Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

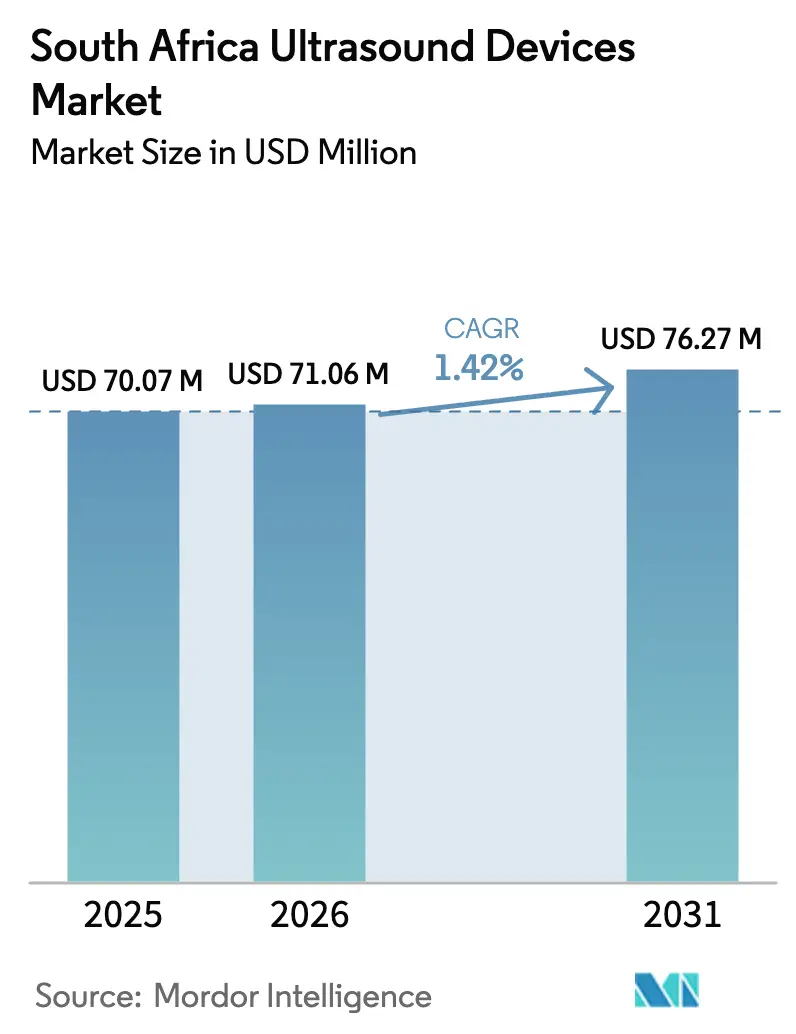

| Base Year Market Size (2025) | USD 70.07 Million |

| Market Size (2026) | USD 71.06 Million |

| Market Size (2031) | USD 76.27 Million |

| Growth Rate (2026 - 2031) | 1.42% CAGR |

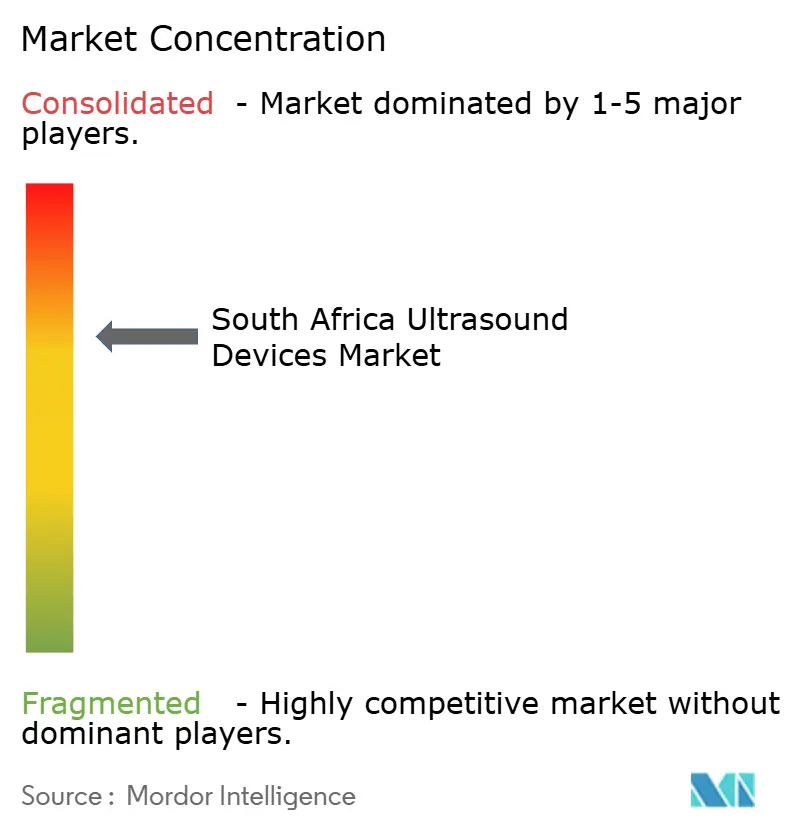

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Ultrasound Devices Market Analysis by Mordor Intelligence

South Africa Ultrasound Devices Market size in 2026 is estimated at USD 71.06 million, growing from 2025 value of USD 70.07 million with 2031 projections showing USD 76.27 million, growing at 1.42% CAGR over 2026-2031.

This measured trajectory reflects constrained hospital budgets, volatile currency movements, and the gradual rollout of the National Health Insurance (NHI) program, yet the underlying demand for real-time imaging in maternal care, cardiology, and perioperative monitoring continues to expand. Portable and handheld scanners post the fastest volume gains as rural outreach programs embrace point-of-care models, while advanced 3D and 4D platforms maintain revenue leadership due to their higher selling price and superior diagnostic performance. Strategic investments by private hospital groups, combined with foreign grant funding for maternal health, sustain equipment refresh cycles even as public-sector tenders slow. Regulatory reforms under SAHPRA preserve clinical safety standards and favor brands with proven after-sales support, subtly raising the competitive bar for new entrants.

Key Report Takeaways

- By application, obstetrics and gynecology led with 21.41% share of the South Africa ultrasound devices market in 2025, while anesthesiology recorded the fastest CAGR at 3.71% through 2031.

- By technology, 3D and 4D imaging held 41.89% of the South Africa ultrasound devices market share in 2025; high-intensity focused ultrasound is projected to expand at a 3.44% CAGR to 2031.

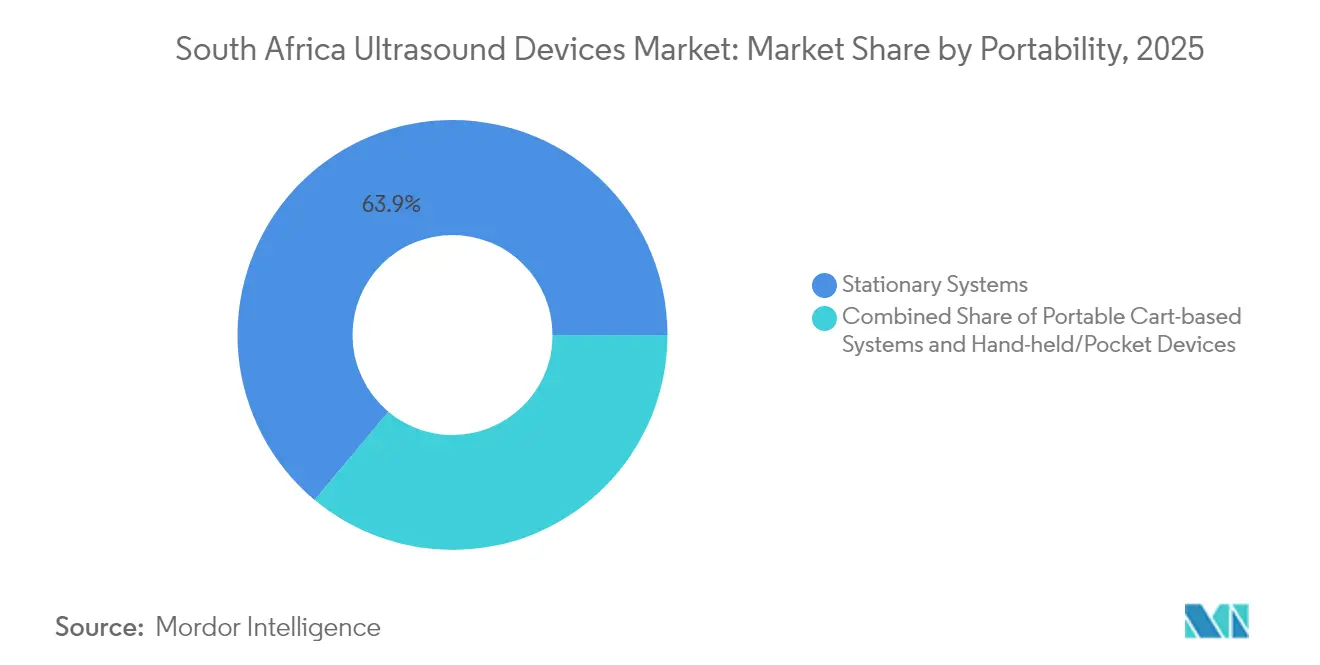

- By portability, stationary systems accounted for 63.92% of the South Africa ultrasound devices market size in 2025 and handheld devices are advancing at a 4.56% CAGR through 2031.

- By end user, hospitals captured 50.62% revenue share in 2025, whereas diagnostic imaging centers are set to post the quickest growth at 4.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Non-Communicable Diseases | +0.4% | National, concentrated in urban centers | Medium term (2-4 years) |

| National Health Insurance (NHI) Rollout | +0.3% | National, phased implementation | Long term (≥ 4 years) |

| Point-of-Care & Handheld Ultrasound Adoption | +0.5% | National, rural emphasis | Short term (≤ 2 years) |

| Private Sector Investment Surge | +0.2% | Western Cape, Gauteng primary | Medium term (2-4 years) |

| Tele-Ultrasound & AI-Driven Remote Mentoring | +0.3% | National, rural connectivity focus | Medium term (2-4 years) |

| Adoption of 3D/4D Imaging and Wavefront-Guided Systems | +0.2% | Urban centers, private facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Non-Communicable Diseases

Non-communicable diseases cause 57% of deaths in South Africa, creating sustained imaging demand across cardiology and vascular care.[1]International Trade Administration, “South Africa – Medical Equipment,” Trade.gov Cardiac ultrasound enables early detection of hypertensive heart disease while Doppler studies support diabetes management protocols. The NHI preventive-care focus pushes public clinics to screen high-risk adults, encouraging bulk procurement of entry-level scanners. Private primary-care networks deploy mobile units for workplace screenings, broadening the South Africa ultrasound devices market. AI-supported cardiac packages reduce operator dependency, allowing nurses to capture diagnostic views that specialists later review remotely.

National Health Insurance Rollout

The NHI Act centralizes equipment purchasing under a single fund, promising uniform technology standards across provinces. A three-year budget of ZAR 1.4 billion (USD 74 million) concentrates on primary-care clinics where compact ultrasound aligns with point-of-care workflows. Yet the 15-year implementation horizon introduces spending uncertainty, prompting hospitals to defer high-end system upgrades until reimbursement rules clarify. Portable platforms with integrated tele-consult features position well for upcoming tenders that prioritize rural outreach.

Point-of-Care & Handheld Ultrasound Adoption

Bedside imaging shortens diagnosis-to-treatment time in trauma, obstetrics, and perioperative care. Devices such as Butterfly iQ+ deliver whole-body scanning with a single probe, supporting the Siyakubona program that equips 1,000 midwives across five provinces.[2]Bill & Melinda Gates Foundation, “Siyakubona Maternal Health Project,” Butterflynetwork.com Emergency responders report 79.5% correlation between pre-hospital and in-hospital findings, validating the clinical utility of handhelds. Battery life of six hours, smartphone connectivity, and pay-per-scan cloud storage lower entry barriers for small practices and contribute materially to the South Africa ultrasound devices market growth.

Private Sector Investment Surge

Life Healthcare earmarked ZAR 2.1 billion (USD 114 million) for domestic projects in 2024, including AI-enabled imaging suites. Netcare’s ZAR 6.6 billion (USD 370 million) annual supplier spend, with 52% to black-owned firms, anchors vendor relationships and supports transformation targets. Western Cape’s USD 400 million med-tech hub attracts start-ups focusing on advanced visualization, raising competitive intensity inside the South Africa ultrasound devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Personnel | -0.3% | National, rural areas most affected | Long term (≥ 4 years) |

| High Import Tariffs & Currency Volatility | -0.2% | National, import-dependent market | Short term (≤ 2 years) |

| SAHPRA Registration Delays | -0.2% | National, regulatory bottlenecks | Medium term (2-4 years) |

| Cybersecurity Risks & Legacy Systems | -0.1% | National, healthcare facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Personnel

Vacancies exceed 27,000 critical posts and the radiologist attrition rate tops 13% annually, leaving scanners idle in many district hospitals.[3]Democratic Alliance, “Health Human Resource Crisis,” Da.org.za The first accredited sonography degree began only in 2024, so near-term staffing relief is limited. AI workflow tools that label anatomy and suggest measurements do help, yet they still require minimum operator competence. Delays in processing foreign critical-skills visas further tighten the talent pool and restrain the South Africa ultrasound devices market.

High Import Tariffs & Currency Volatility

More than 76% of ultrasound equipment is imported, exposing buyers to rand swings that reached ZAR 18.43 per USD (USD 1.0) in May 2025. Import duties and logistics surcharges raise landed costs by up to 12%. Large corporates hedge currency risk, whereas small clinics shift to multiyear leasing that ultimately inflates lifetime ownership costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Maternal Health Drives Core Demand

Obstetrics and gynecology generated 21.41% of the South Africa ultrasound devices market share in 2025, buoyed by national targets to cut maternal mortality. The Siyakubona roll-out shows that handheld scanners can shorten first-trimester booking delays in rural clinics, underpinning recurring probe purchases and consumables. Cardiology remains a steady revenue pillar as non-communicable diseases rise, while anesthesiology posts a 3.71% CAGR by embedding real-time nerve-block guidance into perioperative protocols.

Point-of-care lung and abdominal scans gained visibility during COVID-19 and remain in routine use for sepsis and trauma triage. Community nursing programs add basic obstetric scanning to extend reach into low-resource districts. Continuous expansion of these mid-level services broadens the South Africa ultrasound devices market beyond tertiary hospitals.

By Technology: Advanced Imaging Leads Innovation

3D and 4D platforms captured 41.89% of the South Africa ultrasound devices market in 2025, reflecting clinician preference for volumetric fetal and cardiac data. High-intensity focused ultrasound grows at a 3.44% CAGR as non-invasive fibroid therapy pilots receive favorable patient feedback. Doppler packages stay relevant for vascular mapping, while 2D remains the affordable baseline across public facilities.

AI echo-workflow modules trim exam time by automating chamber segmentation, aiding overworked staff. GE Healthcare’s USD 51 million AI acquisition adds real-time guidance that appeals to training hospitals. Integration with cloud PACS makes advanced packages more appealing, despite higher capital outlay.

By Portability: Mobility Transforms Access

Stationary rooms still dominate with 63.92% of the South Africa ultrasound devices market size in 2025, especially in large hospitals that require full cardiac, vascular, and interventional capabilities. Yet handheld units clock the fastest 4.56% CAGR as grant-funded community programs equip ambulances and outreach teams. Cart-based systems remain popular for emergency departments wanting mobility without sacrificing power.

Handheld buyers value dual-probe architecture, six-hour battery life, and smartphone connectivity. SAHPRA’s classification ensures safety, yet importers must show electromagnetic compliance, lengthening time-to-market for the latest models.

By End User: Hospitals Anchor Market Demand

Hospitals absorbed 50.62% of 2025 revenue thanks to broad procedure mixes and stronger maintenance budgets. Diagnostic imaging centers, advancing at 4.27% CAGR, tap rising demand for same-day appointments and short report turnaround. Primary-care clinics use basic handheld sets under NHI outreach, while private practices prefer pocket devices that fit cash-flow constraints.

Emergency medical services integrate portable scans for on-scene triage, driving annual fleet demand from ambulance providers. Training institutes purchase simulation-ready systems that combine phantom modules with AI coaching, contributing incremental volume to the South Africa ultrasound devices market.

Geography Analysis

Western Cape enjoys the highest equipment density given a decade-long USD 400 million med-tech investment that nurtures device start-ups and specialist clusters. Provincial health authorities still face bed shortages and aging scanners at Groote Schuur and Tygerberg, prompting fresh tenders favoring portable units that can fill service gaps.

Gauteng hosts most private hospitals and posts the strongest premium-system sales, yet public facilities struggle with limited radiotherapy and ultrasound capacity for a populous catchment. Private insurance penetration fuels demand for 3D cardiac and obstetric studies, sustaining value growth inside the South Africa ultrasound devices market.

KwaZulu-Natal leverages a digital patient registry across 3,215 public clinics, creating an IT backbone for networked ultrasound storage. Eastern Cape serves as the pilot site for mid-level practitioner training under Siyakubona, illustrating how skill development can lift utilization in low-income areas. Rural provinces still lag in specialist availability, yet expanded fiber coverage and tele-ultrasound mentoring programs offer a path to closing the diagnostic gap.

Competitive Landscape

Global brands dominate procurement due to proven quality records and compliance infrastructure. GE Healthcare leverages its Vscan Air line and recent AI acquisitions to address point-of-care and workflow automation segments, keeping its global share above 30%. Siemens Healthineers pushes premium 4D obstetric and cardiology suites while integrating nuclear-diagnostics capabilities from its USD 223 million takeover of a Novartis unit, creating a broader imaging portfolio.

Philips emphasizes value-tier cart systems with built-in cardiac strain and tissue-specific presets that appeal to mid-range hospitals. Canon Medical gains traction by bundling extended warranties and zero-interest financing, helping it penetrate cost-sensitive public tenders. Local distributors such as Grobir Medical and AiM Medical negotiate exclusive import rights, yet their bargaining power remains limited given manufacturer-direct relationships with large hospital chains.

Barriers to entry stem from SAHPRA documentation, cybersecurity requirements, and a service-network mandate that compels all vendors to maintain local technical teams. Emerging niche players focus on specialized software, for example, AI auto-scoring of lung images for tuberculosis screening, aiming to partner with hardware leaders rather than compete head-on.

South Africa Ultrasound Devices Industry Leaders

Siemens Healthineers AG

GE Healthcare

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare announced a strategic collaboration with NVIDIA to develop autonomous X-ray and ultrasound systems, leveraging AI-enabled software to enhance medical imaging capabilities and reduce technician workload. The partnership utilizes NVIDIA's Isaac for Healthcare platform for training and testing autonomous devices in virtual environments, positioning both companies at the forefront of next-generation diagnostic imaging technology

- May 2024: The South African government signed the National Health Insurance Act into law, fundamentally restructuring healthcare procurement and delivery systems. The legislation establishes centralized purchasing mechanisms that will significantly impact medical device acquisition patterns, including ultrasound equipment procurement across public healthcare facilities.

South Africa Ultrasound Devices Market Report Scope

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. These devices are being utilized as both diagnostic imaging and therapeutic modality and have a wide range of applications in the medical field. South Africa, Ultrasound Devices Market is Segmented by Application (Cardiology, Gynecology/Obstetrics, Radiology, and Other Applications), Technology (2D Ultrasound Imaging, 3D and 4D Ultrasound Imaging, and Other Technologies), Type (Stationary Ultrasound and Portable Ultrasound). The report offers the value (in USD million) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Other End Users |

Key Questions Answered in the Report

How large is the South Africa ultrasound devices market in 2026?

The market is valued at USD 71.06 million in 2026 and is on track to reach USD 76.27 million by 2031.

What CAGR is expected for ultrasound equipment sales in South Africa?

Sales are projected to grow at a 1.42% CAGR between 2026 and 2031.

Which application holds the largest share of ultrasound spending?

Obstetrics and gynecology leads with 21.41% of 2025 revenue due to national maternal health targets.

Why are handheld scanners gaining popularity?

Handheld devices support point-of-care workflows in rural areas, reduce capital outlay, and integrate tele-consult features that suit NHI outreach goals.

Which province offers the greatest growth opportunity for vendors?

The Western Cape combines strong private investment with public-sector modernization plans, making it the primary growth engine for new installations.

Page last updated on: