Cellular IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

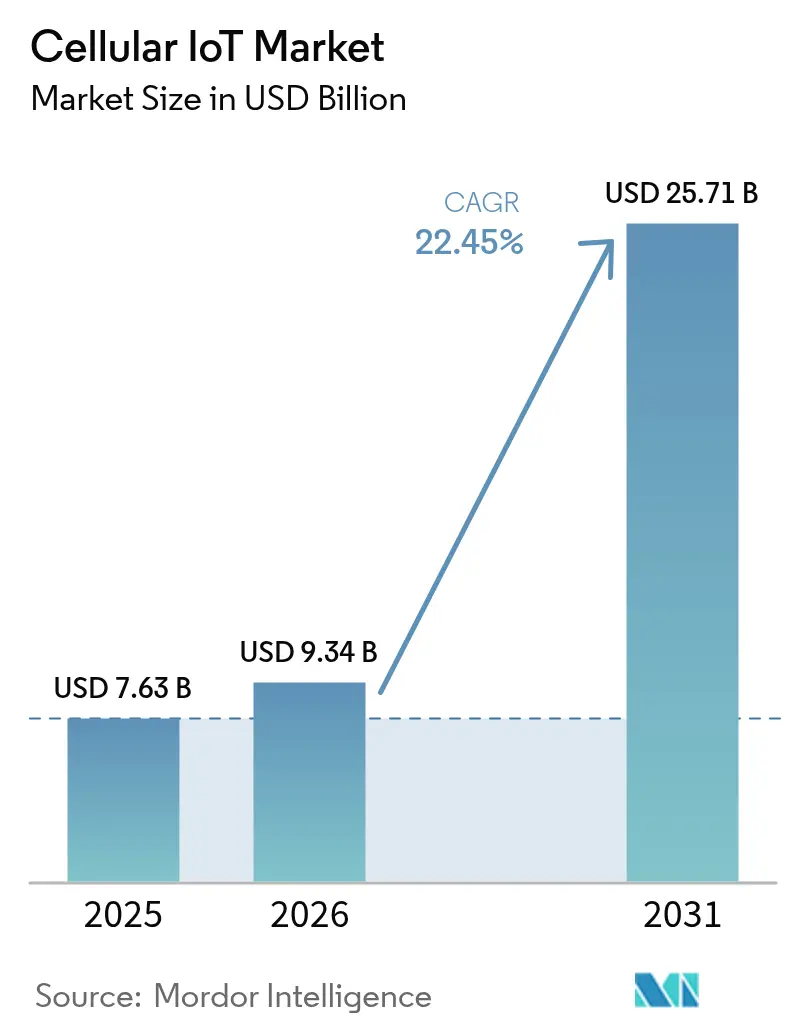

| Market Size (2026) | USD 9.34 Billion |

| Market Size (2031) | USD 25.71 Billion |

| Growth Rate (2026 - 2031) | 22.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cellular IoT Market Analysis by Mordor Intelligence

The cellular IoT market size was valued at USD 7.63 billion in 2025 and estimated to grow from USD 9.34 billion in 2026 to reach USD 25.71 billion by 2031, at a CAGR of 22.45% during the forecast period (2026-2031). Demand scales on the back of 5G RedCap commercialization, smart-city funding mandates, and precision-agriculture roll-outs that extend connectivity beyond factory floors. Asia Pacific remains the epicenter of scale manufacturing, allowing module average selling prices to drop below USD 4 and accelerating the shift from sunset 2G/3G networks to 4G Cat-1bis and 5G RedCap-enabled devices. Operators in North America, Europe, and China continue to migrate toward standalone 5G core deployments, creating headroom for ultra-reliable low-latency services in industrial automation and connected mobility. Services outpace hardware growth as enterprises depend on global connectivity management platforms and managed security to mitigate fragmented regulations. Meanwhile, semiconductor capacity at ≥65 nm nodes stays tight, keeping cost discipline front-of-mind for device makers even as chipset performance improves.

Key Report Takeaways

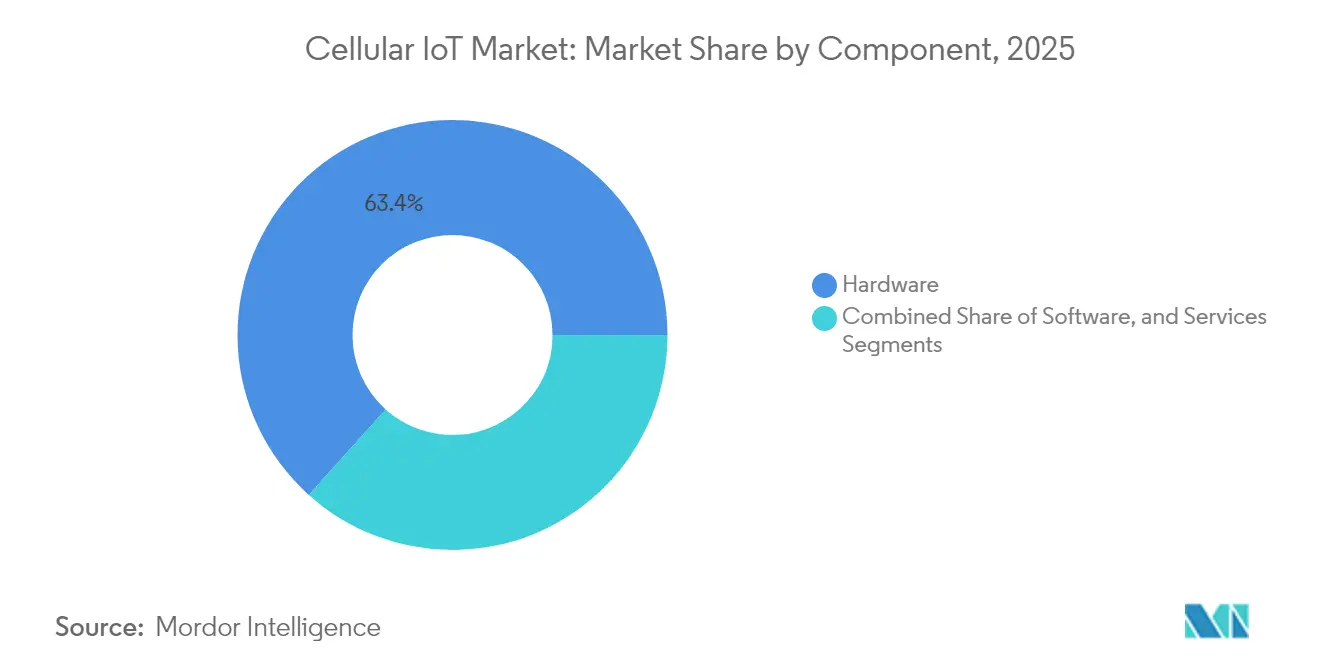

- By component, hardware accounted for 63.35% of revenue in 2025 while services are projected to post a 24.10% CAGR through 2031.

- By technology, 4G LTE Cat-1 commanded 56.20% revenue share in 2025; 5G RedCap is on course to grow at 27.10% CAGR to 2031.

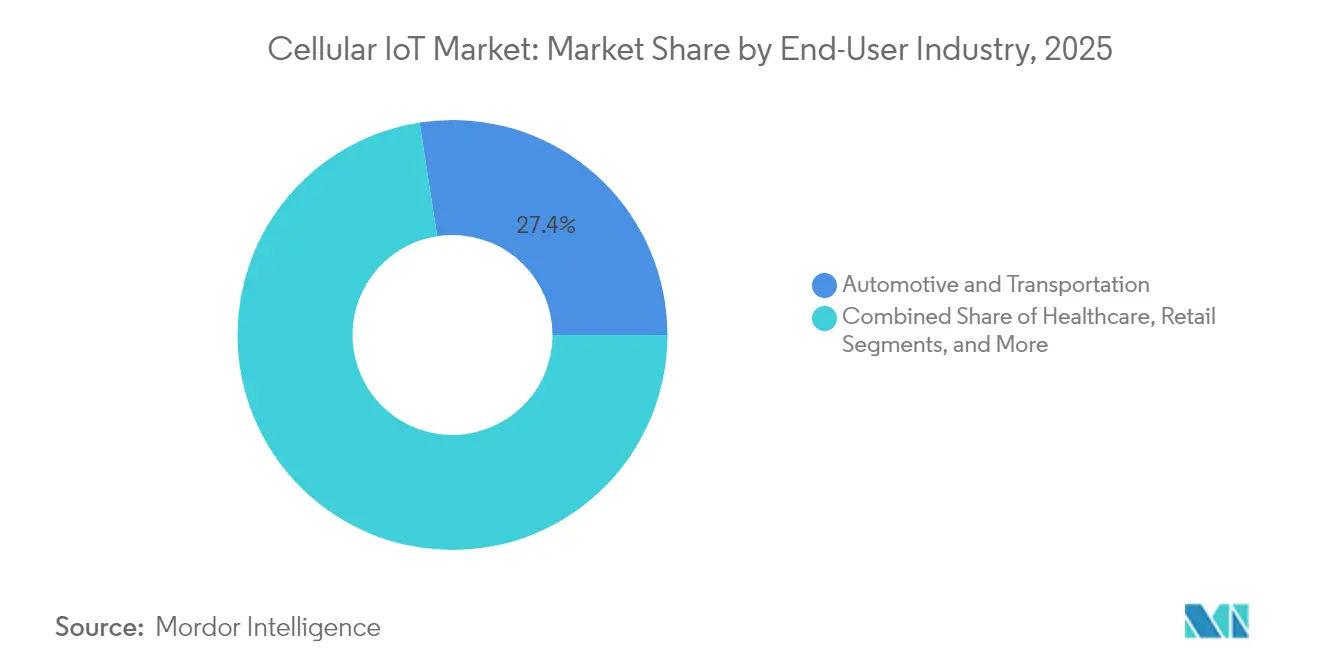

- By end-user industry, automotive and transportation held 27.45% revenue share in 2025; agriculture is forecast to expand at 23.80% CAGR through 2031.

- By application, asset tracking led with 29.40% revenue share in 2025; wearables and personal devices are projected to register a 27.90% CAGR to 2031.

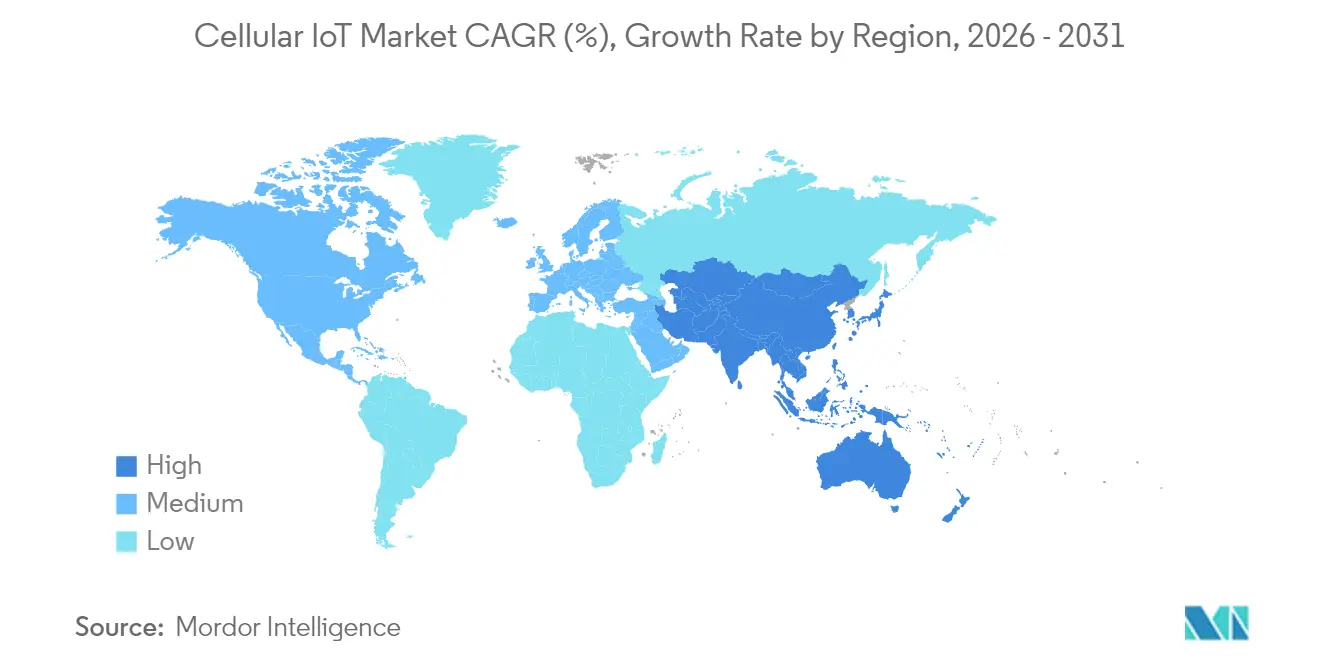

- By geography, Asia Pacific captured 69.60% of the cellular IoT market share in 2025 and is set to grow at 28.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cellular IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G SA roll-out enabling URLLC IoT | +4.2% | Global, led by China and North America | Medium term (2-4 years) |

| Module ASPs below USD 4 for Cat-1bis | +3.8% | Asia Pacific core, spill-over to global | Short term (≤ 2 years) |

| Government-funded NB-IoT smart-city mandates | +3.5% | China, EU, India | Medium term (2-4 years) |

| 5G RedCap modules unlock mid-tier devices | +4.5% | North America and EU early adoption | Long term (≥ 4 years) |

| Sustainability-linked asset-tracking demand | +2.9% | Global with EU leadership | Medium term (2-4 years) |

| Mass certification of eSIM/iSIM | +3.1% | Global deployment, Asia Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G SA roll-out enabling URLLC IoT

Commercial standalone 5G networks deliver sub-5 ms latency that industrial firms require for closed-loop automation. AT&T’s June 2024 RedCap launch in Dallas allowed chipset vendors to certify devices on a live 5G SA network and confirmed power-consumption cuts of 65% against LTE Cat-4 modules.[1]AT&T, “AT&T Leads with First 5G RedCap Launch,” att.comTelefonica’s German trials and Samsung–Hyundai manufacturing lines underline readiness, yet true scale hinges on national 5G SA coverage and affordable module supply.

Module ASPs below USD 4 for Cat-1bis

Large 2024 tenders in China pushed Cat-1bis modules under USD 4, widening 4G’s addressable base before older networks shut down. Quectel and Fibocom together captured two-thirds of module revenue, but heavy reliance on a single manufacturing region has triggered supply-security reviews in Europe and the United States. Non-Chinese suppliers face margin compression; u-blox exited the segment in January 2025 after sustained losses.

Government-funded NB-IoT smart-city mandates

China’s National Development and Reform Commission issued guidelines in May 2024 requiring NB-IoT deployments in metering and environmental monitoring for 100 smart cities by 2027. India’s Smart Cities Mission and South Korea’s National Strategic Smart City Program mirror the trend, collectively channeling billions of dollars into cellular IoT infrastructure. The policies guarantee device volume, stabilize operator ROI, and spur international adoption of standardized LPWA frameworks.

5G RedCap modules unlock mid-tier devices

3GPP Release 18 introduced enhanced RedCap with 5 MHz bandwidth while sustaining 10 Mbps peak rates. Ericsson, Optus, and Qualcomm have demonstrated RedCap-connected AI cameras that improve worker safety. T-Mobile’s 2025 5G Advanced launch has already positioned RedCap as a default option for wearables and smart infrastructure, reinforcing mid-tier device migration away from LTE-only platforms.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High power draw of 5G modules in battery devices | -2.8% | Global, remote deployments | Short term (≤ 2 years) |

| 2G/3G sunsets causing retrofit costs | -3.2% | North America and Europe | Medium term (2-4 years) |

| Cat-1bis chipset supply volatility | -2.1% | Global supply chains | Short term (≤ 2 years) |

| Fragmented IoT security standards | -1.9% | Worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High power draw of 5G modules in battery devices

Even after RedCap efficiency gains, absolute power remains a challenge for sensors targeting 10-year field life. Nordic Semiconductor’s nRF9151 module introduced Power Class 5 output to extend battery cycles and accommodate satellite fallback links essential for remote agriculture. Device makers are integrating energy-harvest options but must trade cost and size against performance.

2G/3G sunsets causing retrofit costs

AT&T discontinued NB-IoT service while European carriers phase out 2G and 3G through 2027, forcing upgrades of long-lifecycle meters and industrial controllers. Retrofit expenses deter immediate replacements, prompting some utility customers to delay expansion until RedCap ecosystems fully mature. Inventory-optimization software helps minimize write-offs by staging module swaps in step with service wind-down schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Shifts to Service Innovation

Hardware contributed 63.35% of 2025 revenue as manufacturers rushed to replace legacy units ahead of network sunsets. Qualcomm posted 27% year-over-year IoT revenue growth to USD 1.58 billion in Q2 2025 on the back of robust chipset demand. The cellular IoT market size attributed to services is expected to outpace hardware with a 24.10% CAGR through 2031, reflecting climbing subscriptions for global connectivity management, firmware-over-air updates, and zero-touch security patches.

Global enterprises now insist on unified dashboards that orchestrate multi-carrier, multi-technology fleets. KORE Wireless already manages 19 million active lines across 200 countries through AI-driven fault detection. Professional services teams fill knowledge gaps in radio-planning, certification, and regulatory compliance. Managed-service contracts ensure recurring revenue that cushions hardware price erosion, aligning vendor incentives with customer uptime and security objectives.

By Technology: 4G LTE Maintains Leadership as 5G RedCap Emerges

4G LTE Cat-1 secured 56.20% revenue share in 2025 after Chinese OEMs slashed module prices below USD 4. Complementary LPWA modes such as LTE-M and NB-IoT serve ultra-low-throughput use cases including metering and leak detection. Legacy 2G/3G connections decline faster than previously forecast because operators are reallocating spectrum to 5G SA. The cellular IoT market size for 4G will taper as customers migrate to RedCap, but it remains a high-volume option where coverage and cost trump bandwidth.

5G RedCap is registering a 27.10% CAGR and is viewed as the bridge between LPWA and full-spec 5G. Samsung and Hyundai validated RedCap in a February 2025 factory trial, showing deterministic latency and 40% energy savings compared with LTE-M. Non-terrestrial networks that complement terrestrial 5G are gaining momentum; Viasat and Myriota launched the first 5G NTN service for environmental sensing in March 2025, opening pathways for global coverage on a single module SKU.

By End-User Industry: Automotive Leadership Challenged by Agricultural Surge

Automotive and transportation captured 27.45% revenue share in 2025 on the strength of mandated emergency-call modules and fleet telematics. Vehicle-to-everything applications are driving automakers to embed multiple antennas, and Lear Corporation forecasts a USD 5 billion automotive 5G opportunity by 2030. Software updates delivered over cellular links reduce recall expenses and improve safety features, further rooting connectivity into vehicle architectures.

Agriculture’s 23.80% CAGR ranks highest among verticals as growers digitize irrigation, soil monitoring, and livestock management. China’s irrigation project with 1,614 controllers resulted in 40% water savings and 80% labor reduction. 1NCE reports more than 7% of its active clients now hail from the farming sector, signaling structurally higher demand for rugged, low-maintenance modules. Remote assets often require satellite back-up links, making dual-mode cellular-sat combinations attractive for harsh or isolated locales.

By Application: Asset Tracking Dominance Faces Wearables Disruption

Asset tracking delivered 29.40% revenue share in 2025, fueled by supply-chain visibility mandates. TOPFLYtech’s freight-monitoring deployment for U.S. transport fleets underscores scale potential as enterprises prioritize condition-based monitoring to cut spoilage and CO₂ emissions. Advanced cold-chain trackers integrate humidity and shock sensors, feeding real-time data to compliance dashboards.

Wearables and personal devices are rising at 27.90% CAGR, buoyed by health-monitoring rules that require seamless emergency connectivity. RedCap modules lower battery draw, encouraging OEMs to embed cellular links in smartwatches and medical wearables. eSIM and iSIM simplify activation, and 5G’s network slicing supports quality-of-service tiers indispensable for critical alerts. Adoption will vary by region, but premium consumer and enterprise segments provide a deep upgrade runway.

Geography Analysis

Asia Pacific secured 69.60% of 2025 revenue and is set to advance at 28.60% CAGR through 2031 on the back of national digital-transformation plans. China expects 4.1 billion licensed cellular connections by 2030, representing 70% of global totals. The cellular IoT market size attached to Chinese deployments alone is poised to dwarf every other region combined as 5G-Advanced coverage blankets additional provinces.

Regional manufacturing concentration cuts module costs but introduces dependency risk that Western regulators now scrutinize. India’s USD 5.76 billion Smart Cities Mission and Indonesia’s upcoming RedCap spectrum auctions add incremental volume outside China. Emerging markets across Southeast Asia adopt turnkey cloud-managed private-network packages that offset limited local telecom expertise, ensuring that connectivity gaps shrink quickly. North America positions itself as the premium application hub, with AT&T and T-Mobile focusing on low-latency industrial deployments. Europe places compliance and sustainability at the center of IoT spending, with Telefonica testing RedCap in Germany and Ericsson rolling out private 5G in French municipalities. The cellular IoT market share of Asia Pacific is unlikely to erode before 2030, but revenue mix will swing toward managed services in all three regions as device counts grow.

Regulatory Landscape

Cellular IoT rules are tightening around radio approvals, spectrum harmonization, and security-led device authorization, which increases compliance work for global SKUs. In the United States, the FCC set new measures that take effect in June 2026 to strengthen national security in telecommunications equipment authorization, including priority review paths for devices tested in Trusted Test Labs. As a result, OEMs and module suppliers are shifting toward localized test strategies and earlier certification planning.

Elsewhere, spectrum and technical requirements continue to evolve. Indonesia enforced KEPMEN KOMDIGI No. 569 Year 2025 in January 2026, adding Band 41 (2496-2690 MHz) for 4G LTE and 5G NR devices and affecting band support decisions for modules shipped into the market. In Europe, CEPT adopted Report 90 in June 2025 to define harmonized conditions in the 900 MHz band for new narrowband technologies beyond NB-IoT, while standards work feeding future certification baselines continues, including ETSI TS 138.291 v19.3.0 published in April 2026 for 5G NR Ambient IoT physical layer specifications.

Value Chain Analysis

The cellular IoT value chain spans silicon and RF components (chipsets, power management, memory), module design and manufacturing, device OEM integration, and certification and testing, followed by operator connectivity and recurring software and services such as connectivity management, device management, and security. Market dynamics are strongly shaped by high-volume module suppliers and their manufacturing ecosystems, where Quectel and Fibocom lead module revenue in this RD. Operators and connectivity-management specialists monetize fleet onboarding, provisioning (including eSIM/iSIM), and lifecycle operations.

Recent supply-chain moves also point to a shift from single-region sourcing toward localized production and more bundled delivery models. In India, Quectel expanded its partnership with Syrma SGS Technology in April 2026 to manufacture IoT antennas locally, and Optiemus Electronics began a manufacturing partnership with Quectel in June 2026 to produce wireless communication modules in Noida, indicating deeper regional assembly and component localization. On the downstream side, operators are packaging more of the deployment workflow: AT&T rolled out an industrial logistics and asset-tracking service in July 2026 that bundles sensor hardware (from Wiliot) with connectivity and field services. This reinforces services as a differentiation route alongside hardware price competition.

Competitive Landscape

Two Chinese suppliers-Quectel and Fibocom-soak up 64% of global module revenue, giving them disproportionate influence over pricing and component roadmaps. Their volume leverage compresses margins for competitors and creates a single-region sourcing risk that has moved up the agenda of Western policymakers. Qualcomm’s February 2025 purchase of Sequans’ 4G IoT assets for USD 200 million broadened its mid-tier portfolio and secured experienced engineering talent for upcoming RedCap silicon. Sequans now concentrates on 5G RedCap design, clarifying its niche in the value chain.

Strategic partnerships differentiate solution providers. Telit Cinterion’s alliance with floLIVE and Skylo couples terrestrial and satellite coverage for seamless global asset tracking, a capability critical for maritime and mining customers. T-Mobile’s tie-up with Thales and SIMPL offers a turnkey eSIM-based connectivity kit that reduces onboarding time for device makers. Smaller specialists carve out white-space opportunities in regulated sectors-medical wearables, intrinsically safe sensors, or devices rated for -40 °C-that demand certifications often missing in low-cost offerings.

Semiconductor tightness at mature process nodes persists through 2027, challenging volume forecasts. Vendors hedge by dual-sourcing or transitioning to more advanced nodes where capacity exists, albeit at higher wafer costs. Security remains a differentiator; module makers that integrate hardware-rooted secure elements and align with IEC 62443 see stronger uptake in industrial accounts that face cyber-liability legislation.

Cellular IoT Industry Leaders

Qualcomm Technologies Inc.

AT&T

Ericsson

Huawei Technologies

Fibocom Wireless

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise buyers are increasingly prioritizing end-to-end cellular IoT operations, which creates whitespace for managed connectivity, device lifecycle tooling, and security services that work across multiple carriers and technologies. Scale indicators in the ecosystem, including global cellular IoT connections at 4.7 billion in 2025 and module shipments at 612 million units, support this direction. Investment and consolidation around global IoT service platforms also point to demand for integrated offerings, such as Telenor and Verdane agreeing in May 2026 on a joint ownership structure for Telenor Connexion (valued at SEK 7.5 billion) with additional growth capital commitments. For vendors, the opportunity centers on simplifying global onboarding (eSIM/iSIM, unified dashboards) and packaging compliance and monitoring as recurring services as device fleets expand across jurisdictions.

Technology transitions are widening addressable segments where LTE economics and 5G capability overlap. RedCap momentum is moving beyond trials into broader operator activity, and industry tracking cites 42 operators in 27 countries investing in 5G RedCap as of April 2026. Industrial validation programs, including the Samsung and Hyundai factory trial, help translate URLLC and deterministic behavior into deployable designs for cameras, sensors, and AGVs. Non-terrestrial extensions add another layer of opportunity for logistics, agriculture, and remote monitoring, where a single module SKU can blend terrestrial and satellite coverage. In parallel, regulatory discussions such as satellite IoT and M2M authorization pathways in India highlight ongoing market-building work that solution providers can productize into global coverage offers.

Recent Industry Developments

- July 2026: AT&T deployed an industrial logistics and asset-tracking service that bundles sensor hardware from Wiliot with network connectivity, kitting, and field installation. The service expands the operator role from connectivity provider to solutions integrator, pulling more deployment value into managed-service contracts for large fleets.

- June 2026: Qualcomm announced a definitive agreement to acquire Modular Inc, adding software capabilities aimed at generative and agentic AI across edge and data center environments. For cellular IoT, the additional edge software assets strengthen platform stickiness around on-device intelligence and lifecycle management that sits alongside modem and module roadmaps.

- June 2024: AT&T launched 5G RedCap on its standalone network in Dallas, enabling device vendors to certify RedCap products on a live 5G SA environment. The launch provided a commercialization path for mid-tier IoT devices that need 5G features without full 5G complexity, supporting operator and ecosystem readiness for RedCap-based designs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cellular IoT market is counted as global annual revenue generated from cellular-based connectivity for machines and non-handset devices, including the related hardware, software, and connectivity services delivered over licensed cellular networks.

Scope exclusions: We exclude unlicensed LPWAN connectivity, satellite-only IoT connectivity, and consumer handsets, even if they enable app-based device management.

Segmentation Overview

- By Component

- Hardware

- Modules / Chipsets

- Antennas

- Gateways and Routers

- Software

- Connectivity Management Platform

- Device Management

- Security Platform

- Data Analytics Platform

- Services

- Professional Services

- Managed Services

- Hardware

- By Technology

- 2G

- 3G

- 4G LTE (Cat-1/Cat-4)

- LTE-M

- NB-IoT

- 5G NR (eMBB and RedCap)

- Non-Terrestrial (Satellite NTN)

- By End-User Industry

- Automotive and Transportation

- Energy and Utilities

- Manufacturing and Industrial

- Healthcare

- Retail

- Consumer Electronics

- Agriculture

- Logistics and Supply Chain

- Smart Cities / Public Infrastructure

- By Application

- Asset Tracking

- Smart Metering

- Industrial Automation

- Remote Monitoring and Control

- Wearables and Personal Devices

- Smart Home Devices

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- GCC (Saudi Arabia, UAE, Qatar, etc.)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base on how cellular IoT demand is created and monetized across devices, modules, and connectivity plans. Public references were used to ground assumptions, such as ITU indicators, GSMA publications on cellular IoT and spectrum, OECD communications datasets, and national telecom regulator releases for subscription and coverage context.

We also reviewed sources that help translate activity into revenue, such as customs and trade statistics for electronics shipments, patent databases for cellular IoT related filings, and company filings plus investor presentations for pricing direction and product mix. Where needed, paid database subscriptions were used for company financials and intelligence, news and financials, and patent look-ups so basic inputs stay consistent across regions and time. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary inputs came from interviews and surveys with module and chipset ecosystem participants, connectivity providers, device makers, and system integrators, plus informed buyers in high-volume use cases such as smart metering, asset tracking, and industrial monitoring. We used these discussions to confirm adoption timing by region, typical connection pricing, and how LTE-M, NB-IoT, and early 5G IoT deployments are being budgeted and contracted, which then helped close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 19% | APAC: 37% |

| Mid tier: 50% | Functional/Unit leaders: 35% | EMEA: 36% |

| Smaller Players: 22% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool reconstruction, where cellular IoT revenue is derived by mapping the installed base and net adds of cellular-connected devices to typical revenue per connection and associated enablement spend, then extended by technology mix. To keep the model grounded, selective bottom-up approximations were used as checks, such as sampled ASP times shipment volumes for key module categories and channel discussions on connection pricing bands.

Key inputs that influence the totals include active cellular IoT connections by region, the LTE-M versus NB-IoT versus 4G and 5G share shift, average connectivity ARPU trends by contract length, module pricing erosion, and the pace of 2G and 3G sunsets that move devices into newer cellular standards. For forecasting, scenario analysis was used to reflect different rollout speeds and pricing paths, with assumptions tightened using expert views on operator coverage expansion and enterprise deployment cycles. Where granular splits were missing, we used conservative proxy ratios from adjacent public indicators and then re-tested them in interviews before finalizing.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals like connection growth, coverage expansion, and the implied spend per device, so the revenue line stays consistent with observable market activity. When a variance showed up, we revisited assumptions, re-validated outliers, and triggered follow-up calls if the change looked structural rather than noise.

Each estimate passes through multi-step analyst review, including logic checks on units, currency conversions, and year alignment, followed by a final sign-off review. The report is refreshed annually, and interim updates are made when major market events occur, such as large technology sunsets, regulatory moves, or step changes in pricing. Before delivery, a fresh pass is completed so clients receive the most current view that can be traced back to clear inputs.

Mordor Intelligence's Cellular IOT Market Size Compared Against Other Published Estimates

Published cellular IoT market values often differ, even when the topic name looks the same, because the revenue items counted and the timing of conversion into USD are not always aligned. Differences in what is treated as cellular IoT revenue, and whether older generation connections and platform layers are included, also tend to widen the spread.

A refresh-led gap shows up when module ASP erosion and connectivity pricing are updated at different points in the year, or when FX timing is handled differently across multi-region totals. In addition, some estimates appear to blend broader IoT connectivity or adjacent device categories, while others focus mainly on connections, which changes the implied pricing math. By re-checking pricing bands and applying consistent currency timing close to publication, Mordor Intelligence reduces drift that can occur when earlier-year assumptions are carried forward without re-validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.34 B (2026) | |

| Global Consultancy A | USD 7.53 B (2024) | Uses an earlier base year and may emphasize connectivity revenue more heavily, which can undercount device-side and enablement revenue when multi-year enterprise rollouts are still ramping. |

| Trade Publisher B | USD 4.90 B (2024) | Appears to apply a narrower revenue scope and a different ASP progression, which can compress totals when module price declines and FX timing are not refreshed in step with contract repricing. |

The table mainly shows that scope boundaries and timing choices can move the number by several billion dollars, even before forecasting assumptions are debated. When the counted revenue lines are clearly separated and the pricing and FX inputs are refreshed and re-checked, the resulting market size becomes easier to reconcile with connection and deployment signals, and it stays more repeatable year to year.

Key Questions Answered in the Report

What is the current size of the cellular IoT market?

The cellular IoT market reached USD 9.34 billion in 2026 and is projected to climb to USD 25.71 billion by 2031.

Which region leads the cellular IoT market?

Asia Pacific holds 69.60% revenue share and is predicted to grow at 28.60% CAGR through 2031, driven by large-scale smart-city and manufacturing initiatives.

Why is 5G RedCap important for cellular IoT?

5G RedCap balances higher data rates with lower power and cost, enabling mid-tier devices such as industrial sensors and wearables to migrate from LTE without the complexity of full 5G.

Which application segment is growing fastest?

Wearables and personal devices are forecast to expand at a 27.90% CAGR thanks to health-monitoring adoption and power-efficient RedCap modules.

How are module prices affecting adoption?

Sub-USD 4 Cat-1bis modules from Asia Pacific suppliers lower the cost barrier, accelerating the replacement of 2G/3G devices before network sunsets.

What challenges could slow cellular IoT deployment?

High 5G module power draw for battery devices, retrofit costs from legacy network shutdowns, and fragmented security standards are key restraints highlighted in the forecast period.

Page last updated on: