Endoscopic Ultrasound Needles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 172.62 Million |

| Market Size (2031) | USD 236.49 Million |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscopic Ultrasound Needles Market Analysis by Mordor Intelligence

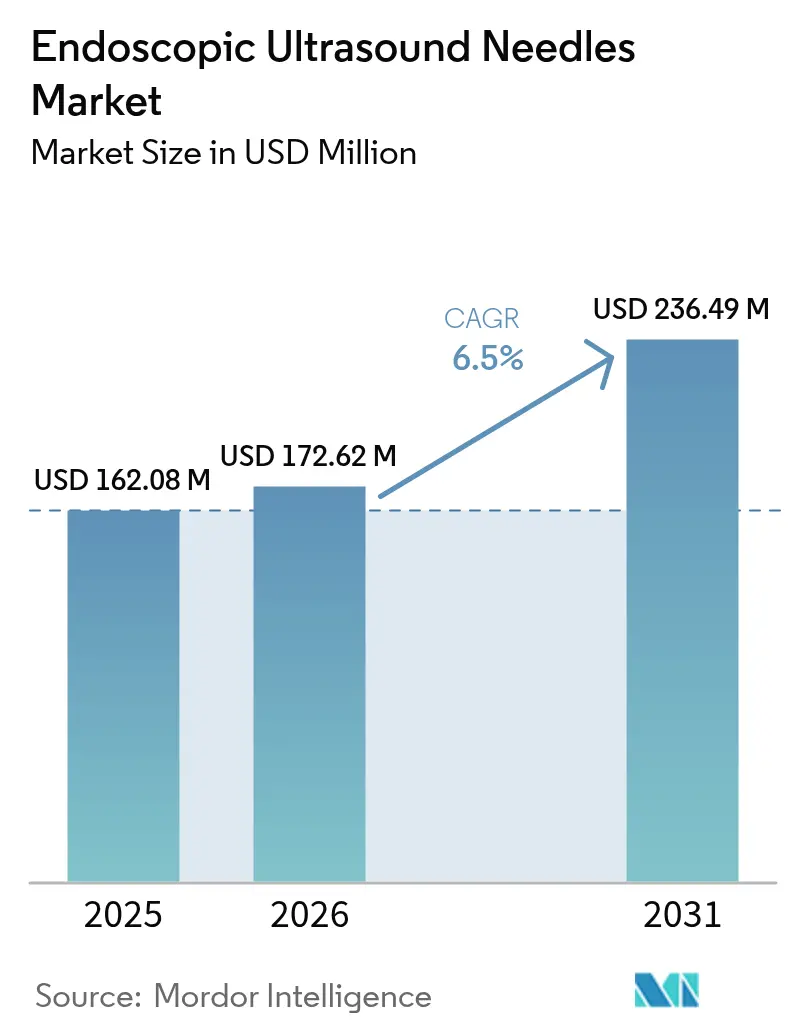

The endoscopic ultrasound needles market size was valued at USD 162.08 million in 2025 and estimated to grow from USD 172.62 million in 2026 to reach USD 236.49 million by 2031, at a CAGR of 6.50% during the forecast period (2026-2031). The growing demand for precision diagnostics, the rapid convergence of artificial intelligence with needle design, and the shift away from surgical biopsies underpin the steady expansion of the endoscopic ultrasound needles market. Hospitals continue to anchor global volumes, yet ambulatory surgical centers are winning share as outpatient biopsies gain traction. Fork-tip geometries, 25G gauges, and Nitinol construction collectively redefine sampling efficiency, while North America sustains its leadership through comprehensive reimbursement policies. Competitive intensity is shaped by proprietary tip designs, AI-enabled targeting technology, and strict FDA Class II requirements that raise entry barriers.

Key Report Takeaways

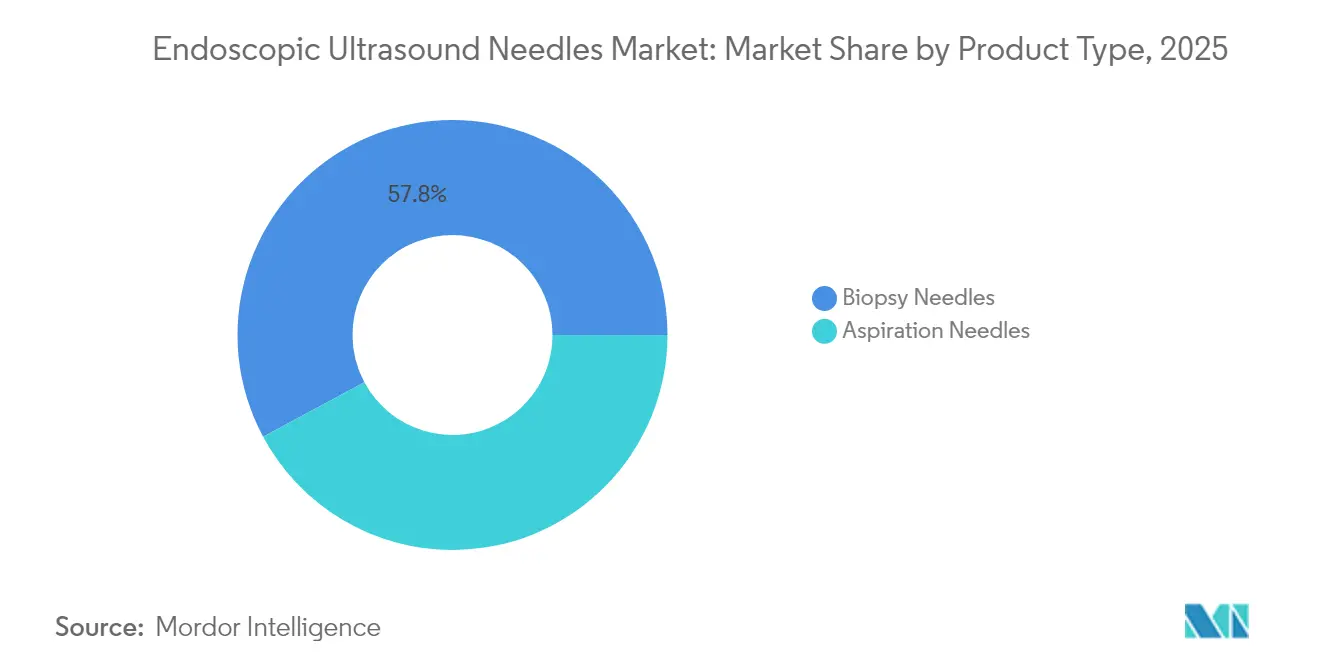

- By product type, biopsy needles captured 57.84% revenue share in 2025 and are projected to grow at 8.29% CAGR through 2031.

- By needle gauge, 22 G held 28.22% of the endoscopic ultrasound needles market share in 2025, while 25 G is projected to advance at a 7.41% CAGR to 2031.

- By tip design, Franseen needles led with a 30.05% share in 2025, and fork-tip designs are expanding at a 7.08% CAGR.

- By application, pancreatic lesions accounted for a 28.52% share in 2025, while bronchial or mediastinal lesions are projected to rise at an 8.62% CAGR.

- By end user, hospitals retained 42.98% share in 2025 and ambulatory surgical centers are growing at 8.74% CAGR.

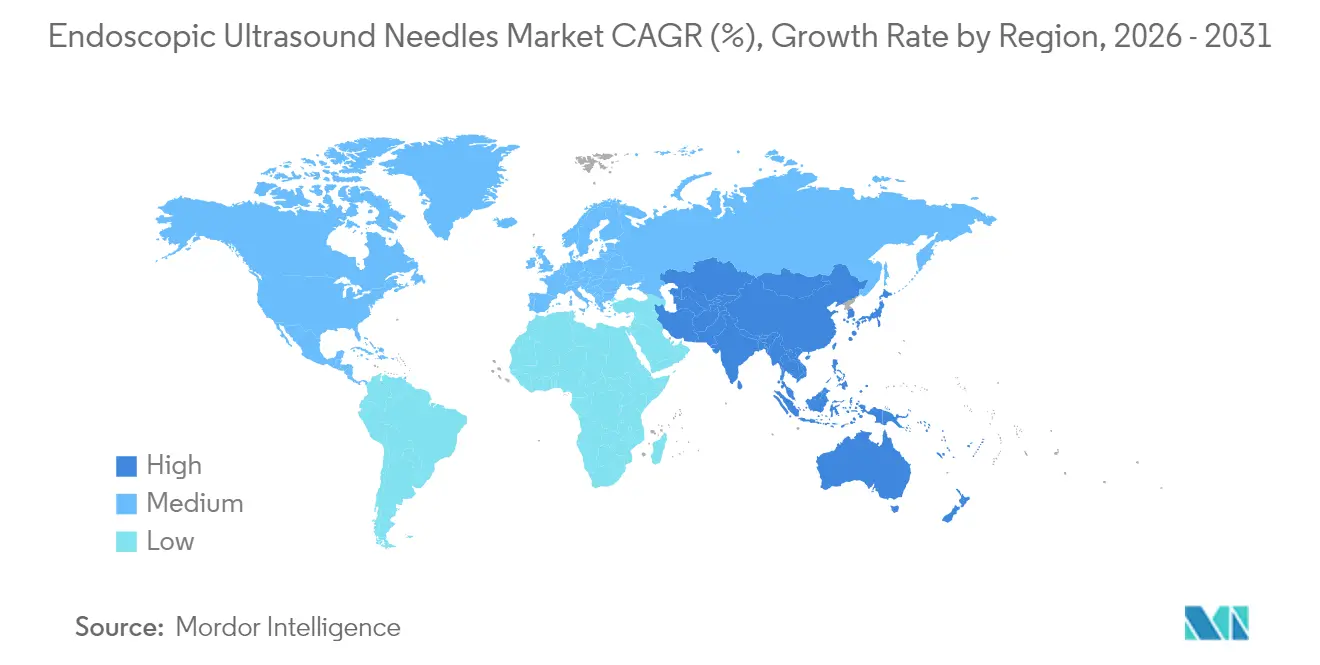

- By geography, North America held 41.95% share in 2025 and Asia-Pacific is registering the fastest 7.29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Endoscopic Ultrasound Needles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Gastrointestinal And Pancreatic Cancers | 1.80% | North America, Asia-Pacific | Medium term (2–4 years) |

| Rising Preference For Minimally Invasive Diagnostic Procedures | 1.50% | Global, led by developed markets | Short term (≤ 2 years) |

| Increasing Geriatric Population With Comorbidities | 1.20% | North America, Europe, Japan | Long term (≥ 4 years) |

| Favorable Reimbursement Policies For Endoscopic Ultrasound Procedures | 1.10% | United States, Western Europe | Short term (≤ 2 years) |

| Rapid Adoption Of Franseen And Fork-Tip Fine Needle Biopsy Technology | 1.00% | Global, higher uptake in tertiary centers | Medium term (2–4 years) |

| Integration Of AI-Guided Targeting Systems In EUS Platforms | 0.90% | North America, Europe, expanding to Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Gastrointestinal and Pancreatic Cancers

Early-onset pancreatic cancer diagnoses have risen 2.47% annually since 2019, increasing reliance on tissue sampling for definitive staging[1]American Cancer Society, “Pancreatic Cancer Facts & Figures,” cancer.org. Molecular profiling protocols now accompany most pancreatic biopsy requests, which boosts daily use of EUS needles in oncology centers. Higher sample-volume requirements favor biopsy rather than aspiration tools and reinforce hospital procurement of premium designs. The endoscopic ultrasound needles market, therefore, benefits from the oncology community’s shift toward large-core tissue retrieval. In the Asia-Pacific region, national cancer plans mirror this trend, accelerating device adoption across public hospitals.

Rising Preference for Minimally Invasive Diagnostic Procedures

CMS broadened coverage for EUS-guided fine needle aspiration and biopsy in 2024, validating the approach as cost-effective compared with open or laparoscopic biopsies[2]Centers for Medicare & Medicaid Services, “National Coverage Determinations,” cms.gov. Clinical evidence shows a single EUS pass can achieve histological confirmation that once required multiple surgical attempts, cutting anesthesia exposure and recovery time. Ambulatory surgical centers report higher patient satisfaction scores and stronger profit margins when using streamlined outpatient EUS workflows. These factors collectively stimulate procurement budgets, sustaining near-term growth in the Endoscopic Ultrasound Needles market. Manufacturers are therefore prioritizing compact systems tailored to outpatient settings.

Increasing Geriatric Population with Comorbidities

Adults aged 65 and older represent 67% of pancreatic cancer cases and often cannot tolerate surgical biopsies due to cardiovascular risk[3]National Cancer Institute, “Cancer Stat Facts,” cancer.gov. Conscious-sedation EUS procedures mitigate anesthesia-related complications while maintaining a high diagnostic yield. Ambulatory clinics offer geriatric-friendly scheduling and same-day discharge, both of which are attractive to older patients managing multiple disorders. This demographic alignment boosts procedure volumes and stable demand for single-use, ultra-fine needles. Over the long term, aging societies in Europe and Japan ensure a durable base for the endoscopic ultrasound needles market.

Integration of AI-Guided Targeting Systems in EUS Platforms

Machine learning algorithms now achieve 94% accuracy in pancreatic mass detection, compared to 78% for conventional imaging. Real-time lesion mapping reduces repeat procedures and drives first-pass success beyond 90%. Hospitals upgrading imaging stacks inevitably refresh compatible biopsy tools, expanding high-margin needle sales. Vendors integrating predictive software and proprietary tip designs create closed ecosystems, which deepen client lock-in and lift replacement cycles across the endoscopic ultrasound needles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Skilled Endoscopic Ultrasound Operators | −1.1% | Most acute in emerging markets | Long term (≥ 4 years) |

| High Cost Of Premium Biopsy Needles And Reusable Accessories | −0.8% | Asia-Pacific, Latin America | Medium term (2–4 years) |

| Stringent Infection-Control Protocols Increasing Procedure Turnaround Time | −0.6% | Global, stricter in Europe and North America | Short term (≤ 2 years) |

| Competition From Emerging Non-Invasive Liquid Biopsy Technologies | −0.5% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Endoscopic Ultrasound Operators

Fewer than 15% of practicing gastroenterologists perform advanced EUS, limiting daily capacity in both urban and rural centers. Training requires 150–200 mentored cases, a hurdle for hospitals with thin specialist rosters. Asia-Pacific health systems build new cancer institutes faster than they can train operators, which caps near-term installations despite equipment subsidies. Private teaching partnerships and tele-proctorship programs aim to narrow the skills gap, but the shortage remains a long-tail restraint on the Endoscopic Ultrasound Needles market.

High Cost of Premium Biopsy Needles and Reusable Accessories

Next-generation Fork-Tip or Franseen needles cost three to four times more than standard lancet models, and strict infection-control rules forbid reuse. Budget-sensitive hospitals in Latin America and certain parts of Asia often restrict premium products to a small subset of reimbursed patients, opting for more affordable cytology tools for routine work. Ambulatory centers must balance device spend against tight payer contracts, which slows penetration of high-end designs. Persistent price pressure therefore tempers overall value growth of the endoscopic ultrasound needles market, even as unit volumes climb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type – Biopsy Needles Drive Market Evolution

Biopsy needles held a 57.84% market share of the endoscopic ultrasound needles market in 2025, reflecting oncologists’ demand for intact core tissue that enables comprehensive molecular profiling. Their 8.29% CAGR through 2031 outpaces aspiration tools as personalized medicine protocols standardize across cancer centers. The endoscopic ultrasound needles market benefits from this structural shift, with biopsy instruments commanding premium pricing against stable year-on-year volume growth.

Aspiration needles retain their value for rapid on-site cytology, particularly in community settings without access to molecular labs. Yet the widening tissue requirements of pancreatic, biliary, and bronchial oncology place a growing ceiling on cytology-only devices. Established vendors leverage FDA 510(k) pathways to deploy iterative enhancements that maintain regulatory compliance while boosting diagnostic yield.

By Needle Gauge – Ultra-Fine Precision Gains Momentum

The 22 G gauge provided the largest contribution at 28.22% in 2025, balancing core volume with manageable bleeding risk. However the 25 G category shows a 7.41% CAGR through 2031, winning adoption for delicate pancreatic and pediatric cases where minimal trauma is paramount. Endoscopic Ultrasound Needles market size for 25 G solutions is projected to expand steadily as nitinol alloys allow thinner walls yet maintain lumen integrity.

Larger 19 G products support demanding genomic studies at academic centers, although slower growth keeps them niche. Gauge selection remains tightly linked to FDA validation protocols that test each diameter for tensile strength and biocompatibility.

By Tip Design – Fork-Tip Innovation Reshapes Sampling Efficiency

Franseen tips controlled 30.05% share in 2025, but Fork-Tip designs post the highest 7.08% CAGR to 2031. Comparative trials demonstrate higher intact-core rates and fewer passes per case, which aligns with payer pressure to shorten procedure time. The endoscopic ultrasound needles market therefore responds with rapid product cycles emphasizing proprietary cutting surfaces.

Lancet and side-beveled tools remain relevant for hyper-vascular lesions where controlled entry reduces hemorrhage risk. Collaborative R&D between STARmed and Olympus illustrates the strategic value of pairing surface metallurgy with ergonomics to protect share in this competitive arena.

By Application – Bronchial Sampling Emerges as Growth Driver

Pancreatic lesions accounted for 28.52% of global procedures in 2025, confirming the organ’s ongoing diagnostic challenge. Yet bronchial and mediastinal indications are clocking an 8.62% CAGR as pulmonologists adopt EUS-bronchoscope hybrids for lung cancer staging. Endoscopic Ultrasound Needles market size in thoracic oncology thus expands beyond classical gastroenterology.

Biliary strictures and gastrointestinal wall masses add diversified volume, supported by 2024 American College of Gastroenterology guidelines that endorse EUS biopsy for indeterminate biliary narrowing.

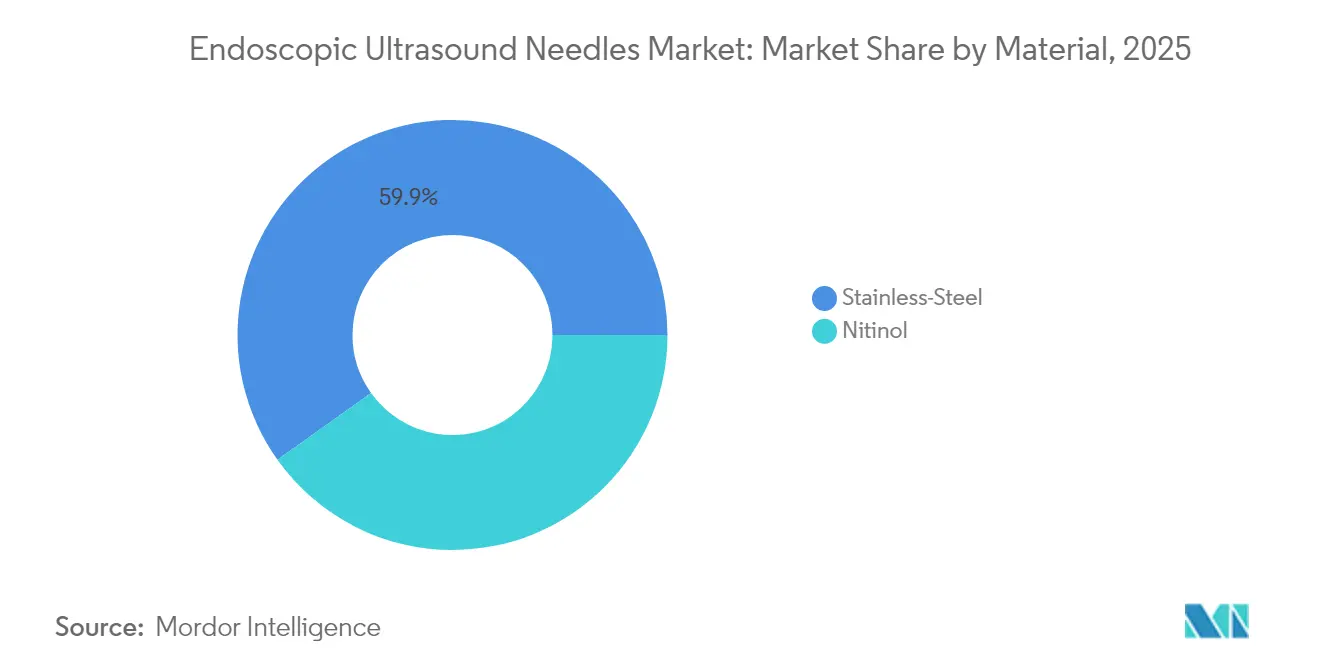

By Material – Nitinol Innovation Challenges Steel Dominance

Stainless steel held 59.86% share in 2025 due to cost advantages and well-understood mechanical behavior. Nitinol grows at 7.38% CAGR by offering flexibility and shape memory that preserve tip sharpness through multiple passes. Endoscopic ultrasound needles market share for nitinol climbs fastest in centers that tackle tortuous anatomy such as pancreatic tail lesions.

ISO 13485 quality frameworks guide alloy consistency, corrosion resistance, and manufacturing traceability, building clinician trust in these premium devices.

By End User – Ambulatory Centers Capture Market Momentum

Hospitals retained a 42.98% share in 2025, but ambulatory surgical centers posted a robust 8.74% CAGR through 2031. Medicare reimbursement parity and consumer preference for outpatient care boost procedure migration. The endoscopic ultrasound needles market size within ambulatory centers is expected to expand as compact cart-based EUS platforms become more prevalent in suburban clinics.

Specialty cancer clinics leverage high throughput to negotiate bulk prices, sustaining demand for single-use needles that avoid reprocessing overhead. Device makers now tailor packaging and accessory kits for same-day discharge workflows, strengthening their positioning with facility administrators.

Geography Analysis

North America generated 41.95% of global revenue in 2025, buoyed by CPT codes 43238 and 43242 that secure reimbursement in both hospital and ambulatory settings. Academic networks funnel constant clinical trials, which accelerates early adoption of AI-guided targeting and nitinol needles. Canadian centers follow U.S. protocols, while Mexican medical tourism funnels additional volumes from uninsured U.S. patients seeking lower procedure costs.

Asia-Pacific records the fastest 7.29% CAGR, driven by government oncology initiatives, growing specialist training pipelines, and urban hospital expansion. China’s cancer screening plan funds EUS suites in provincial centers, while Japan’s aging demographics propel demand for gentler diagnostics. Private hospitals in India add premium EUS services for overseas patients, broadening the endoscopic ultrasound needles market footprint. Diverse regulatory regimes require tailored submissions, but recent alignment of China’s National Medical Products Administration with ISO standards eases entry for global brands.

Europe exhibits steady growth anchored in evidence-based guidelines and well-funded universal healthcare. Germany, the United Kingdom, and France lead installations, often pairing high-end needles with AI-assisted imaging upgrades. Southern Europe trails slightly yet benefits from EU Medical Device Regulation harmonization, which streamlines purchasing decisions. Real-world evidence programs across university hospitals further validate performance claims, reinforcing clinician confidence in new designs.

Competitive Landscape

The endoscopic ultrasound needles industry shows moderate fragmentation. No single vendor exceeds a one-third share, and the top five together control under 50%, creating space for mid-sized specialists. Boston Scientific and Olympus leverage integrated scope-to-needle ecosystems that encourage bundled procurement contracts. Cook Medical focuses on core-biopsy geometry, while Fujifilm and Pentax rely on channel partnerships to expand regional reach.

Differentiation centers on proprietary tip designs, alloy composition, and AI-enabled positioning software. Vendors file continuous 510(k) submissions to sustain product cadence, knowing minor performance gains can sway hospital value analyses. Strategic collaborations, such as the 2024 STARmed-Olympus alliance, combine materials engineering with distribution muscle to accelerate market penetration.

New entrants emphasize ultra-fine pediatric gauges, reusable handle systems with disposable sheaths, and software modules that overlay lesion maps on live ultrasound feeds. These niche offerings seek to exploit unmet needs rather than confront incumbents head-on. Over the planning horizon, consolidation remains plausible if dominant imaging vendors pursue bolt-on acquisitions to close technology gaps.

Endoscopic Ultrasound Needles Industry Leaders

Medtronic PLC

CONMED Corporation

Olympus Corporation

Boston Scientific Corporation

Cook Group Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Olympus launched the SecureFlex needle system with enhanced flexibility for difficult anatomy, maintaining tip sharpness throughout prolonged cases

- February 2025: Limaca Medical commenced U.S. sales of its Precision-GI™ platform targeted at high-volume ambulatory settings

- May 2024: Cook Medical launched EchoTip AcuCore needles to capture larger core specimens for genomic profiling.

Global Endoscopic Ultrasound Needles Market Report Scope

As per the scope of the report, endoscopic ultrasound (EUS) needles are specialized biopsy tools used during endoscopic ultrasound procedures to obtain tissue samples from organs and lesions within or adjacent to the gastrointestinal tract. They enable minimally invasive fine-needle aspiration (FNA) or fine-needle biopsy (FNB), providing high diagnostic accuracy for conditions like pancreatic, biliary, and mediastinal lesions.

The endoscopic ultrasound needles market is segmented by Product (Aspiration Needles and Biopsy Needles), Needle Gauge (19G, 22G, 25G), Tip Design (Lancet, Franseen, Fork-Tip, Side-Beveled), Application (Pancreatic Lesions, Gastrointestinal Wall Lesions, Bronchial/Mediastinal Lesions, Biliary Lesions), Material (Stainless-Steel, Nitinol), End-User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and geography (North America, Europe, Asia Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Aspiration Needles |

| Biopsy Needles |

| 19G |

| 22G |

| 25G |

| Lancet |

| Franseen |

| Fork-Tip |

| Side-Beveled |

| Pancreatic Lesions |

| Gastrointestinal Wall Lesions |

| Bronchial / Mediastinal Lesions |

| Biliary Lesions |

| Stainless-Steel |

| Nitinol |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Aspiration Needles | |

| Biopsy Needles | ||

| By Needle Gauge | 19G | |

| 22G | ||

| 25G | ||

| By Tip Design | Lancet | |

| Franseen | ||

| Fork-Tip | ||

| Side-Beveled | ||

| By Application | Pancreatic Lesions | |

| Gastrointestinal Wall Lesions | ||

| Bronchial / Mediastinal Lesions | ||

| Biliary Lesions | ||

| By Material | Stainless-Steel | |

| Nitinol | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Global Endoscopic Ultrasound Needles Market?

The Global Endoscopic Ultrasound Needles Market size is expected to reach USD 172.62 million in 2026 and grow at a CAGR of 6.50% to reach USD 236.49 million by 2031.

What is the current Global Endoscopic Ultrasound Needles Market size?

In 2026, the Global Endoscopic Ultrasound Needles Market size is expected to reach USD 172.62 million.

Who are the key players in Global Endoscopic Ultrasound Needles Market?

Medtronic PLC, CONMED Corporation, Olympus Corporation, Boston Scientific Corporation and Cook Group Incorporated are the major companies operating in the Global Endoscopic Ultrasound Needles Market.

Which is the fastest growing region in Global Endoscopic Ultrasound Needles Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Endoscopic Ultrasound Needles Market?

In 2026, the North America accounts for the largest market share in Global Endoscopic Ultrasound Needles Market.

What years does this Global Endoscopic Ultrasound Needles Market cover, and what was the market size in 2025?

In 2025, the Global Endoscopic Ultrasound Needles Market size was estimated at USD 172.62 million. The report covers the Global Endoscopic Ultrasound Needles Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Endoscopic Ultrasound Needles Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: