Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

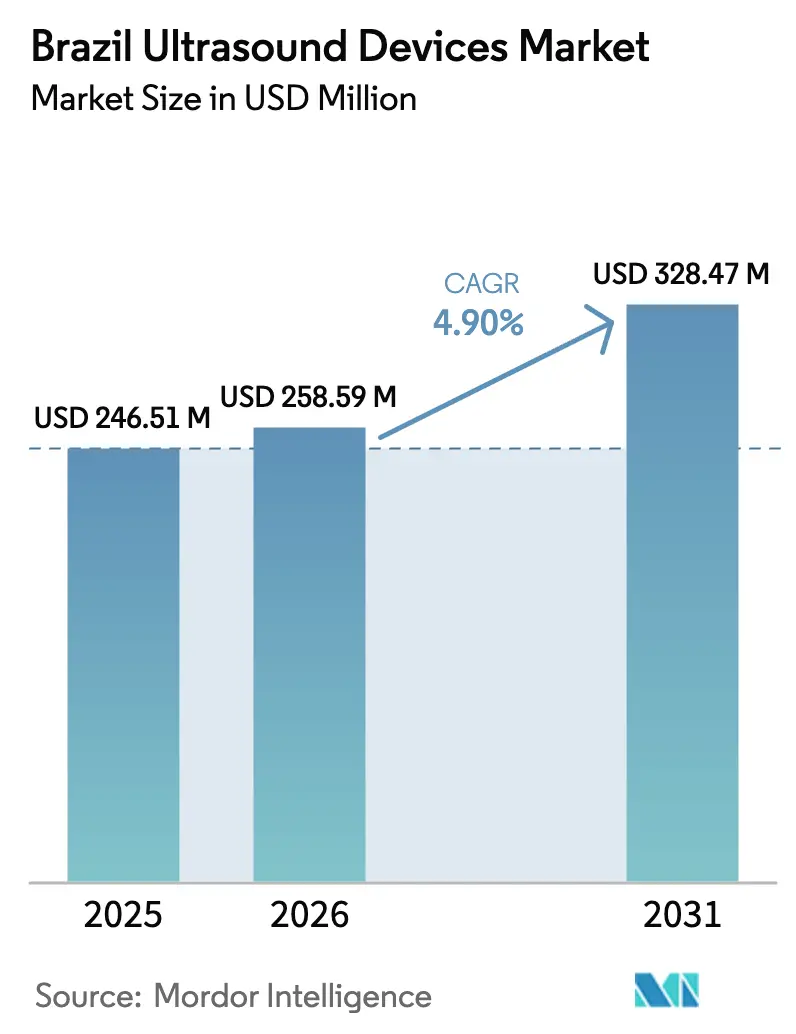

| Base Year Market Size (2025) | USD 246.51 Million |

| Market Size (2026) | USD 258.59 Million |

| Market Size (2031) | USD 328.47 Million |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Ultrasound Devices Market Analysis by Mordor Intelligence

The Brazil Ultrasound Devices Market size is expected to grow from USD 246.51 million in 2025 to USD 258.59 million in 2026 and is forecast to reach USD 328.47 million by 2031 at 4.90% CAGR over 2026-2031.

Growth rests on telehealth programs that move imaging services into remote municipalities, while AI integration raises productivity across crowded urban hospitals. Premium cart-based systems still dominate capital budgets, yet handheld scanners post double-digit gains as clinicians seek bedside diagnostics that do not require certified sonographers. Regional consumption is heavily skewed toward the Southeast where 54% of current installations are located, but government incentives are accelerating deployments in the North and Northeast. Price-sensitive public tenders are also widening the pathway for Chinese suppliers that pair adequate image quality with aggressive financing packages.

Key Report Takeaways

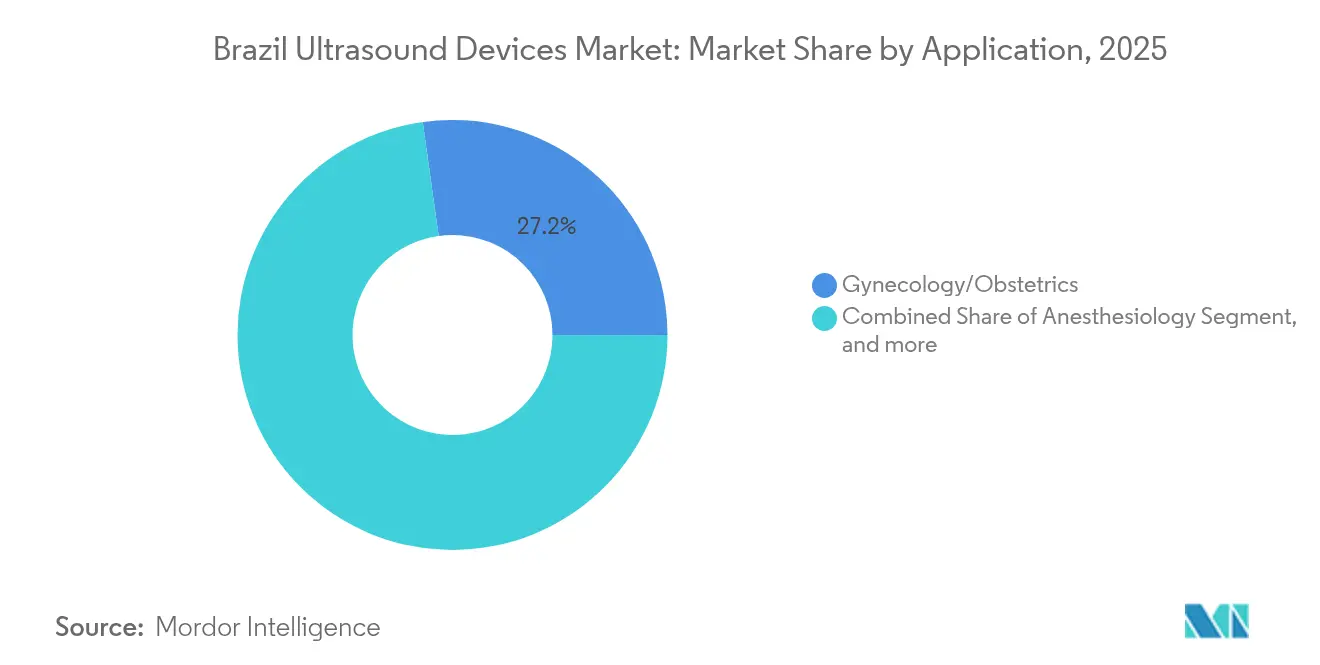

- By application, gynecology/obstetrics led with 27.21% revenue share in 2025, while anesthesiology is set to grow at an 7.78% CAGR from 2026 to 2031.

- By technology, 3D & 4D imaging captured 45.60% of the Brazil ultrasound devices market size in 2025; AI-enabled/automated ultrasound systems are poised for a 8.79% CAGR over the same horizon.

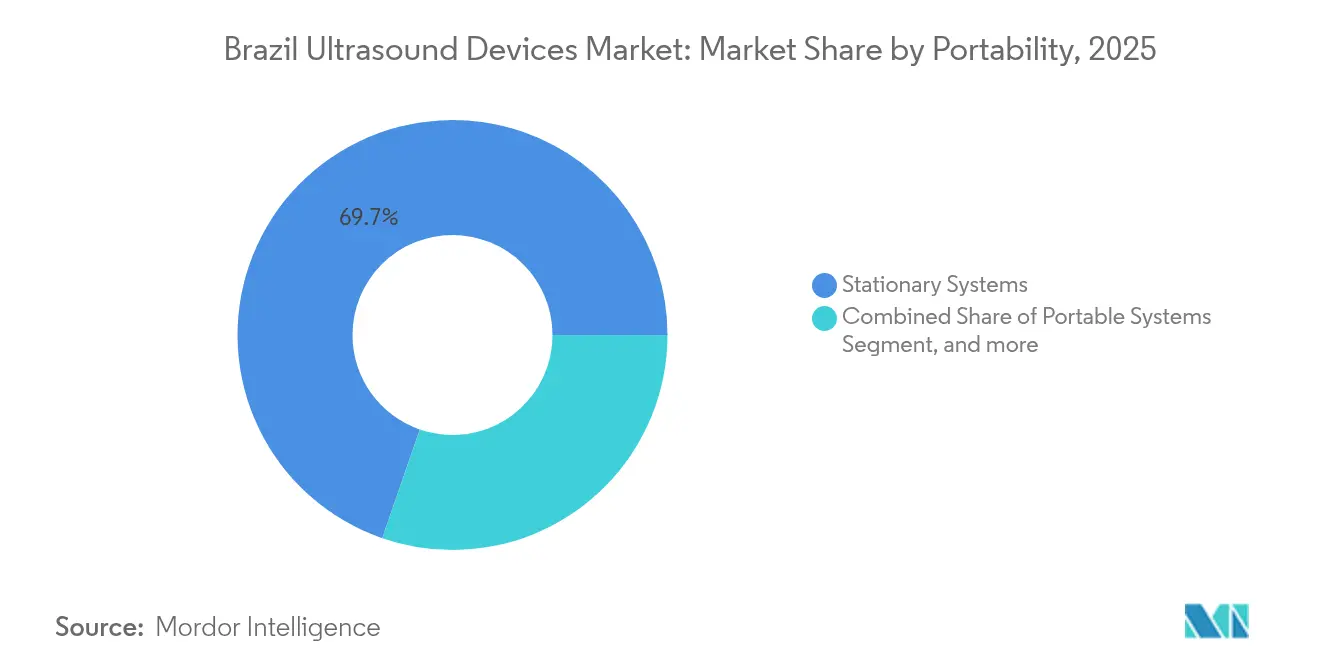

- By portability, stationary systems accounted for 69.70% of the Brazil ultrasound devices market size in 2025, whereas handheld/wireless scanners are climbing at an 10.72% CAGR toward 2031.

- By end user, hospitals represented 42.74% of the Brazil ultrasound devices market share in 2025, and diagnostic imaging centers are forecast to rise at a 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of tele-ultrasound coverage through Brazil’s SUS “Telessaúde Brasil” network | +1.2% | North & Northeast | Medium term (2-4 years) |

| Rise of private diagnostic chains and imaging hubs | +0.9% | Southeast & South | Long term (≥4 years) |

| Mandatory cardiac screening for professional athletes | +0.6% | Nationwide | Short term (≤2 years) |

| High teenage pregnancy rates driving OB-GYN ultrasound demand | +0.5% | North & Northeast | Medium term (2-4 years) |

| Growing adoption of AI-enabled portable ultrasound systems | +1.0% | Nationwide | Short term (≤2 years) |

| Public–private collaborations expanding screening programs | +0.6% | Northeast & North | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Tele-Ultrasound Coverage through SUS “Telessaúde Brasil” Network

Local health posts now transmit images to university hospitals where certified radiologists validate results. In 2024, 60.3% of teledermatology cases were resolved in primary care without referrals, demonstrating the same model that ultrasound sessions can emulate.[1]João Castelo-Branco, “Performance of Telehealth Centers in Pará,” teleconsulta.fiocruz.br Primary-care participation in the network already reaches 84.4%, and twelve dedicated tele-health hubs operate in the Amazon basin. By pairing low-bandwidth image compression with store-and-forward protocols, the Brazil ultrasound devices market gains access to municipalities previously unreachable by conventional service contracts. This initiative also mitigates the shortage of certified sonographers by letting nurses capture scans that specialists later interpret remotely. Medium-term impact is expected to lift utilization volumes and create recurring consumables demand for probe covers and gel in remote clinics.

Rise of Private Diagnostic Chains and Imaging Hubs

Urban conglomerates such as DASA are centralizing high-throughput equipment in regional hubs that process referrals from satellite collection points. Hub-and-spoke logistics raise utilization above 80%, enabling premium 3D & 4D consoles to recoup capital outlays faster. A 2024 study on handheld ultrasound accuracy in confirming intrauterine device placement showed 92.9% sensitivity, validating small-format imaging in busy obstetrics clinics. Chains now add handheld probes to obstetrics suites so technicians can triage routine checks, freeing premium rooms for complex fetal assessments. Over the long term, this operational model anchors a steady replacement cycle across the Brazil ultrasound devices market.

Mandatory Cardiac Screening for Professional Athletes

FIFA recommendations issued for the 2025 season place echocardiography within athlete evaluations once risk factors surface. Brazilian clubs and federations are procuring portable units that fit locker room constraints, fuelling a niche yet influential segment of the Brazil ultrasound devices market. A school-based study found handheld scanners flagged 7.9% of children with possible rheumatic abnormalities, although confirmatory machines verified only 3.2%, underscoring the value of rapid triage.[2]Victor Baggish, “FIFA Cardiac Screening Consensus,” escardio.org Demand clusters around training centres in major cities, giving manufacturers an entry point to promote AI modules that automate left-ventricular measurements.

High Teenage Pregnancy Rates Driving OB-GYN Ultrasound Demand

National fertility continues to decline, yet adolescent pregnancies persist above regional averages in the North and Northeast. Prenatal protocols require at least three scans per gestation, anchoring steady throughput for obstetric probes. Harvard T.H. Chan School researchers flagged persistent inequalities in diagnostic access, prompting federal grants that subsidize ultrasound procurement in maternal-health clinics.[3]Rifat Atun, “Cancer Care and Health System Inequities in Brazil,” hsph.harvard.edu Vendors now tailor maintenance packages that guarantee uptime in remote towns, further expanding the addressable Brazil ultrasound devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Class III reclassification of AI ultrasound systems | -1.1% | Nationwide | Short term (≤2 years) |

| Chronic shortage of certified sonographers | -0.9% | Nationwide | Long term (≥4 years) |

| Uneven distribution of imaging resources across regions | -0.7% | North & Northeast | Medium term (2-4 years) |

| Import dependency and currency fluctuation risks | -0.5% | Nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Class III Reclassification of AI Ultrasound Systems

ANVISA’s Resolution RDC 751/2022 raised AI-enabled devices from Class II to Class III, mandating full registration dossiers and factory inspections. Filing times lengthened, and working capital requirements climbed as importers stock units while awaiting approval. Smaller innovators risk delaying launches, narrowing competitive choices for public tenders across the Brazil ultrasound devices market. The burden is felt most in the short term until firms align quality-management files with Brazilian expectations.

Chronic Shortage of Certified Sonographers

Brazil tallies 2.77 physicians per 1,000 inhabitants, yet distribution skews toward general practice. Specialty imaging remains concentrated in capitals, leaving district hospitals without accredited sonographers. Procedure backlogs rise, lowering throughput even where equipment sits idle. Vendors respond with training modules and AI guidance, but workforce expansion needs policy intervention over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Maternal Health Drives Market Leadership

Gynecology and obstetrics captured 27.21% of the Brazil ultrasound devices market size in 2025, underpinned by mandatory prenatal screening protocols and persistently high adolescent pregnancy rates in the North and Northeast. Hospitals allocate premium 3D cups and curved probes to maternity wards, ensuring fetal anomaly detection remains on par with international standards. Screening frequency supports steady consumables demand, reinforcing vendor service footprints in secondary cities.

Anesthesiology follows as the fastest-growing specialty at an 7.78% CAGR over 2026-2031. The shift toward ultrasound-guided nerve blocks lowers peri-operative opioid use, aligning with national patient-safety goals. Portable linear probes give anesthetists a real-time view of target nerves, enabling day-surgery centers to shorten turnaround times. Growth also benefits from residency-program curricula that now mandate ultrasound modules for regional blocks, widening practitioner familiarity across the Brazil ultrasound devices market.

By Technology: AI Integration Reshapes Capabilities

3D & 4D imaging commanded 45.60% of the Brazil ultrasound devices market share in 2025, driven by high-definition fetal screening and complex musculoskeletal evaluations. Private diagnostic chains market premium appointments to affluent urban consumers, leveraging volumetric renderings to differentiate services. Workstations include advanced workstation software that reconstructs heart valves for pre-surgical planning.

AI-enabled platforms are on course for a 8.79% CAGR, even after Class III reclassification raised compliance hurdles. Automating routine measurements reduces scan time for small clinics short on manpower, widening use cases in primary care. Cloud-delivered updates add cardiology and abdominal modules without hardware swaps, sustaining a longer revenue stream per installed base within the Brazil ultrasound devices market.

By Portability: Handheld Devices Transform Access Paradigms

Stationary carts retained 69.70% of the Brazil ultrasound devices market size in 2025 because tertiary hospitals still require full Doppler packages and transesophageal probes. Multi-disciplinary departments exploit integrated reporting software that links to electronic health records, justifying continued investment in high-end consoles.

Handheld scanners are rising at an 10.72% CAGR as community clinics and ambulance teams embrace their phone-like interfaces. In a 2024 field study, school nurses used handheld echocardiography to screen 3,000 children in less than four weeks, demonstrating scalability. Battery improvements now permit six hours of continuous operation, while waterproof housings suit tropical field work. This versatility strengthens the rural footprint and draws new public funding to the Brazil ultrasound devices market.

By End User: Hospitals Lead While Imaging Centers Grow Fastest

Hospitals, both public and private, accounted for 42.74% of the Brazil ultrasound devices market share in 2025. Multidisciplinary workflows rely on on-site radiologists who integrate imaging into surgical and emergency pathways. Replacement cycles are tied to accreditation audits that require image-quality benchmarks, securing recurring orders for premium probes.

Diagnostic imaging centers and radiology clinics are forecast to climb at a 7.23% CAGR as corporate networks open satellite sites near commuter rail stations. Chain operators maximize scanner uptime through extended evening hours, boosting throughput and unit economics. Public–private agreements grant these centers overflow patients from SUS, widening payer diversification and stabilizing cash flow inside the Brazil ultrasound devices market.

Geography Analysis

The Southeast holds economic and demographic primacy, translating significant share of installed systems in 2024. São Paulo and Rio de Janeiro host the headquarters of major private chains and academic hospitals that procure cutting-edge 3D & 4D consoles to maintain referral dominance. Despite volume strength, public–private disparities persist, prompting philanthropic programs to outfit peri-urban maternity wards with midrange carts.

The Northeast is the fastest-growing territory. Federal incentives subsidize equipment loans for municipalities with high maternal-mortality ratios. Regional health secretariats integrate mobile vans into prenatal outreach, connecting to obstetrics tele-consultants in Salvador. This structure raises preventive-care coverage and stimulates replacement demand for battery and probe components in the Brazil ultrasound devices market.

The North and Central-West together still represent a smaller slice, yet telemedicine corridors are shortening logistical hurdles across the Amazon basin. Twelve broadband hubs commissioned by the Federal University of Pará forward images to Belém specialists, shaving travel costs for riverine communities. Vendors tailor ruggedized kits that survive humidity and transport shocks, unlocking an untapped cohort of first-time buyers.

The South ranks second in revenue owing to higher per-capita income and insurance penetration. State legislatures pioneer unified referral portals that steer patients to the nearest available scanner, lifting utilization rates. Academic centres in Curitiba trial AI triage algorithms that flag abnormal scans for expedited review, a blueprint likely to spread nationwide and enlarge the Brazil ultrasound devices market.

Competitive Landscape

Global multinationals dominate the premium segment, yet Chinese manufacturers are steadily gaining share by matching local technical-assistance requirements at lower price points. Global suppliers retain a technological edge, yet purchasing committees increasingly weigh life-cycle cost against headline specifications. GE Healthcare, Philips, and Siemens Healthineers collectively dominate tenders for high-end consoles, supported by local field-service networks. In 2024 they joined AdvaMed’s new Medical Imaging Division, aligning advocacy on cybersecurity patches and third-party servicing guarantees. This collaboration streamlines engagement with ANVISA during post-market surveillance inquiries.

Mindray spearheads the value segment, shipping cart models that bundle Doppler and touch-screen interfaces at a 20% discount to European peers. Local distributor networks ease after-sales logistics, helping the brand penetrate SUS procurement lists. Portable specialists Butterfly Network and Clarius Mobile Health target emergency physicians with app-based interfaces, and partnerships with telecom firms secure cloud storage packages that appeal to tele-health workflows in the Brazil ultrasound devices market.

Capital concentration remains moderate; leading brands account for nearly 55% of unit revenue, leaving space for domestic assemblers that import sub-systems and add probes locally. Currency volatility forces all vendors to hedge component costs, occasionally delaying price-list updates and lengthening negotiation cycles with public buyers.

Brazil Ultrasound Devices Industry Leaders

GE HealthCare

Siemens Healthineers AG

Koninklijke Philips N.V.

Canon Medical Systems Corporation

Fujifilm Sonosite Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: GE Healthcare outlined plans to launch more than 120 AI-enabled diagnostic devices globally, a pipeline that includes Brazil-specific ultrasound configurations optimized for prenatal screening.

- July 2024: Philips Foundation partnered with SAS Brasil to open a digital-health innovation lab focused on ultrasound training for clinicians in remote areas, amplifying skill-transfer capacity without relocating trainees.

Brazil Ultrasound Devices Market Report Scope

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They are being utilized for the assessment of various conditions in the kidney, liver, and other abdominal conditions. They are also majorly used in chronic diseases, which include health conditions such as heart disease, asthma, cancer, and diabetes. Therefore, these devices are being utilized as both diagnostic imaging and therapeutic modality and have a wide range of applications in the medical field.

The Brazil ultrasound devices market is segmented by application (anesthesiology, cardiology, gynecology / obstetrics, radiology / general imaging, musculoskeletal, vascular, critical care & emergency, urology, and gastroenterology), by technology (2D ultrasound imaging, 3D & 4D ultrasound imaging, Doppler ultrasound (color & spectral), high-intensity focused ultrasound (HIFU), contrast-enhanced ultrasound, AI-enabled / automated ultrasound, and Point-of-Care ultrasound (PoCUS)), by portability (stationary systems, portable systems, and handheld / wireless scanners), by end user (public hospitals (SUS), private hospitals, diagnostic imaging centers & radiology clinics, primary & maternity clinics, and ambulatory surgery centers), and by Region (Southeast, South, Northeast, North, and Central-West). The report offers the value (in USD million) for the above segments. The report offers the value (in USD million) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology/Obstetrics |

| Radiology/General Imaging |

| Musculoskeletal |

| Vascular |

| Critical Care & Emergency |

| Urology |

| Gastroenterology |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Ultrasound (Color & Spectral) |

| High-Intensity Focused Ultrasound (HIFU) |

| Contrast-Enhanced Ultrasound |

| AI-Enabled/Automated Ultrasound |

| Point-of-Care Ultrasound (PoCUS) |

By Portability

| Stationary Systems |

| Portable Systems |

| Handheld/Wireless Scanners |

By End-User

| Public Hospitals (SUS) |

| Private Hospitals |

| Diagnostic Imaging Centers & Radiology Clinics |

| Primary & Maternity Clinics |

| Ambulatory Surgery Centers |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology/Obstetrics | |

| Radiology/General Imaging | |

| Musculoskeletal | |

| Vascular | |

| Critical Care & Emergency | |

| Urology | |

| Gastroenterology | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Ultrasound (Color & Spectral) | |

| High-Intensity Focused Ultrasound (HIFU) | |

| Contrast-Enhanced Ultrasound | |

| AI-Enabled/Automated Ultrasound | |

| Point-of-Care Ultrasound (PoCUS) | |

| By Portability | Stationary Systems |

| Portable Systems | |

| Handheld/Wireless Scanners | |

| By End-User | Public Hospitals (SUS) |

| Private Hospitals | |

| Diagnostic Imaging Centers & Radiology Clinics | |

| Primary & Maternity Clinics | |

| Ambulatory Surgery Centers |

Key Questions Answered in the Report

What is the current value of the Brazil ultrasound devices market?

The Brazil ultrasound devices market size stands at USD 258.59 million in 2026 and is projected to reach USD 328.47 million by 2031.

Which application segment generates the highest revenue?

Gynecology and obstetrics lead with 27.21% of 2025 revenue, supported by mandatory prenatal screening protocols.

Why are handheld ultrasound scanners gaining popularity?

Handheld units grow at an 10.72% CAGR because they extend imaging services to rural clinics and emergency departments lacking certified sonographers.

How does ANVISA’s Class III reclassification affect manufacturers?

The new rule demands full registration dossiers and factory inspections, lengthening approval timelines and increasing compliance costs for AI-enabled platforms.

What technologies are seeing the quickest uptake?

AI-enabled ultrasound systems record a 8.79% CAGR as automated measurements shorten exam times and alleviate workforce shortages.

Page last updated on: