Underwater/Marine IoT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

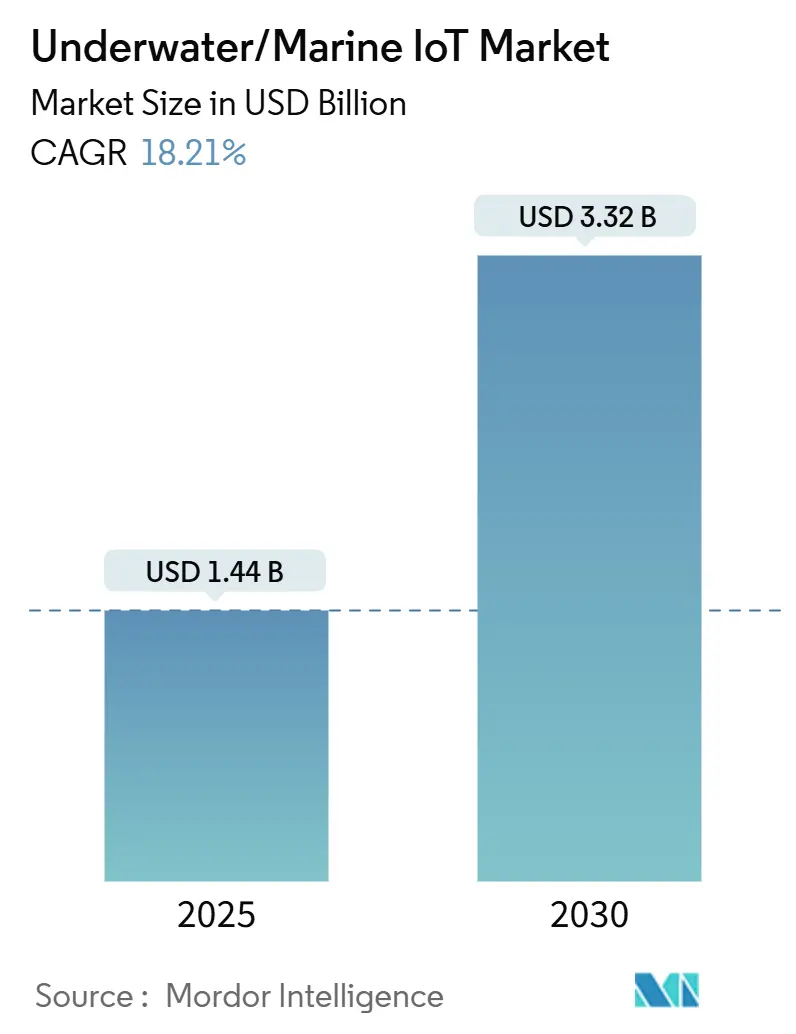

| Market Size (2025) | USD 1.44 Billion |

| Market Size (2030) | USD 3.32 Billion |

| Growth Rate (2025 - 2030) | 18.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underwater/Marine IoT Market Analysis by Mordor Intelligence

The underwater/marine IoT market size stands at USD 1.44 billion in 2025 and is forecast to reach USD 3.32 billion by 2030, registering an 18.21% CAGR over 2025-2030. Rising defense spending, expanding offshore renewable energy assets, and stricter marine-environment rules are accelerating deployments as users look for real-time visibility across wide ocean areas. Defense agencies are fielding secure sensor grids for contested waters, while offshore wind developers connect foundation, cable, and wildlife monitors to optimize uptime. Falling prices for acoustic modems and multi-parameter sensors are widening commercial adoption, and AI-enabled hybrid acoustic-optical networks are easing long-standing bandwidth limits. At the same time, operators increasingly outsource complex data analytics, pushing a services pivot inside the underwater/marine IoT market.

Key Report Takeaways

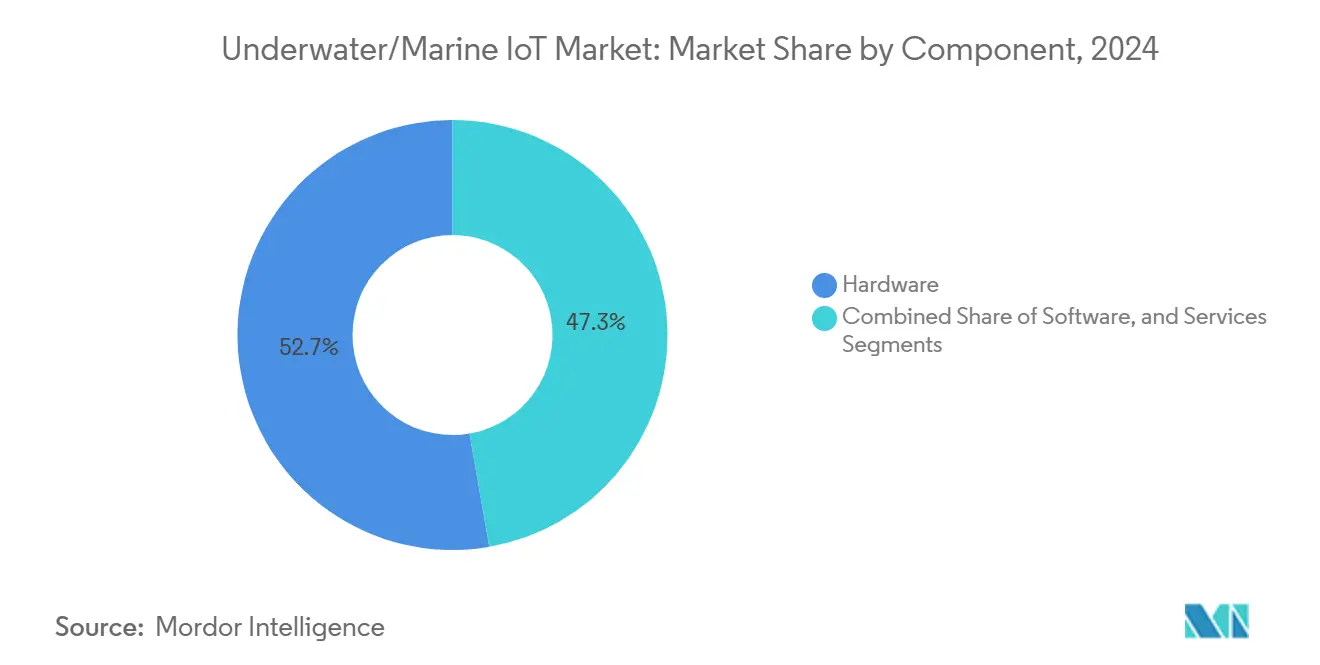

- By component, hardware led with 52.73% of the underwater/marine IoT market share in 2024, while services are projected to advance at a 19.77% CAGR through 2030.

- By communication technology, acoustic systems accounted for 61.83% of the underwater/marine IoT market share in 2024, and hybrid acoustic-optical platforms are expanding at a 20.32% CAGR to 2030.

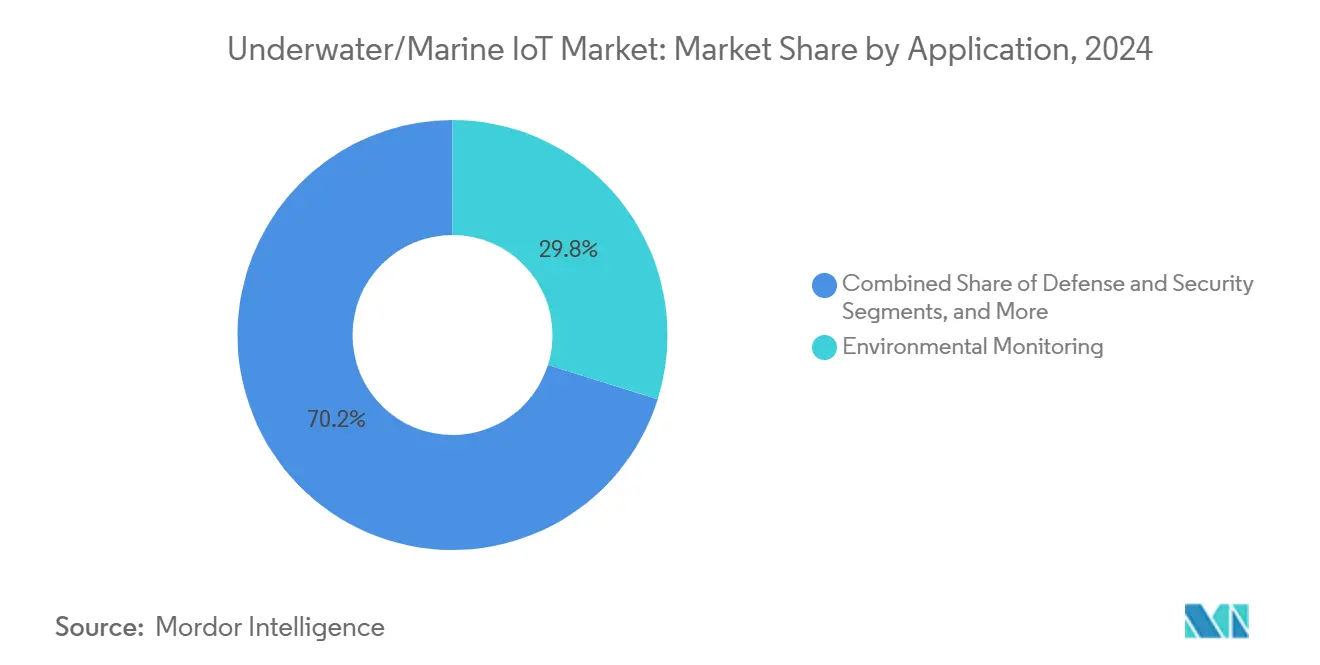

- By application, environmental monitoring captured 29.83% of the underwater/marine IoT market share in 2024; aquaculture and fisheries are growing fastest at 18.77% CAGR through 2030.

- By end-user, government and research agencies held 38.73% of the underwater/marine IoT market share in 2024, while aquaculture producers record the highest projected CAGR at 18.99% to 2030.

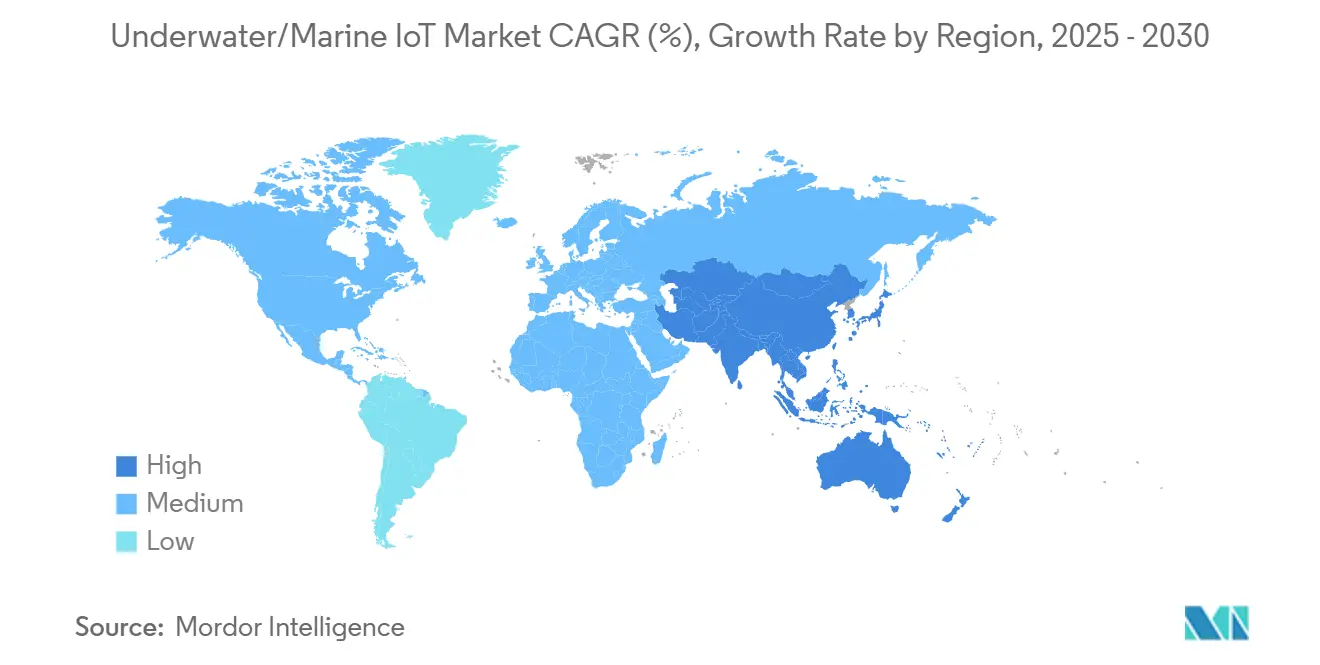

- By geography, North America led with 39.83% of the underwater/marine IoT market share in 2024, and Asia-Pacific is poised to climb at a 19.45% CAGR through 2030

Global Underwater/Marine IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Defense modernization programs driving secure subsea networks | +3.2% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid cost decline in acoustic modems and multi-parameter sensors | +2.8% | Global | Short term (≤ 2 years) |

| Offshore energy expansion demanding real-time monitoring | +3.5% | North America, Europe, Asia-Pacific coastal regions | Long term (≥ 4 years) |

| AI-enabled self-healing hybrid acoustic-optical mesh networks | +2.1% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Energy-harvesting power modules extending node life | +1.9% | Global, particularly remote offshore locations | Long term (≥ 4 years) |

| High-seas biodiversity treaties mandating acoustic eDNA sensor grids | +2.7% | Global, with focus on international waters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Defense Modernization Programs Driving Secure Subsea Networks

Military agencies are funding dense underwater sensor webs that deliver continuous situational awareness in contested zones. The U.S. Navy’s Distributed Maritime Operations concept pairs autonomous seabed nodes with unmanned surface relays to widen detection envelopes.[1]“Tactical Undersea Network Architectures,” DARPA, darpa.mil NATO’s Maritime Unmanned Systems Initiative is aligning standards so allied navies can plug-and-play different vendors’ hardware, enlarging the procurement pool. These programs stipulate encrypted acoustic links and anti-jamming features, which raise hardware requirements but secure future revenue for ruggedized platforms. Artificial-intelligence routines embedded in gateways cut human workload by ranking threats and predicting maintenance, extending dwell times. As more fleets adopt unmanned undersea tactics, the underwater/marine IoT market gains long-term volume.

Rapid Cost Decline in Acoustic Modems and Multi-Parameter Sensors

Volume manufacturing and advanced semiconductor packaging have pushed average acoustic-modem prices down roughly 40% since 2022. Multi-parameter probes that once cost USD 15,000 now list for under USD 5,000, adding dissolved-oxygen, pH, and turbidity readings to a single unit. Software-defined radio architectures let operators retune frequencies via firmware updates rather than hardware swaps, shrinking lifecycle cost. These savings unlock new use cases for mid-size research institutes and fisheries that previously lacked funding. Lower entry barriers broaden adoption beyond defense and oil-and-gas, sustaining double-digit expansion in the underwater/marine IoT market

Offshore Energy Expansion Demanding Real-Time Monitoring

Global offshore-wind capacity is on track to hit 370 GW by 2030, and every turbine foundation and export cable needs structural-health and environmental monitoring.[2]“Offshore Wind Outlook,” International Energy Agency, iea.org Operators use seabed sensors to track scour, vibration, and marine life activity, preventing unplanned shutdowns that can cost USD 1 million per day in lost power sales. Deepwater oil fields continue to commission new subsea tie-backs, adding leak-detection nodes and corrosion probes at depths exceeding 3,000 m. Combined demand from renewables and hydrocarbons makes energy the largest commercial buyer group in the underwater/marine IoT market and underpins stable long-cycle orders for suppliers.

AI-Enabled Self-Healing Hybrid Acoustic-Optical Mesh Networks

Hybrid networks use long-range acoustics for control signals and short-burst optical links for bandwidth-heavy data, such as 4K video or large sonar sets. Machine-learning algorithms predict link degradation from temperature, salinity, or biofouling shifts, then reroute traffic automatically. This self-healing function solves latency pockets that previously required human intervention. Vendors like Hydromea package LED-based modems that run on milliwatts yet transfer megabits per second across tens of meters, enabling swarm robotics for inspection tasks. As reliability improves, commercial users trust the underwater/marine IoT market to replace manual dives, raising recurring data-service revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Signal attenuation and latency in deep-water acoustic channels | -2.1% | Global, particularly deep ocean applications | Long term (≥ 4 years) |

| High CAPEX and OPEX for long-duration buoy/node maintenance | -1.8% | Global, concentrated in remote offshore locations | Medium term (2-4 years) |

| Cyber-physical risks from spoofed GNSS and acoustic jamming | -1.3% | Global, heightened in contested maritime zones | Short term (≤ 2 years) |

| Biofouling-driven sensor drift impacting data fidelity | -1.1% | Global, severe in tropical and temperate waters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Signal Attenuation and Latency in Deep-Water Acoustic Channels

Temperature and salinity gradients bend sound waves, creating multipath echoes that blur signals and add seconds of delay at depths beyond 1,000 m. Shipping noise and marine-life calls further erode throughput. Even with adaptive equalization and spatial diversity antennas, practical data rates often stay below 10 kbps over multi-kilometer links. These physics limits restrict real-time video and large sonar file transfer, forcing designers to schedule bandwidth or cache data locally. The constraint shaves growth potential from deep-sea segments of the underwater/marine IoT market until next-generation techniques mature.

High CAPEX and OPEX for Long-Duration Buoy and Node Maintenance

Pressure-rated nodes range from USD 10,000 to USD 50,000 each, and annual vessel days to clean biofouling or swap batteries can exceed equipment cost in remote waters. A single deep-water service call may run USD 15,000, limiting deployment density for small operators. Energy-harvesting add-ons and robotic cleaning arms promise relief, but current output and reliability fall short for multi-sensor payloads. High upkeep eats into ROI calculations and slows adoption among budget-constrained buyers inside the underwater/marine IoT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Services Disruption

Hardware still captures 52.73% of 2024 revenue as rugged sensors, acoustic modems, and pressure housings form the backbone of every installation. Sensors that log vibration, chemistry, and acoustic signatures bundle into compact frames that survive 3,000 m depths. Communication modules now offer mesh functions and smart power modes to stretch battery life. Despite the up-front spend, buyers see hardware as a long-term asset, keeping demand steady in the underwater/marine IoT market.

Services are climbing fastest at 19.77% CAGR through 2030 because many owners lack subsea expertise. Specialized firms design layouts, install nodes, and run cloud analytics so clients view actionable KPIs rather than raw data. Subscription models spread cost over contracts lasting five to seven years, easing budget approval. As value migrates to insights, service revenue will narrow the gap with hardware and reshape profit pools within the underwater/marine IoT market.

By Communication Technology: Acoustic Legacy Meets Optical Innovation

Acoustic links held 61.83% share in 2024, anchoring shallow- and mid-water projects that need kilometer-scale coverage. Advances in spread-spectrum coding lift resilience against shipping noise, and directional arrays push ranges beyond 20 km in good conditions. These upgrades keep acoustics the backbone of command-and-control traffic in the underwater/marine IoT market.

Hybrid acoustic-optical systems log the quickest gains at 20.32% CAGR. Optical bursts move data above 1 Mbps across tens of meters, letting ROVs and AUVs stream video without surfacing. Automatic mode-switching balances range and speed so users obtain high-resolution feeds when close and reliable acoustics when distant. As more fleets adopt mixed-mode radios, suppliers expect rising orders and a broader addressable base for the underwater/marine IoT market.

By Application: Environmental Monitoring Leads Aquaculture Surge

Environmental monitoring accounted for 29.83% revenue in 2024, propelled by global biodiversity treaties that require habitat assessments across 30% of the ocean by 2030. Governments deploy sensor grids that record chemistry, sound, and eDNA fingerprints, feeding conservation dashboards. Compliance deadlines guarantee multi-year funding, making this segment a stable driver for the underwater/marine IoT market.

Aquaculture and fisheries show the steepest climb at 18.77% CAGR. Farms pair dissolved-oxygen probes with machine-vision cameras to automate feeding, improving feed-conversion ratios and lowering excess waste. Growing seafood demand and tighter sustainability audits spur investment across Asia-Pacific, Norway, and Chile, expanding the commercial slice of the underwater/marine IoT market size.

By End-User: Government Research Yields to Commercial Adoption

Government and research agencies still command 38.73% of 2024 spend thanks to defense surveillance grids and national observatory programs. These users favor high-spec nodes with multi-year endurance, locking in repeat hardware orders and calibration services inside the underwater/marine IoT market.

Aquaculture producers are rising at an 18.99% CAGR as they digitize operations for better yields. Offshore wind operators and shipping terminals join the wave, adopting networked sensors to manage assets and cut insurance risk. This commercial momentum diversifies demand and cushions the underwater/marine IoT market against potential defense budget swings.

Geography Analysis

North America held 39.83% of 2024 revenue, lifted by U.S. Navy unmanned-systems programs and NOAA’s Integrated Ocean Observing System that spans both coasts. Canada’s Ocean Networks Canada array adds Arctic and Atlantic coverage, and Gulf of Mexico energy firms maintain extensive pipeline-integrity networks. Stable public funding plus private energy spend anchors long-term growth for the underwater/marine IoT market in the region.

Europe follows on the strength of offshore-wind deployment targets and rigorous environmental directives from Brussels. Norway integrates monitoring across oil, gas, and aquaculture sites, while the United Kingdom links sensors to its expanding North Sea wind farms. Standardized EU rules simplify cross-border procurement, encouraging multi-country tenders that benefit suppliers active in the underwater/marine IoT market.

Asia-Pacific is the fastest mover at 19.45% CAGR. China outfits smart ports and surveillance grids along Belt and Road sea lanes. Japan installs tsunami-warning cable arrays, and Southeast Asian shrimp farms now trial water-quality nodes that text alerts to farmers’ phones. Rapid industrialization and disaster-preparedness budgets combine to sustain momentum for the underwater/marine IoT market across the region.

Competitive Landscape

Kongsberg and Teledyne lead on breadth, offering acoustic networks, vehicles, and analytics dashboards under one roof.[3]“Reports and Presentations 2024,” Kongsberg Gruppen, kongsberg.com Sonardyne, EvoLogics, and Hydromea specialize in high-accuracy positioning or optical modems, winning niche contracts. New entrants leverage cloud AI or swarm robotics to differentiate, while traditional hardware makers add subscription analytics to defend margins.

Strategic moves center on integrated solutions rather than single devices. Teledyne’s 2024 acquisition of Seatronics deepened its subsea-electronics lineup, bundling sensors with life-of-field service plans. Kongsberg’s Arctic research contract embeds AI within sensor nodes, showcasing value in data-driven autonomy. Patent filings surge in optical modulation and low-power edge AI, signaling sustained innovation aimed at easing bandwidth and maintenance pain points for the underwater/marine IoT market.[4]United States Patent and Trademark Office, “Patent Search,” uspto.gov

Cybersecurity and biofouling pose shared headaches. Vendors respond with encrypted acoustic protocols and copper-alloy faceplates that deter marine growth. Collaborative standard efforts under NATO and IEEE seek common interfaces so multination fleets can mix-and-match gear, which over time could lower integration cost and broaden the addressable underwater/marine IoT market.

Underwater/Marine IoT Industry Leaders

Kongsberg Gruppen ASA

Teledyne Technologies Inc.

Inmarsat Global Limited

Xylem Inc.

Sonardyne Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Kongsberg Gruppen announced expansion of its autonomous underwater vehicle manufacturing facility in Norway with a USD 120 million investment to meet growing demand for defense and commercial underwater IoT applications. The facility will triple production capacity by 2027.

- August 2025: Ocean Infinity completed successful trials of its hybrid acoustic-optical communication system in the Mariana Trench, achieving real-time data transmission from depths exceeding 8,000 meters. The breakthrough enables continuous monitoring of deep-sea mining operations and environmental impact assessment.

- July 2025: AKVA Group ASA launched its new AI-powered aquaculture monitoring platform, integrating underwater IoT sensors with machine learning algorithms for predictive fish health management. The USD 40 million investment targets global salmon farming operations.

- May 2025: Fugro N.V. established a strategic partnership with Microsoft to develop cloud-based analytics for underwater IoT data processing, enabling real-time optimization of offshore wind farm operations across global installations.

Global Underwater/Marine IoT Market Report Scope

| Hardware |

| Software |

| Services |

| Acoustic |

| Optical |

| Radio Frequency (RF) |

| Hybrid Acoustic-Optical |

| Magnetic Induction |

| Environmental Monitoring |

| Oil and Gas Operations |

| Defense and Security |

| Aquaculture and Fisheries |

| Underwater Research and Exploration |

| Offshore Renewable Energy |

| Smart Ports and Shipping |

| Disaster Monitoring and Early Warning |

| Other Application |

| Government and Research Agencies |

| Offshore Energy Companies |

| Aquaculture Producers |

| Shipping and Maritime Logistics Firms |

| Defense / Naval Forces |

| Environmental NGOs and Conservation Orgs |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Communication Technology | Acoustic | ||

| Optical | |||

| Radio Frequency (RF) | |||

| Hybrid Acoustic-Optical | |||

| Magnetic Induction | |||

| By Application | Environmental Monitoring | ||

| Oil and Gas Operations | |||

| Defense and Security | |||

| Aquaculture and Fisheries | |||

| Underwater Research and Exploration | |||

| Offshore Renewable Energy | |||

| Smart Ports and Shipping | |||

| Disaster Monitoring and Early Warning | |||

| Other Application | |||

| By End-User | Government and Research Agencies | ||

| Offshore Energy Companies | |||

| Aquaculture Producers | |||

| Shipping and Maritime Logistics Firms | |||

| Defense / Naval Forces | |||

| Environmental NGOs and Conservation Orgs | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

Key Questions Answered in the Report

How fast is spending on underwater sensor services growing?

Services revenue inside the Underwater IoT market is projected to rise at a 19.77% CAGR through 2030 as owners outsource deployment and data analytics.

Which communication platform is seeing the quickest uptake?

Hybrid acoustic-optical links are expanding at a 20.32% CAGR because they marry long-range acoustics with optical bandwidth for video and large data files.

Why is Asia-Pacific the fastest expanding region?

China’s marine surveillance projects, Japan’s tsunami-warning upgrades, and Southeast Asian aquaculture investments drive a 19.45% CAGR across the region.

What keeps hardware spending high despite falling prices?

Each node must survive high pressure, corrosion, and biofouling, so rugged sensors and modems still account for 52.73% of total 2024 revenue.

What limits data rates in deep-sea networks?

Temperature and salinity gradients bend acoustic waves, causing multipath distortion that caps throughput around 10 kbps over multi-kilometer ranges.

Page last updated on: