beyond concept stages, supported by commercial precedents.

By Therapeutic Application: Cardiology Anchors Share as Neurology Leads Growth

Cardiology held a 22.70% share in 2025, maintaining its lead in the United States medical device market due to structural heart procedures, electrophysiology, and coronary imaging. Sustained demand is driven by high disease prevalence and hospital investments, with advancements like Abbott's AI-powered Ultreon 3.0 enhancing procedural capabilities.

Neurology is forecast to grow at a 7.63% CAGR from 2026 to 2031, making it the fastest-growing therapeutic application. Growth is supported by neuromodulation, stroke interventions, and AI integration in care pathways, alongside an aging population driving demand for neurological and stroke-related treatments.

By End User: Hospitals Dominate as ASCs Capture Complexity

Hospitals accounted for 65.45% of end-user demand in 2025, dominating the United States medical device market due to high-acuity procedures, intensive monitoring, and capital-heavy equipment needs. Investments in imaging systems, robotics, and connected infrastructure reinforce hospitals as key launch environments for premium devices.

Ambulatory Surgery Centers are projected to grow at a 7.67% CAGR from 2026 to 2031, driven by the migration of procedures to cost-effective sites and device redesign for compactness and efficiency. This shift compels manufacturers to adapt product packaging, service models, and disposable strategies for these settings.

Geography Analysis

By 2026, the United States medical device manufacturers market is expected to reach USD 377.72 billion. While national regulations under FDA and CMS provide a unified policy framework, regional variations exist in manufacturing density, clinical capabilities, and procedural intensity. Key clusters in Minnesota, Massachusetts, California, and the Southeast drive innovation and scaled production, combining original equipment manufacturers, suppliers, and specialized talent.

Minnesota plays a critical role in cardiac and neurological devices due to its strong corporate base and supplier ecosystem. The Boston area focuses on women's health, interventional, and digital health, fostering early adoption and advanced product development. California leads in robotic surgery, structural heart, continuous monitoring, and software-linked devices, particularly in the Bay Area and Southern California. The Southeast excels in contract manufacturing, sterilization, and logistics, making the United States medical device market both regionally specialized and nationally interconnected.

Competitive Landscape

The United States medical device manufacturers market is primarily dominated by large, diversified companies, though many high-growth categories remain fragmented. Key players like Medtronic, Abbott, Boston Scientific, Stryker, and Becton, Dickinson and Company hold significant revenue shares in core device categories but face competition from specialists excelling in AI diagnostics, neuromodulation, and connected monitoring. Larger firms leverage established distribution networks and regulatory expertise, while smaller companies excel in agility within emerging categories, creating a dynamic competitive landscape.

Strategic positioning is increasingly influenced by software ecosystems and AI advancements. Stryker's SmartHospital platform, focusing on virtual care and workflow automation, exemplifies efforts to integrate devices with hospital operations. Similarly, Abbott's Ultreon 3.0 clearance highlights the use of AI to enhance decision-making without disrupting workflows. Specialist companies, such as Aidoc with its FDA-cleared AI foundation model, continue to create competitive opportunities. Despite strong incumbents, the market offers growth potential in pediatric AI devices, adaptive neuromodulation, and closed-loop wearable systems.

U.S. Medical Device Manufacturers Industry Leaders

Johnson & Johnson

Medtronic plc

Stryker Corporation

Baxter

Boston Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Medtronic acquired SPR Therapeutics for approximately USD 650 million in cash, adding the FDA-cleared SPRINT peripheral nerve stimulation system for chronic pain to its neuromodulation portfolio. This marked its third major acquisition in 2026, bringing its disclosed deal value above USD 1.785 billion year-to-date.

- April 2026: Medtronic completed the acquisition of CathWorks for USD 585 million, integrating the AI-powered FFRangio coronary physiology system into its interventional cardiology portfolio.

- April 2026: Abbott received FDA clearance for the Ultreon 3.0 AI-powered OCT coronary imaging platform, enabling real-time plaque characterization with a 1-second pullback, benefiting PCI patients with kidney disease requiring low-contrast procedures.

- March 2026: MiniMed received FDA clearance for the MiniMed Flex insulin pump, which was approximately 50% smaller than its predecessor and the first to feature smartphone control, following its Nasdaq IPO.

U.S. Medical Device Manufacturers Market Report Scope

As per the scope of the report, a medical device is any instrument, machine, implant, software, or material intended for use in the diagnosis, prevention, treatment, or monitoring of diseases or injuries. Crucially, these tools do not achieve their primary purpose through chemical, metabolic, or immunological means inside or on the human body.

The U.S. medical device manufacturers market is segmented by device type, technology platform, therapeutic application, and end-user. By device type, the market includes diagnostic devices (diagnostic imaging devices such as MRI systems, CT scanners, and ultrasound, and in-vitro diagnostics), therapeutic devices (implants, drug-delivery pumps, surgical devices including robotics & navigation and energy-based devices), and monitoring devices (multiparameter monitors, remote patient monitors, and others). By technology platform, the market is segmented into conventional electro-mechanical & disposable, wearable & remote monitoring, telehealth & mHealth, robotic surgery, 3-D printing, augmented/virtual reality, nanotechnology & smart materials, and AI-as-a-Medical-Device (SaMD). By therapeutic application, the market is categorized into cardiology, orthopedics & sports medicine, neurology, ophthalmology, general & laparoscopic surgery, oncology, and others. By end-user, the market is segmented into hospitals, ambulatory surgery centers, physician offices and specialty clinics, diagnostic laboratories and imaging centers, home care and remote monitoring settings, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Diagnostic Devices | Diagnostic Imaging Devices | MRI Systems |

| CT Scanners | ||

| Ultrasound | ||

| In-Vitro Diagnostics | ||

| Therapeutic Devices | Implants | |

| Drug-Delivery Pumps | ||

| Surgical Devices | Robotics & Navigation | |

| Energy-based Devices | ||

| Monitoring Devices | Multiparameter Monitors | |

| Remote Patient Monitors | ||

| Others |

| Conventional Electro-mechanical & Disposable |

| Wearable & Remote Monitoring |

| Telehealth & mHealth |

| Robotic Surgery |

| 3-D Printing |

| Augmented / Virtual Reality |

| Nanotechnology & Smart Materials |

| AI-as-a-Medical-Device (SaMD) |

| Cardiology |

| Orthopedics & Sports Medicine |

| Neurology |

| Ophthalmology |

| General & Laparoscopic Surgery |

| Oncology |

| Others |

| Hospitals |

| Ambulatory Surgery Centers |

| Physician Offices and Specialty Clinics |

| Diagnostic Laboratories and Imaging Centers |

| Home Care and Remote Monitoring Settings |

| Others |

| By Device Type | Diagnostic Devices | Diagnostic Imaging Devices | MRI Systems |

| CT Scanners | |||

| Ultrasound | |||

| In-Vitro Diagnostics | |||

| Therapeutic Devices | Implants | ||

| Drug-Delivery Pumps | |||

| Surgical Devices | Robotics & Navigation | ||

| Energy-based Devices | |||

| Monitoring Devices | Multiparameter Monitors | ||

| Remote Patient Monitors | |||

| Others | |||

| By Technology Platform | Conventional Electro-mechanical & Disposable | ||

| Wearable & Remote Monitoring | |||

| Telehealth & mHealth | |||

| Robotic Surgery | |||

| 3-D Printing | |||

| Augmented / Virtual Reality | |||

| Nanotechnology & Smart Materials | |||

| AI-as-a-Medical-Device (SaMD) | |||

| By Therapeutic Application | Cardiology | ||

| Orthopedics & Sports Medicine | |||

| Neurology | |||

| Ophthalmology | |||

| General & Laparoscopic Surgery | |||

| Oncology | |||

| Others | |||

| By End User | Hospitals | ||

| Ambulatory Surgery Centers | |||

| Physician Offices and Specialty Clinics | |||

| Diagnostic Laboratories and Imaging Centers | |||

| Home Care and Remote Monitoring Settings | |||

| Others | |||

Key Questions Answered in the Report

What is the 2031 outlook for U.S. medical device manufacturers?

The sector is forecast to reach USD 510.26 billion by 2031 from USD 377.72 billion in 2026, growing at a 6.20% CAGR over 2026-2031.

Which device category leads revenue in the United States?

Diagnostic Devices held the largest share at 38.45% in 2025 because imaging and in-vitro diagnostics remain central to hospital and outpatient workflows.

Which segment is growing fastest through 2031?

Monitoring Devices is projected to post the fastest device-type growth at a 7.23% CAGR, supported by remote patient monitoring and wider home-based care use.

Why are hospitals still the main buyers of medical devices?

Hospitals held 65.45% of end-user demand in 2025 because they concentrate high-acuity procedures, complex monitoring, and capital-intensive equipment purchases.

What is driving growth in outpatient device demand?

ASCs are expected to grow at a 7.67% CAGR as more procedures move to lower-cost settings and manufacturers adapt devices for smaller footprints and easier deployment.

How are large companies defending their positions in this sector?

Leading companies are using focused acquisitions, AI-linked product upgrades, and software ecosystems, with Medtronic's 2026 deal activity and Abbott's Ultreon 3.0 clearance standing out.

Page last updated on: