Ultrasound Needle Guides Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

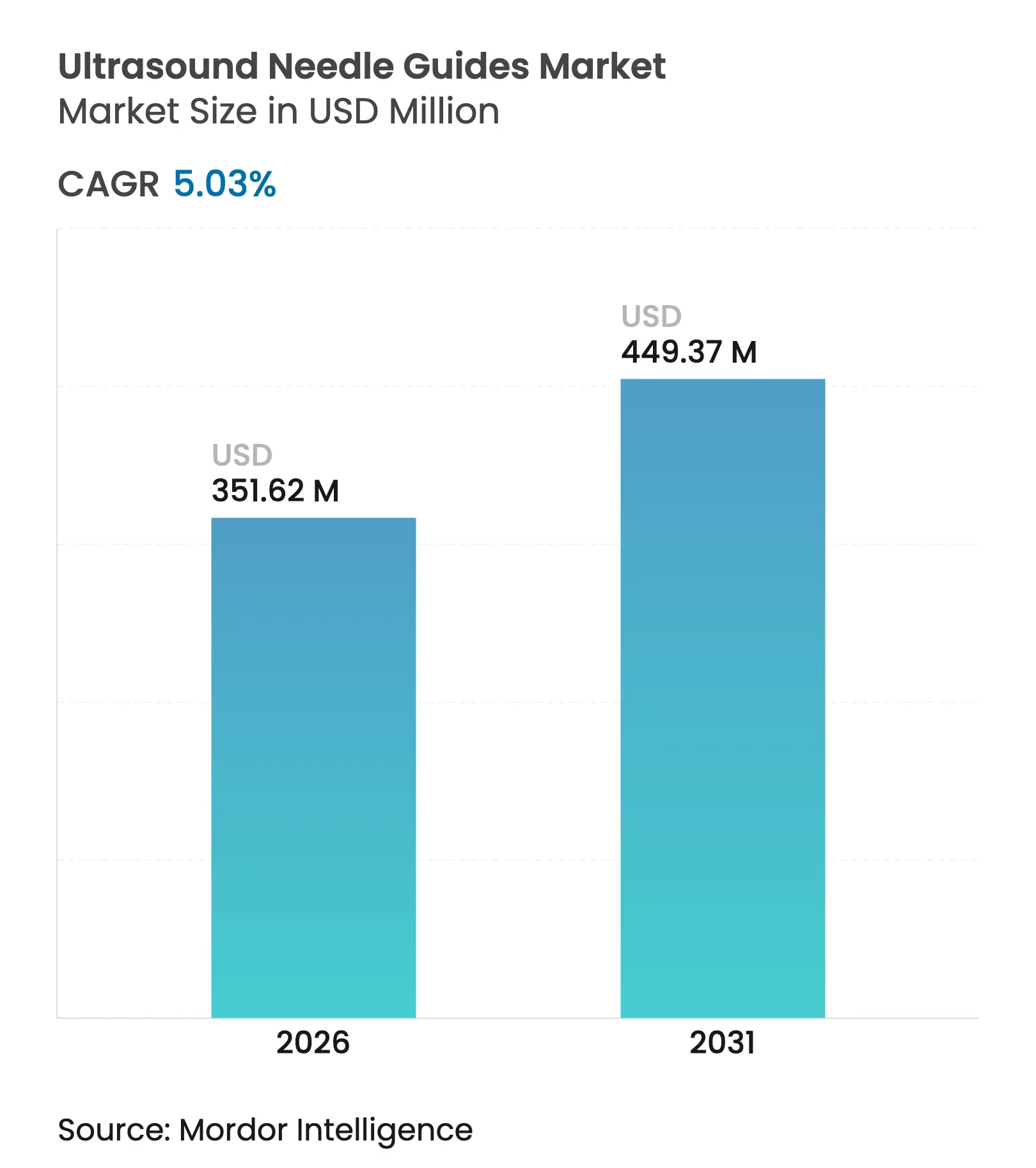

| Market Size (2026) | USD 351.62 Million |

| Market Size (2031) | USD 449.37 Million |

| Growth Rate (2026 - 2031) | 5.03 % CAGR |

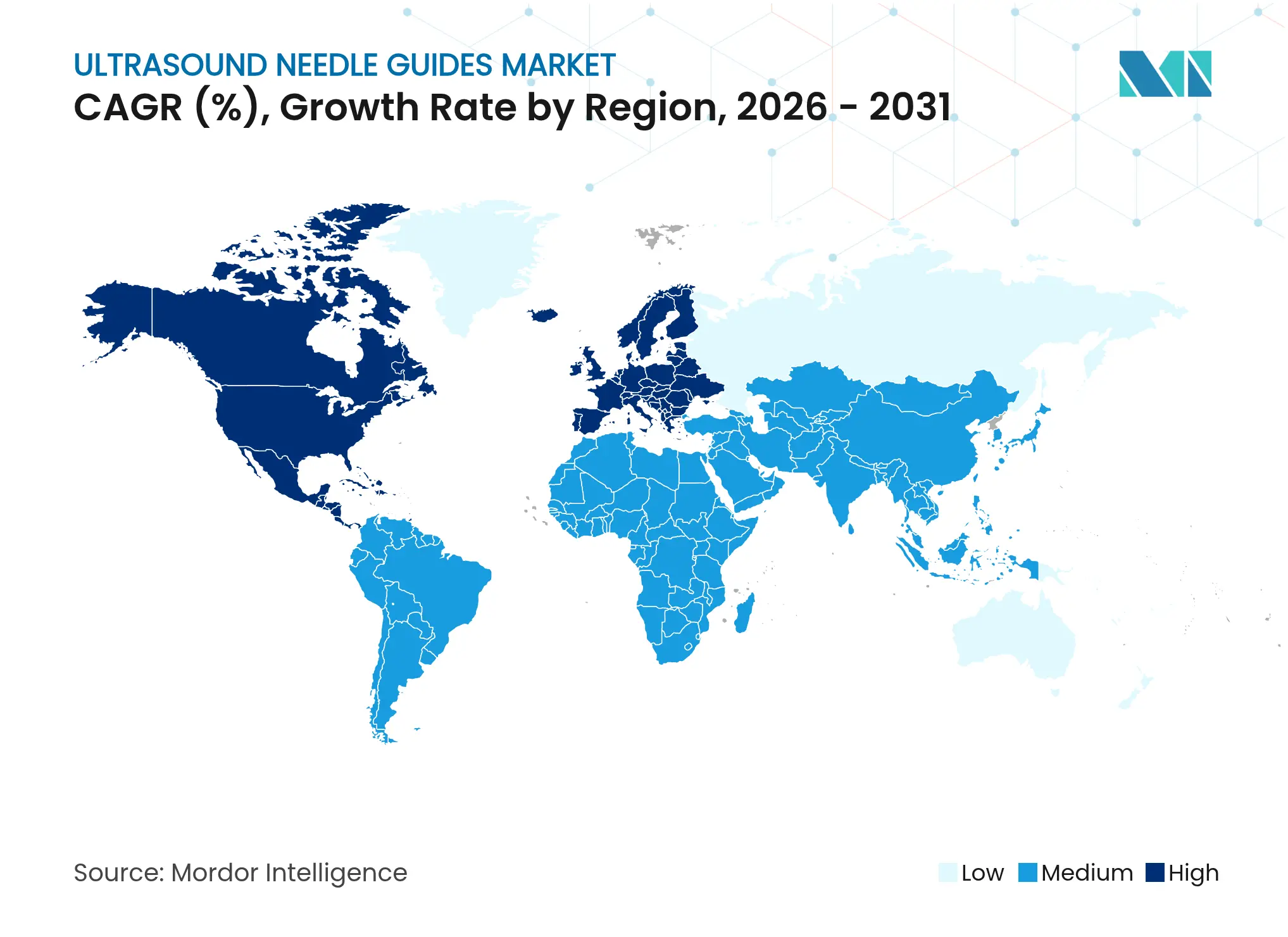

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ultrasound Needle Guides Market Analysis by Mordor Intelligence

The ultrasound needle guides market size was valued at USD 334.79 million in 2025 and estimated to grow from USD 351.62 million in 2026 to reach USD 449.37 million by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). Rapid uptake of precision-guided interventions, mounting emphasis on infection prevention, and the entry of AI-assisted visualization tools collectively sustain positive momentum for the ultrasound needle guides market despite its maturation phase. Product development now centers on tighter integration between disposable guide kits and next-generation ultrasound consoles, allowing facilities to raise first-pass accuracy while curbing procedure times. Hospitals remain pivotal demand hubs; however, ambulatory surgical centers (ASCs) are emerging as a crucial volume channel as outpatient models steadily displace inpatient care in North America and parts of Europe. Geographical expansion continues in Asia-Pacific where health-system modernization programs and aging demographics create durable tailwinds for the ultrasound needle guides market.

Key Report Takeaways

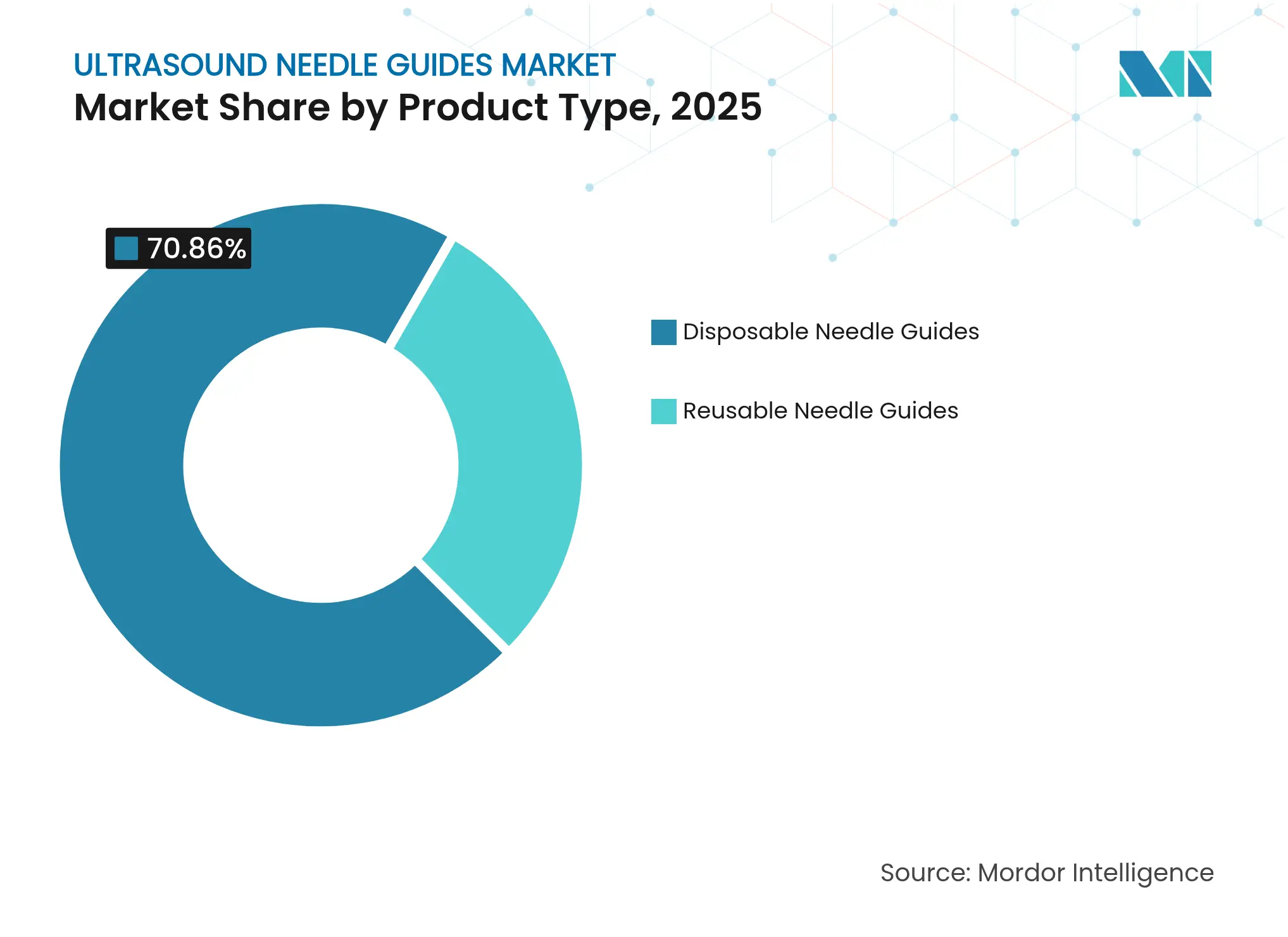

- By product type, disposable needle guides led with 70.86% of the ultrasound needle guides market share in 2025.

- By product type, reusable needle guides are projected to expand at a 5.82% CAGR through 2031.

- By application, biopsy procedures accounted for 43.20% share of the ultrasound needle guides market size in 2025.

- By application, pain-management procedures are advancing at a 5.95% CAGR through 2031.

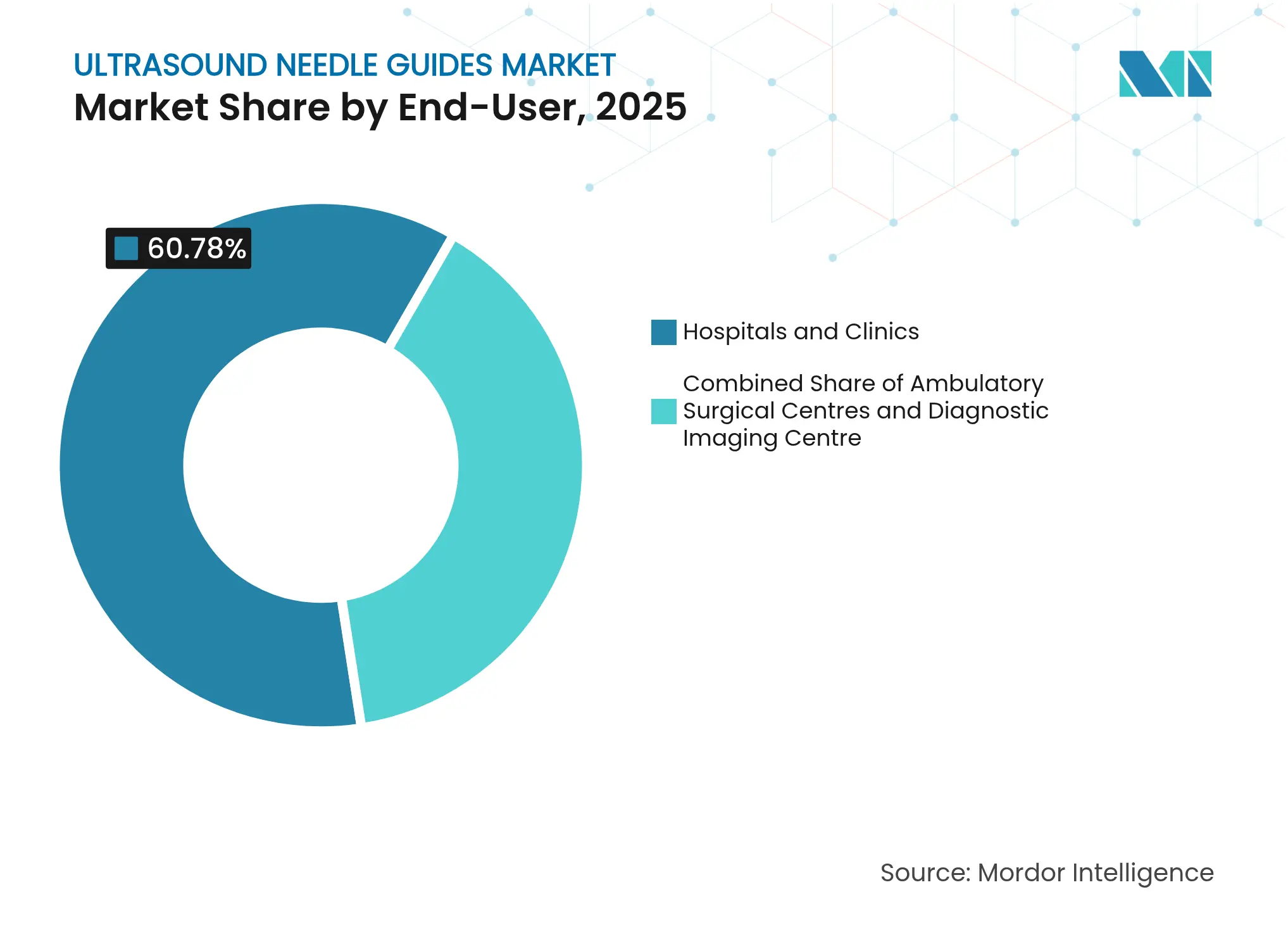

- By end-user, hospitals and clinics commanded 60.78% revenue in 2025, while ASCs record the highest forecast CAGR at 5.84% to 2031.

- By geography, North America held 41.75% share in 2025; Asia-Pacific is set to rise at a 6.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrasound Needle Guides Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising adoption of minimally-invasive ultrasound-guided

procedures

Rising adoption of minimally-invasive ultrasound-guided

procedures

| +1.2% | Global, North America & EU lead | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, North America & EU lead

|

Impact Timeline

:

Medium term (2-4 years)

|

Advancements in ultrasound imaging & needle

visualization

Advancements in ultrasound imaging & needle

visualization

| +0.9% | Global, developed markets | Long term (≥ 4 years) | |||

Growing prevalence of chronic diseases needing biopsy or

vascular access

Growing prevalence of chronic diseases needing biopsy or

vascular access

| +0.8% | Global, APAC fastest | Long term (≥ 4 years) | |||

Investments in point-of-care & handheld ultrasound

devices

Investments in point-of-care & handheld ultrasound

devices

| +0.7% | APAC core, spill-over to MEA | Medium term (2-4 years) | |||

Infection-control switch to sterile single-use transducer

covers

Infection-control switch to sterile single-use transducer

covers

| +0.6% | Global, regulatory-driven | Short term (≤ 2 years) | |||

AI-enabled needle-tracking algorithms unlocking next-gen

guide designs

AI-enabled needle-tracking algorithms unlocking next-gen

guide designs

| +0.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Adoption of Minimally-Invasive Ultrasound-Guided Procedures

Health-systems worldwide emphasize minimally-invasive care that reduces patient trauma and shortens recovery, positioning ultrasound guidance as the default approach for vascular access, regional anesthesia, and tissue biopsy. The U.S. Army Institute of Surgical Research and MIT Lincoln Laboratory demonstrated an AI-enabled nerve-block device that allows frontline medics to achieve expert-level results in under 40 seconds, underscoring technology’s role in closing skill gaps. Clinical evidence shows ultrasound-guided nerve blocks decrease opioid use and postoperative pain scores, fueling procedural adoption across emergency and perioperative settings. Electromagnetic tracking reduces average distance-to-target error by 57.1%, bolstering confidence among less-experienced operators. Reimbursement models that reward outcome-based care complement these clinical gains by lowering complication-related costs.

Advancements in Ultrasound Imaging & Needle Visualization

Software-centric innovation now supplements or even replaces hardware upgrades. Fujifilm Sonosite’s 2024 patent for on-screen out-of-plane markers exemplifies algorithms that overlay intuitive cues on legacy equipment, removing the need for specialized probes. Camera-based clip-on guidance modules from Clear Guide Medical furnish submillimeter precision while eliminating tedious calibration steps, broadening adoption among small clinics. Miniaturized electromagnetic sensors can adhere to existing probes without altering ergonomics, delivering real-time, three-dimensional tracking. These advances collectively democratize premium guidance capabilities, especially for facilities that cannot commit to full console upgrades.

Growing Prevalence of Chronic Diseases Needing Biopsy / Vascular Access

Chronic conditions such as liver disease, cancer, and kidney failure require repeated tissue sampling and vascular interventions, sustaining baseline demand for accurate needle placement. Ultrasound-guided percutaneous liver biopsy attains diagnostic yields above 95% while lowering complication rates, leading to guideline endorsement as the procedural standard. Rising oncology caseloads intensify the need for precise tissue acquisition to support molecular profiling. BD’s 2024 survey found 11% of patients experience ≥10 needlesticks for a single blood draw, highlighting deficiencies that guidance technologies aim to resolve. Outpatient management of chronic ailments further boosts demand for portable, user-friendly guide systems capable of delivering hospital-grade accuracy in ambulatory environments.

Investments in Point-of-Care & Handheld Ultrasound Devices

Capital is flowing into miniaturized ultrasound platforms that relocate imaging from radiology suites to bedside and remote settings. ThinkSono secured EUR 2.1 million in 2024 to commercialize an AI-guided deep-vein-thrombosis screening tool deployable by non-specialists. Smart Alpha promotes a cloud-connected pocket ultrasound promising “anywhere, anytime” imaging by general staff. Early studies on handheld robotic devices indicate femoral-vein cannulation in 80 seconds with novice users, signaling transformative potential for high-throughput outpatient centers. As these platforms pair with low-cost disposable guides, the ultrasound needle guides market broadens beyond traditional tertiary hospitals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage

Of Skilled Ultrasound Operators

Shortage

Of Skilled Ultrasound Operators

| -1.1% | Global, acute in developed markets | Medium term (2-4 years) |

(~)

% Impact on CAGR Forecast

:

-1.1%

|

Geographic

Relevance

:

Global,

acute in developed markets

|

Impact

Timeline

:

Medium

term (2-4 years)

|

High

Capital & Consumable Costs Of Advanced Guide Systems

High

Capital & Consumable Costs Of Advanced Guide Systems

| -0.8% | APAC & MEA, cost-sensitive markets | Short term (≤ 2 years) | |||

Sustainability

Mandates Curbing Single-Use Plastics In Hospitals

Sustainability

Mandates Curbing Single-Use Plastics In Hospitals

| -0.6% | Europe & North America, regulatory-driven | Medium term (2-4 years) | |||

Limited

Reimbursement For Ultrasound-Guided Pain-Management

Limited

Reimbursement For Ultrasound-Guided Pain-Management

| -0.4% | Global, with variations by healthcare system | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Skilled Ultrasound Operators

Diagnostic sonographers retire at an average age of 60.8 years, nearly three years earlier than the general labor force, creating a talent deficit during a period when ultrasound accounts for 45% of U.S. imaging volume. Training pipelines struggle to offset attrition, constraining procedure capacity in high-acuity hospitals and rural clinics alike. Complexity further amplifies the gap; ultrasound-guided regional anesthesia demands specialist expertise rarely available outside tertiary centers. Algorithmic guidance offers a mitigation path, yet broad clinical validation and user acceptance remain pending over the medium term.

High Capital & Consumable Costs of Advanced Guide Systems

Premium guidance platforms elevate precision but command price points beyond the budgets of many ASCs and public hospitals, especially in emerging economies. Reimbursement discrepancies compound the hurdle: Medicare payouts for ultrasound-guided pain interventions range from USD 36 to USD 118, often below fluoroscopy rates, diminishing ROI for new equipment. Sustainability pressures add layers of complexity as facilities balance disposable use against environmental goals. Comparative life-cycle analyses show 43% lower ecological footprint for reprocessed sleeves, nudging purchasing committees toward reusable alternatives that, in turn, require investment in validated sterilization workflows [1]Lichtnegger S. et al., “Single-Use and Reprocessed IPC Sleeves,” RMHP, dovepress.com .

Segment Analysis

By Product Type: Disposables Dominate Infection Control

Disposable needle guides held 70.86% of the ultrasound needle guides market share in 2025 as infection-control regulations tightened globally. Hospitals value the ready-to-use sterility of single-use kits that integrate with probe covers, lowering cross-contamination risk without lengthy reprocessing. CIVCO Medical Solutions’ Verza system underpins this dominance by marrying clip-on ease with procedure-specific sterile packs. In revenue terms, the ultrasound needle guides market size for disposables is forecast to climb to USD 318.62 million by 2031 as emerging markets adopt stringent hygiene protocols.

Reusable guides nonetheless advance at a 5.82% CAGR as sustainability directives gather force in Europe and certain U.S. health systems. Comparative life-cycle evidence highlights a 72.1% reduction in ozone-layer impact for reprocessed accessories, persuading procurement teams to weigh environmental savings against sterilization overheads. GE HealthCare’s lineup of autoclavable biopsy guides exemplifies how manufacturers hedge bets by offering hybrid portfolios that satisfy both infection-control and green-procurement stakeholders. Technological upgrades—such as laser-etched channels for enhanced echogenicity—bridge performance gaps between reusable and disposable options, accelerating acceptance among high-volume imaging centers.

Note: Segment shares of all individual segments available upon report purchase

By Application: Biopsy Procedures Lead Clinical Adoption

Biopsy procedures accounted for 43.20% of the ultrasound needle guides market size in 2025, reflecting oncology’s relentless demand for accurate, real-time tissue sampling. Subspecialties ranging from hepatology to interventional radiology rely on needle-guide kits to improve yield and minimize complications, qualities that resonate with value-based reimbursement models. Manufacturers focus on modular biopsy guides compatible with diverse gauge sizes to broaden platform versatility.

Pain-management applications present the fastest CAGR at 5.95% through 2031 as CPT code coverage expands for ultrasound-guided nerve blocks. Broader reimbursement fuels adoption in emergency departments and outpatient pain clinics, where clinicians seek alternatives to opioid analgesics. Vascular-access, fluid-drainage, and regional-anesthesia segments together sustain baseline sales by providing steady, high-frequency use cases vital to manufacturer recurring-revenue models. Ongoing AI integration promises to blur lines between these categories by allowing single platforms to address multiple applications without manual recalibration.

By End-User: ASCs Challenge Hospital Dominance

Hospitals and clinics retained 60.78% of 2025 sales because tertiary centers perform complex, imaging-intensive interventions requiring advanced guidance platforms. Integrated EMR and PACS architectures further entrench hospital purchasing power by facilitating bulk equipment bundles that include probes, sterile-barrier kits, and software licenses. Accordingly, the ultrasound needle guides market size for hospitals is projected to hit USD 281.2 million in 2031 as replacement cycles align with AI-enabled console launches.

ASCs, however, deliver the strongest growth trajectory at a 5.84% CAGR, propelled by procedural migration from inpatient floors to cost-efficient outpatient suites. Their lean business models focus on rapid turnover, pushing guide manufacturers to prioritize clip-on disposables and intuitive visualization overlays that minimize setup time. Diagnostic imaging centers occupy a niche defined by high biopsy volumes and stringent radiologist preference for precision hardware; they function as early adopters for cutting-edge accessories capable of boosting first-pass success and image clarity.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 41.75% of 2025 revenue due to mature ultrasound penetration, favorable reimbursement, and robust clinical training pipelines. Recent FDA guidance on diagnostic ultrasound systems offers clear predicates for 510(k) submissions, encouraging manufacturers to accelerate next-gen guide launches. Academic-industry consortia frequently trial AI-assisted needle-tracking algorithms in U.S. centers, translating into early commercial traction once clearances occur. Major hospital networks leverage scale to negotiate bundle contracts that include guide kits, sterile probe covers, and software maintenance, cementing vendor relationships for multiyear cycles.

Europe follows with entrenched infection-control standards and rigorous environmental directives that collectively shape purchasing patterns. Reusable guide systems gain greater relative acceptance here than in North America, supported by centralized sterilization services and cross-country green procurement mandates. Product launches like the Clarius-ThinkSono AI-guided platform resonate with European clinicians who value software-centric solutions compliant with MDR regulations. Evidence-driven healthcare culture further necessitates peer-reviewed validation, steering vendors toward multicenter clinical studies prior to market access.

Asia-Pacific registers the fastest CAGR at 6.08% through 2031, underpinned by expanding health budgets in China, India, and Southeast Asia. Government incentives to deepen medical-device localization, coupled with accelerating physician adoption of ultrasound, provide fertile ground for guide manufacturers. APACMed’s 2024 white paper forecasts substantial economic and clinical benefits from AI in interventional imaging, reinforcing the region’s appetite for algorithm-driven guidance . However, cost pressures necessitate value-engineered products, driving multinational suppliers to launch tiered portfolios that balance essential functionality with affordability. Local OEMs meanwhile leverage proximity to high-growth markets to pilot frugal-innovation models that can later scale globally.

The Middle East & Africa and South America comprise smaller but steadily expanding shares on the back of private-sector hospital construction and telehealth initiatives that widen access to ultrasound-based procedures. Multinational aid agencies often fund procurement of portable scans and accompanying guide kits in remote clinics, forging early brand familiarity that vendors can convert into long-term relationships as incomes rise.

Competitive Landscape

Market Concentration

The ultrasound needle guides market remains moderately fragmented; no single player exceeds a 25% share, yet the top five firms collectively hold a commanding position by virtue of differentiated portfolios. CIVCO Medical Solutions sustains leadership through broad probe compatibility and partnerships with console OEMs; its Verza disposable kit remains a flagship offering favored in infection-control sensitive environments civco.com. Boston Scientific leverages cross-disciplinary device experience to introduce integrated biopsy systems that marry echogenic needle designs with proprietary ultrasound consoles. Becton Dickinson focuses on vascular-access innovations, aligning guide accessories with catheter insertion platforms to present closed-loop solutions that enhance procedural hygiene.

Strategic collaborations intensify technology convergence. In 2024 Smith+Nephew partnered with JointVue to integrate ultrasound-based preoperative planning into orthopedic robotics, creating cross-selling opportunities for needle-guide accessories [3]Smith+Nephew, “Smith+Nephew Partners with JointVue for Ultrasound Preoperative Planning,” smith-nephew.com . Mendaera raised USD 73 million in Series B financing to accelerate handheld robotic guidance platforms, subsequently inking an agreement with EchoNous to merge robotics with ultrasound imaging. Patent activity likewise accelerates: Fujifilm Sonosite’s 2024 filing outlines dynamic on-screen guides for needles inserted out of the imaging plane, reflecting a move toward software innovation that reduces hardware dependence.

Emerging competitors exploit AI to sidestep hardware incumbency. ThinkSono and Smart Alpha emphasize algorithm-based needle detection on commodity probes, seeking entry in resource-constrained markets that prioritize low capital outlay. Reimbursement alignment and clinician trust represent barriers, but successful proof-of-concept pilots in Europe suggest impending commercial adoption. The net result is a competitive environment where legacy device makers and software-first entrants vie for ecosystem control, compelling continuous R&D investment and partnership formation.

Ultrasound Needle Guides Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mermaid Medical Group received UKCA approval for the TP Pivot Pro disposable needle guide developed by CIVCO Medical Solutions, offering 20-degree needle angulation for enhanced access.

- November 2024: DeepSight Technology showcased NeedleVue LiteCart at RSNA 2024, providing real-time needle visualization without radiation or complex calibration.

- September 2024: RIVANNA obtained a U.S. patent for an ultrasound-guided needle-insertion system aimed at improving accuracy in diverse procedures.

- November 2023: BD introduced the SiteRite 9 Ultrasound System featuring Cue needle-tracking, enhancing catheter placement efficiency.

Table of Contents for Ultrasound Needle Guides Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Adoption Of Minimally-Invasive Ultrasound-Guided Procedures

- 4.2.2Advancements In Ultrasound Imaging & Needle Visualisation

- 4.2.3Growing Prevalence Of Chronic Diseases Needing Biopsy / Vascular Access

- 4.2.4Investments In Point-Of-Care & Handheld Ultrasound Devices

- 4.2.5Infection-Control Switch To Sterile Single-Use Transducer Covers

- 4.2.6Ai-Enabled Needle-Tracking Algorithms Unlocking Next-Gen Guide Designs

- 4.3Market Restraints

- 4.3.1Shortage Of Skilled Ultrasound Operators

- 4.3.2High Capital & Consumable Costs Of Advanced Guide Systems

- 4.3.3Sustainability Mandates Curbing Single-Use Plastics In Hospitals

- 4.3.4Limited Reimbursement For Ultrasound-Guided Pain-Management

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value – USD)

- 5.1By Product Type

- 5.1.1Disposable Needle Guides

- 5.1.2Reusable Needle Guides

- 5.2By Application

- 5.2.1Biopsy Procedures

- 5.2.2Regional Anaesthesia

- 5.2.3Vascular Access

- 5.2.4Fluid Aspiration & Drainage

- 5.2.5Pain Management

- 5.2.6Other Interventional Procedures

- 5.3By End-User

- 5.3.1Hospitals & Clinics

- 5.3.2Ambulatory Surgical Centres

- 5.3.3Diagnostic Imaging Centres

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Roper Technologies (CIVCO Medical Solutions)

- 6.3.2Aspen Surgical Products

- 6.3.3FUJIFILM Sonosite

- 6.3.4Becton, Dickinson & Co.

- 6.3.5Argon Medical Devices

- 6.3.6Remington Medical

- 6.3.7Geotek Medical

- 6.3.8Rocket Medical

- 6.3.9BIRR

- 6.3.10Sheathing Technologies

- 6.3.11weLLgo Medical Products

- 6.3.12GE HealthCare

- 6.3.13Boston Scientific

- 6.3.14Cook Medical

- 6.3.15Smiths Medical

- 6.3.16Medline Industries

- 6.3.17Philips Healthcare

- 6.3.18Clarius Mobile Health

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Ultrasound Needle Guides Market Report Scope

Ultrasound needle guides are medical devices or accessories designed to work alongside ultrasound systems, ensuring precise and safe needle positioning during various medical procedures such as biopsy procedures and regional anesthesia, among others. The ultrasound needle guides market is segmented by product type, application, end-user and geography. By product type, the market is segmented into disposable needle guides and reusable needle guides. By application, the market is segmented into biopsy procedures, regional anesthesia, vascular access, fluid aspiration and drainage procedures, pain management and other interventional procedures. Other interventional procedures include tumor ablation, and musculoskeletal interventions, among others. By end-user, the market is segmented into hospitals and clinics, ambulatory surgical centers and diagnostic imaging centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.