Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

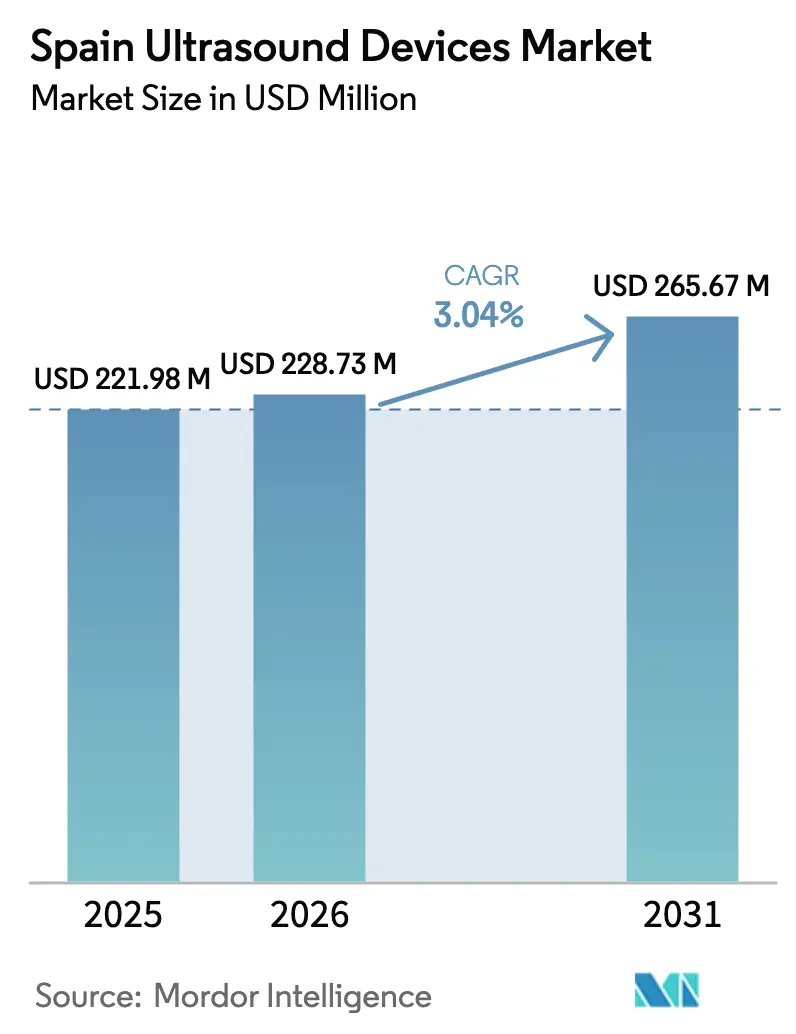

| Base Year Market Size (2025) | USD 221.98 Million |

| Market Size (2026) | USD 228.73 Million |

| Market Size (2031) | USD 265.67 Million |

| Growth Rate (2026 - 2031) | 3.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Ultrasound Devices Market Analysis by Mordor Intelligence

The Spain Ultrasound Devices Market size is expected to grow from USD 221.98 million in 2025 to USD 228.73 million in 2026 and is forecast to reach USD 265.67 million by 2031 at 3.04% CAGR over 2026-2031.

Public sources account for 71.7% of national health spending, so device purchasing decisions continuously balance universal‐coverage goals with cost‐effectiveness mandates. An aging population, the normalization of bedside imaging protocols after COVID-19, and rapid uptake of portable systems combine to sustain demand even as hospital capital budgets tighten. AI-guided workflow tools reduce operator dependence and accelerate throughput, encouraging both public and private providers to refresh installed fleets. At the same time, the EU Medical Device Regulation (MDR) and Spain’s AEMPS certification timelines raise compliance costs that slow the launch of premium systems. Market participants therefore prioritize platform interoperability, simplified training requirements, and clear cost-utility evidence to secure tenders across Spain’s autonomous regions.

Key Report Takeaways

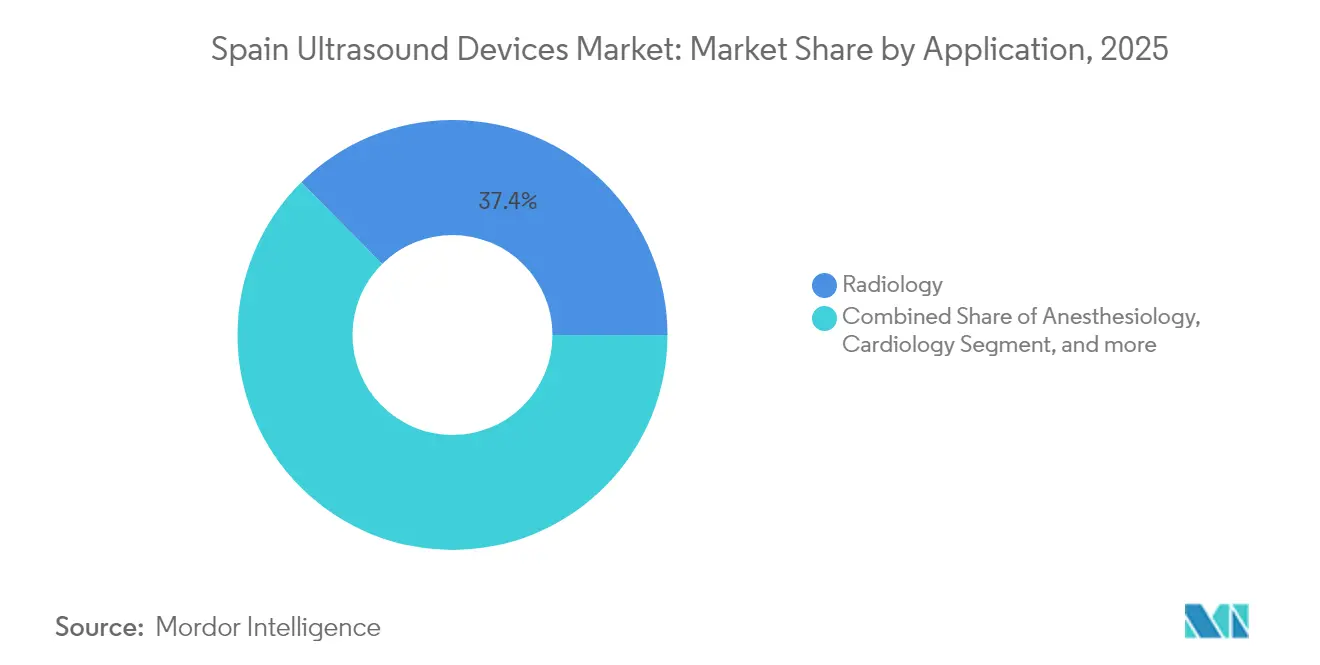

- By application, radiology led with 37.42% revenue share of the Spain ultrasound devices market share in 2025, while Critical Care is projected to post the fastest 5.87% CAGR through 2031.

- By technology, 3D & 4D captured 41.12% of the Spain ultrasound devices market size in 2025, whereas high-intensity focused ultrasound is set to expand at a 5.36% CAGR to 2031.

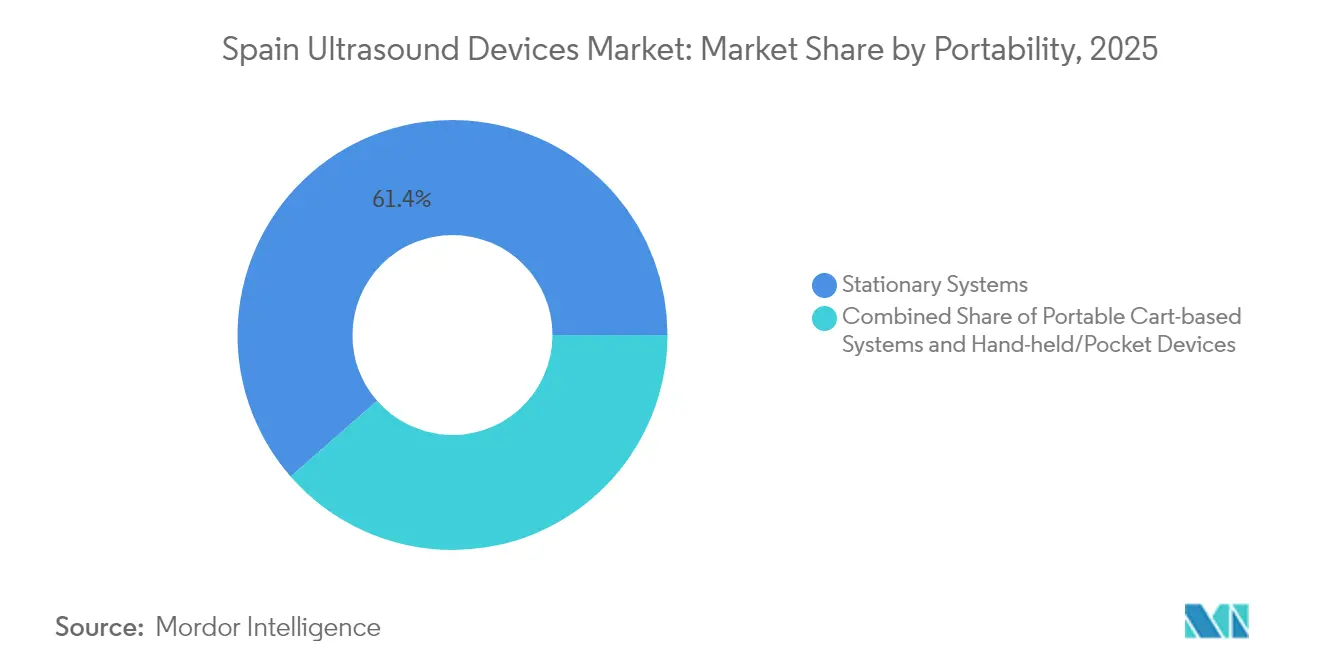

- By portability, stationary systems accounted for 61.43% share of the Spain ultrasound devices market size in 2025, but hand-held/pocket devices are forecast to climb at a 7.18% CAGR through 2031.

- By end user, public hospitals commanded 38.92% of the Spain ultrasound devices market size in 2025, while home healthcare settings are advancing at a 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic disease burden | +0.8% | National; higher in rural provinces | Long term (≥ 4 years) |

| Point-of-care and handheld ultrasound uptake | +0.6% | Early acceleration in Andalusia, Canary, Madrid | Medium term (2-4 years) |

| Oncology and cardiac service capacity build-outs | +0.4% | Castilla y León, Valencia, Catalonia | Medium term (2-4 years) |

| AI-enabled workflow optimization | +0.3% | Barcelona, Madrid, Sevilla | Short term (≤ 2 years) |

| Post-COVID bedside imaging standardization | +0.2% | All autonomous regions | Short term (≤ 2 years) |

| Tele-ultrasound pilots in remote islands | +0.1% | Canary, Balearic, rural interiors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging population and chronic disease burden

Rising life expectancy lifts ultrasound demand across cardiology, endocrinology, and musculoskeletal care. The European Central Bank projects aging-related health costs to climb by 7 percentage points of GDP by 2070, placing diagnostic efficiency at the center of budget planning. AI-assisted muscle assessment already achieves 82.3% accuracy in detecting malnutrition-linked sarcopenia, illustrating how advanced algorithms help physicians manage geriatric syndromes with limited scan time.[1]Juan Martinez et al., “AI Muscle Ultrasound Accuracy in Elderly Nutrition,” MDPI Nutrients, mdpi.com

Point-of-care and handheld ultrasound uptake

The Andalusian health service has trained more than 1,000 primary-care clinicians in abdominal scanning, reinforcing policy momentum for bedside imaging programs.[2]Servicio Andaluz de Salud, “Plan de Formación en Ecografía Abdominal,” juntadeandalucia.es Comparative evaluations of devices like Vscan Air and SonoEye confirm diagnostic performance on par with full-size consoles, encouraging hospitals to adopt “probe-first” triage pathways. Structured POCUS guidance from WONCA Europe underscores the technology’s role in closing rural care gaps.

Oncology and cardiac service capacity build-outs

A EUR 120 (USD 139) million European Investment Bank loan is modernizing five Castilla y León hospitals, expanding imaging suites that favor multipurpose ultrasound systems.[3]European Investment Bank, “Hospital Modernization Castilla y León,” eib.org Galicia’s electronic cardiology consultation program cut waiting times by 51.8% for complex oncology patients, demonstrating how integrated ultrasound pathways relieve specialist bottlenecks. Instituto Cartuja’s adoption of MR-guided focused ultrasound for uterine fibroids showcases therapeutic opportunities beyond diagnostics.

AI-enabled workflow optimization

Spanish centers are piloting AI guidance that lets non-sonographer nurses diagnose deep vein thrombosis with up to 98% sensitivity, tackling staffing shortages during night shifts. Another multicenter study reached 94% patient-level accuracy in infant meningitis screening, suggesting AI can reduce invasive lumbar punctures. Government research grants confirm national commitment to algorithm-ready imaging ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU MDR and AEMPS approval timelines | -0.4% | National; affects all manufacturers | Long term (≥ 4 years) |

| Public procurement price pressure | -0.3% | High in regions with tight budgets | Medium term (2-4 years) |

| Shortage of accredited sonographers | -0.2% | Acute in rural and island territories | Long term (≥ 4 years) |

| Hospital CAPEX reallocation post-COVID | -0.1% | Public hospitals nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU MDR and AEMPS approval timelines

Low certification throughput under the new regulation has extended market-entry cycles. The Medical Device Coordination Group noted backlog risks through 2025, prompting manufacturers to reroute launch budgets toward post-market surveillance rather than innovation. Spain’s AEMPS adds localized clinical data requirements, stretching smaller companies’ resources.

Public procurement price pressure

Value-based tendering emphasizes outcomes, yet hospital committees still gravitate to lowest-price bids when evidence is inconclusive. Health-technology assessors apply cost-effectiveness thresholds below EUR 30,000 (USD 34,929) per life-year gained, filtering out premium consoles lacking head-to-head savings data. Providers therefore favor versatile systems that cover multiple disciplines with minimal accessory spend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care expands bedside imaging horizons

Radiology remained the largest contributor, holding 37.42% of Spain ultrasound devices market share in 2025. Critical Care, while smaller, is projected to deliver a 5.87% CAGR thanks to mandatory ultrasound competencies in intensive-care residency programs. Spain ultrasound devices market size for critical care is on track to bridge the capacity gap created by rising admissions of multimorbid elderly patients. Hospitals equip shock management teams with handheld probes that facilitate rapid fluid-status checks and cardiac function snapshots. Meanwhile, cardiology leverages electronic consultation models to accelerate echo interpretation, and gynecology/obstetrics integrates AI Doppler analytics to shorten prenatal visits. Musculoskeletal and rheumatology practitioners have raised ultrasound adoption to 90% of practice units, reflecting clinician comfort with in-office joint evaluation. Urology and vascular labs seize focused ultrasound for non-invasive ablation, and emergency departments rely on portable scanners for rule-out protocols in trauma bays.

Spain ultrasound devices market participants recognize that cross-department sharing of consoles boosts utilization rates, a key tender criterion. Structured accreditation from the Spanish Society of Intensive Medicine underpins consistent image quality, while AI decision support reduces inter-observer variability. As reimbursement moves toward bundled-care models, multispecialty ultrasound applications will remain central to cost-containment strategies.

By Technology: HIFU redefines therapeutic potential

3D & 4D imaging secured 41.12% of Spain ultrasound devices market size in 2025, driven by obstetric volume and oncologic staging needs. High-intensity Focused Ultrasound is poised for a 5.36% CAGR, reflecting Instituto Cartuja’s success with MRgFUS uterine fibroid therapy and the CE extension for adenomyosis. Spain ultrasound devices market stakeholders note that HIFU’s non-invasive nature lowers postoperative stays, aligning with value-based care metrics. Conventional 2D imaging persists in primary care, where the Canary Islands deployment verifies its relevance for broad access. Doppler innovation accelerates through AI auto-classification that trims fetal-monitoring workflow time. Wireless and smartphone-linked probes broaden research participation and support remote training, offsetting the shortage of academic sonographers.

Developers focus on open-source operating systems that cut licensing expenses and encourage agile upgrades. This orientation complements Spain’s need for long hardware life cycles and future-proofed connectivity amid evolving MDR software classifications.

By Portability: Handheld probes shift scanning to the patient

Stationary consoles retain 61.43% share, anchored by tertiary-center radiology suites. Nevertheless, handheld scanners project a 7.18% CAGR, fueled by improvements in B-mode resolution and battery autonomy. Spain ultrasound devices market stakeholders observe that emergency physicians using Butterfly iQ+ reached 91.7% sensitivity for retinal-detachment detection, and prehospital crews achieved 79.5% agreement with in-hospital findings during trauma transfer. Cart-based portables serve mixed-acuity wards, balancing power and mobility. Wireless advances minimize infection-control steps, a post-COVID purchasing imperative.

Handheld makers emphasize subscription pricing that bundles cloud archiving and AI triage, lowering upfront barriers. Health regions with dispersed clinics such as Extremadura and Aragón prioritize pocket models that sync to electronic health records over cellular networks, ensuring clinical documentation continuity.

By End User: Home healthcare captures decentralized demand

Public Hospitals remained the largest customers with 38.92% of Spain ultrasound devices market size in 2025. Yet Home Healthcare Settings show a 6.74% CAGR, buoyed by telemedicine platforms that integrate high-definition video with ultrasound feeds. La Palma’s program saved more than EUR 1 (USD 1.16) million in annual travel costs, demonstrating economic viability. Private Hospitals harness premium imaging for specialty services such as reproductive medicine, while diagnostic centers streamline throughput via AI triage that flags normal exams for rapid reporting. Emergency medical services and mobile units deploy ruggedized probes to improve triage at mass-casualty scenes.

Remote-guided scanning protocols allow family physicians to consult specialists in real time, expanding ultrasound’s footprint beyond traditional brick-and-mortar sites. Device makers now collaborate with telecom operators to guarantee bandwidth in mountainous areas, an essential step to sustaining image fidelity during home visits.

Geography Analysis

Spain ultrasound devices market exhibits pronounced regional patterns shaped by autonomous budgeting and geography. Andalusia leads primary-care integration with over 1,000 clinicians certified in abdominal ultrasound, resulting in faster referrals for hepatobiliary diseases. The Canary archipelago pioneered a network of 57 primary-care ecographs linked to radiologists on the mainland, lowering diagnostic delays for island residents. Madrid and Barcelona host research clusters that test AI-driven workflow engines financed by the national digital-transformation agenda.

Valencia’s flood response during the 2024 DANA storms validated the resilience of portable systems that continued operating despite power limitations. Galicia’s e-cardiology consultations trimmed waitlists for oncology patients needing echo clearance, demonstrating how digital tools expedite imaging access. Overall, Spain ultrasound devices market participants tailor go-to-market plans to each region’s procurement norms and clinical priorities. Island territories require rugged, lightweight probes with cloud connectivity, while metropolitan centers demand AI-rich consoles that streamline radiology throughput. The coexistence of these needs ensures a steady replacement cycle through the forecast horizon.

Regulatory Landscape

Ultrasound devices in Spain operate under the EU Medical Device Regulation (MDR 2017/745), with national oversight led by the Agencia Espanola de Medicamentos y Productos Sanitarios (AEMPS) under the Ministry of Health. Royal Decree 192/2023 brings Spanish device requirements in line with the MDR and reinforces obligations for economic operators, including Spain-specific registration for commercialization (Registro de Comercializacion) alongside EU-level processes such as EUDAMED. Conformity assessment is carried out via notified bodies, including the Spain-designated Centro Nacional de Certificacion de Productos Sanitarios (CNCps, NB 0318), while manufacturers and importers manage increased documentation and post-market surveillance expectations under the MDR.

In 2026, Spain added policy levers that tighten the link between evidence and public funding decisions for health technologies. Real Decreto 415/2026 (27 May 2026) set a formal framework for health technology assessment (HTA), assigning RedETS to evaluate non-pharmacological technologies, which puts imaging equipment and ultrasound-based AI applications closer to structured inclusion, financing, and pricing within the National Health System. At the same time, Royal Decree 90/2026 introduced a selective financing regime for certain medical devices charged to the pharmaceutical provision of the NHS (effective 1 July 2026), which increases the need for dossier-ready clinical and economic evidence for ultrasound used in non-hospital care pathways.

Competitive Landscape

Competition is moderately fragmented. Global conglomerates leverage full-line portfolios and extensive service networks, while local disruptors target portability and AI niches. Product differentiation centers on embedded decision support, wireless data security, and cross-modality integration rather than list price. Partnerships between hospital consortia and software start-ups have yielded AI guidance modules that reach 98% sensitivity for deep vein thrombosis detection, reducing reliance on scarce sonographers. Such collaborations shorten learning curves and strengthen vendor lock-in.

High-intensity Focused Ultrasound suppliers cultivate alliances with gynecology clinics to showcase non-invasive fibroid therapy outcomes. Handheld innovators partner with medical schools to embed POCUS curricula, generating early-career brand loyalty. MDR compliance represents both a moat and a cost burden; firms with mature quality systems secure certificates sooner, capturing share while smaller rivals await notified-body slots. Pricing strategies increasingly bundle service, AI updates, and cloud archiving into multiyear subscriptions, aligning vendor revenue with customer usage.

White-space opportunities lie in rural connectivity solutions, adaptive training platforms, and specialized probes for oncology guidance. Vendors that prove real-world economic gains such as reduced patient transfers strengthen their positions in Spain ultrasound devices market.

Spain Ultrasound Devices Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-driven clinical pathway expansion creates near-term whitespace for vendors that connect ultrasound acquisition to standardized benefits and measurable outcomes. The Common Package of Benefits of the Spanish National Health System was amended by Order SND/356/2026 (20 April 2026) to include prenatal screening for preeclampsia, which incorporates ultrasound assessment of uterine artery pulsatility index; this supports demand for obstetric ultrasound workflows with reliable Doppler performance across public provision. Point-of-care expansion also has operational proof points in Spain, including the Andalusian health service training more than 1,000 primary-care clinicians in abdominal scanning, which supports broader deployment of portable and handheld systems with simplified training and guided workflows.

Spain is also formalizing how evidence translates into adoption, favoring suppliers that package devices with data, interoperability, and HTA-ready documentation. Real Decreto 415/2026 and RedETS activity (including its 2026 work plan prioritizing diagnostic imaging) elevate comparative effectiveness, workflow productivity, and cost-utility evidence in procurement and reimbursement-linked decisions. Royal Decree 90/2026 (effective 1 July 2026) further highlights financing mechanics for devices used outside hospitals, reinforcing opportunities for ultrasound solutions aligned with home care and tele-ultrasound models already demonstrated in island and rural settings. Within these shifts, ultrasound platforms with integrated AI guidance, secure connectivity, and service-inclusive commercial models align better with procurement realities across Spain's autonomous regions, where public spending discipline remains tight.

Recent Industry Developments

- June 2026: RedETS (Andalusian Health Technology Assessment Department & Basque Office for Health Technology Assessment) released new and emerging health technology fact sheets covering ultrasound-related technologies including therapeutic intravascular ultrasound for pulmonary hypertension. The release points to a formal evaluation pathway for advanced ultrasound therapies in Spain and could affect adoption timelines and tender decisions.

- March 2026: FUJIFILM Healthcare Europe introduced ARIETTA DeepInsight platforms (ARIETTA 850/750/650) and L52H high-frequency transducer at ECR 2026. Fujifilm strengthened its presence in Spain for high-end ultrasound and AI-assisted imaging, which may shift tender competition.

- February 2025: Canon Medical Systems Corporation unveiled Aplio beyond ultrasound system for high-throughput environments at ECR 2025. The system adds competitive pressure in Spain for scalable, efficient imaging platforms and factors into procurement decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of ultrasound imaging systems sold and installed in Spain across public and private care settings, counting revenues tied to the equipment itself within the defined period.

Scope exclusions: We exclude unrelated diagnostic modalities (such as CT, MRI, and X-ray) and we also exclude services, maintenance contracts, and broad hospital IT spending.

Segmentation Overview

- By Application

- Anesthesiology

- Cardiology

- Gynecology / Obstetrics

- Musculoskeletal

- Radiology

- Critical Care

- Urology

- Vascular

- Other Applications

- By Technology

- 2D Ultrasound Imaging

- 3D & 4D Ultrasound Imaging

- Doppler Imaging

- High-Intensity Focused Ultrasound

- Other Technologies

- By Portability

- Stationary Systems

- Portable Cart-based Systems

- Hand-held / Pocket Devices

- By End User

- Public Hospitals

- Private Hospitals & Clinics

- Diagnostic Imaging Centres

- Home Healthcare Settings

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by setting the boundaries and building a fact base for demand and supply signals in Spain. We review public sources such as Spain's Ministry of Health publications, the Spanish National Statistics Institute (INE), Eurostat health and trade tables, OECD health indicators, and guidance and publications from bodies like WHO to understand imaging access, demographic pressure, and care delivery trends.

To translate these signals into market inputs, we also use hospital procurement notes available on public portals, customs and trade classifications where relevant, and a mix of company annual reports, investor presentations, and credible medical press coverage for product launches and replacement cycles. When needed, paid subscriptions are used for company financials and intelligence, patent search support, and tender tracking to fill gaps that are not consistently visible in free sources. These examples are illustrative, and many other public and secondary sources were also referenced to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk research cannot fully confirm, especially around purchasing timing, mix shifts toward portable systems, and pricing movement by system class. We interview and survey a spread of stakeholders, including imaging department users, hospital procurement teams, distributors, and service partners. We then re-check assumptions across Spain's main care settings so the final model reflects recurring buying patterns rather than one-off quotes.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 46% | Functional/Unit leaders: 37% | |

| Smaller Players: 21% | Managers: 49% |

Market-Sizing & Forecasting

Market sizing is built using one clear top-down path first. Spain-level demand is reconstructed from imaging activity signals, facility coverage, and replacement patterns, then translated into device revenues using realistic pricing bands. Once totals are formed, we corroborate them using selective bottom-up approximations, such as sampled ASP times unit logic by system category, distributor channel checks, and supplier-side sanity checks to correct any obvious over or under counts.

A few inputs that tend to matter in this market include public and private hospital equipment renewal cycles, growth in outpatient imaging and point-of-care use, population aging and chronic disease load that pushes imaging volume, procurement timing linked to budgets and tenders, and average selling price progression as features and portability improve. Forecasting is run using scenario analysis, where the core case is shaped by expert views on tender cadence, replacement timing, and price mix, and then stress-tested with slower and faster adoption paths. Where bottom-up signals are incomplete, gaps are handled with conservative ranges that are anchored to known installed-base behavior and validated through follow-up calls.

Data Validation & Update Cycle

Validation is done through stepwise checks so the model does not rely on a single series. Outputs are compared against independent signals such as import patterns where applicable, public tender wins, installed base replacement expectations, and reported spending priorities. Large variances are reviewed before sign-off.

If an input shifts materially, for example a major procurement wave or a sudden pricing reset, analysts re-contact sources and re-run sensitivity checks so the totals remain consistent with the latest market reality. The report is refreshed annually, with material events incorporated through interim updates, followed by a final pre-delivery review pass so clients receive the most current view available at release time.

Mordor Intelligence's Spain Ultrasound Devices Market Size Compared With Other Published Estimates

Different published market values can vary because the underlying counting logic is not always the same, even when the title looks similar. The most common reasons are differences in what is included as device revenue, how portable and cart-based systems are treated, and whether the estimate leans on shipment signals, tenders, or installed base replacement math.

By tracking tender timing, checking installed base replacement expectations, and refreshing pricing bands with primary inputs, Mordor Intelligence keeps the Spain ultrasound devices total focused on equipment revenues earned in-country, instead of blending in service streams or broader imaging spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 221.98 M (2025) | |

| Trade Journal A | USD 80.00 M (2023) | This value appears to focus on ultrasound systems in a narrower definition, and it reads like it may reflect a subset of hospital purchasing and player-reported shares rather than a full market total across care settings. |

| Regional Consultancy B | USD 487.30 M (2026) | This estimate likely expands the scope beyond core ultrasound device revenues, or it applies more aggressive ASP and volume growth assumptions, which can inflate the 2026 total when replacement cycles and tender pacing are not constrained. |

Taken together, the spread is mainly explained by scope boundaries and the strength of the pricing and volume assumptions used for forward years. Our approach stays traceable to a practical demand pool, with totals that can be rebuilt from replacement logic, procurement cadence, and realistic price mix, and then re-validated when new signals emerge.

Key Questions Answered in the Report

What is the current value of the Spain ultrasound devices market?

The market is valued at USD 228.73 million in 2026 and is projected to reach USD 265.67 million by 2031.

Which application area contributes the largest revenue?

Radiology leads with 37.42% revenue share in 2025.

Which segment is growing fastest by portability?

Hand-held/Pocket devices are advancing at a 7.18% CAGR through 2031.

How does EU MDR affect ultrasound device suppliers in Spain?

Extended certification timelines and added clinical evidence requirements delay product launches and raise compliance costs.

Why are home healthcare providers investing in ultrasound?

Telemedicine frameworks and AI guidance let caregivers perform scans at patients’ homes, cutting travel time and easing hospital capacity constraints.

What technological trend is disrupting traditional therapy?

High-intensity Focused Ultrasound offers non-invasive treatment for conditions like uterine fibroids, spurring a 5.36% CAGR within the technology segment.

Page last updated on: