Italy Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

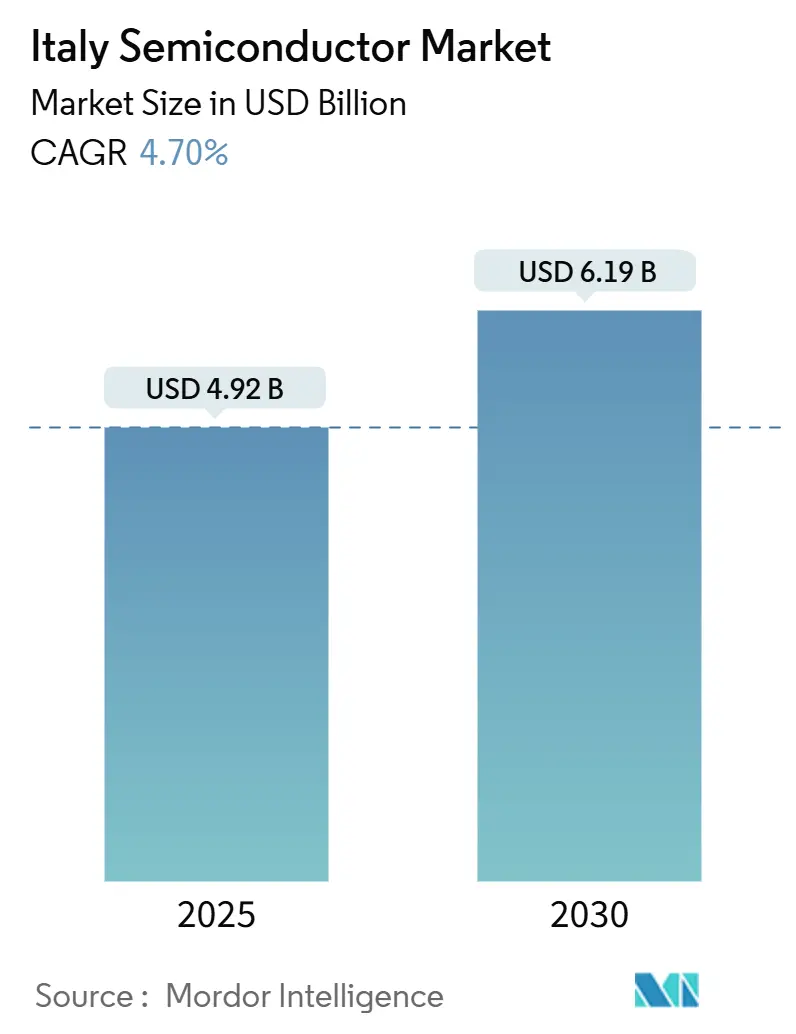

| Market Size (2025) | USD 4.92 Billion |

| Market Size (2030) | USD 6.19 Billion |

| Growth Rate (2025 - 2030) | 4.70% CAGR |

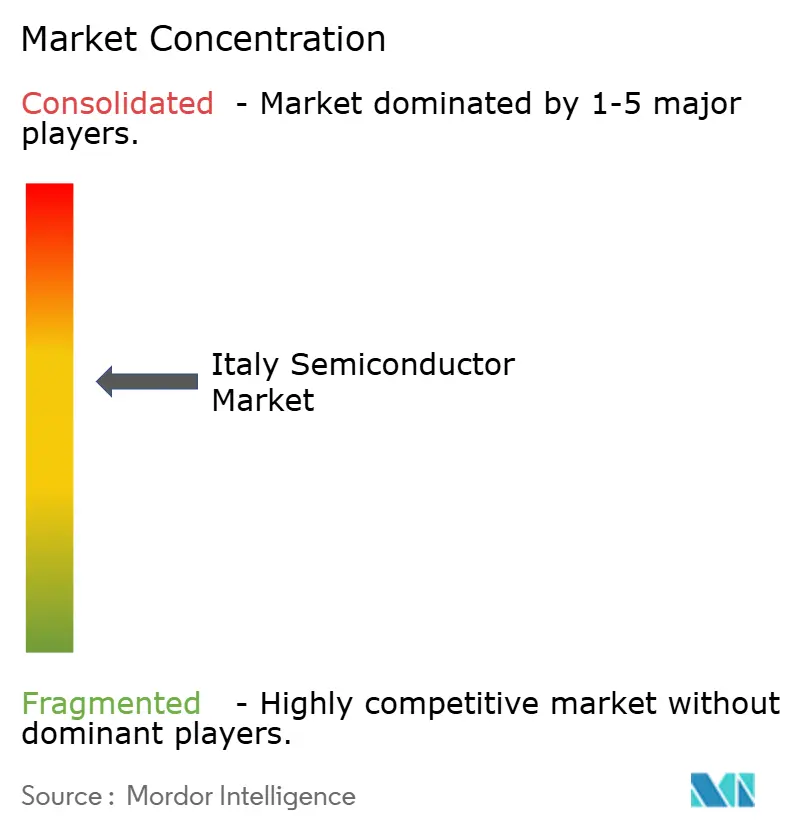

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Semiconductor Market Analysis by Mordor Intelligence

The Italy semiconductor market size reached USD 4.92 billion in 2025 and is forecast to expand at a 4.70% CAGR, lifting the value to USD 6.19 billion by 2030. Sustained capital inflows from the National Recovery and Resilience Plan, deep-rooted automotive electronics demand, and the entrance of large-scale advanced-packaging capacity underpin this growth trajectory. Domestic champion STMicroelectronics has retained technology leadership through vertically integrated SiC and power platforms, while Silicon Box’s EUR 3.2 billion (USD 3.5 billion) Novara project signals accelerating foreign direct investment. Energy-efficiency retrofits under Piano Transizione 5.0 and nationwide 5G private-network deployments widen the application base, even as talent shortages at sub-28 nm constrain Italy’s progression toward leading-edge nodes. Overall, the Italy semiconductor market is transforming from a supply-constrained ecosystem into a strategically positioned contributor to Europe’s chip sovereignty goals.[1]European Commission, “State aid: Commission approves EUR 2 billion Italian measure for STMicroelectronics SiC plant,” ec.europa.eu

Key Report Takeaways

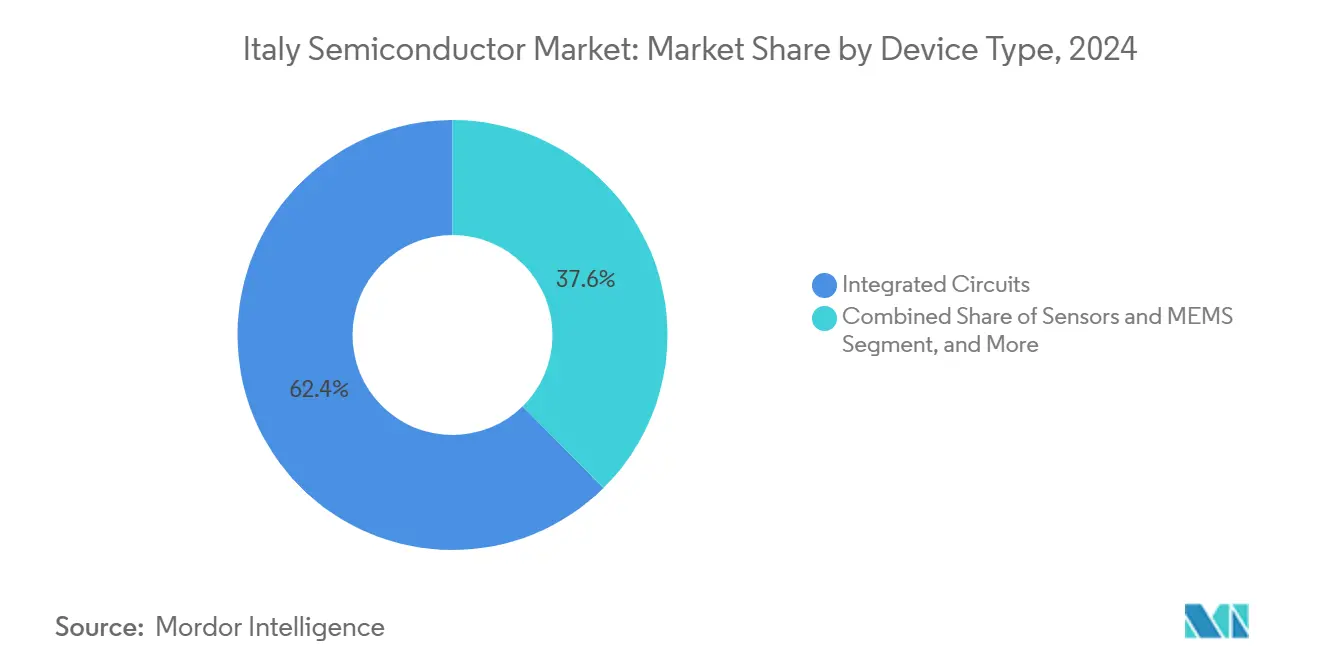

- By device type, integrated circuits led with a 62.40% Italy semiconductor market share in 2024, while sensors and MEMS are growing fastest at a 7.91% CAGR through 2030.

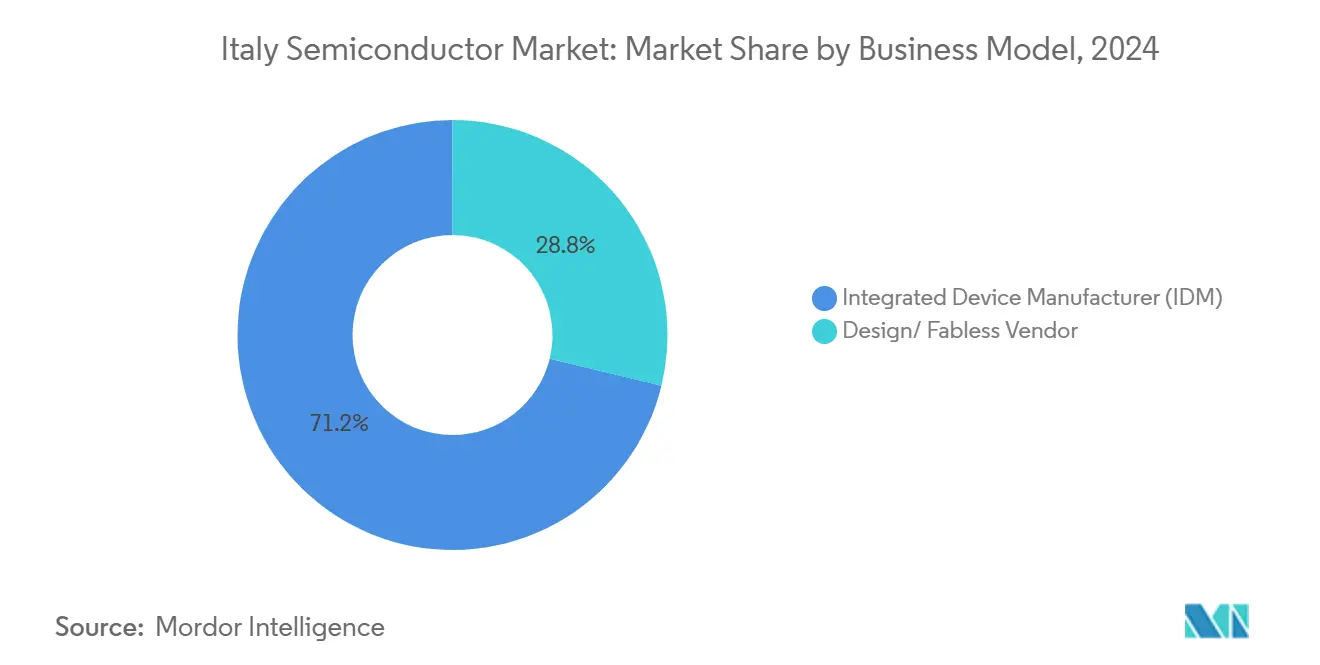

- By business model, the IDM segment held 71.20% of the Italy semiconductor market size in 2024; the fabless segment is progressing at an 8.03% CAGR to 2030.

- By end-user industry, automotive captured 28.60% revenue in 2024, and AI applications are advancing at an 8.80% CAGR through 2030.

Italy Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EV-driven SiC demand | +1.20% | Northern Italy, with spillover to Sicily | Medium term (2-4 years) |

| Rising industrial automation retrofits | +0.80% | Lombardy, Emilia-Romagna, Piedmont | Short term (≤ 2 years) |

| 5G private-network roll-outs by Italian telcos | +0.60% | National, with early gains in Milan, Rome, Turin | Medium term (2-4 years) |

| National micro-electronics R&D tax incentives (2025-29) | +0.90% | National, concentrated in university clusters | Long term (≥ 4 years) |

| Edge-AI chip design start-up activity in Turin and Milan | +0.40% | Northern Italy technology hubs | Long term (≥ 4 years) |

| Automotive camera-module legislation (Euro NCAP 2026) | +0.70% | National, with manufacturing in Piedmont | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated EV-driven SiC Demand

STMicroelectronics inaugurated Europe’s first fully integrated SiC line in Catania, targeting 15,000 200 mm wafers per week once fully ramped.[2]STMicroelectronics, “Catania SiC Mega-Fab Fact Sheet,” st.com Vertical integration curtails outsourced substrate reliance and lowers unit costs by 30%, enabling Italian fabs to meet the 800 V powertrain shift in premium EVs. Logistics efficiencies stemming from proximity to German and French automakers further improve supply assurance, anchoring Italy semiconductor market growth in power devices.

Rising Industrial-Automation Retrofits

The EUR 12.7 billion Piano Transizione 5.0 tax-credit pool has accelerated procurement of semiconductor-rich robotics, sensors, and PLCs.[3]Ministero delle Imprese e del Made in Italy, “Piano Transizione 5.0 Incentive Guidelines,” mimit.gov.it Lombardy’s 670 microelectronics firms reported turnover resilience during early-2025, confirming broad-based pull for analog ICs and industrial-grade MCUs. As manufacturing plants replace aging 200 mm toolsets with energy-efficient lines, demand for power-management chips multiplies, deepening the Italy semiconductor market footprint across industrial verticals.

5G Private-Network Rollouts by Italian Telcos

TIM secured EUR 725 million to backhaul 5G traffic over fibre, complementing Vodafone’s first nationwide energy-sector private network and WindTre’s Port of Genoa. These projects require RF front-end modules, high-performance baseband ASICs, and edge-AI accelerators and segments addressed by Silicon Box’s Novara advanced-packaging hub. With population coverage already at 72%, semiconductors for small-cell densification form a reliable demand-pipeline for the Italy semiconductor market.

National Micro-electronics R&D Tax Incentives (2025-29)

Italy grants up to 75% R&D cost relief under the IPCEI Micro-electronics program, allocating EUR 1.5 billion through 2029. University-industry consortia funnel grants toward FD-SOI, neuromorphic, and photonics projects. Turin-based Neuronova taped out a processor achieving 1,000× energy improvement over conventional AI chips, demonstrating how fiscal incentives translate into indigenous IP creation. Such programs widen the design-startup funnel and embed longer-term growth drivers within the Italy semiconductor industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-cost volatility on 200mm fabs | -0.80% | National, acute in energy-intensive regions | Short term (≤ 2 years) |

| Talent scarcity in sub-28nm process engineering | -0.60% | Northern Italy technology clusters | Medium term (2-4 years) |

| Slow permitting for new clean-room capacity | -0.40% | National, bureaucratic bottlenecks | Medium term (2-4 years) |

| Post-2027 SiGe export-control risk for China-bound sales | -0.30% | National, export-dependent manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-cost Volatility on 200 mm Fabs

Electricity prices climbed 24% and gas 27% year-on-year in January 2025, pushing Italian power tariffs 40% above Spain and 30% above France and Germany. Because energy can represent 20% of 200 mm wafer costs, domestic fabs pivot to higher-margin specialty devices, limiting scale. While STMicroelectronics targets carbon neutrality by 2027, interim renewable investments strain cash flows, creating a drag on Italy semiconductor market expansion.

Talent Scarcity in Sub-28 nm Process Engineering

SEMI estimates the EU will require one million additional semiconductor workers by 2030. Italy’s universities lack EUV lithography exposure, forcing firms to hire expatriate engineers at premium wages. The FAMES Academy’s FD-SOI curriculum will alleviate shortages, but a three-year training lag misaligns with immediate production roadmaps, slowing advanced-node penetration within the Italy semiconductor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Drive Market Leadership

Integrated circuits commanded 62.40% of the Italy semiconductor market size in 2024, led by analog power-management and automotive MCUs. Analog ICs underpin battery-management systems in EVs, while microcontrollers run body-electronics and industrial PLCs. DSPs profit from 5G radio deployments, and memory chips service new colocation data centers. Sensors and MEMS, the fastest-growing category at a 7.91% CAGR, gain from Euro NCAP vision mandates and industrial IoT retrofits. Discrete devices stay relevant for renewable-energy inverters, and optoelectronics flourish with LED automotive lighting and fiber backhaul. Although 5 nm nodes are set to grow 8.24%, domestic manufacturing remains skewed toward mature technologies above 28 nm, counterbalanced by design-led access to overseas foundries.

Mature-node capacity expansions at STMicroelectronics’ Agrate 300 mm line and Tower Semiconductor’s specialty processes widen analog and RF output, keeping Italy competitive on differentiated products rather than commodity logic. Simultaneously, Silicon Box’s panel-level advanced-packaging operation shortens interposer supply chains, raising value capture from chiplet architectures. In tandem, MEMS gyroscopes and pressure sensors produced in Lombardy deliver critical content for industrial automation and autonomous-vehicle platforms, anchoring the Italy semiconductor market’s multi-product resilience.

By Business Model: IDM Dominance Faces Fabless Challenge

The IDM model retained a 71.20% Italy semiconductor market share in 2024, as STMicroelectronics leverages front-to-back control for SiC and BCD platforms. Supply guarantee and cost retention advantages remain pronounced amid global capacity tightness. Yet the fabless cohort is expanding at an 8.03% CAGR, propelled by asset-light start-ups and overseas foundry access. Novara’s advanced-packaging facility caters directly to fabless designers pursuing chiplet and heterogeneous-integration roadmaps at 5 nm and below.

Italian design houses capitalize on proximity to European automotive OEMs and R&D tax credits to target edge-AI and neuromorphic niches. Neuronova’s ultra-low-power processor, developed with 99% local design content, exemplifies how fabless agility can unlock emerging verticals. As IP portfolios deepen, collaboration between IDMs and design firms grows STMicroelectronics licenses specialty process nodes to external customers at Agrate, blending IDM scale with foundry services. These hybrid arrangements temper competitive friction and create pathways for broader participation across the Italy semiconductor market.

By End-user Industry: Automotive Leadership Meets AI Disruption

Automotive electronics generated 28.60% of 2024 revenue, anchored by electrification and ADAS mandates. Euro NCAP 2026 rules multiply camera and radar demand, while 800 V battery packs elevate SiC MOSFET penetration. Communications, covering wireless infrastructure and wired backhaul, benefits from aggressive 5G fibre rollouts. Industrial segments gain from energy-efficient automation, coupling power ICs with industrial-grade sensors in factory retrofits.

AI applications, though nascent, clock the fastest CAGR at 8.80%, spurred by data-sovereignty-driven cloud investments and edge inference for manufacturing analytics. Consumer electronics maintain moderate growth, while computing and data-storage business underpins demand for DDR5 and PCIe controllers. Government aerospace and defense programs sustain high-margin orders for radiation-hardened and secure-element chips. Cross-pollination between automotive functional-safety standards and AI accelerators creates blended opportunities for Italian suppliers, deepening the Italy semiconductor market’s strategic relevance.

Geography Analysis

Northern-Italy clusters host design, R&D, and specialty packaging, with Lombardy alone sheltering 670 microelectronics firms that employ 19,000 staff and post EUR 3.8 million turnover. Piedmont rises as a manufacturing nucleus through Silicon Box’s Novara project, complementing existing wafer-supply chain assets such as MEMC’s EUR 400 million expansion to one million wafers annually. Emilia-Romagna’s Big Data Technopole houses the “Leonardo” supercomputer, creating downstream demand for high-bandwidth memory and accelerator-class ASICs in HPC research.

Sicily diversifies the geographic footprint via STMicroelectronics’ EUR 5 billion Catania SiC complex, an integrated substrate-to-device line green-lit by EUR 2 billion state aid. The site leverages lower operating costs and proximity to Mediterranean logistics corridors, balancing northern concentration. Central government policy encourages multi-regional dispersion, mitigating single-point-of-failure risk while ensuring the Italy semiconductor market remains cohesive through rail and fibber interconnectivity.

Collectively, these clusters form a national value-chain mosaic: design hubs in Turin and Milan, volume front-end in Catania, and advanced packaging in Novara. Such geographic stratification aligns with the European Chips Act’s decentralization ethos, while Italy’s ports facilitate quick shipment to continental customers and Middle Eastern markets. University partnerships across these regions’ secure talent pipelines, reinforcing long-term competitiveness of the Italy semiconductor market.

Competitive Landscape

STMicroelectronics anchors the competitive field with end-to-end control of SiC, BCD, and MEMS processes, supplying Tier-1 automotive and industrial customers with high-reliability components. Silicon Box enters as an advanced-packaging pure-play, offering chiplet panel-level solutions that shorten time-to-market for fabless clients. Tower Semiconductor collaborates with STMicroelectronics at Agrate, raising specialty analog capacity and bringing photonics know-how to domestic soil. LFoundry, acquired by SMIC, injects mature-node CMOS capacity focused on automotive image sensors.

Technoprobe, buoyed by Teradyne’s USD 516 million equity infusion, strengthens back-end test-interface capabilities, while MEMC expands wafer production to underpin upstream supply stability. Emerging disruptors such as Neuronova target neuromorphic AI, leveraging R&D incentives to develop proprietary IP. Competitive intensity thus pivots from sheer wafer scale toward system integration and advanced packaging differentiation, positioning the Italy semiconductor market as a mid-node, high-value ecosystem rather than a commoditized volume producer.[4]Invest in Lombardy, “Lombardy: A Technological Hub for Chips,” investinlombardy.com

Italy Semiconductor Industry Leaders

STMicroelectronics N.V.

Infineon Technologies AG

ON Semiconductor Corporation

NXP Semiconductors N.V.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: STMicroelectronics completed a manufacturing-footprint restructuring, doubling Agrate 300 mm capacity to 4,000 wafers per week and initiating 200 mm SiC production in Catania

- February 2025: European Commission approved EUR 1.3 billion state aid for Silicon Box’s Novara advanced-packaging plant, the anchor of a EUR 3.2 billion total investment

- January 2025: Infineon commenced construction of a new backend facility in Thailand, aligning global power-device capacity

- December 2024: Tower Semiconductor received a manufacturing-excellence award from Semtech, underscoring analogy-specialty prowess

Italy Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| By Business Model | Integrated Device Manufacturer (IDM) | ||

| Design/ Fabless Vendor | |||

| By End-user Industry | Automotive | ||

| Communication (Wired and Wireless) | |||

| Consumer | |||

| Industrial | |||

| Computing/Data Storage | |||

| Data Center | |||

| AI | |||

| Government (Aerospace and Defense) | |||

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design/ Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the Italy semiconductor market in 2025?

The Italy semiconductor market size stands at USD 4.92 billion in 2025.

What is the projected CAGR for Italy's chip sector to 2030?

Market value is forecast to grow at a 4.70% CAGR between 2025 and 2030.

Which device category leads Italian chip revenue?

Integrated circuits dominate with 62.40% revenue share in 2024.

Why is Silicon Box building an advanced-packaging plant in Novara?

The EUR 3.2 billion project targets chiplet and heterogeneous-integration demand from Europe's fabless designers.

How will Euro NCAP 2026 rules affect semiconductor demand?

Mandatory ADAS features will increase orders for image sensors, camera ECUs, and high-performance processors used in automotive platforms.

What is the main growth restraint for Italian fabs?

Energy-cost volatility, with electricity prices 40% above Spain, puts pressure on 200 mm production economics.

Page last updated on: