Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

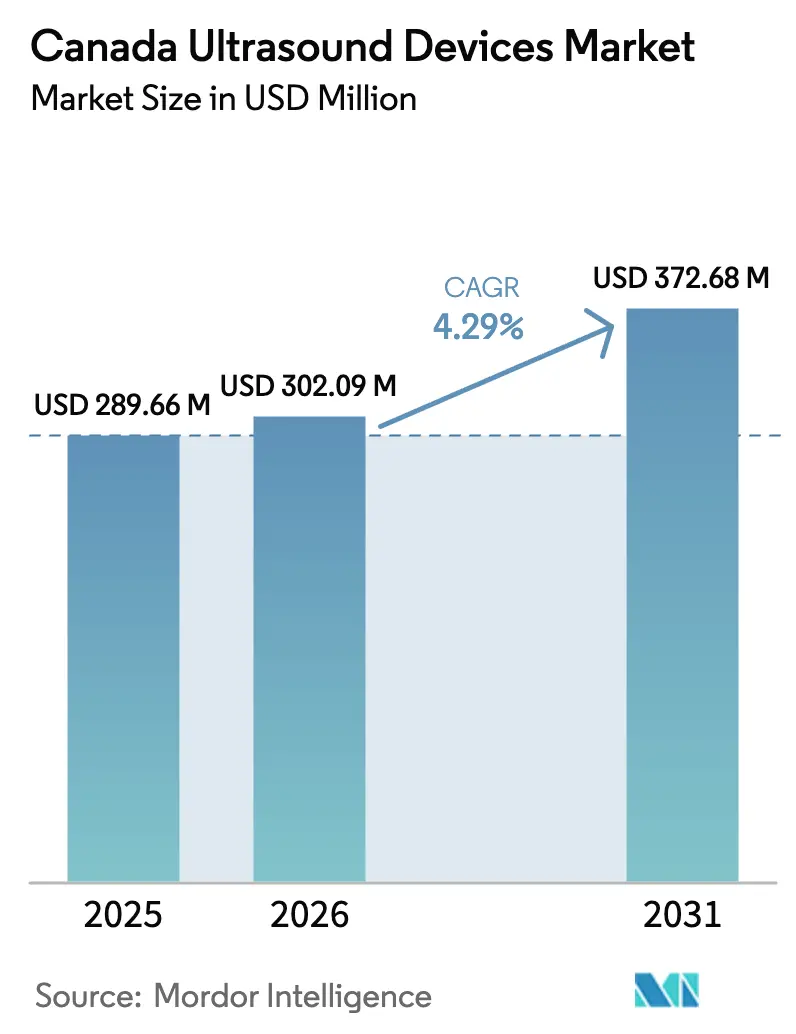

| Base Year Market Size (2025) | USD 289.66 Million |

| Market Size (2026) | USD 302.09 Million |

| Market Size (2031) | USD 372.68 Million |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

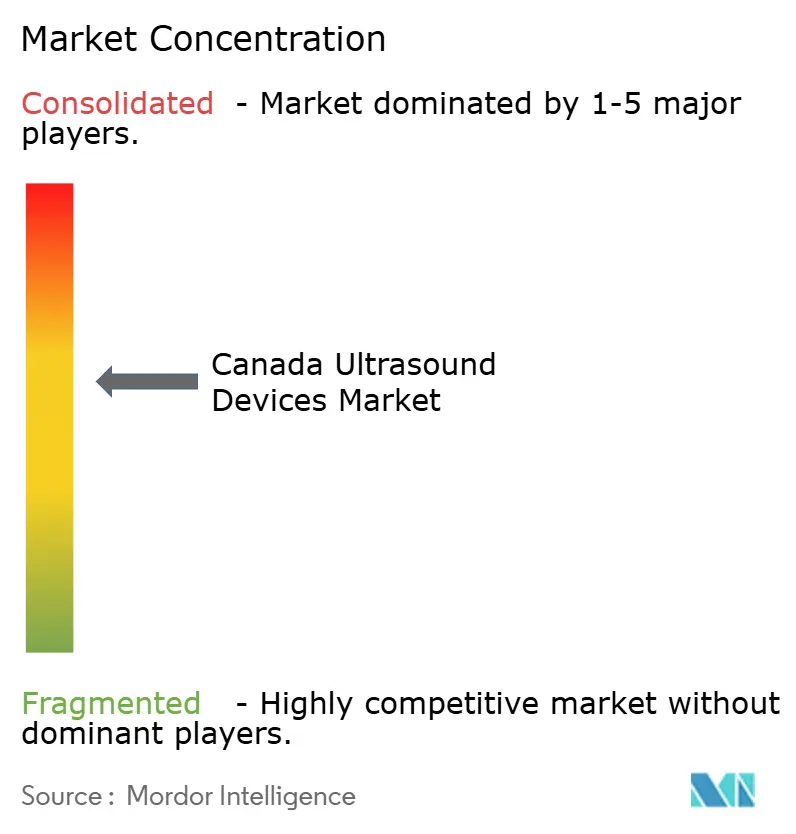

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Ultrasound Devices Market Analysis by Mordor Intelligence

The Canada Ultrasound Devices Market size was valued at USD 289.66 million in 2025 and estimated to grow from USD 302.09 million in 2026 to reach USD 372.68 million by 2031, at a CAGR of 4.29% during the forecast period (2026-2031).

Growing federal and provincial investments in diagnostic imaging, combined with rapid uptake of artificial-intelligence (AI) algorithms that automate image acquisition and interpretation, are accelerating adoption across cardiology, obstetrics, anesthesiology, and primary care. Rising cardiovascular disease prevalence, a demographic tilt toward older age cohorts, and expansion of prenatal screening programs continue to generate consistent procedure volumes. Portable high-frequency probes and handheld scanners are reshaping point-of-care workflows, even as stationary consoles retain leadership in tertiary centers. Meanwhile, global manufacturers and domestic innovators are racing to embed cloud-based workflow engines that counter acute sonographer shortages and shorten scan-to-report times, creating a competitive focus on usability rather than pure hardware specifications.

Key Report Takeaways

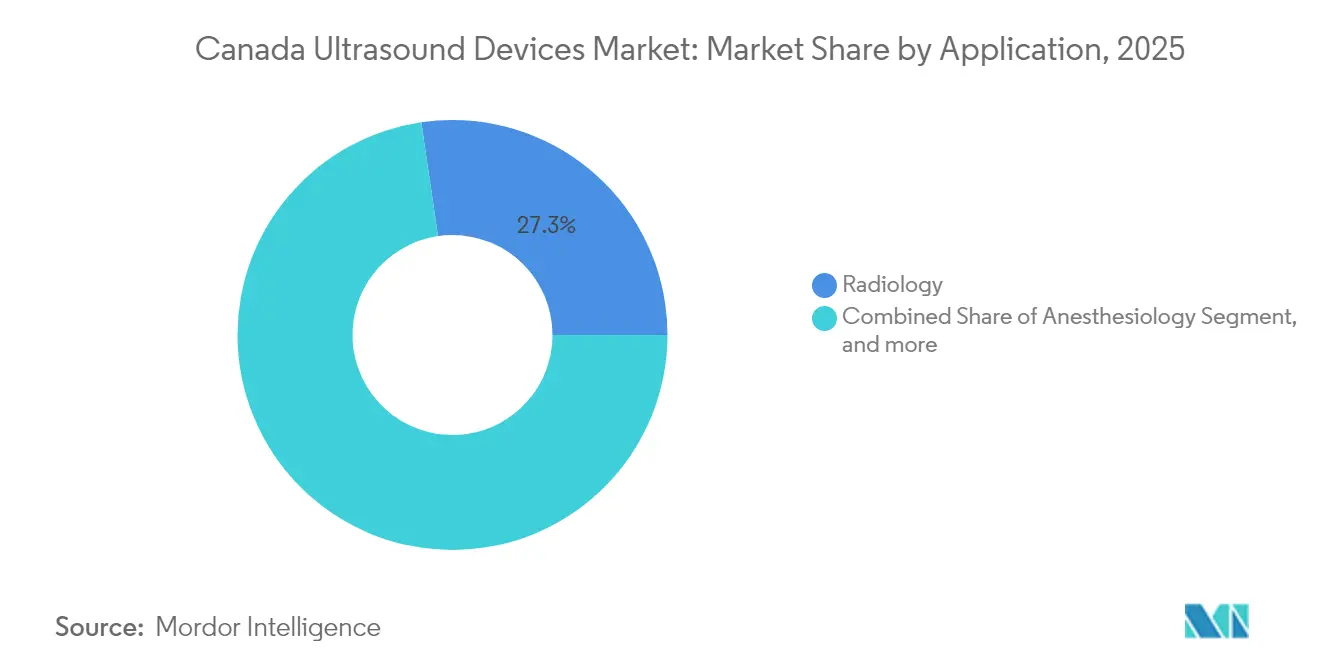

- By application, radiology led with 27.32% revenue share in 2025, while anesthesiology is expected to post the fastest 8.19% CAGR to 2031.

- By technology, 3D/4D imaging commanded 47.88% of the Canada ultrasound devices market size in 2025, yet high-intensity focused ultrasound is forecast to grow at 12.14% CAGR over 2026-2031.

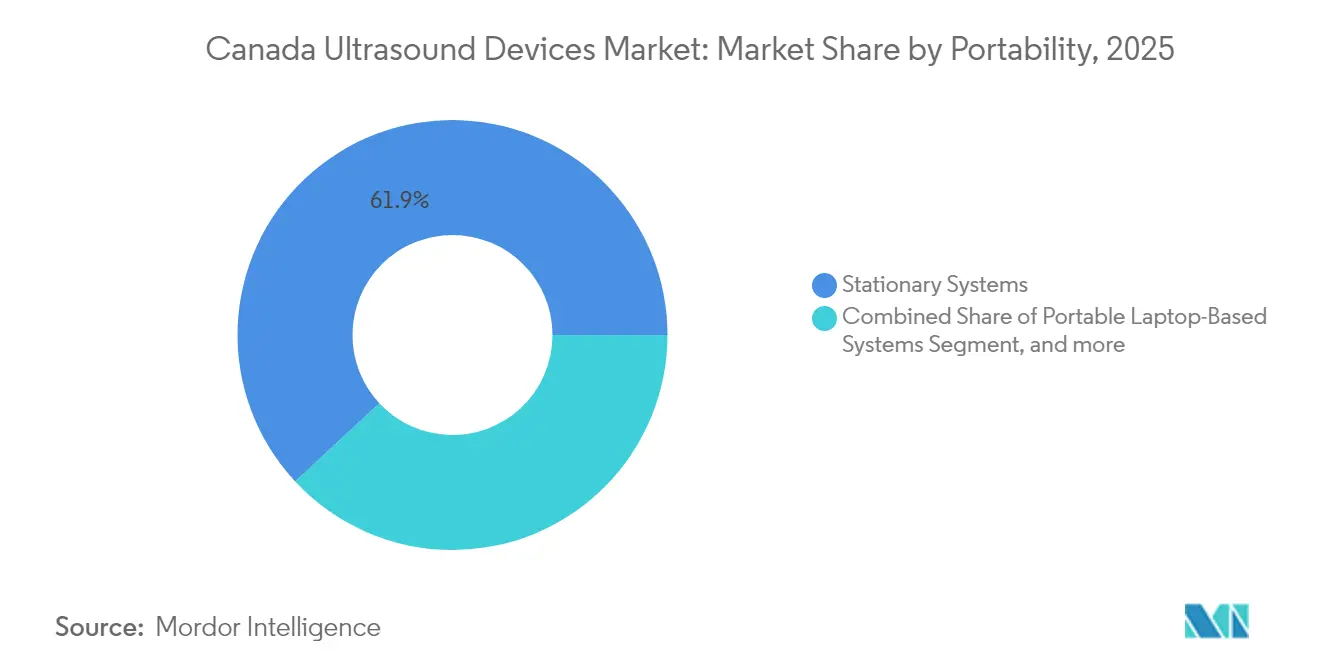

- By portability, stationary systems held 61.94% of the Canada ultrasound devices market share in 2025, whereas handheld devices are projected to record a 14.52% CAGR through 2031.

- By end user, hospitals dominated with 57.86% share of the Canada ultrasound devices market size in 2025, while diagnostic imaging centers are projected to rise at a 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government funding for diagnostic imaging equipment expansion | +1.2% | National, emphasis on rural and underserved regions | Medium term (2-4 years) |

| Rising cardiovascular disease burden increasing echocardiography volumes | +0.8% | National, concentrated in urban centers | Long term (≥4 years) |

| Aging demographics and growth in prenatal screening programs | +1.0% | National, higher impact in Ontario and Quebec | Long term (≥4 years) |

| AI-enabled image analysis adoption supported by provincial reimbursements | +1.5% | National, early adoption in major urban centers | Medium term (2-4 years) |

| Expansion of point-of-care ultrasound in emergency & primary care | +0.6% | National, with rural uptake | Short term (≤2 years) |

| Technological advancements in portable & wireless ultrasound platforms | +0.7% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Government Funding for Diagnostic Imaging Equipment Expansion in Canada

Federal and provincial spending programs are scaling diagnostic capacity by absorbing capital costs for ultrasound consoles and probes. Ottawa’s CAD 200 (USD 145.9) billion ten-year accord, which targets care backlogs, ring-fences allocations for imaging suites and mobile outreach units. British Columbia has already installed 18 MRI and nine CT scanners since 2024, freeing budgets for complementary ultrasound upgrades that streamline patient triage.[1]Government of British Columbia, “Diagnostic Imaging Expansion,” news.gov.bc.ca Research infrastructure grants worth CAD 86 (USD 62.7) million awarded to 47 institutions in 2024 further bolster faculty-led ultrasound innovation pipelines. Collectively, these disbursements reduce acquisition barriers for community clinics and catalyze volume growth across the Canada ultrasound devices market.

Rising Cardiovascular Disease Burden Increasing Echocardiography Volumes

Cardiovascular disease remains the country’s second-largest mortality driver after cancer, steering clinicians toward scalable non-invasive imaging modalities. AI-optimized echocardiography now supports earlier detection of left-ventricular dysfunction and cardiomyopathy at the bedside. The University of British Columbia’s publicly funded handheld-ultrasound network has equipped rural practitioners with probe-to-cloud devices that transmit real-time cardiac loops for central review, lifting diagnostic throughput while cutting patient travel.[2]University of British Columbia, “Handheld Ultrasound Network,” med.ubc.ca Sustained incidence trends translate into predictable capital replacement cycles, reinforcing the Canada ultrasound devices market’s mid-single-digit CAGR.

Aging Demographics and Growth in Prenatal Screening Programs

Ontario anticipates a 23% increase in residents 65 years and older within five years, a trajectory mirrored nationally and linked to greater imaging intensity for osteoporosis, vascular screening, and oncology follow-up. Parallel expansion of prenatal genetic screening engaging roughly 70% of pregnancies drives consistent first-trimester and anatomy-scan demand. Enhanced first-trimester screening now achieves 89.02% detection for trisomy 21, underscoring the clinical value of high-resolution transducers.[3]Prenatal Screening Ontario, “Enhanced First Trimester Screening Performance,” prenatalscreeningontario.ca These demographic tailwinds raise baseline procedure volumes across the Canada ultrasound devices market.

AI-Enabled Image Analysis Adoption Supported by Provincial Reimbursements

Provincial health plans are beginning to reimburse AI-augmented ultrasound reads when algorithms demonstrably shorten exam times and improve diagnostic confidence. GE HealthCare’s cardiac-strain analytics, cleared in 2024, trim average scan duration by 7 minutes and reduce the rescanning rate by 22% in early adopter sites. A leading Ontario academic hospital has catalogued 87 fully deployed AI imaging projects, many tethered to picture-archiving systems for automated measurements. This reimbursement support accelerates replacement purchases of consoles capable of running on-device algorithms, reinforcing growth in the Canada ultrasound devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of skilled labor to handle the advanced equipment | -0.7% | National, more severe in rural areas | Short term (≤2 years) |

| Health Canada licensing delays for handheld ultrasound devices | -0.4% | National | Short term (≤2 years) |

| Budget constraints in smaller healthcare facilities | -0.5% | Rural and small urban centers | Medium term (2-4 years) |

| Reimbursement limitations for certain ultrasound procedures | -0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled Labor to Handle the Advanced Equipment

Early retirements among sonographers, averaging 60.8 years, are constricting workforce supply relative to scan demand. Manitoba’s primary training program filled only 80% of seats in 2024, signaling pipeline strain. Shortages extend to anesthesiologists and medical radiation technologists, leading to surgical postponements and under-utilization of newly procured consoles. Vendors are responding with AI-driven automation and scan-quality feedback, yet human capital remains a gating factor that trims the Canada ultrasound devices market’s effective growth rate.

Health Canada Licensing Delays for Handheld Ultrasound Devices

Class II and III probes must obtain a Medical Device Licence and comply with the Medical Device Single Audit Program, lengthening approval timelines by six to nine months relative to the United States. Although January 2024 amendments expedite urgent public-health approvals, handheld devices that combine multiple arrays and cloud analytics still undergo rigorous documentation, creating a drag on commercial launch schedules. The resulting “device lag” constrains early revenue realization, particularly for domestic start-ups targeting the Canada ultrasound devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Radiology Anchors Volume, Anesthesiology Accelerates

Radiology contributed 27.32% of the Canada ultrasound devices market size in 2025 as comprehensive abdominal, pelvic, and thyroid studies remain cornerstones of diagnostic workflows. Stable reimbursement and modality familiarity ensure radiology sustains a high baseline of console utilization in tertiary centers. Anesthesiology, however, is poised for an 8.19% CAGR to 2031, propelled by expanded peripheral nerve-block protocols and critical-care adoption of cardiac output monitoring. The anesthesiology sub-segment captured 8.27% of the Canada ultrasound devices market share last year, yet its rapid growth, aided by improved catheter visualization through high-frequency probes, underscores shifting procedural paradigms toward ultrasound-guided techniques.

Cardiology follows closely, fortified by AI-assisted strain imaging that detects sub-clinical heart failure. Gynecology and obstetrics leverage 3D/4D renderings to enhance fetal anomaly detection, while emergency medicine relies on focused assessment with sonography for trauma to expedite triage. Each discipline’s evolving workflow requirements stimulate iterative hardware and software refresh cycles, sustaining value within the Canada ultrasound devices market.

By Technology: 3D/4D Dominates, HIFU Disrupts

Three-dimensional and four-dimensional imaging accounted for 47.88% of 2025 revenue, anchored by obstetric visualization and congenital heart defect screening. Vendors bundle volumetric rendering with cloud-share features that allow expectant parents and referring physicians to access scans remotely, strengthening patient engagement.

High-intensity focused ultrasound (HIFU) represents the innovation frontier, projected to log a 12.14% CAGR as non-invasive fibroid ablation and oncology indications secure regulatory clearances. MRI-guided HIFU systems at Sunnybrook Health Sciences Centre demonstrate fibroid volume reductions of up to 50%, positioning the modality as a cost-effective alternative to surgery. Doppler advancements such as vector-flow mapping add hemodynamic detail to vascular studies, and AI de-noise algorithms elevate image clarity at lower transmit powers, further differentiating platforms within the Canada ultrasound devices market.

By Portability: Stationary Consoles Lead, Handheld Probes Surge

Stationary consoles command 61.94% of market revenue in 2025 due to superior image quality, integrated reporting suites, and comprehensive modality support. Nevertheless, handheld probes are surging at a 14.52% CAGR through 2031 as battery life, wireless connectivity, and AI-enabled presets reduce training overhead.

Cloud-linked handheld devices foster distributed care models, enabling specialist oversight without patient transfer. Laptop-based portables bridge the gap when hospital-grade transducer diversity is required in field clinics, underscoring a stratified equipment ecosystem in the Canada ultrasound devices market.

By End User: Hospitals Remain Core, Imaging Centers Expand

Hospitals generated 57.86% of 2025 revenue by consolidating emergency, inpatient, and specialty service lines under one budget. Diagnostic imaging centers, however, are forecast to rise at a 8.95% CAGR as outpatient reimbursement parity and faster appointment scheduling attract primary-care referrals.

Ambulatory surgical centers employ ultrasound to guide regional anesthesia and vascular access, reinforcing procedural efficiency. Mobile imaging vans contract with Indigenous health authorities to deliver obstetric and cardiac scans in remote communities, diversifying demand channels across the Canada ultrasound devices market.

Geography Analysis

Major metropolitan provinces such as Ontario, Quebec, British Columbia, and Alberta account for significant share of national ultrasound unit shipments, reflecting hospital density and funding capacity. Ontario’s demographic shift toward a larger senior population intensifies demand for musculoskeletal, vascular, and oncology imaging. Quebec’s universal prenatal screening coverage fosters high first-trimester ultrasound utilization. British Columbia’s capital grants have expanded MRI fleets, prompting parallel purchases of high-end ultrasound systems to balance imaging workloads.

Prairie provinces rely heavily on portable probes to offset sparse sonographer distribution, with Saskatchewan piloting a telerobotic arm that allows remote specialists to maneuver a probe situated hundreds of kilometers away. Atlantic Canada leverages federal pathology turnaround-time funding to acquire multipurpose consoles that serve both echocardiography and vascular labs. In northern territories, Indigenous-focused programs fund handheld devices for nursing stations, elevating prenatal and trauma care accessibility.

Inter-provincial interoperability reforms under the Connected Care for Canadians Act support seamless image exchange, reducing duplicate scans and aiding load balancing between urban and rural facilities. Collectively, these regional patterns emphasize how public-sector capital flows and workforce distribution shape the opportunity landscape for vendors competing in the Canada ultrasound devices market.

Competitive Landscape

GE HealthCare, Philips, Siemens Healthineers, and Canon Medical Systems collectively capture more than half of annual console placements, wielding broad portfolios and nationwide service networks. GE HealthCare’s 2024 purchase of Intelligent Ultrasound for USD 51 million imported real-time voice guidance and AI quality-assurance modules into its Versana platform, cutting operator adjustment steps by 38%. Philips spotlights its PureWave crystals that enhance penetration in bariatric imaging, while Siemens Healthineers advances its eSieMeasure cardiology suite that auto-calculates ejection fraction.

Domestic disruptor Clarius Mobile Health sells smartphone-connected probes in more than 58 countries; 90% of revenue is export-driven, yet the firm capitalized on CAD 3.4 (USD 2.4) million in federal scale-up funding to extend manufacturing capacity in Vancouver. Butterfly Network leverages semiconductor-based CMUT arrays to price probes below USD 2,500, capturing rapid POCUS adoption among paramedics and community midwives.

Strategic alliances dominate go-to-market motions: Novartis partnered with Clarius in May 2024 to accelerate psoriatic arthritis detection via musculoskeletal ultrasound, broadening therapeutic outreach. Arrayus Technologies secured Health Canada clearance for MRI-guided focused ultrasound in uterine fibroid ablation, differentiating through resonance-based targeting. Competitive intensity therefore pivots on AI depth, modality-specific workflow claims, and post-purchase education services aimed at mitigating labor shortages within the Canada ultrasound devices market.

Canada Ultrasound Devices Industry Leaders

Koninklijke Philips N.V.

Hologic Inc.

GE HealthCare Technologies Inc.

Canon Medical Systems Corporation

FUJIFILM Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: GE HealthCare launched the Versana Premier ultrasound system featuring AI-enabled tools for workflow optimization and enhanced diagnostic capabilities across multiple specialties, including general practice, OBGYN, and cardiology.

- October 2024: Arrayus Technologies Inc. announced that its Magnetic Resonance Imaging (MRI)-guided focused ultrasound system received approval from Health Canada for the ablation of uterine fibroid tissue. This approval, following a successful first-in-human clinical trial, provides Canadian healthcare providers with a safe, non-invasive alternative to traditional surgical options for this common gynecological condition. Such regulatory approvals are crucial for expanding the application of ultrasound devices in various medical fields.

- May 2024: Novartis Pharmaceuticals Canada Inc. partnered with Clarius Mobile Health to support the early detection of psoriatic arthritis in Canada. By improving access to ultrasound technology, this collaboration enables rheumatologists to identify diagnostic markers earlier, potentially reducing the time to diagnosis for PsA patients. This partnership demonstrates how collaborations can drive the adoption of ultrasound devices in specialized medical fields.

- March 2024: Clarius Mobile Health received Health Canada approval for its Musculoskeletal (MSK) Artificial Intelligence (AI) model, which uses AI to automatically identify and measure tendons in the foot, ankle, and knee. This model is now available with the Clarius L7 HD3 and L15 HD3 high-frequency wireless handheld ultrasound scanners. Such advancements highlight the growing role of AI in enhancing the functionality and efficiency of ultrasound devices.

Canada Ultrasound Devices Market Report Scope

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They are being utilized to assess various conditions in the kidney, liver, and other abdominal disorders. They are also majorly used in chronic diseases, including heart disease, asthma, cancer, and diabetes. Canada Ultrasound Devices Market is Segmented by Application (Anesthesiology, Cardiology, Gynecology/Obstetrics, Musculoskeletal, Radiology, Critical Care, and Other Applications), Technology (2D Ultrasound Imaging, 3D and 4D Ultrasound Imaging, Doppler Imaging, and High-intensity Focused Ultrasound), Type (Stationary Ultrasound and Portable Ultrasound). The report offers the value (in USD million) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology/Obstetrics |

| Radiology |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D and 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound (HIFU) |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Laptop-Based Systems |

| Handheld/Pocket Ultrasound Devices |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology/Obstetrics | |

| Radiology | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D and 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound (HIFU) | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Laptop-Based Systems | |

| Handheld/Pocket Ultrasound Devices | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Ambulatory Surgical Centers | |

| Other End Users |

Key Questions Answered in the Report

What is the current value of the Canada ultrasound devices market?

The market is currently valued at USD 302.09 million in 2026 and is projected to reach USD 372.68 million by 2031.

Which segment is growing the fastest?

Handheld probes are expanding at a 14.52% CAGR, supported by AI presets and provincial funding for point-of-care imaging.

Why is anesthesiology a high-growth application?

Ultrasound-guided nerve blocks and catheter placements improve procedural safety, driving an 8.19% CAGR in the anesthesiology segment.

What regulatory challenges do vendors face?

Health Canada’s Medical Device Licensing and Single Audit Program introduce additional documentation and ISO 13485 requirements that can delay handheld device approvals by up to nine months.

How significant is government funding in market expansion?

Federal and provincial investments, including a CAD 200 (USD 146.0) billion ten-year plan, directly subsidize diagnostic imaging equipment.

Page last updated on: