Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

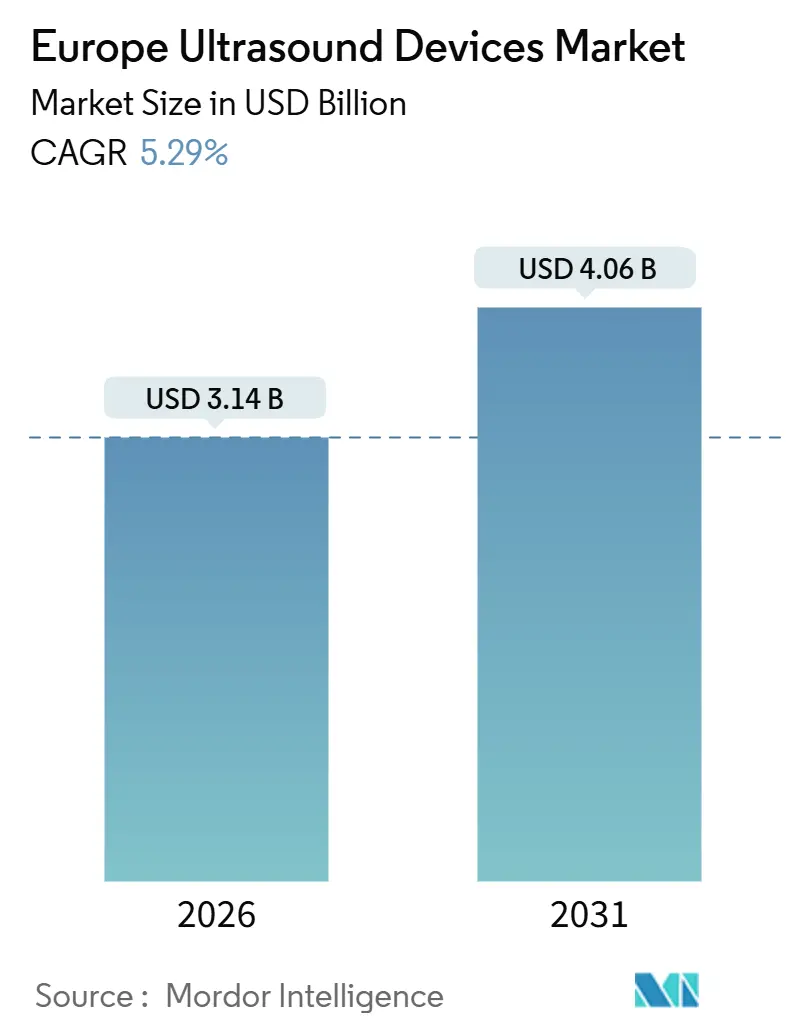

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 4.06 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

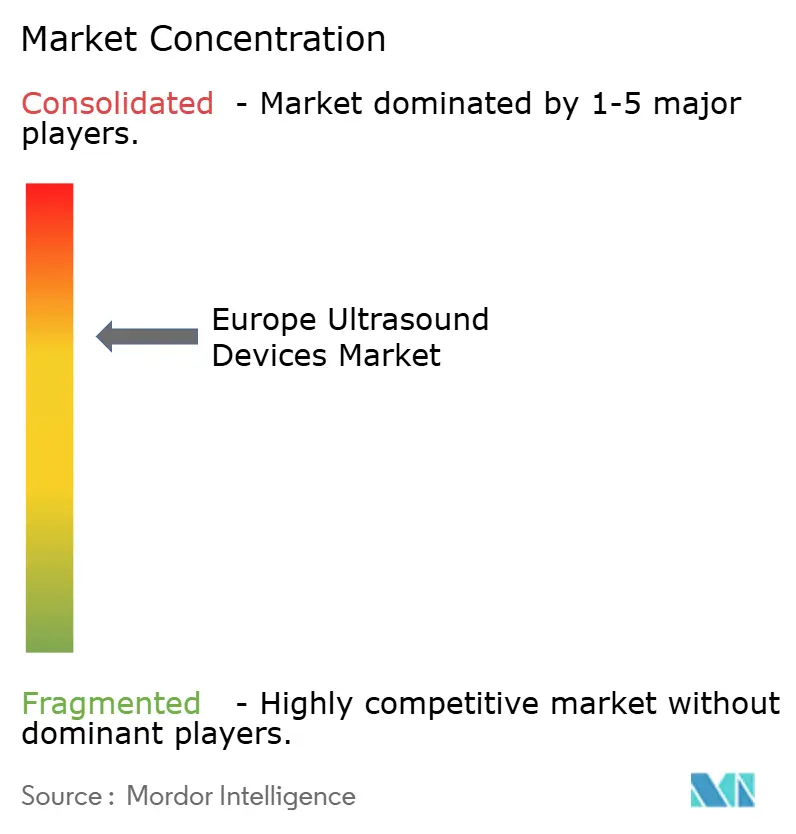

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ultrasound Devices Market Analysis by Mordor Intelligence

The Europe Ultrasound Devices Market size is estimated at USD 3.14 billion in 2026, and is expected to reach USD 4.06 billion by 2031, at a CAGR of 5.29% during the forecast period (2026-2031).

A structural shift is underway: while hospital radiology departments still rely on cart systems, ambulatory surgical centers (ASCs), community diagnostic hubs, and home-care providers are demanding compact, portable, and handheld products that are growing at nearly twice the overall pace. Environmental policies also reinforce the modality’s momentum because a full ultrasound lifecycle emits only 2.5 metric tons of CO₂-equivalent, compared to 30–40 tons for CT and 50–60 tons for MRI, giving it a decisive advantage as hospitals work toward net-zero operations. A widening chronic disease burden, particularly cardiovascular and oncologic conditions, keeps utilization volumes high, while AI-enabled workflow features shorten exam times and help offset the region’s sonographer shortage. Competitive dynamics are intensifying: leading multinationals are defending premium cart revenues yet simultaneously releasing lower-priced probes to counter new entrants that position handheld devices as everyday tools for general practitioners and paramedics. Procurement, however, is slowing in some countries because EU Medical Device Regulation (MDR) certificates take longer to secure, and payers have yet to harmonize reimbursement for handheld scans performed outside hospital radiology suites.

Key Report Takeaways

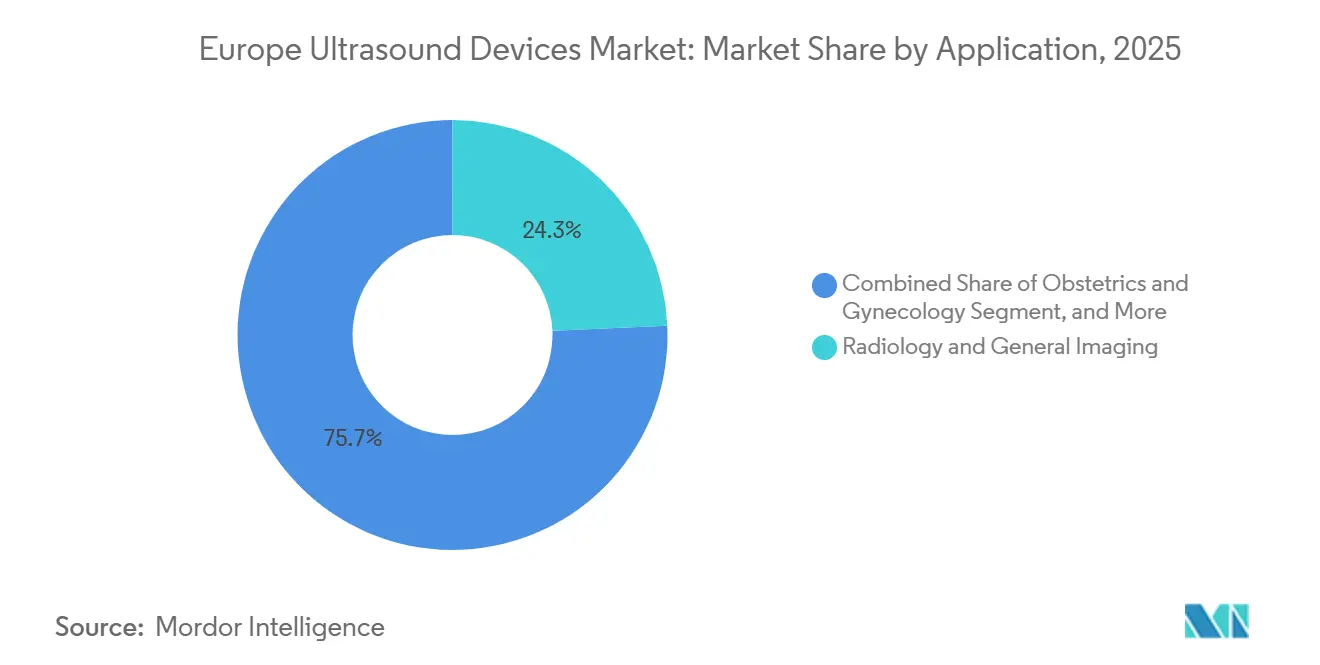

- By application, radiology and general imaging accounted for 24.31% of the Europe ultrasound devices market share in 2025, whereas obstetrics and gynecology is advancing at a 7.48% CAGR through 2031.

- By technology, 3D and 4D imaging held 44.73% of the Europe ultrasound devices market size in 2025, while high-intensity focused ultrasound (HIFU) is expanding at a 7.97% CAGR.

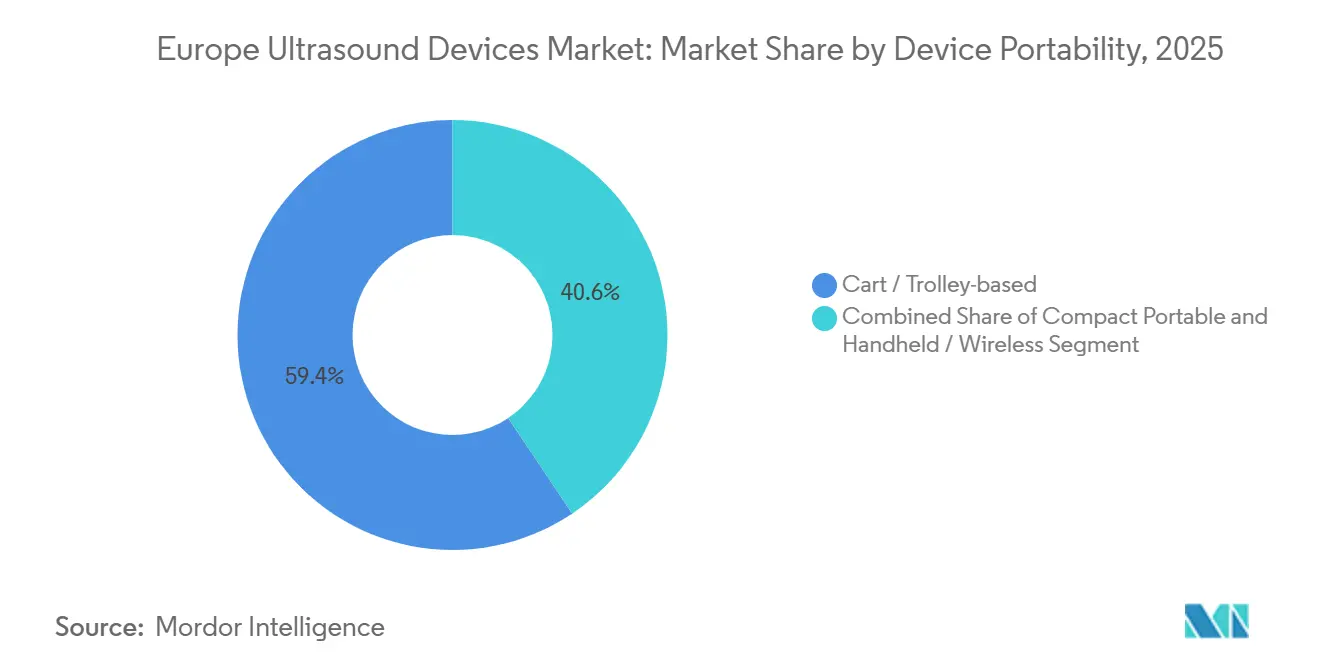

- By device portability, cart and trolley systems led with 59.38% share of the Europe ultrasound devices market size in 2025, yet compact portable units are progressing at a 6.54% CAGR.

- By end user, hospitals retained 54.26% of the Europe ultrasound devices market share in 2025, but ASCs are growing fastest at a 9.44% CAGR.

- By country, Germany captured 32.26% of the Europe ultrasound devices market size in 2025, whereas Spain is projected to post the strongest trajectory with an 8.58% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased adoption of diagnostic imaging in primary care | +0.9% | Germany, UK, France; limited uptake in Eastern Europe | Medium term (2-4 years) |

| Growing burden of chronic diseases | +1.1% | Germany, UK, Italy and other aging markets | Long term (≥ 4 years) |

| Miniaturization and point-of-care uptake in ambulances and home-care | +0.8% | UK, Germany, Spain, especially large urban centers | Short term (≤ 2 years) |

| AI-enabled workflow efficiencies that cut exam time | +0.7% | Germany, UK, France, anchored in academic hospitals | Medium term (2-4 years) |

| Hospital decarbonization mandates that favor ultrasound over CT/MRI | +0.6% | UK, France, Germany in line with Greener NHS and EU Green Deal | Long term (≥ 4 years) |

| Growing minimally invasive diagnostics and larger imaging facility count | +1.0% | Spain, Italy where new outpatient sites are opening | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Adoption of Diagnostic Imaging in Primary Care

Primary-care physicians across Western Europe are equipping surgeries with handheld or laptop ultrasound devices to shorten referral queues and triage non-urgent complaints on-site. Germany already has 98% penetration in general practices, setting a reference model for neighboring health systems.[1]Judith Wachtler et al., “Ultrasound Availability in Primary Care in Germany,” BMC Primary Care, bmc.org The United Kingdom’s Integrated Diagnostics and Pathology framework is placing portable scanners in 155 Community Diagnostic Centres, allowing musculoskeletal and abdominal scans to be completed outside hospitals, thereby relieving pressure on radiology departments. Eastern Europe remains behind the curve because budgets and reimbursement codes still favor hospital-centric imaging. Whether ministries adjust tariff schedules for primary-care scans will determine how quickly adoption spreads to that region.

Growing Burden of Chronic Diseases

Cardiovascular disease continues to cause 45% of all European deaths, which in turn generates steady demand for repeat echocardiography and Doppler studies to monitor heart-failure progression.[2]European Society of Cardiology, “Cardiovascular Disease Statistics 2024,” escardio.org Oncology pathways increasingly rely on ultrasound-guided needle biopsies and contrast-enhanced exams for real-time characterization of liver and kidney tumors, enabling clinicians to avoid radiation-based CT when diagnostic performance is equal. Diabetes complications prompt vascular screening that identifies peripheral artery disease earlier, thereby expanding the overall pool of patients examined. Because each chronic patient now undergoes multiple imaging events per year, utilization rates rise even though the continent’s population is aging rather than growing. Portable probes are well-suited for at-home monitoring and community follow-up visits, which outpace stationary installations in hospitals.

Miniaturization and Point-of-Care Uptake in Ambulances and Home-Care

Handheld probes retailing below USD 5,000, such as the Butterfly iQ3 and GE HealthCare Vscan Air SL, transmit high-quality images directly to smartphones, enabling paramedics to assess internal bleeding or cardiac function before patients arrive at emergency rooms. Clarius devices add AI auto-measurements and direct DICOM export over Wi-Fi, supporting home-nursing teams that need rapid bladder or deep-vein scans. The United Kingdom published 54 procurement notices for ultrasound in 2025, allocating a significant share to portable gear destined for its community hubs. Payment gaps persist, however, because many insurers reimburse handheld scans at only 50–70% of cart exam rates or not at all, discouraging uptake in smaller practices. Compliance with ISO 13485 and IEC 60601 standards helps vendors clear regulatory hurdles; however, broad adoption hinges on updated fee schedules.

AI-Enabled Workflow Efficiencies Reducing Exam Time

Cart platforms, such as Philips EPIQ Elite and Samsung Medison HERA W10 Elite, automate labor-intensive measurements, including ejection fraction and fetal biometry, thereby reducing the sonographer's workload by approximately 25% per study. Siemens Healthineers’ latest ACUSON Sequoia utilizes deep learning in liver elastography, enabling clinicians to characterize fibrosis in fewer sweeps.[3]Siemens Healthineers, “ACUSON Sequoia Deep Learning Release,” siemens-healthineers.com Despite these gains, a 2024 systematic review revealed that many commercial algorithms exhibit domain shift when applied outside the institution where they were trained, underscoring the importance of multi-center validation. The EU MDR now classifies most adaptive algorithms as high-risk software, obligating the submission of prospective clinical evidence, which elongates the product approval timeline. The European Society of Radiology is developing standard evaluation metrics to accelerate acceptance once those datasets become available.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented reimbursement for handheld devices | −0.5% | UK, France, Spain where point-of-care codes lag behind technology | Short term (≤ 2 years) |

| Shortage of certified sonographers in Eastern Europe | −0.7% | Poland, Romania, Bulgaria with spillover into Germany and Austria | Long term (≥ 4 years) |

| Cybersecurity risk from wireless data transmission | −0.3% | Germany, France and all GDPR-regulated markets | Medium term (2-4 years) |

| Procurement delays linked to new EU MDR certification | −0.4% | EU-wide, worst in Italy and Spain where notified-body queues persist | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Reimbursement for Handheld Devices

Most European tariff systems were designed for hospital radiology, so a handheld abdominal scan in a community clinic can be reimbursed at 30–50% below the equivalent cart-based code, or not reimbursed at all. NICE endorsed point-of-care ultrasound in emergency departments in 2024, yet NHS billing tables have not been updated, forcing trusts to either absorb the cost or restrict its deployment. France and Spain maintain dual fee schedules that pay radiologist-performed exams significantly more than clinician-performed studies, limiting the uptake of handheld devices beyond urban hospitals. Eastern European funds are even tighter, and payers often refuse coverage for any ultrasound conducted outside a radiology department, curbing handheld adoption where it might otherwise offset sonographer shortages.

Shortage of Certified Sonographers Across Eastern Europe

A European Commission study reveals that the region is short 1.2 million healthcare workers, including a significant shortfall of radiographers and sonographers. In 2024, the European Society of Radiology reported that 45% of radiologists are over 51 years old, and 19% will retire within the next five years. Poland now posts non-urgent ultrasound waits of up to eight weeks, driving patients either to private imaging chains or across the German border. The annual training output of roughly 700 sonographers across Eastern Europe is insufficient to backfill these departures, leaving new scanners idle due to a lack of operators. Western Europe feels a ripple effect as skilled staff migrate westward for higher wages, so workforce ceilings ultimately limit equipment sales throughout the union.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Prenatal Screening Fuels Rapid Obstetric Growth

In 2025, radiology and general imaging maintained a 24.31% share of the European ultrasound devices market, thanks to their entrenched workloads in hospital departments, including abdominal, soft-tissue, and vascular imaging. However, obstetrics and gynecology are scaling fastest at a 7.48% CAGR because national prenatal protocols now recommend three to four scans per pregnancy and add 3D/4D imaging for anomaly detection. The European ultrasound devices market size tied to obstetric endpoints is therefore rising more quickly than radiology volumes, especially in Spain and Italy, where maternal screening investments are part of post-pandemic recovery budgets. A simultaneous surge in cardiac Doppler and echocardiography is driven by heart-failure monitoring: cardiovascular disease causes 45% of European deaths, and each case necessitates serial imaging. Emergency and critical-care teams accelerate uptake of FAST protocols, while musculoskeletal clinics deploy high-frequency probes as cheaper, faster alternatives to MRI for tendon tears.

Clinical diversification broadens revenue streams because every incremental application requires at least one dedicated transducer. This momentum benefits vendors that offer modular platforms flexible enough to support obstetrics, vascular and anesthesiology workflows on the same console. Conversely, radiology growth is capped by staff shortages, creating a ceiling on the number of additional exams that hospital departments can absorb. Portable scanners further tilt share toward obstetrics because prenatal visits often occur in outpatient settings where mobility is prized.

By Technology: 3D/4D Retains Lead, HIFU Climbs From Niche to Growth Engine

Three-dimensional and four-dimensional imaging captured 44.73% of the European ultrasound devices market size in 2025, owing to its dominance in fetal, breast, and musculoskeletal use cases. Vendors refine algorithms that render lifelike fetal images within seconds, deepening demand among expectant parents and clinicians. At the same time, HIFU is expanding at a 7.97% CAGR by offering a non-invasive alternative for uterine fibroid and prostate cancer ablation, reducing hospitalization and surgical risk. Doppler modalities remain essential for vascular assessments, whereas elastography is emerging as a preferred non-invasive method to stage liver fibrosis, aligning with EASL practice guidelines.

As reimbursement agencies increasingly cover therapeutic ultrasound, vendors are packaging diagnostic and ablative capabilities on the same platform, thereby elevating average selling prices. European notified bodies nevertheless demand robust safety data for each indication, lengthening the time to market. Vendors capable of bundling 3D/4D, Doppler, elastography, and HIFU on a unified upgradeable architecture stand to maximize replacement-cycle sales as hospitals streamline fleets.

By Device Portability: Compact Portable Gains Ground Over Heavy Carts

Cart and trolley systems still accounted for 59.38% of the European ultrasound devices market size in 2025, as they offer premium image quality, broad probe support, and high-end features such as contrast-enhanced ultrasound. Yet compact portable units are expanding at a 6.54% CAGR as ASCs and emergency departments prioritize mobility when space and budget are limited. Handheld products now constitute the fastest-growing sub-segment: devices priced between USD 2,000 and USD 5,000 appeal to primary-care clinics and paramedic services that previously could not justify a USD 50,000 cart. The European ultrasound devices market share of handhelds remains small today, yet month-to-month unit shipments are rising steeply.

This shift in portability forces incumbent OEMs to defend their margins by releasing scaled-down versions of their flagship consoles, while newcomer brands compete on subscription pricing and smartphone integration. Hospitals are also acquiring portable units as backup devices for resuscitation bays and isolation rooms, so a single institution may purchase both categories, blurring historical segmentation lines.

By End User: Outpatient Migration Propels ASC Demand

Hospitals accounted for 54.26% of total spending in 2025; however, ASCs delivered the strongest CAGR at 9.44%, as payers increasingly reward lower-cost outpatient pathways. Diagnostic imaging centers pick up the overflow from hospitals burdened by staffing shortages, while home-care agencies integrate handheld probes for monitoring chronic diseases. Italy has earmarked EUR 76 million to equip outpatient centers with nearly 1,000 scanners, demonstrating the state's commitment to decentralized imaging. Spain’s forthcoming 150 diagnostic sites reinforce this trend, and the United Kingdom’s Community Diagnostic Centres embed scanners within primary-care networks.

Hospitals remain irreplaceable for high-acuity exams such as intra-operative cardiac imaging, but every shift toward outpatient care shrinks the cart addressable market and enlarges the portable category. Vendors that tailor service contracts and financing to ASC purchasing cycles will capture this momentum.

Geography Analysis

Germany’s leadership is built on decades of primary-care adoption, which now drives steady upgrade cycles as practices transition from 2D to AI-enabled 3D/4D systems. Carbon-reduction rules further motivate hospitals to select ultrasound over CT, ensuring that the modality’s installed base continues to expand in radiology suites. The United Kingdom is shifting routine imaging into community hubs to address persistent wait-time overruns; the award of portable probe lots in 2025 confirms the trend. France stays on a moderate trajectory because reimbursement is stable, but adoption of handheld devices by general practitioners is slower due to fee gaps.

Spain is setting the regional growth pace through sizeable public-investment tranches that earmark new diagnostic centers for underserved provinces and favor ultrasound as the default first-line tool. Italy mirrors this push by dedicating recovery funds to ASC equipment. Across Eastern Europe, limited reimbursement and a thin pool of sonographers cap usage; yet, handhelds offer a cost-effective bridge when capital budgets are tight. This geographic diversity demands tailored channel strategies: high-spec carts flourish in Western teaching hospitals, whereas simple portables unlock incremental volume in Southern clinics and Eastern ambulatory sites.

Regulatory Landscape

Ultrasound systems marketed across Europe are governed by the EU Medical Device Regulation (MDR) (Regulation (EU) 2017/745), applicable since 26 May 2021, which sets general safety and performance requirements and requires manufacturers to compile technical documentation and undergo conformity assessment for CE marking. For connected and AI-enabled ultrasound workflows, MDR expectations around clinical evidence and post-market surveillance increase the documentation and validation burden, contributing to longer certificate timelines that can spill into procurement schedules.

A key operational milestone in the MDR infrastructure is EUDAMED, which is being rolled out in phases under the transitional provisions updated via Regulation (EU) 2024/1860. The European Commission indicates the EUDAMED UDI/Devices module becomes mandatory to use from 28 May 2026, raising the importance of UDI readiness, data quality, and system integration for manufacturers and authorized representatives placing ultrasound devices on the EU market. On the engineering side, safety and essential performance expectations are commonly addressed through applicable standards for diagnostic and monitoring ultrasound equipment, including EN IEC 60601-2-37:2024 (diagnostic and monitoring scope), supporting conformity to essential requirements when used within a compliant quality-management system (for example, ISO 13485).

Competitive Landscape

The European ultrasound devices market displays moderate concentration because the top five OEMs, Siemens Healthineers, GE HealthCare, Philips, Canon Medical Systems, and Mindray, collectively held a significant share, benefiting from entrenched service contracts and broad modality portfolios. Siemens earned EUR 11.8 billion in imaging revenue during fiscal 2023 and unveiled the ACUSON Sequoia Crown and Select editions at ECR 2025 with integrated deep-learning liver applications. GE HealthCare counters disruptors with the Vscan Air SL at USD 4,500, while Butterfly Network sells its iQ3 at USD 1,999 plus a USD 420 annual subscription, undercutting incumbents on entry cost. A 2024 expert comparison nonetheless rated Vscan Air highest for usability and purchase intent, illustrating that clinical workflow fit and after-sales support still sway buyers.

Handheld specialists, such as Clarius and FUJIFILM Sonosite, compete by integrating artificial intelligence features that automatically measure bladder volume or cardiac output, narrowing the performance gap against carts. MDR compliance now acts as a competitive filter: large companies marshal the clinical evidence and regulatory staff to certify algorithms quickly, while smaller firms face longer queues. Subscription software and cloud image-management services emerge as differentiators, as hospitals seek scalable solutions that simplify their cybersecurity obligations under the GDPR. The entry of low-cost Chinese producers exerts price pressure, but they have yet to secure a broad Western market share due to limited service infrastructure and brand recognition.

Europe Ultrasound Devices Industry Leaders

Esaote SpA

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthcare

Mindray Medical International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear commercialization opening is forming around AI-enabled workflow automation and high-throughput clinical environments, where providers face staffing constraints and seek shorter exam times and more standardized measurements. In June 2026, Philips introduced the Alturion ultrasound system in Europe with AI-powered workflows for high-volume settings, while Canon Medical Systems showcased Aplio me X at Euroson 2026 with a focus on AI-assisted workflows and battery-powered portability. These launches reinforce demand for platforms that combine imaging performance with embedded automation, connectivity, and easier deployment across outpatient hubs, emergency settings, and community diagnostic sites.

Women’s health, prenatal screening, and interventional workflows provide additional white space as vendors extend ultrasound from diagnostic imaging into procedure guidance and decision support. BrightHeart announced CE mark and a European launch for its B-Right AI platform for prenatal ultrasound in June 2026, indicating that MDR-cleared software layers are moving into routine clinical adoption pathways, not only research pilots. Product introductions at ECR 2026, including Esaote’s MyLab E85 and MyLab C30 GTS Edition positioned for interventional radiology, underline the opportunity for vendors that bundle advanced guidance features, transducer ecosystems, and enterprise imaging integration to fit outpatient growth, ASC purchasing cycles, and hospital decarbonization priorities that favor lower-emission modalities.

Recent Industry Developments

- June 2026: Philips introduced the Alturion ultrasound system in Europe, highlighting AI-powered workflows designed for high-volume clinical environments. The launch signals intensified competition around productivity features that reduce operator burden and standardize measurements, particularly relevant for hospitals and community diagnostic pathways facing workforce constraints.

- October 2025: GE HealthCare introduced the Voluson Performance 18 and 16 systems, adding AI automation aimed at boosting women’s health productivity. The update strengthens GE HealthCare’s position in high-volume OB/GYN settings where protocol-driven prenatal scanning increases demand for faster, more repeatable acquisition and reporting.

- September 2024: Butterfly Network secured CE marking for the iQ3 handheld ultrasound probe, increasing processing capability versus prior generations. CE marking supports broader European deployment of lower-cost handheld scanning in primary care, emergency response, and home-care models that are expanding outside traditional radiology departments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues earned from ultrasound systems and platforms sold and used across Europe for diagnostic imaging and therapeutic procedures, including software-enabled features that ship as part of the system package.

Scope exclusions: We exclude service contracts, installation, training, and standalone consumables that are not billed as part of the ultrasound device sale.

Segmentation Overview

- By Application

- Radiology & General Imaging

- Obstetrics & Gynecology

- Cardiology

- Emergency & Critical Care

- Musculoskeletal

- Anesthesiology

- Other Applications

- By Technology

- 2D Ultrasound Imaging

- 3D & 4D Ultrasound Imaging

- Doppler Imaging

- High-Intensity Focused Ultrasound (HIFU)

- Elastography

- Contrast-Enhanced Ultrasound (CEUS)

- By Device Portability

- Cart / Trolley-based

- Compact Portable

- Handheld / Wireless

- By End User

- Hospitals

- Diagnostic Imaging Centres

- Ambulatory Surgical Centres

- Home Healthcare Settings

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the country pool, and map demand indicators that typically move ultrasound purchasing in Europe. We referenced public sources such as Eurostat health expenditure series, European Commission and national health ministry publications, WHO and OECD health statistics, and peer-reviewed clinical journals covering ultrasound usage and procedure shifts.

To ground the commercial side, we reviewed manufacturer annual reports, investor presentations, product documentation, and reputable press releases that discuss new launches and replacement cycles. Where helpful, we used paid subscriptions for company financials and news screening, and a patent database to track feature progression that can influence average selling price (ASP). The desk sources listed here are illustrative only, and other public documents were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating price bands, replacement timing, and country-level adoption patterns for portable and cart-based systems, since these can shift the revenue mix quickly. We spoke with manufacturers, distributors, hospital procurement teams, radiology and cardiology users, and diagnostic center operators across major European countries and the Rest of Europe, then used follow-up questions to close gaps identified in the desk inputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 22% | |

| Mid tier: 51% | Functional/Unit leaders: 36% | |

| Smaller Players: 22% | Managers: 42% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where country healthcare activity and imaging capacity signals were used to reconstruct the addressable demand pool, which was then translated into device revenues using realistic ASP ladders. To keep the totals honest, the outcome was cross-checked with selective bottom-up approximations, such as sampled unit volumes by portability class multiplied by observed price bands, followed by distributor channel checks.

Inputs that were tracked (illustrative) included the installed base refresh cycle for cart-based systems, the penetration of compact portable and handheld units in point-of-care settings, procedure mix changes in cardiology and OB-GYN, tender intensity in public hospitals, and the pace of feature upgrades like Doppler, elastography, and 3D or 4D capability that usually lift ASP. Forecasts leaned on scenario analysis, since procurement timing can swing by budget cycles, with assumptions stress-tested through primary feedback on pricing moves and expected replacement deferrals.

Where bottom-up signals were missing for smaller countries, gaps were handled by using peer-country ratios and adjusting for known healthcare spend and provider density differences, then reviewing the model impact so it did not overreact to a single proxy.

Data Validation & Update Cycle

Outputs were triangulated across multiple checks, including country totals versus historical import and procurement signals, implied units versus typical replacement behavior, and ASP bands versus the latest product positioning. Any large variance triggered a second pass where assumptions were challenged, and interview respondents were re-contacted if the variance could not be explained by mix or timing.

Before sign-off, the model and its inputs are reviewed in steps by analysts so calculation errors and inconsistent country logic are removed. The report is refreshed annually, and if major events happen in pricing, regulation, or hospital spending, interim updates are made. Right before delivery, a final refresh pass is completed so the numbers align with the most recent currency timing and market signals available.

Mordor Intelligence's Europe Ultrasound Devices Market Market Size Compared Against Other Published Estimates

Published market sizes for Europe ultrasound devices often differ, even when the story on growth feels similar, because the scope and timing choices behind the numbers are not the same. Differences usually come from what is counted as a device sale versus adjacent revenue, which countries are included in Europe, and how pricing changes are carried forward in the forecast.

In this study, the spread is also affected by refresh cadence and currency timing, since hospital tenders and ASP moves for portable systems can shift annual revenue when converted and updated, a control step applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.14 B (2026) | |

| Global Consultancy A | USD 2.72 B (2024) | Uses an earlier base year and a shorter horizon, and it separates diagnostic versus therapeutic revenue in a way that can lower the device total when bundled platform upgrades are treated as non-device items. |

| Industry Publisher B | USD 2.62 B (2026) | Relies more on fixed price progression and broader country lists, which can understate ASP lift from feature-rich systems in Western Europe and can smooth out tender-driven spikes. |

Overall, the comparison shows that year selection, Europe coverage, and how ASP is updated explain most of the gap. By keeping the device boundary clear, checking unit and price realism with interviews, and reviewing outliers country by country, the final number stays traceable to practical inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Europe ultrasound devices market?

The market is valued at USD 3.14 billion in 2026 and is forecast to hit USD 4.06 billion by 2031.

Which application segment is growing the fastest in Europe?

Obstetrics and gynecology leads growth at a 7.48% CAGR due to mandated prenatal screening across many countries.

Why are compact portable units gaining popularity?

They combine lower purchase prices with mobility, suiting ASCs, community diagnostic hubs and emergency departments that need imaging at the point of care.

Which country is projected to record the highest growth rate?

Spain is set to achieve an 8.58% CAGR because of major public investment in new outpatient imaging centers.

How do hospital decarbonization goals influence purchasing?

Ultrasound’s low lifecycle emissions make it a preferred modality as hospitals replace higher-energy CT and MRI scanners to meet net-zero targets.

Page last updated on: