5G IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 45.45 Billion |

| Market Size (2031) | USD 149.83 Billion |

| Growth Rate (2026 - 2031) | 26.94% CAGR |

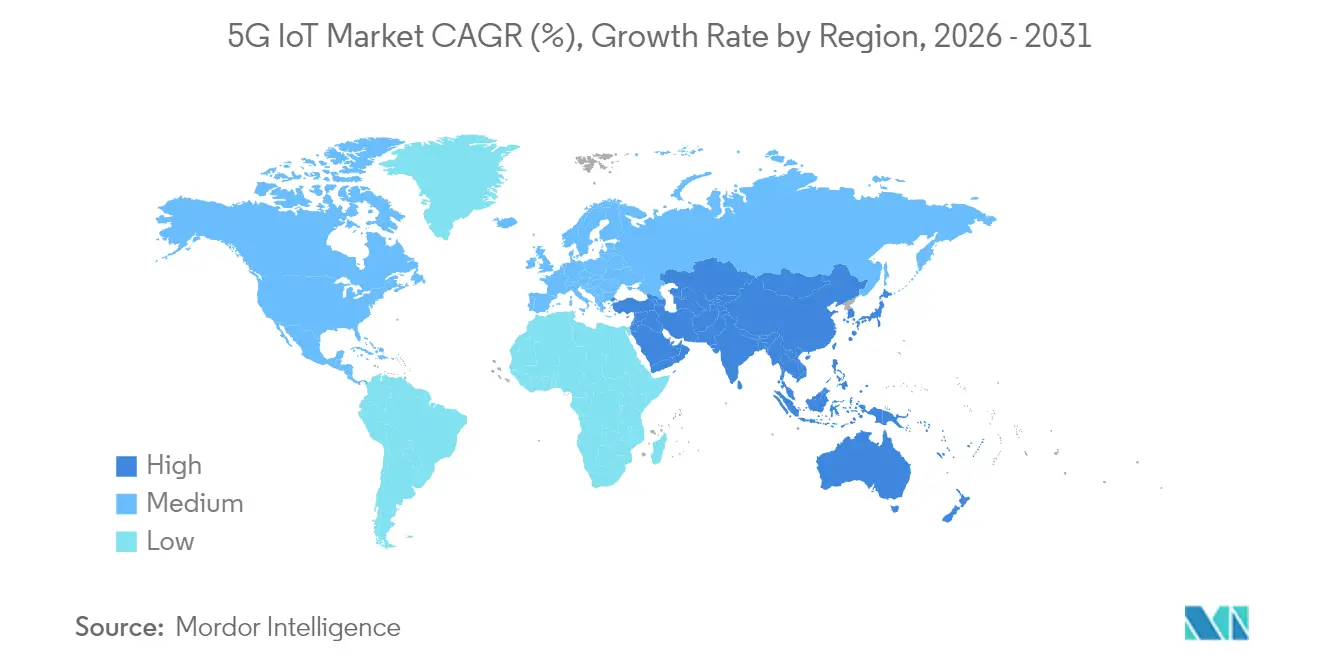

| Fastest Growing Market | Asia |

| Largest Market | Asia |

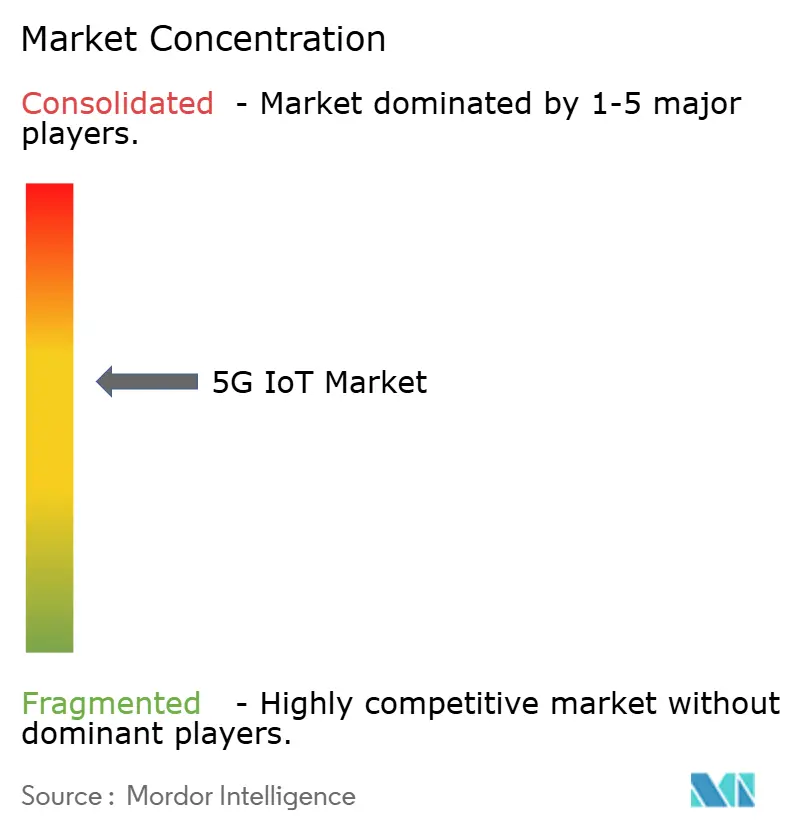

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G IoT Market Analysis by Mordor Intelligence

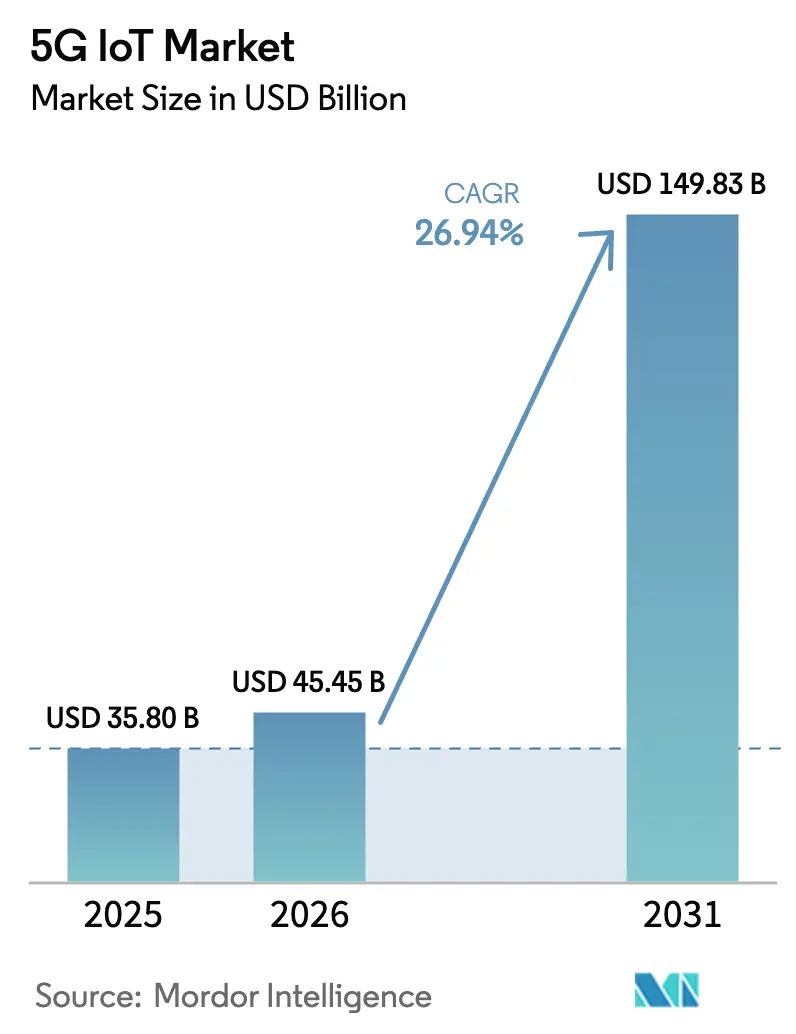

The 5G IoT Market size was valued at USD 35.80 billion in 2025 and estimated to grow from USD 45.45 billion in 2026 to reach USD 149.83 billion by 2031, at a CAGR of 26.94% during the forecast period (2026-2031).

RedCap technology, rolled out under 3GPP Release 17, lowers device complexity and cost, enabling the transition from consumer-centric use cases to large-scale enterprise deployments. Manufacturing, logistics, and automotive firms now justify premium connectivity fees by quantifying productivity gains from ultra-reliable low-latency communications. Governments reinforce adoption through subsidies under the US CHIPS Act and the EU’s IPCEI program, while network-API strategies help operators unlock service revenues beyond pure connectivity. Regulatory demands for supply-chain transparency and energy efficiency further accelerate the shift toward high-density device deployments that only 5G can support.

Key Report Takeaways

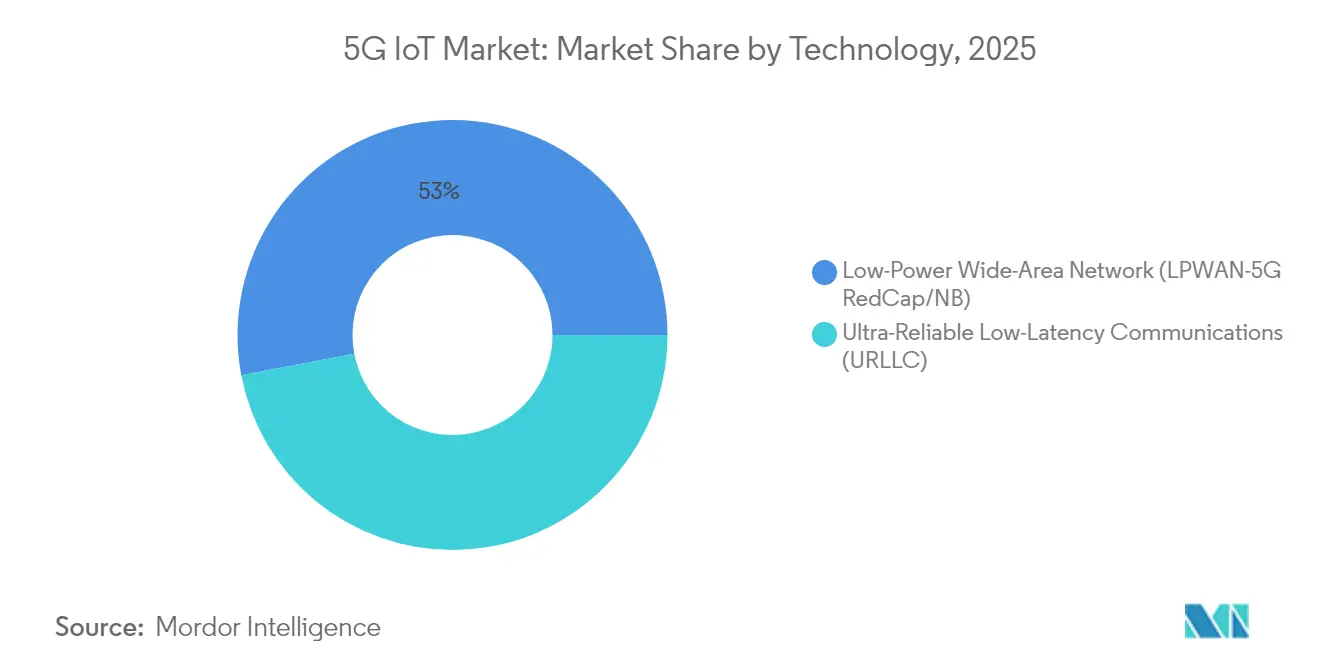

- By technology, LPWAN (5G RedCap) led with 53.00% of the 5G Internet of Things market share in 2025, while URLLC applications are forecast to expand at a 40.63% CAGR through 2031.

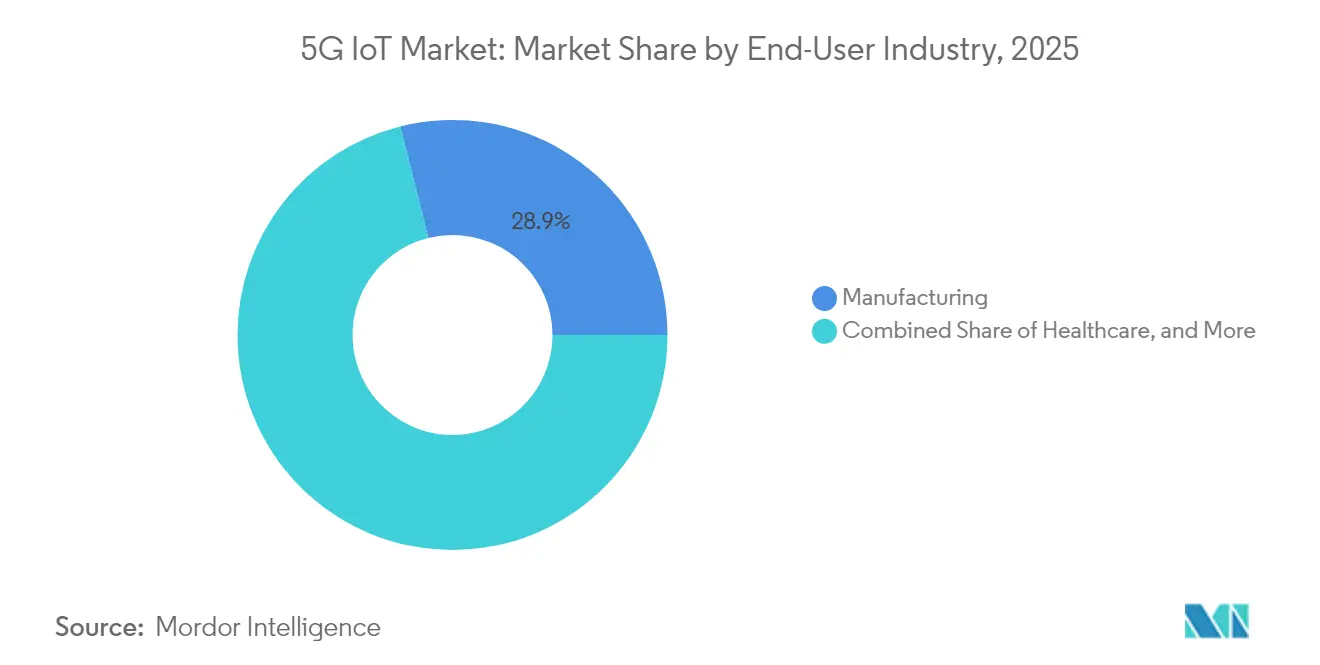

- By end-user industry, manufacturing held 28.90% of the 5G IoT market share in 2025; the automotive segment is projected to grow at 33.12% CAGR between 2026-2031.

- By geography, China accounted for 41.25% revenue share of the market in 2025, whereas India is poised for the fastest growth at 34.95% CAGR to 2031.

- Nokia, Ericsson, and Qualcomm jointly captured an estimated 32% combined share of the market size in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Massive device-density enablement after RedCap roll-out | +8.20% | Global — highest traction in China and North America | Medium term (2-4 years) |

| Telco cloud & network-API monetization playbooks | +6.10% | North America and EU; expanding to APAC | Long term (≥ 4 years) |

| 3GPP-approved reduced-capability chipsets below USD 5 | +7.40% | Global, especially India and LATAM | Short term (≤ 2 years) |

| Energy-price-linked demand for ultra-low-power modules | +4.30% | EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Massive device-density enablement after RedCap roll-out

Release 17 RedCap limits peak data rates to 250 Mbps and employs simpler antenna architectures, trimming module costs by 30-40%. Multi-year battery life aligns with industrial automation, smart metering, and city-wide sensing, while backward compatibility maintains nationwide coverage.[1]Rohde & Schwarz, “RedCap simplifies 5G devices,” rohde-schwarz.com

Telco cloud & network-API monetization playbooks

Cloud-native 5G cores let operators expose quality-of-service, location, and slicing functions through APIs. Enterprises pay a premium for deterministic performance, creating service revenue that offsets heavy spectrum and infrastructure investments.

3GPP-approved reduced-capability chipsets below USD 5

Silicon vendors achieve sub-USD 5 cost by stripping legacy smartphone functions, shrinking memory, and optimizing power management. The price point triggers migrations from 2G/3G to 5G in smart meters, wearables, and municipal sensors.[3]Economic Times, “Chipset vendors hit sub-USD 5 price point,” economictimes.indiatimes.com

Energy-price-linked demand for ultra-low-power modules

High electricity prices push enterprises to adopt IoT nodes with advanced sleep modes and energy harvesting. Ten-year battery life reduces truck rolls for oil-field monitoring and smart agriculture, improving total cost of ownership.[2]MDPI, “Low-power 5G module design,” mdpi.com

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G/LPWAN sufficiency for sub-USD 2 device classes | –4.8% | Global; highest in emerging markets | Long term (≥ 4 years) |

| Security-compliance costs (NIS2, SBOM) squeeze OEM margins | –4.1% | EU core with global ramifications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

4G/LPWAN sufficiency for sub-USD 2 device classes

Many low-value sensors only transmit kilobytes per day; LTE Cat-1 and NB-IoT already meet such needs at half the module cost. Rural utilities and agri-tech firms therefore defer 5G upgrades until pricing aligns with value delivered.

Security-compliance costs (NIS2, SBOM) squeeze OEM margins

The NIS2 directive obliges continuous vulnerability disclosure and software bill-of-materials tracking. Compliance absorbs 9% of IT budgets and disproportionately affects small manufacturers, delaying launches of new 5G IoT devices .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RedCap Bridges Performance-Cost Gap

LPWAN (5G RedCap) captured 53.00% of the 5G market in 2025, reflecting optimum trade-offs between cost and network capabilities. URLLC, although smaller, is projected to grow at a 40.63% CAGR as factories and autonomous vehicles demand sub-1 ms latency. The 5G Internet of Things market size for LPWAN devices is projected to rise significantly as module prices fall toward USD 4 by 2027. Enterprises migrate asset-tracking and environmental-monitoring workloads from LTE Cat-1 to RedCap to leverage network slicing without incurring full 5G hardware costs. Conversely, domains such as robotic welding and remote surgery justify the premium of URLLC, driving specialized chipset innovation.

URLLC use cases frequently pair with edge-compute nodes inside private 5G networks, replacing deterministic wired Ethernet. Audi’s implementation in press-shops improved cycle times and reduced downtime, validating the business case. Component vendors compete on time-sensitive networking features and FEC schemes that guarantee packet delivery, distinguishing offers beyond bandwidth metrics. In sum, technology choice in the 5G Internet of Things market aligns with distinct latency, power, and cost envelopes instead of a one-size-fits-all roadmap.

By End-User Industry: Manufacturing Drives Enterprise Adoption

Manufacturing held 28.90% of the 5G Internet of Things market in 2025 as factories rushed to digitize supply chains and comply with EU CSRD reporting. URLLC-enabled machine vision removes bottlenecks in quality inspection, and RedCap streamlines asset tracking for pallets and tooling. The market size for manufacturing is projected to expand in step with standalone-network rollouts that support time-sensitive networking profiles.

Automotive applications form the fastest-growing segment, forecast at a 33.12% CAGR. Automakers pilot V2X safety messages, over-the-air software updates, and production-line robotics. The shift to software-defined vehicles aligns with 30-year lifecycles, making scalable connectivity essential. Healthcare and smart-city programs adopt 5G for telehealth and waste-management sensors, but volumes remain secondary to manufacturing scale. Across sectors, enterprises focus on monetizable use cases rather than blanket connectivity, solidifying a value-driven adoption model in the 5G Internet of Things market.

Geography Analysis

Asia-Pacific dominated the 5G Internet of Things market with China accounting for 41.25% of revenue in 2025, backed by operator capex and policy incentives. China Unicom plans 5G-Advanced coverage in 300 cities by end-2025, adding massive machine-type capacity and raising network utilization. Local integrators retrofit production lines in steel, textiles, and electronics, mainstreaming private-network know-how. India posts the fastest regional CAGR at 34.95% through 2031 as RedCap’s sub-USD 5 modules fit the budget of small and medium enterprises. Government programs such as Digital India and Make-in-India relax spectrum-leasing rules, accelerating campus-wide deployments in pharma, auto, and energy verticals.

North America prioritizes private-network pilots in semiconductor fabs and defense hubs, aided by CHIPS Act grants. The automotive corridor from Michigan to Texas deploys roadside V2X units and factory URLLC links, validating return-on-investment for high-bandwidth, low-latency services. Cloud hyperscalers partner with carriers to expose network APIs that let enterprises configure paths with code, shortening service-activation cycles from months to minutes. This platform's dynamic extends the 5G Internet of Things market beyond connectivity into application hosting.

Regulatory Landscape

Regulation affecting 5G IoT is widening from radio and device authorization to cybersecurity, supply-chain transparency, and data governance. In the United States, the Federal Communications Commission (FCC) adopted a voluntary IoT Labeling Program (Cyber Trust Mark) in March 2024 and launched it on January 7, 2025, which gives buyers a procurement and retail signal for security-by-design in connected devices.

In 2026, the FCC tightened national-security and compliance requirements that spill over into cellular IoT equipment sourcing and deployment. FCC rules adopted in April 2026 require license and authorization holders to attest to foreign adversary ownership or control (effective June 9, 2026), and May 2026 rules strengthened the equipment authorization program (effective June 15, 2026) through measures such as prioritized review tied to Trusted Test Labs and updated post-market surveillance. Internationally, ITU-T issued multiple 2025 recommendations relevant to large-scale IoT deployments, including ITU-T Y.4814 on zero-trust-enabled access control for decentralized IoT platforms and ITU-T Y.3226 on fixed, mobile, and satellite convergence frameworks aligned with IMT-2020 era IoT architectures.

Value Chain Analysis

The 5G IoT value chain covers standards and spectrum policy (3GPP, ITU, and national regulators), chipset and module suppliers (for example, Qualcomm and MediaTek for NR/RedCap-class devices), network equipment vendors (notably Ericsson, Nokia, Huawei, and ZTE), and operators that package connectivity with private-network and managed-service layers. Systems integrators and specialist private network providers assemble radio, core, and edge compute into vertical solutions for factories, logistics sites, and campuses, while device OEMs and application providers deliver sensors, gateways, and industrial platforms that convert deterministic connectivity into measurable productivity gains.

Commercialization increasingly hinges on certification, roaming, and provisioning workflows rather than radio performance alone. The emergence of eSIM standards for IoT (SGP.32) supports single-SKU global device strategies through remote profile management for unattended endpoints, while operator-to-satellite partnerships for NB-IoT (aligned with 3GPP NTN approaches) extend coverage for cross-border logistics and remote monitoring. Separately, RedCap ecosystem validation programs among operators, network vendors, and chipset providers underscore how silicon readiness, operator acceptance testing, and module availability need to align for standards to translate into scalable deployments.

Competitive Landscape

The 5G Internet of Things market remains moderately fragmented. Nokia and Ericsson ship pre-integrated private-network kits paired with edge clouds, reporting double-digit order growth. Qualcomm extends its Snapdragon X family with RedCap variants, taking IoT revenue to USD 1.55 billion in Q1 2025. Samsung, MediaTek, and Unisoc chase mid-tier industrial modems, intensifying price competition. System integrators such as JMA Wireless and Celona specialize in radio-core bundles for warehouses.

Start-ups embrace software-defined connectivity and non-terrestrial networking. Skylo raises USD 37 million to beam NB-IoT traffic via GEO satellites, targeting logistics firms that traverse coverage gaps. 1NCE exploits a one-time fee model for lifetime connectivity, boasting 18 million active SIMs across 170 countries. Patent filings surge around AI-driven link-adaptation and millimeter-wave beam tracking, as vendors vie to deliver 6G-ready hooks. Investors value recurring revenue: Wireless Logic secured a GBP 3.5 billion valuation on a minority capital injection, indicating robust confidence in horizontal IoT platforms.

End-customer preference is tilting toward outcome-based engagements. Aerospace primes order guaranteed-uptime SLAs, and mining giants procure “connectivity-as-ore-ton” contracts. Vendors who bundle hardware, software, and professional services thus defend margins even as unit prices fall. Over the forecast period, competitive advantage will hinge on vertical domain knowledge, security credentials, and ecosystem breadth inside the 5G Internet of Things market.

5G IoT Industry Leaders

Nokia

Ericsson

Huawei

ZTE

ATandT

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise private 5G is moving from isolated pilots toward repeatable, multi-site operating models that bundle connectivity with automation and edge-enabled applications. A visible proof point is Cargill and NTT DATA expanding private 5G across 50 of Cargill's 1,100 facilities (announced in 2026) to support connected workplace initiatives and AI-enabled robotics, creating whitespace for integrators, device OEMs, and operators that can productize deployment templates, SLAs, and lifecycle management for factories and distribution sites.

Network modernization and AI-native operations are also opening monetization layers for 5G IoT beyond SIM connectivity, particularly where deterministic performance and rapid provisioning are required. Examples include Nokia signing multi-year 5G RAN modernization with Virgin Media O2 (2026) and extending a 5G partnership with Taiwan Mobile (July 2026) that emphasizes AI-powered networks. These programs drive demand for network APIs, slicing-aware device onboarding, and analytics-driven assurance tailored to URLLC and RedCap classes. At the infrastructure layer, projects that expand fiber backbone reach and add edge sites, such as the NEC and Nokia work with Eletronet in Brazil that includes new fiber build and edge data centers through end-2026, support low-latency industrial and city-scale sensing use cases by bringing compute and transport closer to endpoints.

Recent Industry Developments

- July 2026: Ericsson, AT&T, and MediaTek completed North America's first in-field trial of Layer 1/Layer 2 Triggered Mobility (LTM) on AT&T's network, reporting reduced data interruption during cell changes. The result strengthens the performance case for mobile 5G IoT endpoints that move across cells, such as connected logistics assets and vehicles, where session continuity affects application reliability.

- May 2026: Telenor IoT and Sateliot announced a partnership to enable seamless terrestrial and satellite NB-IoT connectivity based on 3GPP Release 17 non-terrestrial network standards. The move broadens the addressable footprint for IoT deployments that face coverage gaps, supporting cross-border logistics, remote monitoring, and multi-region service bundles built around a unified device and subscription model.

- June 2025: Ericsson and Google Cloud unveiled a SaaS core-network platform designed to scale network functions on demand for operators. This supports faster rollout of cloud-native cores that expose capabilities used by 5G IoT services, including policy control and differentiated quality handling, and it lowers operational friction for operators expanding enterprise-grade connectivity portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this study, the 5G IoT market is defined as spending tied to IoT devices and deployments that use 5G connectivity to deliver low latency, high reliability, or higher device density for enterprise and public-sector use cases.

Scope exclusions: We exclude general 4G LTE IoT connectivity and non-cellular IoT networks (such as Wi-Fi, Bluetooth, and LoRaWAN), unless they are directly bundled in a 5G IoT deployment.

Segmentation Overview

- By Technology

- Ultra-Reliable Low-Latency Communications (URLLC)

- Low-Power Wide-Area Network (LPWAN 5G RedCap/NB)

- By End-User Industry

- Manufacturing

- Supply-Chain and Logistics

- Healthcare

- Retail

- Smart Cities and Infrastructure

- Automotive and Transportation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Asia-Pacific

- China

- Japan

- India

- Australia and New Zealand

- Middle East and Africa

- Middle East

- Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the initial market boundary and to gauge demand signals for 5G-enabled IoT rollouts. We leaned on public indicators that track network readiness and device adoption, including 5G coverage milestones, spectrum releases, and IoT connection growth, which are typically published by sources such as the ITU, the GSMA, the FCC, and European Commission portals.

To keep assumptions grounded, we also reviewed filings and investor decks from ecosystem participants, operator announcements, and credible press coverage. This helped confirm timing for items such as RedCap device availability and private 5G deployments. Where needed, select paid database subscriptions were used for company financials and intelligence, news and financials screening, and patent database checks to confirm technology maturity and adoption direction. The sources listed above are illustrative and not exhaustive, and additional public datasets and documents were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how 5G IoT revenue is counted across the value chain, and on separating pilots from scaled deployments. We talked with network-side and device-side experts, system implementers, and end-user teams across major regions, so adoption timing, pricing logic, and volume ramps could be checked against what is visible in public signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | APAC: 44% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 17% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool using 5G IoT adoption indicators, then translates that demand into value using pricing and mix assumptions. In practice, we use signals such as 5G population coverage and rollout pace, expected uptake of private 5G for industrial sites, RedCap device attach rates, and the split of deployments that need URLLC-type performance versus standard cellular IoT.

The totals are then corroborated using selective bottom-up checks, including sampled ASP by device class multiplied by shipment proxies, and channel checks on enterprise deployment run-rates. Where direct volume is not consistently visible, gaps are handled through ranges agreed in interviews, followed by sensitivity checks so the final number is not driven by a single optimistic input.

For forecasting, scenario analysis is used because this market is shaped by step-changes, including spectrum availability, operator SA core readiness, and enterprise budget cycles. Assumptions on ASP progression are adjusted based on expected module cost-down trends and mix shift toward higher volume device categories, and then checked with primary inputs before being applied year by year.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent indicators, then through variance checks versus adjacent markets such as overall IoT connections, 5G subscriptions, and private network announcements. When model results fall outside realistic adoption bands, we review the underlying assumptions, and respondents are re-contacted if the variance appears to be driven by pricing, timing, or scope interpretation.

Each report is refreshed annually, and interim updates are made when material events occur, such as major standard milestones, policy shifts, or abrupt pricing moves. Before delivery, an analyst runs a fresh pass on key inputs so the latest updated view is reflected in the final model outputs.

Mordor Intelligence's 5g IOT Market Sizing Compared With Other Published Estimates

Published 5G IoT market values can vary widely, even when they appear to cover the same theme, because each publisher draws the scope differently and updates core assumptions on its own schedule. The spread is usually driven by what is counted as 5G IoT revenue, how device and connectivity pricing is treated over time, and whether early-stage pilots are included as full deployment value.

Because ASPs and deployment volumes can shift quickly as RedCap devices scale and private 5G adoption broadens, refresh cadence and currency conversion timing can move the headline number from one year to the next. A monthly check of 5G rollout signals (coverage expansion, spectrum actions, and enterprise launch activity) is used before locking annual values, which is how Mordor Intelligence keeps the 2026 estimate aligned to commercial deployments instead of announcements.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 45.45 B (2026) | |

| Global Consultancy A | USD 24.06 B (2026) | This estimate likely uses a narrower revenue capture that emphasizes device-related value and limits counted deployment spend, and it may also apply a faster ASP decline without fully adjusting for mix shift into higher value industrial use cases. |

| Trade Journal B | USD 35.80 B (2025) | This figure is presented for a different base year and is often shared as a headline value without clearly separating pilots from scaled deployments. It can also reflect simplified currency timing and fewer explicit checks against rollout readiness signals, which can change the year-by-year sizing. |

Overall, the gap across sources is mainly explained by year alignment, what parts of the deployment are monetized in the model, and how quickly pricing is assumed to move as volumes scale. When scope, pricing paths, and rollout validation steps are clearly stated, the market size becomes easier to reproduce and more consistent to compare across years.

Key Questions Answered in the Report

What is the current size of the 5G Internet of Things market?

The market stands at USD 45.45 billion in 2026 and is projected to hit USD 149.83 billion by 2031.

Which segment holds the largest 5G Internet of Things market share today?

LPWAN (5G RedCap) technology leads with 53.00% share, thanks to its cost-performance balance.

Which end-user industry is growing fastest?

Automotive applications are forecast to grow at 33.12% CAGR between 2026-2031 as V2X and software-defined vehicles scale.

Why is RedCap considered pivotal for massive IoT deployments?

RedCap pares device costs below USD 5 while preserving 5G compatibility, enabling dense sensor networks across factories and cities.

How do new EU regulations influence 5G IoT adoption?

The CSRD drives demand for real-time supply-chain monitoring, while NIS2 raises compliance costs, rewarding vendors with strong security propositions.

Which region will experience the highest growth through 2031?

India leads with a 34.95% CAGR, buoyed by cost-sensitive RedCap modules and supportive digital-infrastructure policies.

Page last updated on: