Turkey Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

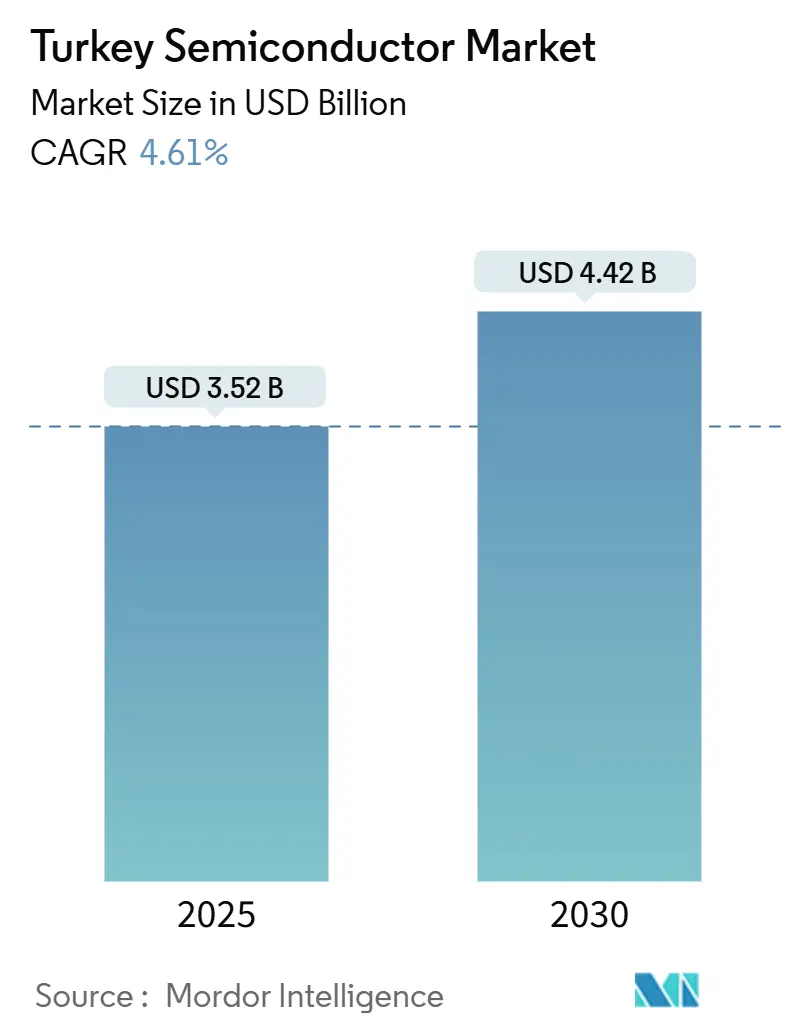

| Market Size (2025) | USD 3.52 Billion |

| Market Size (2030) | USD 4.42 Billion |

| Growth Rate (2025 - 2030) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Semiconductor Market Analysis by Mordor Intelligence

The Turkey semiconductor market size stood at USD 3.52 billion in 2025 and is forecast to reach USD 4.42 billion by 2030, reflecting a 4.61% CAGR over the period. Geopolitical supply-chain diversification under the EU Chips Act, generous domestic incentives, and a customs-union bridge to Europe are positioning the country as a preferred near-shoring destination for chip manufacturing. Government programs allocate USD 5 billion in investment support, while Horizon Europe unlocks EUR 4.175 billion in potential R&D funding, tightening the link between Turkish fabs and European demand. [1]Norton Rose Fulbright, “EU Chips Act Risks and opportunities for businesses,” nortonrosefulbright.com Rapid electric-vehicle (EV) adoption, 5G rollout plans, and expanding defense-electronics programs are multiplying local chip requirements across power management, RF, and sensor categories. International automakers and telecom vendors are accelerating joint ventures to leverage Turkey’s cost advantages and tariff-free EU access. Meanwhile, medium-node fabrication limits and export-control headwinds temper near-term upside by constraining sub-10 nm capacity and equipment availability.

Key Report Takeaways

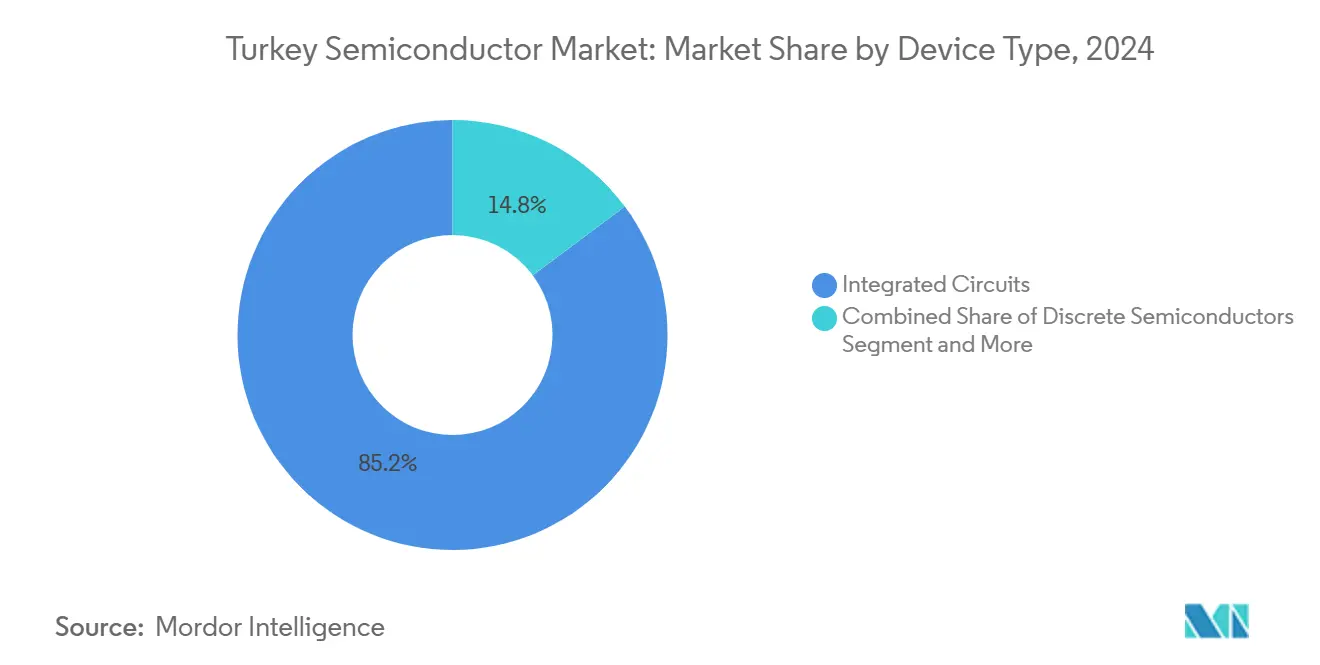

- By device type, integrated circuits held an 85.2% share of the Turkey semiconductor market size in 2024, while sensors and MEMS are advancing at a 6.3% CAGR through 2030.

- By business model, IDM players accounted for 60.3% of the Turkey semiconductor market share in 2024; design and fabless vendors are expanding at a 5.6% CAGR to 2030.

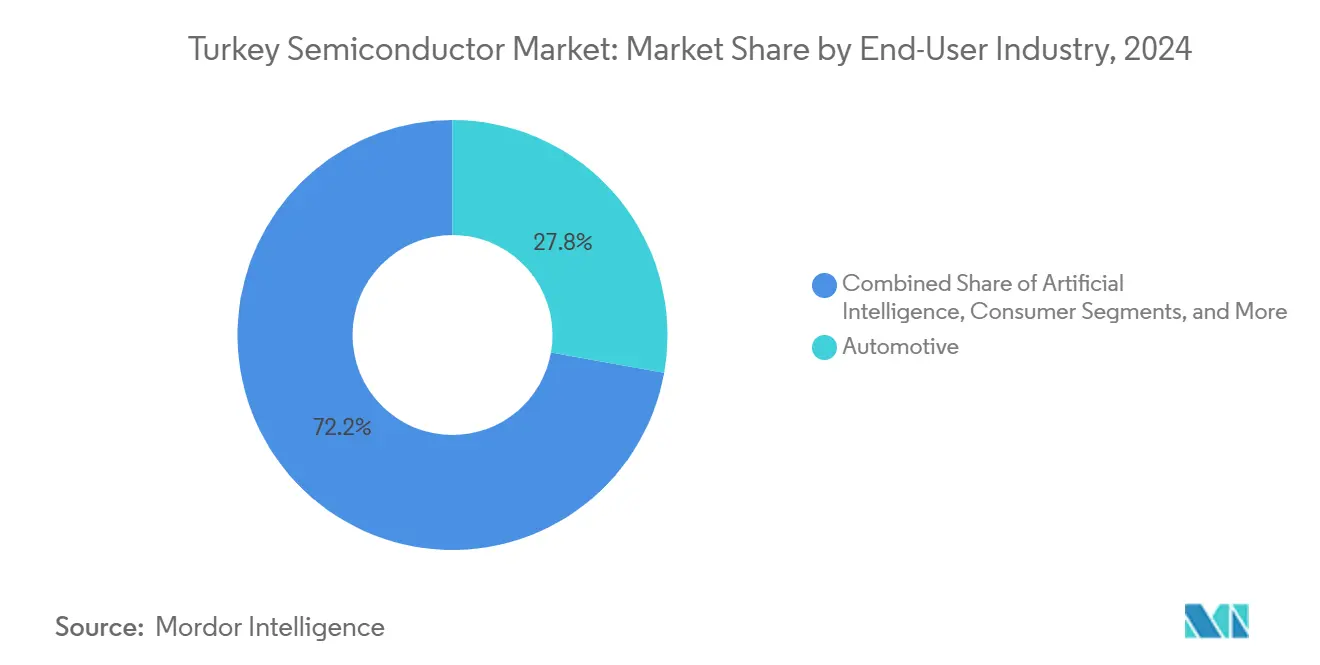

- By end-user industry, automotive commanded 27.81% of the Turkey semiconductor market size in 2024, whereas artificial-intelligence applications are projected to grow at a 6.5% CAGR to 2030.

Turkey Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives and investment programs | +1.2% | National, with concentration in Technology Development Zones | Medium term (2-4 years) |

| Rising domestic demand from automotive electrification | +0.9% | National, with early gains in Bursa, Kocaeli, Sakarya | Short term (≤ 2 years) |

| Growth in 5G and IoT deployments | +0.7% | National, with priority in Istanbul, Ankara, Izmir | Medium term (2-4 years) |

| Expansion of defence-electronics projects | +0.6% | National, with focus in Ankara defense corridor | Long term (≥ 4 years) |

| Qatar–Turkey joint fab partnership | +0.4% | National, with potential facility location undetermined | Long term (≥ 4 years) |

| EU Chips-Act near-shoring to Turkey | +0.5% | National, with emphasis on western industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives and Investment Programs

Turkey’s High Technology Investment Program sets aside USD 5 billion exclusively for semiconductor development within a broader USD 30 billion incentive framework, granting tax exemptions for R&D across 101 Technology Development Zones. [2]Invest in Türkiye, “Investment Zones – Invest in Türkiye,” invest.gov.tr Rather than direct subsidies, the scheme embeds support in infrastructure and fiscal relief, accelerating fab expansions and attracting startups backed by TÜBİTAK BiGG and the Turcorn program. The state aims to lift its share of global FDI inflows to 1.5% by 2028 through these measures. Early evidence shows an uptick in seed-round deal values for local chip design ventures that co-locate near university clusters. Sustaining the driver depends on maintaining macro-economic stability that reassures foreign partners about long-term asset safety.

Rising Domestic Demand from Automotive Electrification

EV sales overtook diesel models in 2024, reaching 99,849 units and 10.1% domestic share, a turning point that multiplies semiconductor content per vehicle. Chinese automaker BYD committed USD 1 billion to a 150,000-unit annual plant, exploiting Turkey’s customs-union status for tariff-free EU exports. Chery Automobile followed with a USD 1.5 billion plan for 200,000 units, cementing a regional EV hub. This inflow forces Tier-1 suppliers to localize advanced power-management ICs, high-voltage SiC devices, and battery-monitoring microcontrollers. The automotive cluster, exporting 70% of output to Western Europe, now retools for electronic architectures, expanding domestic test-handling and back-end assembly capacity.

Growth in 5G and IoT Deployments

Authorities will auction 5G spectrum in August 2025, propelling demand for RF front-ends, base-station SoCs, and edge AI accelerators. Ericsson and Türk Telekom’s 6G research‐sharing pact widens the pipeline for telecom-grade semiconductors adapted to local operating bands. Turkey’s ICT market rose from USD 15 billion in 2021 to USD 25 billion in 2023, reflecting widespread digitalization. A USD 5 billion earmark for 5G infrastructure includes localization quotas that favor domestically designed chipsets. Parallel industrial IoT rollouts, such as ULAQ-TÜRKSAT private 5G networks, lift sensor and secure-element volumes for shipyards, ports, and smart-factory projects.

Expansion of Defence-Electronics Projects

ASELSAN spent USD 329 million—7% of revenue—on R&D in 2024, focusing on gallium-nitride AESA radar chips and infrared detector arrays. Defense programs covering UAV avionics, secure communications, and naval fire-control systems increasingly rely on locally fabricated mixed-signal ASICs to avoid export controls. Havelsan’s simulation suites and Turkish Aerospace’s Kaan fighter advance the demand for high-temperature, radiation-hardened semiconductors. Export growth in defense electronics underpins volume scaling: ASELSAN targets a top-30 global ranking by 2030, widening its supplier ecosystem for RF MMICs and power modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited advanced-node manufacturing capability | -0.8% | National, affecting all high-tech manufacturing regions | Long term (≥ 4 years) |

| Supply-chain dependence on export-controlled equipment | -0.6% | National, with particular impact on defense and AI sectors | Medium term (2-4 years) |

| Skilled-talent shortages and brain-drain | -0.4% | National, with concentration in Istanbul, Ankara technical centers | Medium term (2-4 years) |

| Domestic-currency volatility inflating import costs | -0.5% | National, affecting all import-dependent semiconductor applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Advanced-Node Manufacturing Capability

Domestic production remains stuck above 28 nm; TÜBİTAK’s 250 nm line and the planned Qatar-Turkey 110/65 nm fab trail global leaders by several generations. [3]Para Dergi, “TÜBİTAK'tan çip üretiminde yeni bir adım,” paradergi.com.tr AI accelerators and 5G chipsets developed locally must therefore tape-out at overseas foundries, raising lead-times and currency-risk-adjusted costs. Participation in EU Chips Act projects could accelerate technology transfer, but doing so requires strict IP-sovereignty compliance that may clash with existing Sino-Turkish alliances. The capability gap constrains the Turkey semiconductor market when bidding for sub-10 nm automotive ADAS or data-center ASIC mandates and slows the diffusion of advanced lithography skills.

Supply-Chain Dependence on Export-Controlled Equipment

U.S. BIS rules issued in December 2024 curtail Turkey’s access to advanced lithography tools, high-bandwidth-memory IP, and specialized EDA software if U.S.origin content exceeds de-minimis levels. The Foreign Direct Product regime complicates servicing of older Chinese equipment, forcing maintenance delays and component cannibalization. Compliance burdens weigh especially on defense and AI vendors that need dual-use items, resulting in longer prototyping cycles and inflated BOM costs. ASELSAN’s workaround—developing ASELFLIR-500 after a camera embargo—illustrates resilience but also the expense of substituting restricted imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Drive Market Consolidation

Integrated circuits accounted for 85.2% of Turkey's semiconductor market share in 2024, underpinned by automotive microcontrollers, defense RF MMICs, and telecom SoCs. Analog and MCU categories enjoy robust pull from battery management and body-electronics upgrades, while logic and memory benefit from nascent cloud and AI clusters. Discrete power devices remain indispensable for EV traction inverters and renewable-energy converters. Optoelectronics demand centers on LiDAR and night-vision modules for military and industrial automation projects.

Sensors and MEMS, though smaller, are posting a 6.3% CAGR to 2030—the fastest within the Turkey semiconductor market. Industrial IoT modernization pushes factory owners to deploy pressure, magnetic, and accelerometer units tied to edge gateways. The National AI Strategy also calls for localized sensor fusion at the network edge, spawning demand for embedded MEMS packages co-designed with domestic AI processors.

By Business Model: Design Capabilities Reshape Value Creation

IDM enterprises captured 60.3% of Turkey semiconductor market size in 2024 thanks to vertically integrated leaders such as ASELSAN and the Turkish unit of STMicroelectronics. Their ability to align design, fab, and packaging accelerates time-to-deployment for mission-critical applications. The model’s capital intensity is offset by secure supply; defense contractors prize in-house fabs that bypass export licenses.

Design and fabless outfits are expanding at a 5.6% CAGR to 2030, a sign of the Turkey semiconductor market moving up the value chain into IP creation. Electra IC and HEX Microchip leverage university-linked incubators to tape-out MCU cores and mixed-signal blocks at TSMC and GlobalFoundries. The customs-union accord grants these firms tariff-free shipment of packaged devices into Europe, sharpening cost competitiveness without owning fabs. Their success, however, depends on sustained wafer allocation from overseas partners while domestic node gaps persist.

By End-User Industry: Automotive Electrification Accelerates Demand

Automotive held 27.81% of Turkey semiconductor market size in 2024, anchored by a USD 23.9 billion export engine that now pivots from internal-combustion to electric drivetrains. Every EV carries battery-monitoring ICs, SiC power modules, ADAS processors, and connectivity chipsets—driving per-car semiconductor value far above traditional models. Upcoming BYD and Chery plants will scale local demand for on-board chargers, vehicle-control domain controllers, and solid-state LiDAR driver ASICs.

Artificial-intelligence deployments represent the fastest-growing slice at 6.5% CAGR, supported by the National AI Strategy and emergent data-center projects. Defense AI labs require edge accelerators for drone swarms and autonomous naval craft, while telcos trial 5G Open RAN units powered by AI inference ASICs. Industrial automation adds steady uptake for machine-vision SoCs and predictive-maintenance sensor hubs, integrating domestic AI silicon when available.

Geography Analysis

Turkey’s customs-union link to Europe gives fabricators tariff-free access to 450 million consumers, a lure amplified by EU efforts to double regional semiconductor self-sufficiency by 2030. Bursa, Kocaeli, and Sakarya anchor automotive clusters; Ankara houses a defense-electronics corridor, and Istanbul leads in telecom and design services. Horizon Europe grants worth EUR 4.175 billion channel R&D funds into joint projects that tie Turkish fabs to German and French design houses. Meanwhile, proximity to the Middle East and Central Asia offers alternative export corridors, diversifying revenue streams.

Regional fabs benefit from lower energy tariffs and an industrial electricity grid that already powers large white-goods plants. Amazon’s decision to build satellite parts locally signals confidence in advanced-manufacturing reliability, indirectly expanding aerospace-grade semiconductor demand. [4]Türkiye Today, “Amazon to manufacture satellite parts in Türkiye,” turkiyetoday.com Currency swings remain a short-term challenge but are partly hedged by revenues denominated in EUR and USD from export contracts.

Competitive Landscape

Global majors—STMicroelectronics, Samsung Electronics, and NVIDIA—supply advanced logic, memory, and GPU accelerators to Turkish OEMs, usually through regional distribution hubs. Indigenous companies such as ASELSAN, TÜBİTAK BİLGEM, and Anka Mikroelektronik specialize in defense and industrial ASICs, leveraging government offsets and export-license exemptions to secure niche positions. Competitive advantage increasingly hinges on application-specific IP rather than wafer volumes. ASELSAN’s GaN-based AESA radar chip, flight-tested on F-16s in July 2025, illustrates home-grown breakthroughs that also feed into export campaigns to Azerbaijan and Gulf allies.

Domestic design houses form consortiums with European research institutes to co-develop RISC-V cores and automotive functional-safety libraries. The rise of such alliances reflects Turkey’s twin strategy: capture value at the design level while courting EU fabs for wafer supply under the Chips Act funding umbrella.

Turkey Semiconductor Industry Leaders

STMicroelectronics International N.V.

Samsung Electronics Co., Ltd.

NVIDIA Corporation

ASELSAN Elektronik Sanayi ve Ticaret A.Ş.

Türkiye Bilimsel ve Teknolojik Araştırma Kurumu (TÜBİTAK) BİLGEM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ASELSAN completed maiden flight tests of GaN AESA radar on Turkish F-16 aircraft.

- July 2025: ASELSAN displayed Göksur VLS and Cenk 350-N radar at IDEF 2025, sealing new export deals.

- June 2025: The government confirmed the August 2025 5G spectrum auction to accelerate the national rollout.

- March 2025: ULAQ and TURKSAT signed a contract to build 5G private networks for industrial sites.

- January 2025: Ankara announced USD 2 billion for space and high-tech projects, including semiconductor R&D.

- December 2024: Amazon chose Turkey for satellite-component manufacturing, expanding its aerospace supply chain.

Turkey Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

How large is the Turkey semiconductor market today?

The Turkey semiconductor market size reached USD 3.52 billion in 2025 and is projected to climb to USD 4.42 billion by 2030.

Which end-use segment buys the most chips in Turkey?

Automotive makers led 2024 demand with 27.81% of market value, reflecting the rapid pivot to electric-vehicle production.

What growth rate is forecast for Turkey’s sensor and MEMS segment?

Sensors and MEMS are expected to expand at a 6.3% CAGR through 2030, the fastest among device categories.

How does the EU Chips Act affect Turkey?

Horizon Europe aligns EUR 4.175 billion in R&D grants that can flow to Turkish fabs and design houses, reinforcing tariff-free supply into the EU.

Which domestic company is most active in advanced RF chips?

ASELSAN has invested USD 329 million in R&D and flight-tested GaN-based AESA radar modules on F-16 aircraft in 2025.

When will Turkey launch nationwide 5G service?

The state plans to auction spectrum in August 2025, unlocking base-station and edge-compute semiconductor demand immediately thereafter.

Page last updated on: