Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

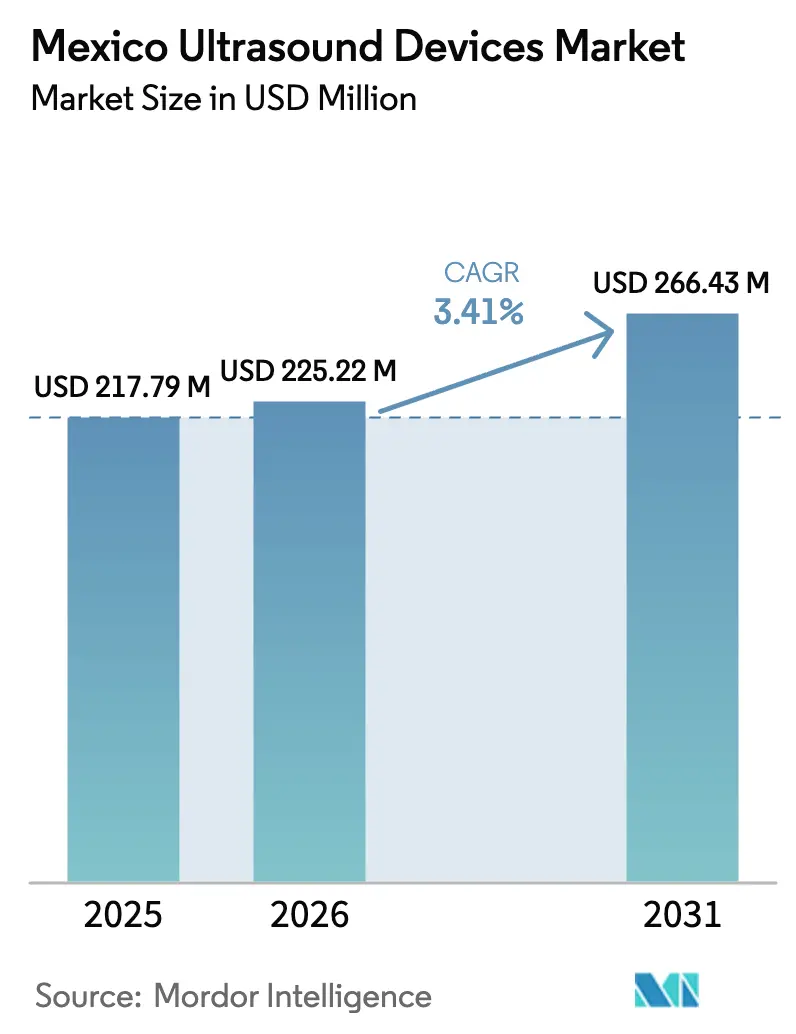

| Base Year Market Size (2025) | USD 217.79 Million |

| Market Size (2026) | USD 225.22 Million |

| Market Size (2031) | USD 266.43 Million |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Ultrasound Devices Market Analysis by Mordor Intelligence

The Mexico Ultrasound Devices Market size is expected to grow from USD 217.79 million in 2025 to USD 225.22 million in 2026 and is forecast to reach USD 266.43 million by 2031 at 3.41% CAGR over 2026-2031.

This measured trajectory stems from synchronized growth in private and public hospital construction, accelerating replacement of obsolete imaging fleets, and steady uptake of AI-enabled point-of-care systems. Expansion plans announced by the Instituto Mexicano del Seguro Social (IMSS) to open nine hospitals and six Family Medicine Units in 2025 underscore how new capacity will anchor demand for mid-range cart-based and premium 3D/4D consoles. Meanwhile, peso volatility, fresh 4-8% import tariffs, and uneven distribution of certified sonographers temper nationwide deployment, keeping the Mexico ultrasound devices market on a moderate but resilient growth path through the decade. Mexico’s standing as Latin America’s second-largest medical-device hub and seventh-largest exporter continues to attract multinational manufacturing investments that help shorten replacement cycles and localize service support.

Key Report Takeaways

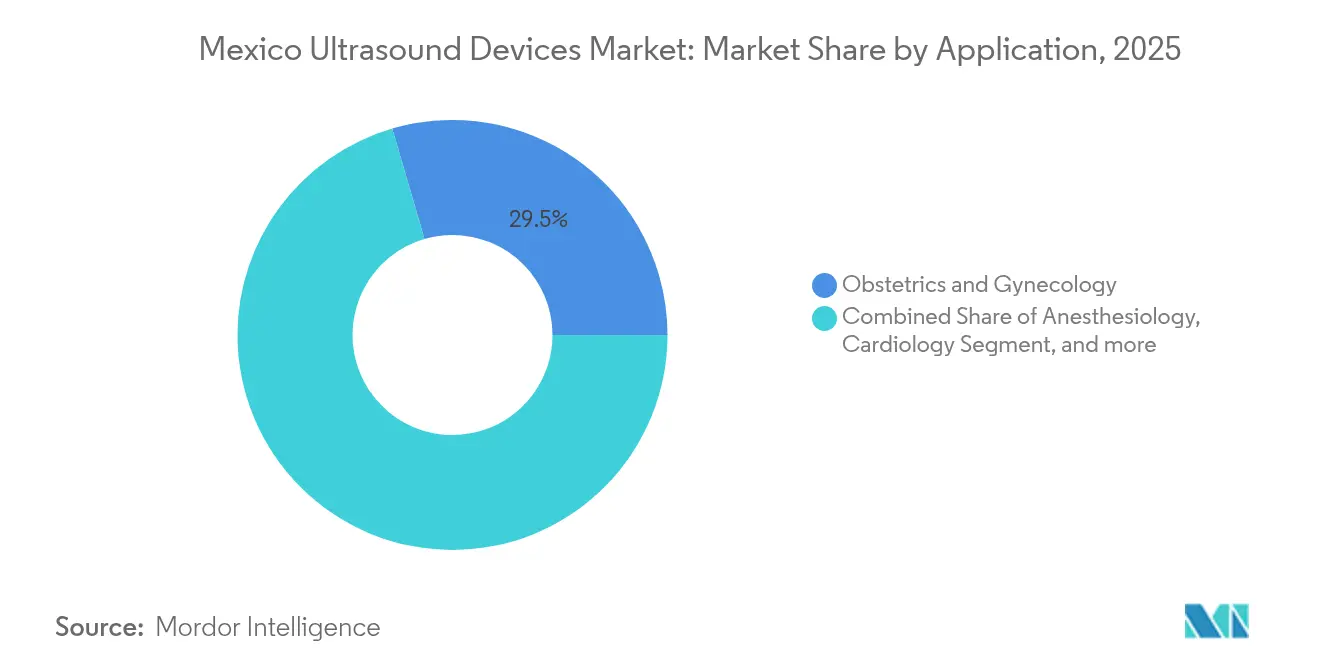

- By application, obstetrics & gynecology led with 29.52% of the Mexico ultrasound devices market share in 2025; anesthesiology is projected to record the fastest 5.86% CAGR through 2031.

- By technology, 3D & 4D systems dominated with a 45.62% revenue share in 2025, while high-intensity focused ultrasound is poised for the highest 5.36% CAGR to 2031.

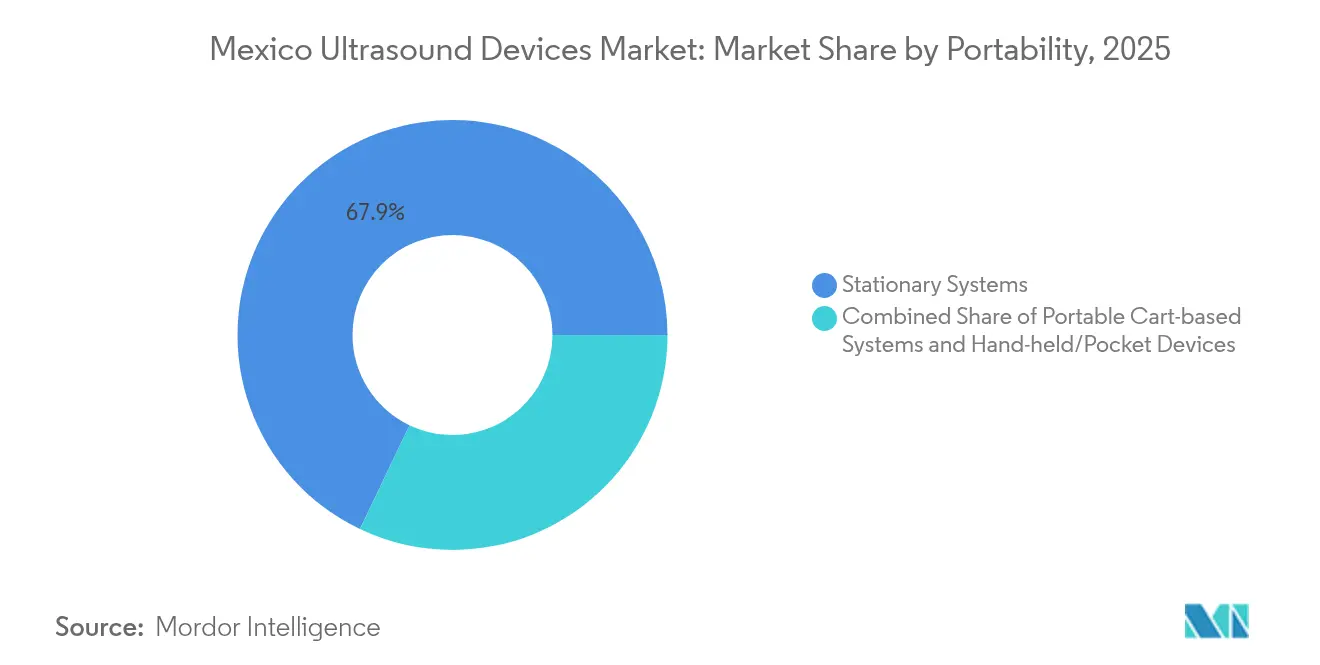

- By portability, stationary systems held 67.92% of the Mexico ultrasound devices market size in 2025, and hand-held/pocket devices are set to expand at a 7.22% CAGR between 2026-2031.

- By end user, hospitals commanded 59.03% revenue share in 2025, whereas diagnostic imaging centers will outpace all peers at a 6.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & metabolic conditions | +0.8% | Urban hubs nationwide | Medium term (2-4 years) |

| Demographic shifts: aging population & high-risk pregnancies | +0.6% | Northern corridor | Long term (≥4 years) |

| Surge in private healthcare investment & hospital expansion | +0.9% | Mexico City, Guadalajara, Monterrey | Short term (≤2 years) |

| Government-led tele-ultrasound pilots in underserved regions | +0.4% | Chiapas, Guerrero, Oaxaca | Medium term (2-4 years) |

| Cross-border medical tourism driving imaging demand | +0.3% | Baja California, Sonora, Chihuahua | Short term (≤2 years) |

| Technological advancements in portable & AI-enabled ultrasound | +0.5% | Tier-1 cities nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Metabolic Conditions

Diabetes prevalence reached 10.3% in 2024, translating into 2.6 million Mexicans who require continuous monitoring, yet only 37.1% access public health services, leaving effective coverage at 9.3%.[1]Héctor Gallardo-Rincón et al., “Effective Coverage of Diabetes Care in Mexico,” insp.mx Ultrasound-guided nephrology protocols, promoted by the Mexican College of Nephrologists, support early detection of diabetic kidney disease by enabling albuminuria evaluation and vascular flow assessment. Concentration of endocrinology clinics in Mexico City, Monterrey, and Guadalajara magnifies regional demand clustering. Portable point-of-care units allow family physicians to perform renal, hepatic, and vascular scans during routine visits, easing referral backlogs. Replacement of legacy grayscale consoles older than 10 years 27% of the national ultrasound stock remains a parallel volume driver.

Demographic Shifts: Aging Population & High-Risk Pregnancies

Mexico’s population reached 130.9 million in 2025, with fertility dropping and life expectancy climbing, resulting in dual pressure on maternal-fetal and geriatric imaging services. The maternal mortality ratio of 59.1 per 100,000 live births contrasts sharply with OECD averages, and only 61.8% of pregnant women receive full antenatal protocols.[2]Pan American Health Organization, “Regional Maternal Mortality Data 2024,” paho.org Advanced 3D/4D scanners improve fetal anomaly detection, allowing obstetricians to act earlier on high-risk pregnancies exacerbated by obesity and hypertension. In geriatrics, households spend USD 308.9 per hospitalization episode, nudging insurers and hospital groups toward preventive abdominal and vascular screening programs that rely on color Doppler and elastography functions. Northern states, where multispecialty geriatric clinics integrate tele-consults with U.S. vascular surgeons, become early adopters of AI-aided echocardiography.

Surge in Private Healthcare Investment & Hospital Expansion

Private operators favor premium ultrasound suites because reliable power and chilled water supply enable the high duty cycles needed for 18–24-hour imaging rosters. IMSS’s 2025 rollout of new hospitals in Ensenada and Tuxtla Gutiérrez injects fresh procurement rounds for mid-tier consoles and bedside POCUS systems. President Claudia Sheinbaum’s healthcare reform package, unveiled in January 2025, allocates funds to expand digitalization, electronic health records, and integrated radiology information systems, accelerating replacement of standalone ultrasound workstations. Private maternity centers record 92.5% C-section rates compared with 51.3% in IMSS facilities, driving proportionally higher scan volumes per delivery.

Government-Led Tele-Ultrasound Pilots in Underserved Regions

The Universidad Nacional Autónoma de México’s AI-enabled remote fetal-brain Doppler platform allows general practitioners in Oaxaca to stream images to perinatologists in Mexico City over WiMAX links, reducing unnecessary transfers.[3]Universidad Nacional Autónoma de México, “AI-Enabled Tele-Ultrasound Platform,” unam.mx Chiapas’ longitudinal POCUS curriculum trained rural doctors to perform 584 studies in 12 months using battery-operated handhelds, changing diagnosis in 58% of obstetric cases. Limited bandwidth and sonographer shortages slow nationwide scale-up; nevertheless, suppliers of pocket probes and cloud-based PACS benefit from steady pilot funding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified sonographers & biomedical engineers | -0.7% | Nationwide, acute in rural zones | Long term (≥4 years) |

| Peso volatility impacting import costs of high-end equipment | -0.5% | All import-dependent facilities | Short term (≤2 years) |

| Delayed reimbursement for point-of-care ultrasound (POCUS) | -0.3% | Public hospitals | Medium term (2-4 years) |

| Infrastructure gaps & uneven access to imaging services | -0.4% | Chiapas, Guerrero, Oaxaca | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Sonographers & Biomedical Engineers

Average retirement age among Mexican sonographers has fallen to 60.8 years due to pandemic burnout and workload stress, worsening the existing 60,000-person healthcare workforce gap in low-density states. Only five radiology master’s programs operate outside the Mexico City-Monterrey-Guadalajara triangle, so equipment donations often sit idle in rural hospitals. Manufacturers now bundle remote training portals and AI-guided scanning to offset head-count shortages, but accreditation bottlenecks remain a structural brake.

Peso Volatility Impacting Import Costs of High-End Equipment

The 2025 tariff package adds 4–8% duties on most ultrasound categories, and a 10% pesodollar swing can alter console quotes by USD 8,000–10,000 per unit. Hospitals negotiating in pesos face budget overruns, prompting deferrals or substitution toward domestically assembled sub-components. COFEPRIS registration fees of USD 5,000–10,000 and review cycles lasting up to 18 months further raise the entry barrier for niche innovators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Maternal Care Dominance Amid Anesthesiology Surge

Obstetrics & gynecology generated the largest slice of the Mexico ultrasound devices market equaling 29.52% share thanks to mandated trimester scans under social-insurance guidelines. Anesthesiology is accelerating at a 5.86% CAGR because regional blocks and vascular access guided by ultrasound cut perioperative complications, pushing trauma centers and ambulatory surgery sites to add compact systems at each operating theater. In intensive-care units, cardiologists rely on quantitative hemodynamic protocols that use advanced Doppler to stratify shock, raising utilization rates for cardiac probes. Musculoskeletal and vascular sub-segments benefit from sports-medicine growth and diabetic foot surveillance, respectively, albeit from smaller revenue bases.

The Mexico ultrasound devices market continues to experience quality-of-care scrutiny in prenatal imaging as 52% of mothers rate first antenatal visits as fair or poor, prompting regulatory pressure for high-resolution abdominal transducers and AI-aided anomaly detection. Guanajuato’s universal prenatal screening initiative, executed through trained general practitioners, illustrates scalable demand for compact high-frequency probes in semi-urban municipalities. Cardiology advocates are piloting AI-driven speckle-tracking modules to reduce inter-operator variability, signaling an upgrade cycle that will permeate secondary hospitals over the next five years.

By Technology: 3D/4D Leadership Faces HIFU Innovation

3D & 4D consoles captured 45.62% revenue in 2025, due largely to obstetricians’ preference for volumetric fetal imaging that enhances anomaly detection and parental engagement. High-Intensity Focused Ultrasound is projected to rise at 5.36% CAGR owing to expanding indications for uterine fibroid ablation and palliative oncology care in private centers catering to medical tourists.

Traditional 2D systems continue to dominate public hospital tenders because unit prices sit 25–40% below premium platforms. Yet the Mexico ultrasound devices market is seeing rapid cross-grade sales as suppliers embed AI beam-forming in mid-range 2D carts, narrowing the performance gap. Doppler imaging units gain momentum via diabetic nephropathy follow-up and peripheral vascular disease screening. Early adopters in Guadalajara are piloting contrast-enhanced liver protocols, indicating that elastography and AI post-processing will further diversify product mixes.

By Portability: Stationary Dominance Challenged by Handheld Innovation

Stationary room-based consoles held 67.92% of the Mexico ultrasound devices market share in 2025 as tertiary hospitals still favor fully featured systems linked to PACS networks. Handheld probes typified by sector-wide evaluations reporting 92.9% sensitivity for abdominal pathology and grows with 7.22% by 2031. Manufacturers bundle cloud-reporting dashboards so obstetricians in Oaxaca can upload images for remote review, aligning with IMSS telehealth priorities.

Cart-based portables straddle both utility and mobility, especially in ED resuscitation bays where trauma surgeons need immediate pericardial and FAST assessments. Service contracts increasingly include back-up batteries and rugged transport cases to offset internal logistics hurdles such as elevator downtime and corridor congestion in aging public facilities. Hand-held adoption, however, depends on reimbursement codes catching up with clinical practice; until then, procurement committees often opt for mid-range carts to satisfy multiple departments under a single capital outlay.

By End User: Hospital Centralization Amid Diagnostic Center Growth

Hospitals accounted for 59.03% of the Mexico ultrasound devices market size owing to integrated care models where one console supports obstetrics, cardiology, and emergency diagnostics. The ISSSTE network’s radiology information system, covering 40 hospitals and 2 million annual studies, exemplifies centralized image governance that boosts utilization rates. Diagnostic imaging centers are gaining ground, expanding at 6.71% CAGR, because outpatient pathways reduce patient wait times by 30-40% compared to public hospitals.

Other end-users urgent-care clinics, ambulatory surgery centers, and sports-medicine practices collectively form a niche but vibrant space, especially in Mexico City’s private healthcare ecosystem. Vendors address this cluster by offering subscription-based device leases to manage capital constraints amid peso fluctuations. As reimbursement evolves, the Mexico ultrasound devices industry is likely to see bundled service models where device, software, and tele-interpretation come under a single monthly fee.

Geography Analysis

Mexico’s heterogeneous healthcare geography shapes device demand along three distinct corridors. The northern manufacturing belt Baja California, Sonora, and Chihuahua benefits from clusters of Philips, Siemens, and Medtronic plants that confer 25% lower production costs versus the United States, shortening lead times for replacement parts and consoles. Hospitals in these states maintain higher ultrasound-to-population ratios and are early adopters of High-Intensity Focused Ultrasound for oncology tourism programs. Monterrey’s private health complexes further elevate regional scan volumes through package procedures aimed at expatriates and U.S. retirees.

Central Mexico, anchored by the Mexico City metropolitan area, houses academic teaching hospitals and national institutes that drive research and training. The region exhibits the country’s highest console density and earliest adoption of AI beam-forming and contrast-enhanced protocols. IMSS’s 2025 infrastructure plan will bolster secondary cities such as Querétaro and Puebla, redistributing a portion of patient flow and spreading demand for mid-range carts. Yet public-sector institutions continue to grapple with maintenance backlogs and funding cycles tied to federal budgets, often delaying high-end replacements.

Southern states Chiapas, Guerrero, and Oaxaca account less market share in the ultrasound installations yet hold the highest unmet need. Tele-ultrasound pilots have proven capable of closing diagnostic gaps by connecting rural clinics with Mexico City specialists using IEEE 802.22 networks. Pilot data reveal reduced patient transfers by 40% and quicker obstetric referrals, but sustainability hinges on expanding broadband coverage and onsite sonographer training. As handheld devices circumvent power and cooling constraints, suppliers that offer bundled solar chargers and waterproof probes are poised to carve out share in these underserved zones.

Competitive Landscape

Mexico’s ultrasound arena reflects moderate concentration. Firms leverage proximity to U.S. supply chains, COFEPRIS regulatory familiarity, and embedded manufacturing footprints to maintain pricing leverage. Philips and Siemens capitalize on maquiladora tax incentives to assemble consoles in Baja California, ensuring rapid parts replacement and bilingual field support. GE Healthcare, post-acquisition of Intelligent Ultrasound’s AI suite, integrated ScanNav Anatomy into its Voluson SWIFT line, offering automated labeling that cuts scanning time by 20% for obstetricians.

Handheld disruptors Butterfly Network, Clarius, and Shenzhen-based Mindray—pursue subscription models that bundle cloud storage and AI organ-recognition, appealing to private emergency rooms that pay in pesos and thus fear exchange-rate spikes. Comparative studies in Mexico City EMS units showed 79.5% agreement between prehospital handheld scans and in-hospital cart-based findings, lending clinical credibility that supports tender approvals.

Regulatory timelines remain a competitive moat. Established brands exploit COFEPRIS equivalency pathways, cutting clearance to 6-12 months, versus 18 months for newcomers. Yet tariff hikes have nudged even incumbents to increase local content: transducer cabling and plastic housings are now sourced from Mexican SMEs under supplier-development programs backed by state governments in Nuevo León and Jalisco. Vendors that align with federal tele-medicine initiatives offering APIs for secure image push to national PACS score higher in public tenders, signaling that software interoperability is now as critical as hardware specifications.

Mexico Ultrasound Devices Industry Leaders

GE Healthcare

Siemens AG

Fujifilm Holdings Corporation

Koninklijke Philips N.V.

Canon Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Canon Medical will participate in the ISUOG World Congress 2025, held in Cancún, Mexico, from September 14–17, marking a major milestone in its commitment to advancing ultrasound in Obstetrics and Gynecology. Following the success of ISUOG 2024 in Budapest, Canon Medical will unveil its latest innovations, including the new Aplio system for Women’s Health, designed to deliver exceptional imaging performance and diagnostic confidence across all stages of care from early pregnancy to complex gynecologic assessments.

- June 2025: EDAN Instruments, Inc. officially launched its new subsidiary, EDAN MEDICAL MÉXICO S de R.L. de C.V., marking a strategic expansion into Latin America. The milestone was celebrated with a ribbon-cutting ceremony last Wednesday in Mexico City, underscoring EDAN’s commitment to strengthening its presence and service capabilities across the Americas. This move reflects EDAN’s long-term growth strategy to localize operations, enhance customer engagement, and deliver advanced medical technologies tailored to regional healthcare needs.

Mexico Ultrasound Devices Market Report Scope

As per the scope of the report, ultrasonography is an imaging method that creates images of various body structures using high-frequency sound waves. They are used to evaluate a variety of disorders relating to the liver, kidneys, and other abdominal conditions, including usage in pregnancy. As a result, these devices have a variety of uses in the medical area, including diagnostic imaging and therapeutic modality. Mexico ultrasound devices market is segmented by application, technology, and type. by application, the market is segmented as cardiology, gynecology/obstetrics, musculoskeletal, radiology, and other applications, by technology the market is segmented as 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging, and high-intensity focused ultrasound, and type the market is segmented as stationary ultrasound and portable ultrasound. The report offers the value (in USD) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Obstetrics & Gynecology |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Obstetrics & Gynecology | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Other End Users |

Key Questions Answered in the Report

What is the projected value of the Mexico ultrasound devices market by 2031?

The market is expected to reach USD 266.43 million by 2031 based on a 3.41% CAGR forecast.

Which application currently holds the largest revenue share?

Obstetrics & Gynecology leads with 29.52% share, reflecting sustained maternal-care priorities.

Which technology segment is growing fastest?

High-Intensity Focused Ultrasound is slated to advance at a 5.36% CAGR through 2031.

How will new tariffs influence equipment purchasing?

The 4-8% duties introduced in 2025 raise import costs, encouraging providers to favor domestically assembled components and portable devices to control budgets.

Why are handheld ultrasound devices gaining momentum?

Handheld units offer comparable diagnostic accuracy, require lower capital, and integrate easily with tele-medicine platforms, suiting underserved and emergency settings

Where are infrastructure investments most concentrated?

IMSS projects for 2025 focus on Ensenada, Tuxtla Gutiérrez, and other secondary cities to decentralize diagnostic capacity.

Page last updated on: