Underwater Communication System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

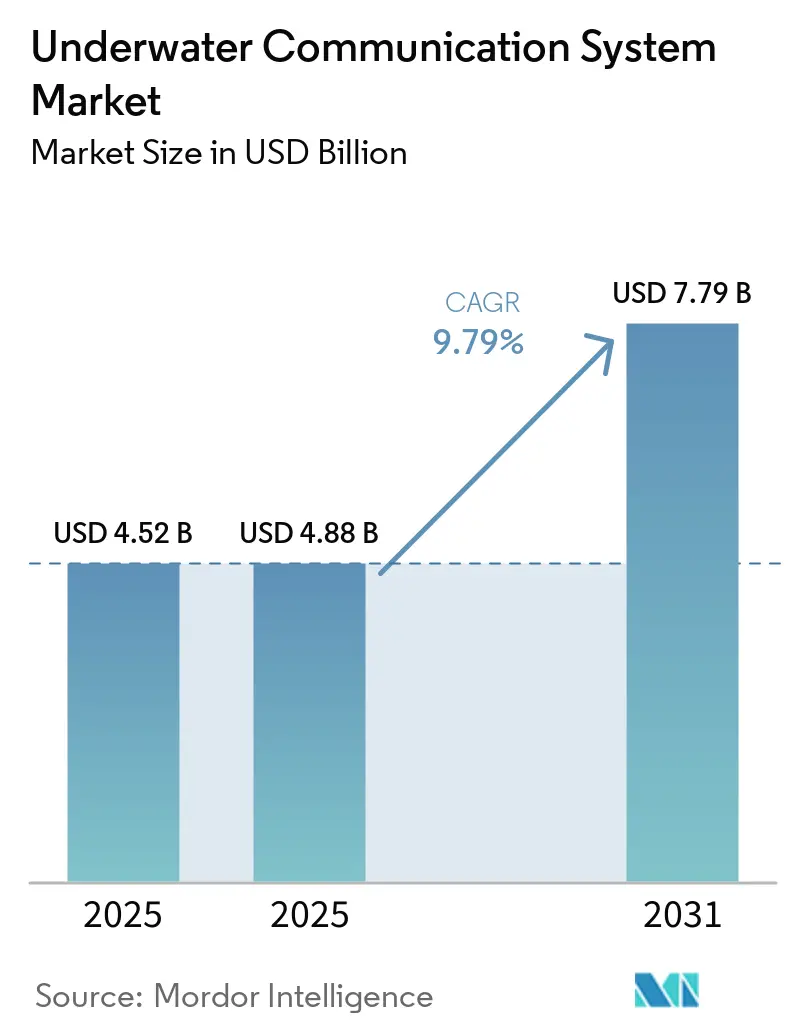

| Market Size (2025) | USD 4.88 Billion |

| Market Size (2031) | USD 7.79 Billion |

| Growth Rate (2026 - 2031) | 9.79% CAGR |

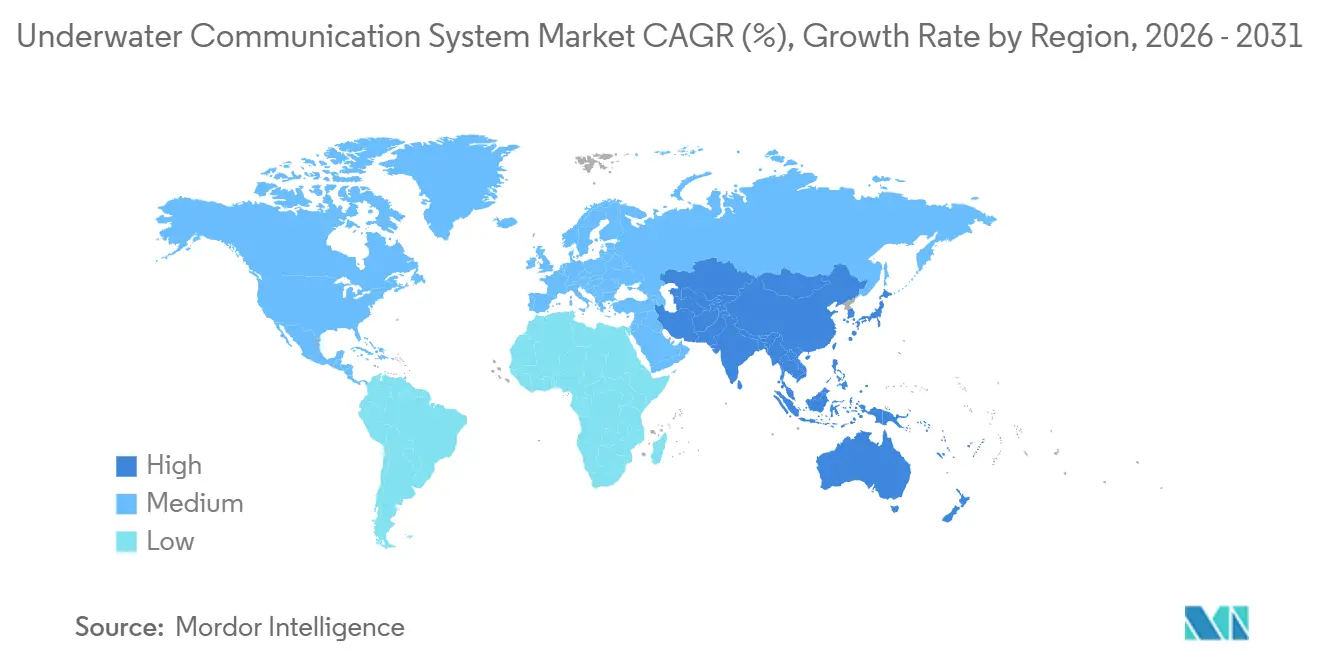

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

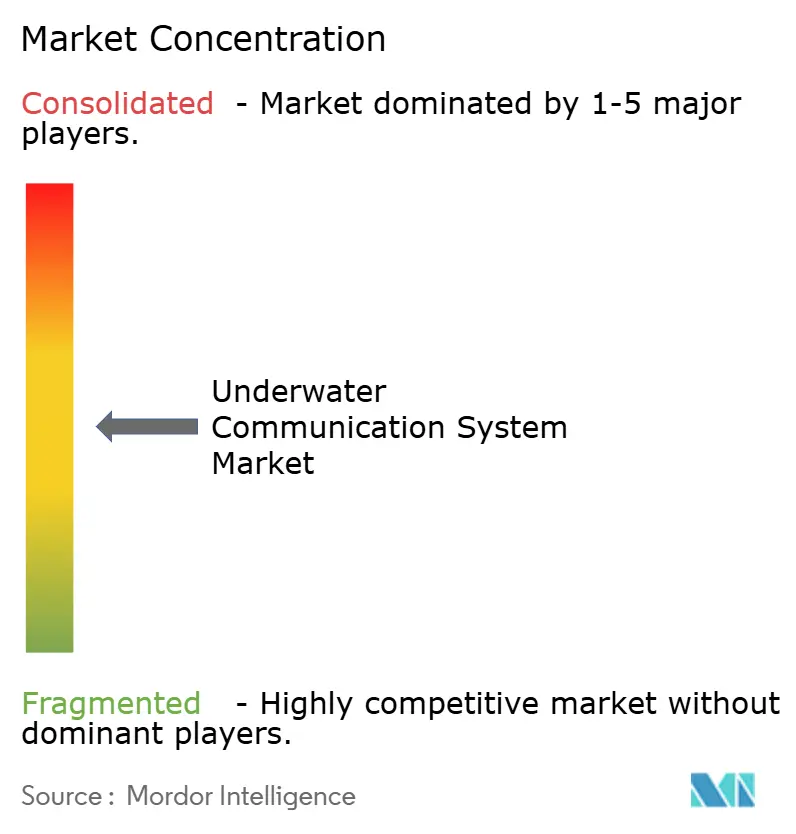

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underwater Communication System Market Analysis by Mordor Intelligence

The underwater communication system market size was valued at USD 4.52 billion in 2025 and is estimated to grow from USD 4.88 billion in 2026 to reach USD 7.79 billion by 2031, at a CAGR of 9.79% during the forecast period (2026-2031). Modular, software-defined architectures are displacing legacy single-band transceivers as defense procurement cycles converge with offshore renewable-energy build-outs. Hybrid optical-acoustic payloads are attracting system integrators that need gigabit uplinks for unmanned platforms, while distributed acoustic sensing on export cables is expanding the addressable node base. The underwater communication system market is also benefiting from government funding aimed at protecting critical seabed infrastructure and at scaling autonomous vehicle fleets for wide-area surveillance. Mid-life modernization schedules for Virginia-class and Columbia-class submarines, combined with the first production units of Australia’s Ghost Shark program, give suppliers multi-year visibility on unit shipments.

Key Report Takeaways

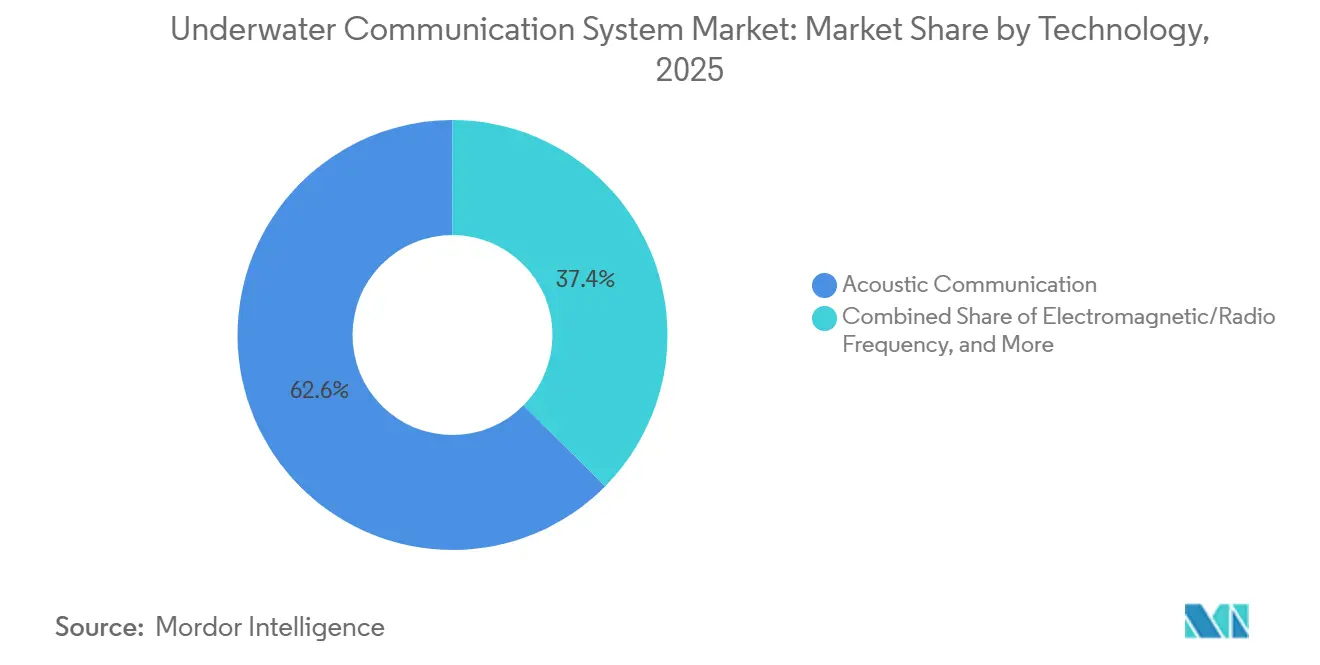

- By technology, acoustic communication led with 62.58% of the underwater communication system market share in 2025, whereas optical blue-green laser systems are projected to expand at an 8.45% CAGR through 2031.

- By component, hardware accounted for 57.53% of 2025 revenue, while software and services are advancing at an 8.39% CAGR to 2031.

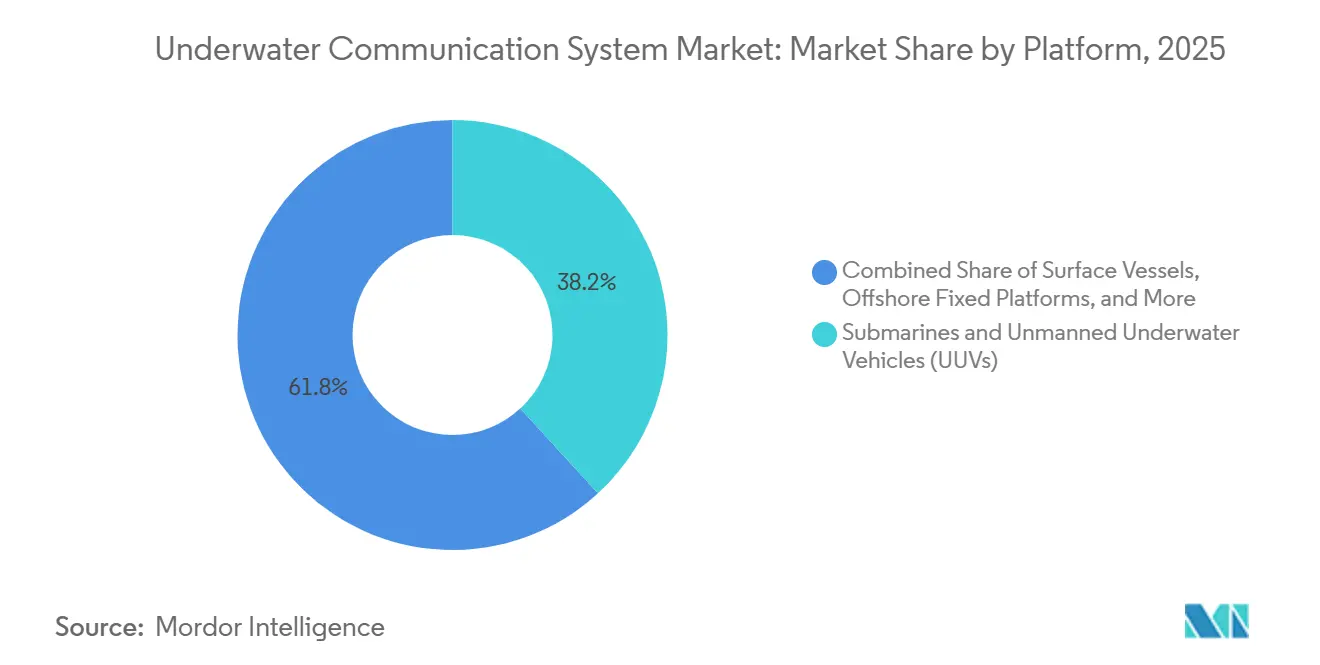

- By platform, submarines and unmanned underwater vehicles captured 38.17% revenue share of the underwater communication system market in 2025, while scientific and monitoring buoys are forecast to post the fastest 8.67% CAGR.

- By application, defense and security generated 44.83% of revenue of the underwater communication system market in 2025, whereas environmental monitoring and oceanography is expected to register an 8.53% CAGR.

- By geography, North America held 31.76% share in 2025, yet Asia-Pacific is anticipated to record the highest 8.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Underwater Communication System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Autonomous Underwater Vehicles | +2.8% | North America, Europe, Asia-Pacific defense corridors | Medium term (2-4 years) |

| Accelerated Subsea Data-Center Pilots by Hyperscalers | +0.9% | North America and Europe coastal zones with fiber-optic landing stations | Short term (≤2 years) |

| Defense Modernization Programs Focused on Contested Seabed Zones | +2.4% | North America, Europe, Asia-Pacific, Middle East | Long term (≥4 years) |

| Growth in Offshore Renewable Energy Installations Needing Real-Time Monitoring | +1.6% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Expansion of Deep-Sea Mineral Exploration Licenses | +1.2% | Clarion-Clipperton Zone, Indian Ocean nodule fields | Long term (≥4 years) |

| Emergence of Software-Defined Acoustic Modems Enabling Dynamic Spectrum Use | +1.4% | Global early adopters in defense and scientific research | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Autonomous Underwater Vehicles

Procurement of extra-large and medium-class autonomous vehicles is rising because navies can maintain a persistent subsea presence at lower cost per patrol hour than crewed submarines. The United States Defense Innovation Unit selected Dive-XL in March 2026 to demonstrate open-architecture payload integration, a model that allows communication modules to be swapped without vessel recertification.[1] Defense Innovation Unit, “Collaborative Autonomy for Maritime Platforms,” diu.mil Australia’s Ghost Shark project delivered its first hull in January 2026 and uses modular bays that accept third-party acoustic or optical transceivers, trimming qualification time for vendors. Japan’s Acquisition, Technology and Logistics Agency achieved a 1 megabit-per-second link at 50 meters using a blue-green laser paired with an acoustic fallback channel, underscoring bandwidth priorities in new vehicle designs.

Accelerated Subsea Data-Center Pilots by Hyperscalers

Microsoft’s Project Natick proved submerged data vaults had lower hardware failure rates, yet follow-on contracts remain absent, implying that maintenance economics still favor land-based edge nodes. [2]Microsoft Research, “Project Natick Phase 2 Findings,” microsoft.com Hyperscalers instead fund distributed acoustic sensing on subsea cables to detect mechanical stress events in real time. Yokogawa Electric launched a 10 000-point sensing platform for offshore wind export cables in December 2024, revealing that communication demand is shifting toward structural health monitoring rather than compute off-loading.

Defense Modernization Programs Focused on Contested Seabed Zones

NATO established a Critical Undersea Infrastructure Coordination Cell in January 2025 following multiple cable sabotage incidents, which accelerated orders for low-probability-of-intercept waveforms. Anduril’s Seabed Sentry acoustic node network, trialed in April 2025, achieved 95% classification accuracy for diesel-electric submarines at ranges beyond 10 kilometers. China’s Transparent Ocean initiative continues to seed fixed acoustic arrays across the South China Sea, compelling allied navies to harden their subsea links.

Growth in Offshore Renewable Energy Installations Needing Real-Time Monitoring

With the expansion of wind farms in Europe's North Sea and Baltic regions, operators are increasingly prioritizing comprehensive monitoring of export-cable strain to prevent significant gigawatt-level curtailments. Effective cable monitoring is critical to maintaining uninterrupted energy transmission and ensuring operational efficiency. In 2024, Indeximate transformed conventional fiber-optic cables into cost-effective acoustic arrays for RWE projects, reducing the cost per monitoring node to under USD 50. This innovation not only lowers costs but also enhances the scalability of monitoring systems. The International Energy Agency projects a global offshore wind capacity of 380 gigawatts by 2030, suggesting a surge in the need for cable-monitoring nodes to support this growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Bandwidth Limits of Acoustic Channels in Turbid Waters | -1.8% | Southeast Asia river deltas, high-sediment littorals | Short term (≤2 years) |

| High CAPEX for Hybrid Optical-Acoustic Networks | -1.4% | Global, with pronounced effect on smaller oil and gas or research operators | Medium term (2-4 years) |

| Regulatory Ambiguity Around RF Spectrum Below 30 kHz | -0.6% | International waters | Long term (≥4 years) |

| Cyber-Security Vulnerabilities in Long-Baseline Networks | -0.9% | Defense and critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Bandwidth Limits of Acoustic Channels in Turbid Waters

Multipath interference, ambient shipping noise, and sediment scatter significantly reduce acoustic data rates to only a few kilobits per second in shallow coastal zones, creating substantial challenges for efficient data transmission. An IEEE Access study revealed that turbidity levels exceeding 50 NTU reduce signal-to-noise ratios by 15 decibels at 20 kilohertz, effectively halving throughput and impacting communication reliability. To mitigate these issues, operators embed edge compute to compress data before uplink, which adds USD 50,000-100,000 in node hardware costs. However, this approach also shortens battery life, further complicating operational efficiency in such environments.

High CAPEX for Hybrid Optical-Acoustic Networks

A two-channel node that houses a blue-green laser plus an acoustic modem can exceed USD 500,000 because of beam-steering optics, gimbals, and redundant power. Laboratory prototypes that achieved 170 gigabits per second required vertical-external-cavity lasers priced at roughly USD 80,000 each. [3]Optical Society of America, “170 Gbps Blue-Green Laser Transmission in Seawater,” osapublishing.org Smaller offshore energy firms hesitate to adopt due to lock-in risks and extended payback periods, which arise from the absence of standardized optical protocols. These challenges make it difficult for such firms to justify the investment, as they face uncertainties in compatibility and long-term cost efficiency. Consequently, the lack of standardization hampers broader adoption within this segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Acoustic Dominance Persists Despite Optical Gains

In 2025, acoustic links held 62.58% of underwater communication system market revenue because they operate over 10 kilometers with modest alignment requirements. Optical blue-green lasers are advancing at an 8.45% CAGR through 2031 as laboratories demonstrate 170 gigabit-per-second polarization-division multiplexing, yet seawater absorption beyond 550 nanometers confines operational range to roughly 100 meters. Electromagnetic systems remain niche since seawater attenuates signals above 30 kilohertz within meters. Hybrid designs pairing an acoustic backbone with an optical burst channel satisfy missions that need high-definition video off-load during close approaches.

Software-defined acoustic modems are now field-programmable, allowing operators to retune carrier frequencies when ambient noise spikes, which reduces downtime and extends asset life. EvoLogics embedded the JANUS open protocol in 2024 to guarantee fleet interoperability across NATO forces. Regulatory uncertainty around sub-30 kilohertz spectrum continues, placing the burden on equipment makers to certify both acoustic and optical paths for each jurisdiction. Meanwhile, gallium-nitride laser diodes are trending toward lower cost curves, promising sub-USD 10 000 optical endpoints suited to aquaculture pens and inspection drones.

By Component: Software Gains as Over-the-Air Updates Reduce Downtime

Hardware captured 57.53% of 2025 revenue because transducers, modems, and subsea-rated connectors still command premium prices. However, the software and services segment is projected to outpace hardware with an 8.39% CAGR, fueled by cloud-hosted fleet management and by waveform hot-patching that saves dry-dock fees. L3Harris won a USD contract in February 2026 to supply 26 shipsets that support over-the-air encryption-key rotation, illustrating how software control is now a procurement must-have.

Transducer innovation focuses on piezo-composite stacks that widen the usable bandwidth envelope, permitting a single unit to cover multiple frequency bands and thereby trim bill of materials. Cable integrity and connector reliability still represent up to 20% of node hardware cost because of pressure housing and corrosion control. On the software side, machine-learning diagnostics assess channel quality in real time and recommend power or frequency adjustments, turning historical field data into predictive maintenance alerts that lower life-cycle cost. Services revenue is rising as offshore installers bundle node commissioning, training, and multi-year support into subscription contracts.

By Platform: Buoys Surge as Offshore Wind Drives Sensor Networks

Submarines and unmanned underwater vehicles delivered 38.17% of underwater communication system market size in revenue terms during 2025, a figure buoyed by multi-year production of Virginia-class upgrades and Ghost Shark prototypes. Yet scientific and monitoring buoys are projected to grow fastest at an 8.67% CAGR because offshore renewable farms need real-time environmental telemetry from hundreds of low-cost endpoints. Buoys also anchor distributed acoustic sensing arrays, relaying compressed data to satellites without dispatching crewed support vessels, thereby improving economics for operators.

Open-architecture middleware on Dive-XL lets navies install a new communications payload within days instead of months, shortening technology refresh cycles and encouraging payload competition. Fixed platforms in the North Sea and Gulf of Mexico are retrofitting acoustic modems to enable digital oilfield workflows, whereas floating structures in Brazil’s pre-salt basin prefer fiber-optic tethers for high-bandwidth export. Monitoring buoys benefit from lithium-sulfur battery packs and solar trickle charging, extending mission endurance past one year and supporting denser mesh topologies.

By Application: Environmental Monitoring Gains as Climate Research Expands

Defense and security applications accounted for 44.83% of 2025 revenue because submarines, seabed arrays, and mine countermeasure systems prioritize encrypted, low-probability-of-intercept links. Environmental monitoring and oceanography, however, is slated for an 8.53% CAGR to 2031 as research agencies blanket continental shelves with chemical and acoustic sensors that quantify carbon uptake and marine-mammal migration. Oil and gas operators rely on real-time pressure and flow data to optimize production and to predict equipment failures, reinforcing steady demand for robust acoustic networks.

Aquaculture firms in Norway and Chile apply mid-band acoustic networks to adjust feeding cycles based on oxygen and ammonia readings, trimming feed waste and improving fish health. Scientific glider fleets operated by national oceanographic labs upload high-resolution profiles over satellite-linked buoys every few days, a workflow that favors burst optical links when the platform surfaces near a mother ship. In marine construction, towed sonar sleds equipped with wideband modems validate trench depth in real time, reducing re-work and penalty costs for cable-lay contractors.

Geography Analysis

North America generated 31.76% of 2025 revenue thanks to submarine communication modernization, increasing offshore wind capacity along the Atlantic coast, and Arctic surveillance initiatives. The Dive-XL program contracts and L3Harris shipset awards provide a visible backlog through 2033, while Canada’s Arctic sensor grid protects the Northwest Passage as shipping lanes expand. Mexico’s deepwater Gulf of Mexico blocks require subsea communication nodes that handle multi-vendor sensor streams, reinforcing regional demand.

Asia-Pacific is forecast to grow at an 8.73% CAGR between 2026 and 2031. Australia’s AUD 1.7 billion (USD 1.12 billion) Ghost Shark investment anchors supplier roadmaps, and Japan’s hybrid optical-acoustic modem prototypes signal a strategic push toward higher bandwidth. China’s Transparent Ocean network extends acoustic surveillance, while South Korea and India fund new submarine builds that integrate software-defined modems. Offshore wind rollouts in Taiwan, Vietnam, and India add hundreds of export-cable monitoring nodes, though export controls on dual-use technologies and diverging certification regimes create market entry hurdles.

Europe shows robust replacement demand across North Sea and Baltic assets that rely on distributed acoustic sensing to detect anchor drags and fishing-gear strikes. NATO’s Baltic Sentry operation highlights infrastructure vulnerability and spurs procurement of low-intercept acoustic waveforms. The Middle East deploys fiber-optic tethers on Persian Gulf platforms to circumvent acoustic bandwidth ceilings, whereas South America’s pre-salt provinces in Brazil demand optical links capable of multimegabit throughput. Chile’s salmon growers and Argentina’s early offshore wind studies broaden the regional application mix, lowering dependence on oil and gas alone.

Competitive Landscape

Market concentration is moderate because no single vendor controls the entire chain from piezo-ceramic transducers to digital signal-processing firmware. Defense primes such as L3Harris Technologies, Thales Group, and Lockheed Martin dominate naval programs, yet commercial specialists like EvoLogics, Sonardyne International, and Teledyne Technologies lead scientific and energy applications. The underwater communication system market is witnessing convergence as incumbents bundle acoustic and optical payloads, while entrants such as Anduril Industries leverage software-first architectures to erode switching costs.

EvoLogics’ 2024 upgrade added JANUS and Standards for Wireless Interoperable Gateways support, giving NATO fleets multi-vendor interchangeability. Kongsberg Gruppen signed a main-supplier pact with Fugro in March 2026 for HiPAP positioning, signaling vertical consolidation in hydrographic survey solutions. Patent filings cluster around beam-steering optics for blue-green lasers and wideband transducer stacks that stretch acoustic bandwidth beyond 20% of center frequency, an area where Teledyne and Ultra Electronics Maritime Systems invest heavily.

Start-ups are repurposing gallium-nitride diodes to create optical transceivers priced under USD 10,000 for aquaculture cages, targeting previously untapped opportunities in the market. These transceivers aim to enhance operational efficiency and monitoring capabilities in aquaculture systems. However, the commercialization of these devices faces significant challenges, particularly in meeting stringent pressure-rating standards required for underwater applications. Overcoming these technical barriers is critical for achieving widespread adoption and scaling production effectively.

Underwater Communication System Industry Leaders

Teledyne Technologies Incorporated

Kongsberg Gruppen ASA

Sonardyne International Ltd.

Ultra Electronics Maritime Systems Inc.

L3Harris Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Kongsberg Gruppen and Fugro announced a main-supplier agreement for HiPAP underwater positioning systems, integrating Fugro’s service network with Kongsberg technology.

- March 2026: The United States Defense Innovation Unit awarded Anduril Industries a Dive-XL contract under the Collaborative Autonomy for Maritime Platforms program.

- March 2026: Teledyne Technologies secured a UK Royal Navy order for underwater gliders equipped with acoustic links for persistent surveillance.

- March 2026: Thales Group unveiled the Expeditionary PathMaster mine countermeasure concept featuring autonomous vehicles and synthetic-aperture sonar.

Global Underwater Communication System Market Report Scope

The Underwater Communication System Market pertains to the development and deployment of technologies designed to facilitate reliable data transmission in submerged environments. These systems primarily utilize acoustic, optical, or radio frequency methods. They are integral to various applications, including defense and naval operations, offshore oil and gas exploration, oceanographic research, environmental monitoring, and underwater robotics.

The Underwater Communication System Market Report is Segmented by Technology (Acoustic Communication, Optical Blue-Green Laser, Electromagnetic Radio Frequency, Hybrid), Component (Hardware including Modems, Transducers, Cables, Sensors; Software and Services), Platform (Submarines and UUVs, Surface Vessels, Fixed and Floating Platforms, Buoys), Application (Defense, Oil and Gas, Environmental Monitoring, Research, Marine Construction), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value USD.

| Acoustic Communication |

| Optical (Blue/Green Laser) |

| Electromagnetic/Radio Frequency |

| Hybrid |

| Hardware | Modems |

| Transducers/Transceivers | |

| Cables and Connectors | |

| Sensors and Antennas | |

| Software and Services |

| Submarines and Unmanned Underwater Vehicles (UUVs) |

| Surface Vessels |

| Offshore Fixed Platforms |

| Offshore Floating Platforms |

| Scientific and Monitoring Buoys |

| Defense and Security |

| Oil and Gas Exploration and Production |

| Environmental Monitoring and Oceanography |

| Scientific Research and Academia |

| Marine Construction and Aquaculture |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | Acoustic Communication | ||

| Optical (Blue/Green Laser) | |||

| Electromagnetic/Radio Frequency | |||

| Hybrid | |||

| By Component | Hardware | Modems | |

| Transducers/Transceivers | |||

| Cables and Connectors | |||

| Sensors and Antennas | |||

| Software and Services | |||

| By Platform | Submarines and Unmanned Underwater Vehicles (UUVs) | ||

| Surface Vessels | |||

| Offshore Fixed Platforms | |||

| Offshore Floating Platforms | |||

| Scientific and Monitoring Buoys | |||

| By Application | Defense and Security | ||

| Oil and Gas Exploration and Production | |||

| Environmental Monitoring and Oceanography | |||

| Scientific Research and Academia | |||

| Marine Construction and Aquaculture | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is global spending on underwater communications growing?

The underwater communication system market size is forecast to rise from USD 4.88 billion in 2026 to USD 7.79 billion by 2031, reflecting a 9.79% CAGR over the period.

Which technology currently leads in revenue?

Acoustic communication led with 62.58% market share in 2025 thanks to its long-range reliability and mature supply chain.

What segment is expanding the quickest?

Optical blue-green laser systems are projected to post an 8.45% CAGR to 2031 as operators seek gigabit burst links for unmanned platforms.

Why is Asia-Pacific considered a high-growth region?

Programs such as Australia's Ghost Shark XLAUV, Japan's hybrid modem R&D, and China's seabed sensor arrays underpin an 8.73% regional CAGR forecast.

Page last updated on: