India Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

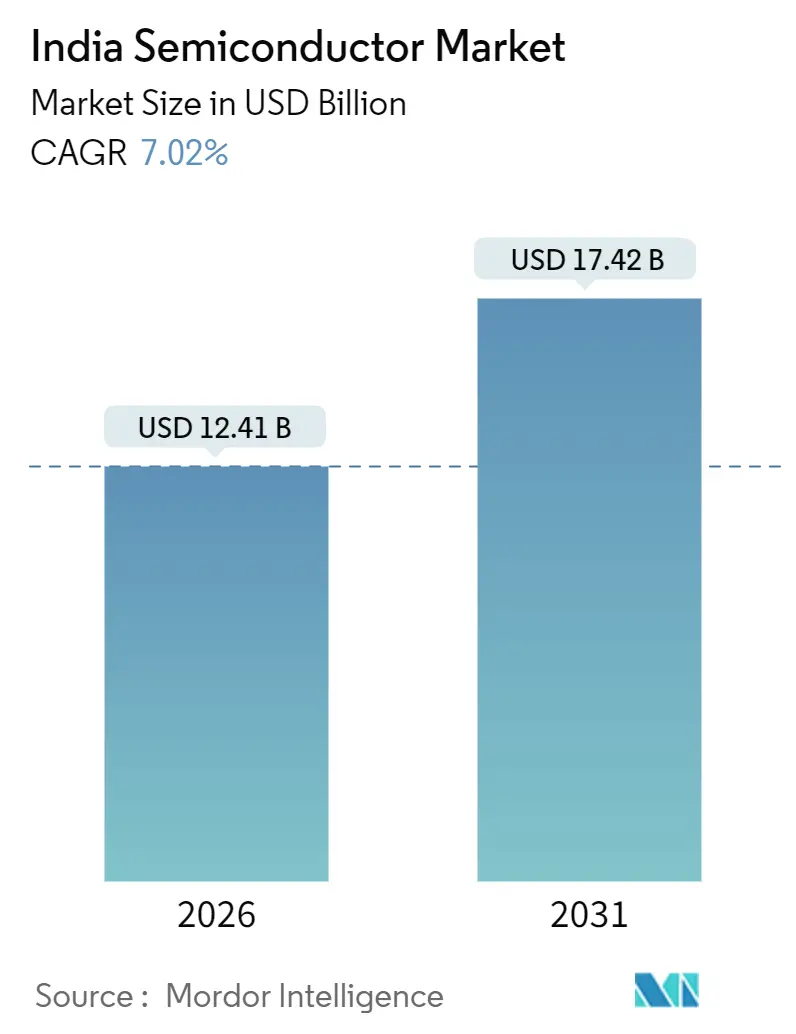

| Market Size (2026) | USD 12.41 Billion |

| Market Size (2031) | USD 17.42 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Semiconductor Market Analysis by Mordor Intelligence

The India semiconductor market size stood at USD 12.41 billion in 2026 and is projected to reach USD 17.42 billion by 2031, advancing at a 7.02% CAGR during 2026-2031. A steady fiscal push under the Production Linked Incentive and Design Linked Incentive schemes is lowering entry barriers and attracting capital-intensive wafer fabrication as well as assembly, test, mark, and pack facilities. Mature-node capacity additions, especially at 28-110 nanometers, are aligning with surging domestic demand for analog, power-management, and microcontroller devices. Programmed electrification of transport, expansion of BharatNet fiber, and the construction of hyperscale data centers are each catalyzing distinct waves of silicon demand, prompting multinational integrated-device manufacturers to deepen local design footprints. Meanwhile, domestic firms are leveraging open-source RISC-V cores to tap niche microcontroller, power semiconductor, and sensor opportunities, signaling a gradual shift from import dependence toward indigenous value creation.

Key Report Takeaways

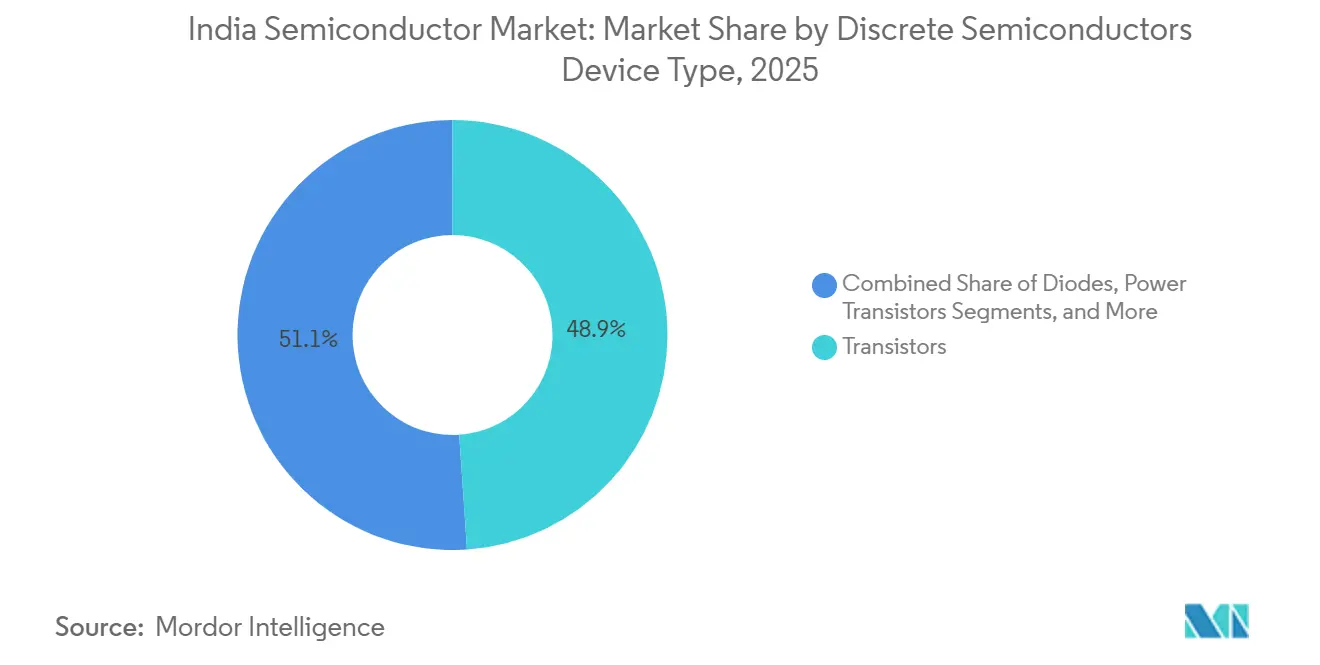

- By device type, discrete semiconductors, transistors captured 48.92% of segment revenue in 2025; diodes, however, are projected to expand at a 7.82% CAGR through 2031.

- By device type, optoelectronics saw light-emitting diodes hold 38.83% of 2025 revenue, yet laser diodes are set to grow at 8.02% CAGR by 2031.

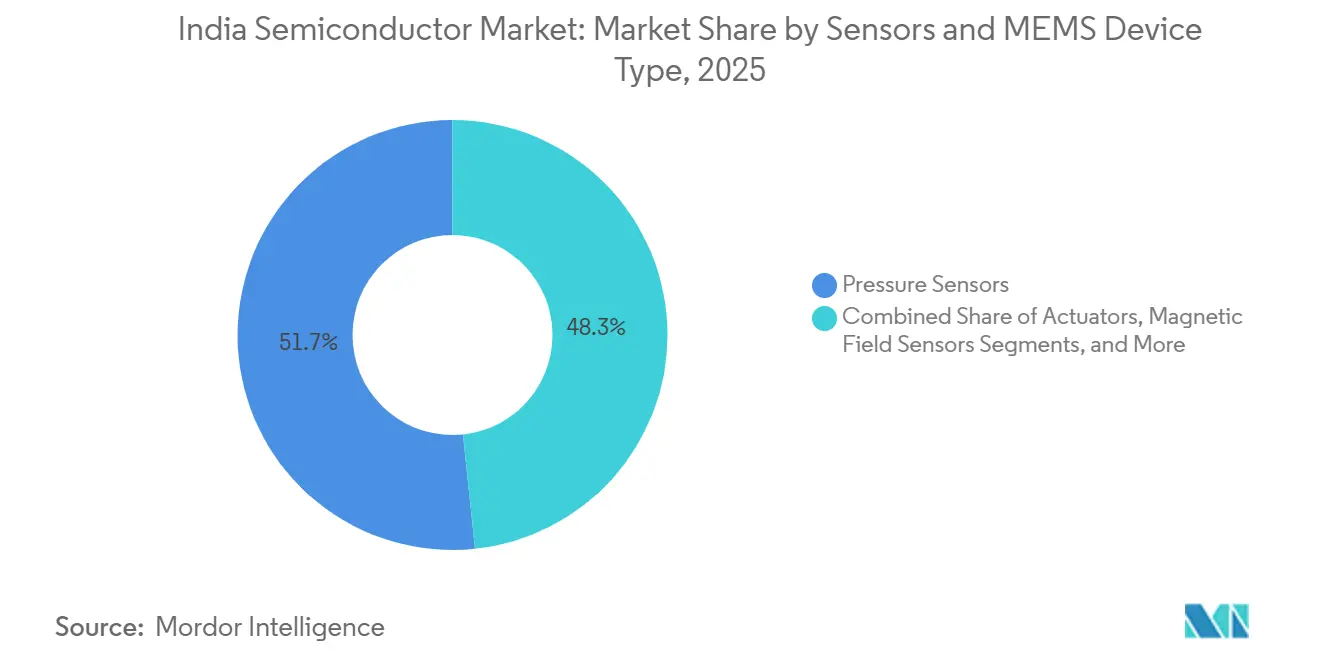

- By device type, sensors and MEMS, pressure sensors dominated with a 51.66% 2025 share; actuators are forecast to accelerate at 8.22% CAGR through 2031.

- By end-user industry, the communication segment accounted for 32.87% of 2025 revenue, while automotive applications are poised for the fastest expansion at an 8.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentive Schemes (PLI, DLI) | +1.8% | National, with early gains in Gujarat, Uttar Pradesh, Punjab | Medium term (2-4 years) |

| Rapid Electrification of Transport | +1.5% | National, concentrated in Maharashtra, Karnataka, Tamil Nadu, Delhi NCR | Long term (≥ 4 years) |

| 5G Roll-out and BharatNet Fibre Expansion | +1.2% | National, rural focus in Uttar Pradesh, Bihar, Madhya Pradesh | Medium term (2-4 years) |

| Data-Centre and AI Workloads | +1.0% | South and West India, primarily Maharashtra, Karnataka, Telangana | Short term (≤ 2 years) |

| Indigenous GaN/SiC Pilot Fabs | +0.6% | National, pilot projects in Karnataka, Gujarat | Long term (≥ 4 years) |

| Trusted Defense-grade Fab Accreditation | +0.5% | North India, centered on Punjab (SCL Mohali), Karnataka (BEL) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentive Schemes (PLI, DLI)

A combined outlay of INR 760 billion (USD 9.1 billion) under the Production Linked Incentive and Design Linked Incentive programs is lowering capital costs by as much as 50% for qualified projects, making greenfield fabs commercially viable where they once were prohibitive. Tata Electronics began site preparation for a 300-millimeter facility in Dholera that targets 50,000 wafer starts per month at mature nodes, and Micron Technology’s back-end plant in Sanand dispatched its first packaged memory in late 2024. The Union Budget 2025 further eliminated customs duties on lithography tools and ultrapure gases, trimming build-out timelines and import barriers. Collectively, these fiscal levers are steering the India semiconductor market toward a more vertically integrated footing.

Rapid Electrification of Transport

Electric-vehicle sales are rising precipitously under the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles scheme, which allocates INR 100 billion (USD 1.2 billion) to charging infrastructure. Higher voltage drivetrains require silicon-carbide MOSFETs, insulated-gate bipolar transistors, and power-management ICs, boosting demand for devices that India has historically imported. Automotive end-user revenue is therefore forecast to grow at an 8.66% CAGR, the fastest among all verticals. The upcoming Dholera fab will dedicate part of its capacity to analog power-management ICs and microcontrollers for electric two-wheelers and passenger cars, narrowing supply-chain exposure to offshore foundries.

5G Roll-out and BharatNet Fibre Expansion

BharatNet Phase III has awarded INR 1.39 trillion (USD 16.7 billion) in contracts to extend fiber connectivity to 270,000 villages by 2030.[1]Department of Telecommunications, “National Broadband Mission,” dot.gov.in Optical line terminals and dense wavelength-division multiplexing equipment embed laser diodes, photonic integrated circuits, and application-specific ICs, widening the market for optoelectronic and mixed-signal devices. Communication equipment already accounted for 32.87% of 2025 demand, and the rural build-out is expected to keep that share resilient even as automotive demand rises. The HCL-Foxconn joint venture in Uttar Pradesh illustrates how localized display-driver IC production can feed both smartphone and base-station ecosystems.

Data-Center and AI Workloads

Maharashtra, Karnataka and Telangana are witnessing a wave of tier-IV data-center construction, each facility requiring tens of thousands of high-bandwidth-memory stacks and custom accelerators. To support this surge, Intel and ARM opened 2-nanometer design centers in Bengaluru in 2025, underscoring confidence in local engineering talent for cutting-edge node designs. The Ministry of Electronics and Information Technology’s AI Mission earmarked INR 103.72 billion (USD 1.25 billion) for GPU procurement and public compute infrastructure, indirectly stimulating domestic packaging demand for memory and interconnect devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skill Shortage in Advanced-node Engineering | -0.8% | National, acute in Karnataka, Telangana, Maharashtra | Short term (≤ 2 years) |

| Limited Ultrapure Water and Power Infrastructure | -0.6% | Gujarat, Uttar Pradesh, Punjab | Medium term (2-4 years) |

| Fragmented OSAT Capacity | -0.4% | National, concentrated in Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Land and Environmental Clearance Delays | -0.3% | Gujarat, Uttar Pradesh, Maharashtra | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skill Shortage in Advanced-node Engineering

The India Electronics and Semiconductor Association estimates a shortfall of 300,000 engineers across design, fabrication and test disciplines, despite a projected need for 85,000 additional professionals by 2027.[2]India Electronics and Semiconductor Association, “Workforce Skill Gap Report,” iesaonline.org Local universities are expanding curricula, and the India Semiconductor Mission has set aside INR 5 billion (USD 60 million) for scholarships and apprenticeships, yet attrition rates above 20% persist in key design hubs. The talent squeeze risks delaying tape-outs and stretching ramp-up timelines, especially for 2-nanometer and below.

Limited Ultrapure Water and Power Infrastructure

A 300-millimeter fab consumes up to 4 million liters of ultrapure water daily and draws upward of 100 megawatts of continuous power. Tata Electronics is investing INR 30 billion (USD 360 million) in desalination and reverse-osmosis facilities at Dholera because municipal supply cannot meet the 18-megohm-centimeter purity standard. Similar power reliability challenges in Gujarat and Punjab necessitate dedicated feeders and on-site substations, adding 8-12% to project capital expenditure and elongating payback periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Discrete Semiconductor Device Type: Power Conversion Drives Diode Momentum

Transistors held 48.92% of discrete-device revenue in 2025, yet diodes are expected to grow at a 7.82% CAGR to 2031 as electric-vehicle chargers and renewable-energy inverters favor silicon-carbide Schottky designs that minimize switching losses. The India semiconductor market size for discrete diodes is therefore set to expand in line with nationwide charger rollouts linked to the FAME program. Varistors, thyristors and transient-voltage suppressors remain relevant for surge protection in telecom and consumer devices, ensuring a balanced product mix.

Cyient-Azimuth’s ARKA GKT-1 system-on-chip, slated for mid-2026 production, integrates gate drivers and MOSFETs on one die, shrinking board space for two-wheeler OEMs. The Design Linked Incentive scheme’s emphasis on compound semiconductors is poised to unlock domestic gallium-nitride transistor development, reducing import reliance for 5G base-station equipment and satellite terminals. Across industrial automation and UPS applications, insulated-gate bipolar transistors continue to dominate high-current switching, anchoring transistor demand even as diode shipments accelerate.

By Optoelectronics Device Type: Laser Diodes Gain on Data-Center Interconnects

Light-emitting diodes commanded 38.83% of optoelectronic revenue in 2025, but laser diodes are projected to outpace with an 8.02% CAGR, reflecting data-center upgrades to 400-gigabit and 800-gigabit Ethernet. Image sensors, chiefly CMOS, service a buoyant smartphone market of more than 150 million annual shipments, while optocouplers enable galvanic isolation in industrial motor drives.

India’s local optoelectronics output remains nascent, with over 80% of parts imported, prompting the phased manufacturing program to offer 15% capital subsidies for photonic IC fabs.[3]Ministry of Electronics and Information Technology, “Phased Manufacturing Programme,” meity.gov.in BharatNet’s fiber build-out will require roughly 50 million optical transceivers by 2030, creating a sizable captive market for vertical-cavity surface-emitting lasers. Initiatives in Kerala and Telangana are exploring photonics assembly lines, signaling early-stage regional diversification within the India semiconductor market.

By Sensors and MEMS Device Type: Actuators Surge in Automotive Safety Systems

Pressure sensors accounted for 51.66% of sensors and MEMS revenue in 2025, yet actuators are forecast to register the fastest growth at 8.22% CAGR through 2031 as adaptive cruise control, lane-keeping assist and automated parking become standard features. Magnetic-field sensors enable brushless DC motor commutation in electric scooters, whereas acceleration and yaw-rate sensors underpin electronic stability control in passenger cars.

The Semi-Conductor Laboratory fabricates MEMS on 150-millimeter wafers using deep reactive-ion etching, capabilities demonstrated by the MEMS acoustic sensor that flew on ISRO’s PSLV-C55 mission.[4]Semi-Conductor Laboratory, “SCL Mohali Modernization Project,” scl.gov.in IIT Madras announced an indigenous MEMS gyroscope in October 2025, signaling domestic design maturity. As OEMs specify piezoelectric and electrostatic actuators for mirror adjustment and brake-by-wire, the India semiconductor market share of domestic MEMS suppliers is poised to rise from a low single-digit base.

By End-User Industry: Automotive Outpaces Communication on EV Momentum

Communication equipment comprised 32.87% of 2025 revenue, powered by 5G base-station rollouts and robust smartphone demand. Automotive, however, is projected to expand at 8.66% CAGR as semiconductor content per electric vehicle approaches USD 1,000, roughly double that of internal-combustion counterparts.

Electric-vehicle battery management, on-board chargers, and advanced driver-assistance modules together lift analog, microcontroller, and power-transistor volumes. Consumer electronics remain a significant end-user, yet lengthening replacement cycles temper growth. Industrial automation benefits from Make in India policies that encourage local sourcing of programmable logic controllers and servodrive ICs. Data-center operators in Maharashtra and Karnataka continue to build GPU-rich clusters that favor high-bandwidth memory and chiplet-based processors, adding another growth vector for the India semiconductor market.

Geography Analysis

North India emerged as the leading contributor to revenue in 2025, underpinned by the HCL-Foxconn INR 37 billion (USD 444 million) display-driver IC plant in Jewar and the INR 45 billion (USD 540 million) modernization of the Semi-Conductor Laboratory in Mohali. Delhi NCR hosts design centers for Intel, Qualcomm, and MediaTek, concentrating on analog layout and verification skills. Haryana’s proximity to automotive OEMs fosters demand for microcontrollers and sensors, whereas Rajasthan’s renewable-energy corridors drive power-transistor uptake. Infrastructure bottlenecks around ultrapure water and grid stability persist but are being mitigated through dedicated feeders and desalination investments.

West India is on track to be the fastest-growing region through 2031. Gujarat’s Dholera Special Investment Region houses Tata Electronics’ INR 910 billion (USD 10.9 billion) fab, while Micron Technology’s INR 225 billion (USD 2.7 billion) assembly and test facility in Sanand shipped its first DRAM modules in 2024. Maharashtra’s automotive corridors and hyperscale data centers add incremental demand for analog and optoelectronic devices. Goa and Mumbai contribute niche production in consumer electronics and laser packaging, respectively, though environmental clearance processes have elongated project gestation by up to a year.

South India retains its status as the nation’s chip-design nucleus. Bengaluru alone hosts more than 300 design outfits, including newly inaugurated 2-nanometer centers from Intel and ARM. IIT Madras showcased the 7-nanometer SHAKTI processor in October 2025, illustrating sovereign micro-architecture ambitions. Telangana’s Hyderabad serves as Qualcomm’s largest design hub outside the United States, while Tamil Nadu’s manufacturing clusters assemble printed circuit boards and power supplies. Andhra Pradesh and Kerala are courting optoelectronics and photonics investors, although time-to-market remains uncertain. East and Northeast India trail the other regions but are beginning to court assembly and test ventures, primarily through state-level incentives.

Competitive Landscape

The India semiconductor market is moderately fragmented; global leaders such as Intel, Samsung, Qualcomm, and MediaTek operate extensive design centers, while domestic challengers, including Tata Electronics, Mindgrove Technologies, and Cyient-Azimuth, target niche, high-growth pockets. Tata Electronics, in partnership with Powerchip Semiconductor Manufacturing Corporation, is investing INR 910 billion (USD 10.9 billion) to build the country’s first high-volume 300-millimeter fab, shifting the competitive field from pure design to integrated manufacturing.

Micron Technology’s Sanand facility sets a benchmark for domestic packaging, yet the lack of sub-10-nanometer foundry capacity forces fabless startups to tape out overseas, thereby sustaining their dependency on Taiwanese and South Korean foundries. The Design Linked Incentive program sweetens the economics of gallium nitride and silicon carbide IP development, encouraging local firms to pursue wide-bandgap opportunities that multinationals do not.

Emerging disruptors are seizing open-source RISC-V architectures to bypass licensing costs. Mindgrove launched India’s first homegrown microcontroller in September 2025, while Cyient-Azimuth’s forthcoming power SOC caters to electric two-wheelers. Compliance hurdles, including ISO 9001 certification and environmental clearances under water and air pollution acts, favor incumbents with established quality systems, though Semicon 2.0 talks suggest richer incentives could soon entice additional 5-7-nanometer proposals.

India Semiconductor Industry Leaders

Tata Electronics Pvt Ltd

Vedanta-Foxconn Semiconductor Ltd.

MosChip Semiconductor Tech

Bharat Electronics Ltd

Applied Materials India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tata Electronics completed land acquisition for its INR 910 billion (USD 10.9 billion) 300-millimeter fab in Dholera and began site preparation for mid-2027 production.

- November 2025: Cyient and Azimuth launched the ARKA GKT-1 power SOC, with commercial volumes planned for mid-2026.

- October 2025: IIT Madras announced a 7-nanometer SHAKTI processor targeting 2028 deployment.

- September 2025: ARM opened a 2-nanometer design office in Bengaluru focused on AI accelerators.

- September 2025: Intel inaugurated a parallel 2-nanometer center in Bengaluru, expanding its Indian workforce to over 13,000 engineers.

India Semiconductor Market Report Scope

The India Semiconductor Market Report is Segmented by Device Type (Discrete Semiconductors, Optoelectronics, Sensors and MEMS, Integrated Circuits), Integrated Circuit Type (Analog, Micro, Logic, Memory), Technology Node (Less Than or Equal to 3nm, 5nm, 7nm, 16nm, 28nm, Greater Than 28nm), End-User Industry (Automotive, Communication, Consumer Electronics, Industrial, Computing, Data Center, AI, Government). Market Forecasts are Provided in Terms of Value (USD).

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifiers and Thyristors | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Optoelectronic Devices | |||

| Sensors and MEMS | Pressure Sensors | ||

| Magnetic Field Sensors | |||

| Actuators | |||

| Acceleration and Yaw Rate Sensors | |||

| Temperature and Other Sensors | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (For Integrated Circuits) | Less Than or Equal to 3nm | ||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| Greater Than 28nm | |||

| Automotive |

| Communication (Wired and Wireless) |

| Consumer Electronics |

| Industrial |

| Computing and Data Storage |

| Data Center |

| Artificial Intelligence |

| Government (Aerospace and Defense) |

| By Device Type | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifiers and Thyristors | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Optoelectronic Devices | ||||

| Sensors and MEMS | Pressure Sensors | |||

| Magnetic Field Sensors | ||||

| Actuators | ||||

| Acceleration and Yaw Rate Sensors | ||||

| Temperature and Other Sensors | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (For Integrated Circuits) | Less Than or Equal to 3nm | |||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| Greater Than 28nm | ||||

| By End-User Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer Electronics | ||||

| Industrial | ||||

| Computing and Data Storage | ||||

| Data Center | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

What is the projected value of the India semiconductor market in 2031?

It is forecast to reach USD 17.42 billion by 2031, growing at a 7.02% CAGR during 2026-2031.

Which device category is expected to record the fastest growth?

Laser diodes, within optoelectronics, are projected to expand at an 8.02% CAGR through 2031 as data-center networks upgrade.

Why is automotive demand rising faster than other end-user segments?

Electric-vehicle adoption and advanced driver-assistance features are doubling semiconductor content per vehicle, driving an 8.66% CAGR in automotive demand.

Which Indian region is likely to see the quickest semiconductor revenue growth?

West India, led by Gujarat’s new wafer fab and packaging plants, is projected to grow through 2031.

How are government incentives shaping local fabrication?

Production Linked Incentive and Design Linked Incentive schemes reduce capital costs by up to 50%, enabling greenfield fabs such as Tata Electronics’ 300-millimeter facility in Dholera.

Page last updated on: