Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

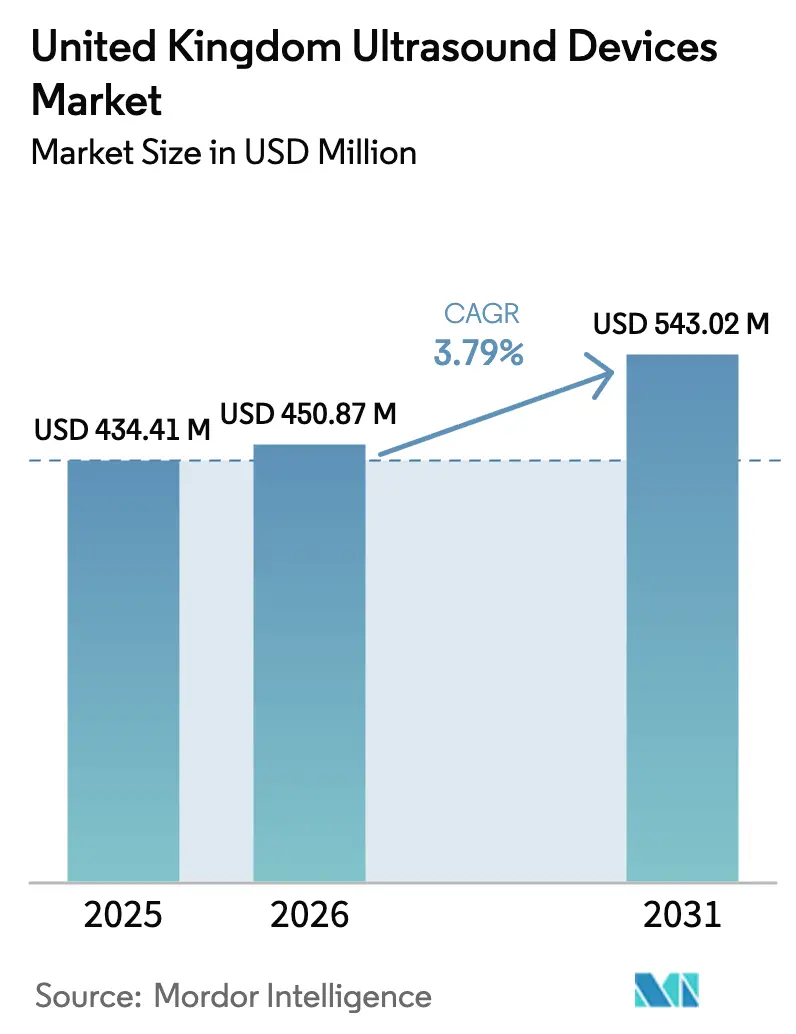

| Base Year Market Size (2025) | USD 434.41 Million |

| Market Size (2026) | USD 450.87 Million |

| Market Size (2031) | USD 543.02 Million |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

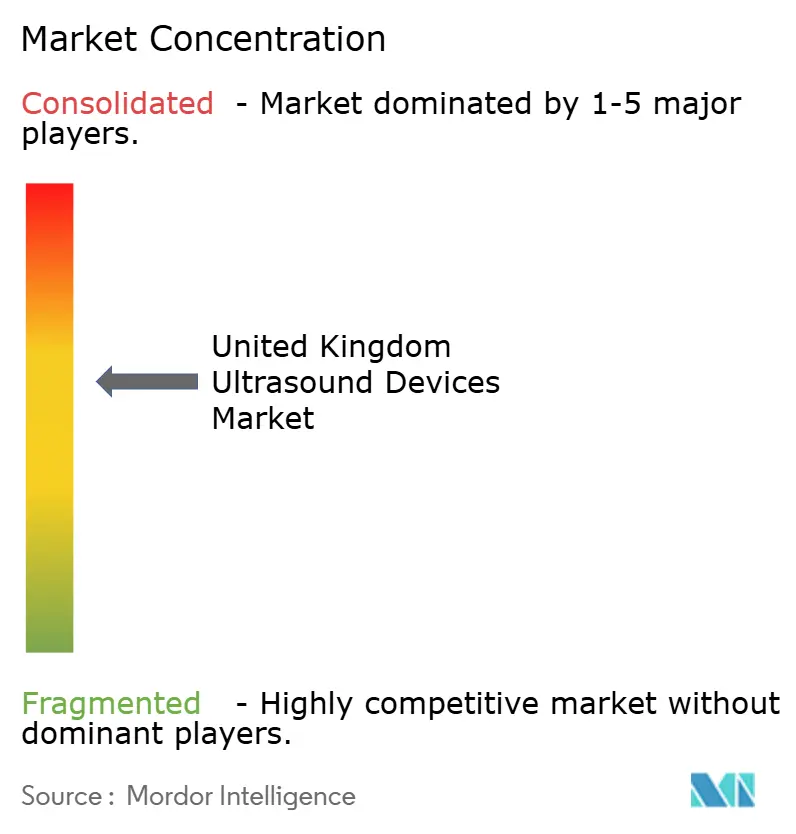

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Ultrasound Devices Market Analysis by Mordor Intelligence

The United Kingdom Ultrasound Devices Market size is expected to grow from USD 434.41 million in 2025 to USD 450.87 million in 2026 and is forecast to reach USD 543.02 million by 2031 at 3.79% CAGR over 2026-2031.

A favourable reimbursement climate for point-of-care imaging, coupled with sustained investments in NHS modernization programmes, underpins this steady trajectory. AI-driven workflow enhancements, expanding home-care deployments, and rising chronic disease diagnoses are accelerating replacement demand even as budgetary pressures persist in some community settings. Hand-held ultrasound models are redefining primary and emergency care pathways, while high-intensity focused ultrasound (HIFU) widens therapeutic opportunities in oncology and urology. Meanwhile, corporate consolidation around AI capabilities epitomised by GE HealthCare’s 2024 acquisition of Intelligent Ultrasound signals a transition toward fully integrated imaging ecosystems.

Key Report Takeaways

- By application, radiology accounted for 32.42% of the ultrasound devices market size in 2025; cardiology is forecast to expand at 6.73% CAGR to 2031.

- By technology, 3D & 4D ultrasound held 47.85% revenue share in 2025, whereas HIFU records the highest projected CAGR at 8.09% through 2031.

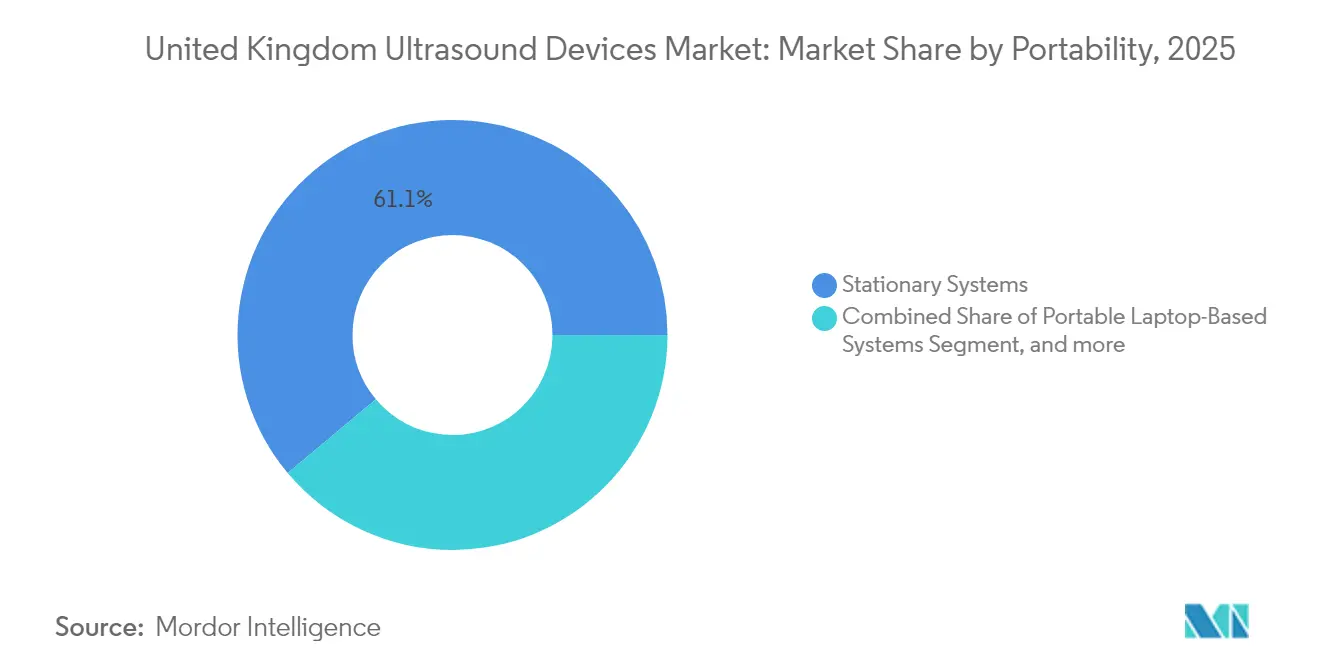

- By portability, stationary systems commanded 61.10% of ultrasound devices market share in 2025, whereas hand-held devices are projected to grow at 11.18% CAGR through 2031.

- By end user, NHS hospitals held 55.30% share of the ultrasound devices market in 2025, while home-care settings advance at a 9.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing burden of chronic diseases | +1.2% | National; highest in deprived urban & coastal areas | Long term (≥ 4 years) |

| Rapid adoption of hand-held ultrasound for rural & home diagnostics | +1.0% | National; early gains in rural regions | Medium term (2-4 years) |

| Technological advancements in ultrasound devices & rising diagnostic usage | +0.8% | National; concentrated in academic medical centres | Medium term (2-4 years) |

| Growing private fertility clinic segment & OB/GYN upgrades | +0.6% | Urban hubs with private care clusters | Short term (≤ 2 years) |

| Expansion of NHS diagnostic imaging modernisation programmes | +0.5% | National; phased roll-out via NHS Trusts | Short term (≤ 2 years) |

| Rising focus on women’s health & fertility monitoring | +0.4% | National; amplified in metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Chronic Diseases

England is projected to have 9.3 million residents living with major illness by 2040, with deprived communities bearing 80% of the additional burden. Cardiovascular conditions alone affect about 2.3 million people, prompting greater reliance on echocardiography and vascular studies. Cancer incidence is expected to climb from 420,000 new cases in 2025 to 506,000 by 2040, reinforcing the centrality of ultrasound in non-invasive tumour staging and therapy monitoring.[1]The Health Foundation, “Health in 2040: More of Us Living for Longer, but with Major Illness,” health.org.uk The cumulative effect is sustained demand for advanced transducers, contrast-enhanced studies, and AI-guided acquisition routines across secondary and primary care.

Rapid Adoption of Hand-Held Ultrasound for Rural & Home Diagnostics

Miniaturisation combined with real-time AI feedback is encouraging remote scanning in paramedic units, care homes, and patient residences. Twenty percent of UK clinicians already use AI in diagnostics, and 35% of NHS AI implementations now sit in imaging workflows. Caption Health’s home-based heart scan pilot illustrates how integrated algorithms reduce operator dependency, bridging workforce shortages while cutting hospital footfall.

Technological Advancements in Ultrasound Devices & Rising Diagnostic Usage

University College London’s photoacoustic tomography scanner creates 3-D vascular maps in minutes, capturing microvascular changes invisible to conventional 2-D imaging.[2]University College London, “Handheld Photoacoustic Tomography Scanner Enables Rapid 3-D Vessel Imaging,” ucl.ac.uk Ultrasound localisation microscopy offers myocardial resolution superior to CT angiography for coronary microvascular disease detection. Layering AI on these modalities automates measurements, streamlines reporting, and trims exam times by up to 40%, multiplying throughput without proportionate head-count growth.

Growing Private Fertility Clinic Segment Driving OB/GYN Ultrasound Upgrades

Private fertility centres are scaling capacity as 43% of workers aged 24-34 prioritise fertility benefits when choosing employers. Samsung Medison’s acquisition of prenatal AI firm Sonio reflects a race to standardise early-trimester measurements and improve anomaly detection. Clinics increasingly market 3D/4D and AI-guided fetal assessments as differentiators to attract self-pay patients, boosting turnover of premium obstetrics consoles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations prolonging product approvals | –0.5% | National | Short term (≤ 2 years) |

| Shortage of sonographers causing under-utilisation of installed base | –1.0% | National; acute in rural settings | Long term (≥ 4 years) |

| Budget constraints in community & rural healthcare | –0.6% | Selected rural & community hospitals | Medium term (2-4 years) |

| Competition from lower-cost imaging alternatives | –0.4% | National; highest in primary care | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations Prolonging Product Approvals

The MHRA’s new device framework, effective from Summer 2025, mandates risk-proportionate surveillance and formalises international recognition pathways. While alignment with Australian, Canadian, US, and EU certificates may shorten duplicate assessments, additional post-market reporting can extend total time-to-market for novel probes and software. Firms with deep regulatory benches will absorb the complexity more easily than start-ups, potentially tempering innovation velocity.[3]Medicines and Healthcare products Regulatory Agency, “UK Medical Device Regulations 2025: Statutory Instrument,” gov.uk

Shortage of Sonographers Causing Under-utilisation of Installed Base

Sonographers retire at 60.8 years on average, well before the general retirement age, leaving high-spec scanners idle during surge periods. The NHS has broadened scope-of-practice for physiotherapists to perform bedside musculoskeletal scans, yet throughput gaps persist. GE HealthCare’s ScanNav tools now guide non-expert operators to acceptable views, demonstrating how embedded AI can partly offset the human capital deficit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cardiology Gains Momentum Amidst Stable Radiology Demand

Radiology/general imaging retained 32.42% ultrasound devices market share in 2025, anchored by abdominal and small-parts examinations across NHS hospitals. Cardiology, however, is projected to outpace all other specialties at a 6.73% CAGR, propelled by microvascular imaging breakthroughs and increasing heart-failure screening in primary care. Ultrasound localisation microscopy enables wall-motion and perfusion analysis once reserved for MRI, broadening echocardiography’s clinical utility. Over the forecast, cardiology’s contribution to ultrasound devices market size is expected to add nearly USD 18 million, intensifying competition among vendors for premium cardiac probes.

Obstetrics & gynecology remains a mature but lucrative field. Home-based fetal growth monitoring trials underline how widespread AI integration may unlock new consumer-direct revenue streams. Critical care and anesthesiology segments increasingly rely on point-of-care systems for fast-track procedural guidance, sustaining baseline demand for robust portable consoles.

By Technology: HIFU Challenges the Dominance of 3D & 4D Systems

3D & 4D modalities commanded 47.85% share of ultrasound devices market size in 2025, supported by obstetric and structural-heart imaging workflows. Yet their growth is moderating as replacement cycles lengthen. By contrast, HIFU will expand at 8.09% CAGR, capturing oncology centres seeking organ-sparing alternatives to surgery. Ablatherm and Sonablate 500 platforms demonstrate 95% freedom from clinically significant prostate cancer, accelerating adoption in both private and NHS settings.

Doppler and contrast-enhanced imaging maintain relevance for hepatic lesions and vascular assessments, while AI post-processing packages elevate 2-D systems through automated vessel tracking and plaque quantification. Vendors are bundling advanced software to retain customers transitioning to mid-range consoles as budget pressures persist.

By Portability: Hand-Held Scanners Redraw Care Pathways

Stationary systems still represent 61.10% of ultrasound devices market share, particularly within tertiary referral centres requiring advanced elasticity imaging and multi-probe configurations. Nonetheless, hand-held devices will generate the highest incremental revenue, growing 11.18% each year. Comparative assessments highlight probe ergonomics, battery life, and secure cloud storage as decisive factors for procurement. The NHS Tech Devices framework, worth GBP 1.5 billion over four years, earmarks mobile imaging for accelerated rollout, signalling long-term institutional commitment to portability.

Cart-based units occupy a middle ground, balancing mobility with upgrade paths for AI modules and contrast packages. Integration with electronic patient records via secure Wi-Fi bolsters their relevance in high-turnover outpatient clinics.

By End User: Home-Care Settings Emerge as the Next Growth Frontier

NHS hospitals captured 55.30% of spending in 2025, fuelling core demand for replacement consoles and specialty transducers. Yet home-care environments will post a 9.88% CAGR as reimbursement policies evolve to support remote cardiac, obstetric, and pulmonary assessments. Caption Care’s home echocardiogram service illustrates how AI-guided acquisition democratises imaging for non-expert carers, reshaping follow-up protocols.

Private hospitals and fertility clinics capitalise on premium 3D/4D and AI-measured follicle tracking, while diagnostic imaging centres diversify into interventional ultrasound suites. General practitioners adopting compact scanners for abdominal complaints exemplify the device’s move toward the point of first contact.

Geography Analysis

London and the Southeast remain the epicentre of advanced ultrasound adoption, driven by teaching hospitals and a dense network of private fertility providers. These regions also host most early-stage trials for AI-enabled modalities, reinforcing their role as reference sites for vendor demonstrations. The North of England and Scotland are closing the technology gap via NHS modernisation funds that subsidise portable platforms in community diagnostic centres.

Rural Wales and parts of Northern Ireland still face limited sonographer availability, hindering full utilisation of installed scanners. Hand-held devices, supported by remote interpretation networks, are mitigating access gaps by allowing community nurses to capture images for off-site review.

Health inequality metrics show deprived coastal towns recording higher cardiovascular and metabolic disease incidence, prompting targeted deployment of point-of-care ultrasound programmes. The projected 9.3 million people with major illness by 2040 underscores the importance of equitable imaging dispersion, aligning national procurement frameworks with population-health objectives.

Competitive Landscape

The market exhibits moderate concentration. GE HealthCare leads through inorganic expansion and deep AI integration, holding sizeable footprints in cardiology and anesthesiology consoles. Siemens Healthineers and Philips leverage broad modality portfolios to cross-sell ultrasound into radiology and oncology pathways, while Canon Medical Systems focuses on software-driven image harmonisation to compete on diagnostic precision.

Samsung Medison’s 2024 purchase of Sonio highlights intensifying competition in the prenatal AI domain, a segment where accurate anomaly screening directly influences reimbursement rates. Disruptors such as Butterfly Network and Clarius Mobile Health court primary-care physicians with subscription-based software upgrades, threatening incumbent pricing power. Regulatory harmonisation efforts may level entry barriers for these agile players, but heightened post-market obligations favour enterprises with robust compliance infrastructures.

White-space opportunities persist in AI-guided workflow tools that shorten scan times, especially for nursing staff assuming ultrasound responsibilities. Therapeutic ultrasound sub-segments like HIFU and histotripsy also offer high-margin expansion paths as clinical trial data validates long-term outcomes.

United Kingdom Ultrasound Devices Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: GE HealthCare completed its USD 53 million acquisition of Intelligent Ultrasound's clinical AI business, integrating AI-driven tools into its ultrasound portfolio to enhance workflow and efficiency for clinicians

- September 2024: University College London researchers unveiled a breakthrough handheld scanner utilizing photoacoustic tomography imaging, enabling real-time, high-quality scans of blood vessels for earlier diagnosis of chronic diseases.

- April 2024: Intelligent Ultrasound Group PLC launched GE Healthcare Technologies Inc.'s SonoLyst software on its latest portfolio of ultrasound machines in the United Kingdom. Powered by Intelligent Ultrasound's ScanNav AI, SonoLystlive enables real-time capture of ultrasound images during mid-trimester scans. The software significantly enhances ultrasound image recognition capabilities. Additionally, SonoLystlive reduces the need for clinicians to manually freeze, annotate, and store images, cutting keystrokes by up to 65% and decreasing exam time for sonographers by up to 40%. This advancement not only improves workflow efficiency for healthcare professionals but also supports the growth of the ultrasound devices market by addressing the demand for cutting-edge, time-saving diagnostic tools.

United Kingdom Ultrasound Devices Market Report Scope

As per the scope of the report, ultrasonography is an imaging method that creates images of various body structures using high-frequency sound waves. They are used to evaluate a variety of disorders relating to the liver, kidneys, and other abdominal conditions, including usage in pregnancy. As a result, these devices have a variety of uses in the medical area, including diagnostic imaging and therapeutic modality. The United Kingdom Ultrasound Devices Market is Segmented by Application (Anesthesiology, Cardiology, Gynecology/Obstetrics, Musculoskeletal, Radiology, Critical Care, and Other Applications), Technology (2D Ultrasound Imaging, 3D and 4D Ultrasound Imaging, Doppler Imaging, and High-intensity Focused Ultrasound), and Type (Stationary Ultrasound and Portable Ultrasound). The report offers the value (in USD million) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology/Obstetrics |

| Radiology |

| Critical Care & Emergency Medicine |

| Other Applications |

By Technology

| 2-D Ultrasound Imaging |

| 3-D & 4-D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound (HIFU) |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Laptop-Based Systems |

| Handheld/Pocket Ultrasound Devices |

By End User

| NHS Hospitals |

| Private Hospitals & Clinics |

| Diagnostic Imaging Centres |

| Ambulatory Surgical Centres |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology/Obstetrics | |

| Radiology | |

| Critical Care & Emergency Medicine | |

| Other Applications | |

| By Technology | 2-D Ultrasound Imaging |

| 3-D & 4-D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound (HIFU) | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Laptop-Based Systems | |

| Handheld/Pocket Ultrasound Devices | |

| By End User | NHS Hospitals |

| Private Hospitals & Clinics | |

| Diagnostic Imaging Centres | |

| Ambulatory Surgical Centres | |

| Other End Users |

Key Questions Answered in the Report

What is the current size of the United Kingdom ultrasound devices market?

The ultrasound devices market size stands at USD 450.87 million in 2026 and is projected to reach USD 543.02 million by 2031.

Which segment is growing fastest by portability?

Hand-held devices are set to expand at 11.18% CAGR, driven by home-care and rural diagnostic use cases.

How will AI influence ultrasound usage over the next five years?

AI is expected to automate measurement, shorten scan times by up to 40%, and widen operator pools, supporting broader deployment across primary and community care.

What regulatory changes should manufacturers track?

The MHRA’s 2025 medical device framework introduces risk-proportionate post-market surveillance and mutual recognition routes, affecting approval timelines and compliance costs.

How significant is the sonographer shortage?

Earlier retirement ages create workforce gaps that lower scanner utilisation; AI-guided tools and expanded roles for allied professionals are being deployed to mitigate the shortfall.

Page last updated on: