Mexico Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

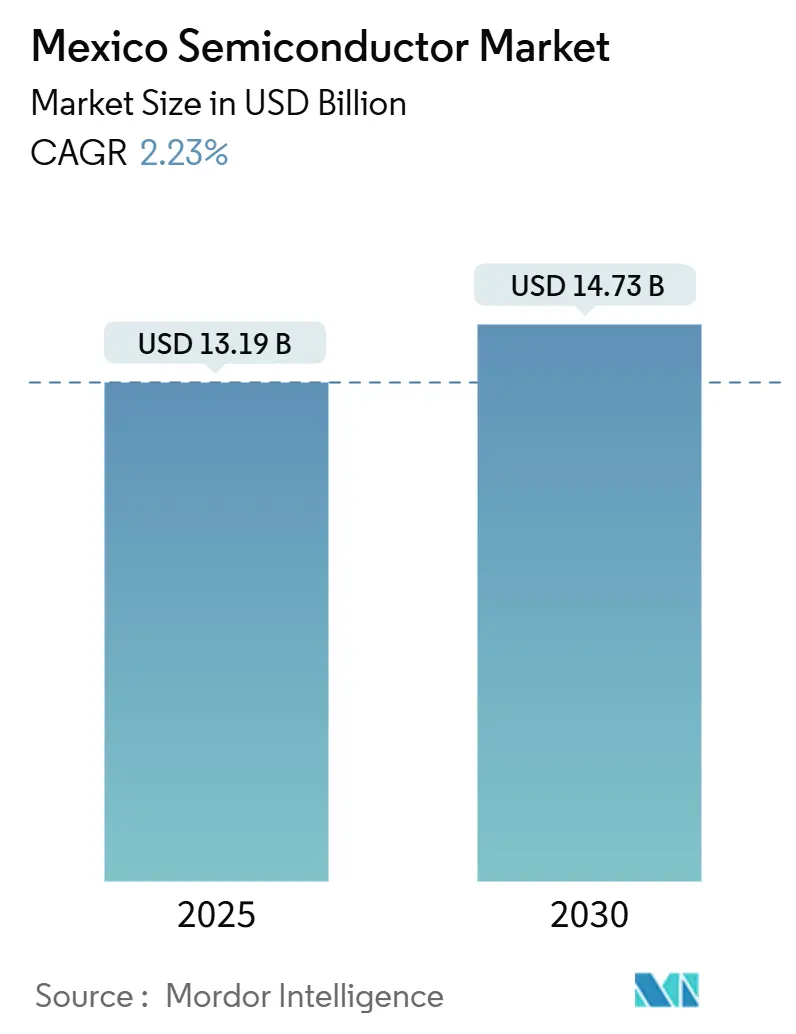

| Market Size (2025) | USD 13.19 Billion |

| Market Size (2030) | USD 14.73 Billion |

| Growth Rate (2025 - 2030) | 2.23% CAGR |

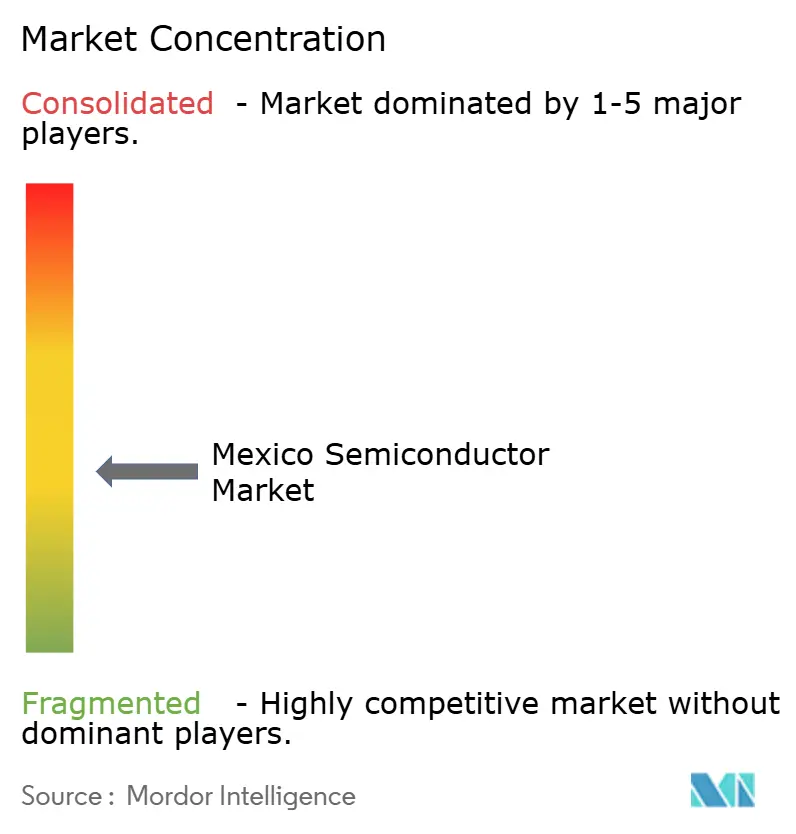

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Semiconductor Market Analysis by Mordor Intelligence

The Mexico semiconductor market size reached USD 13.19 billion in 2025 and is forecast to climb to USD 14.73 billion by 2030, reflecting a 2.23% CAGR. Measured growth stems from Mexico’s pivot from cost-focused assembly toward design-centric capabilities, highlighted by the February 2025 opening of the Kutsari National Semiconductor Design Center. Foxconn’s USD 900 million commitment to manufacture Nvidia GB200 superchips in Guadalajara positions the Mexico semiconductor market as North America’s bridge for AI hardware production. Near-shoring incentives under USMCA and the CHIPS-Plus Act, surging electric-vehicle output, and accelerated 5G roll-outs lift domestic demand even as chronic water and grid constraints temper the growth ceiling. The market’s fragmented competitive field creates white-space opportunities in mature-node production aligned with automotive and industrial requirements, while sustained expansion hinges on coordinated public-private infrastructure investments rather than traditional tax holidays.

Key Report Takeaways

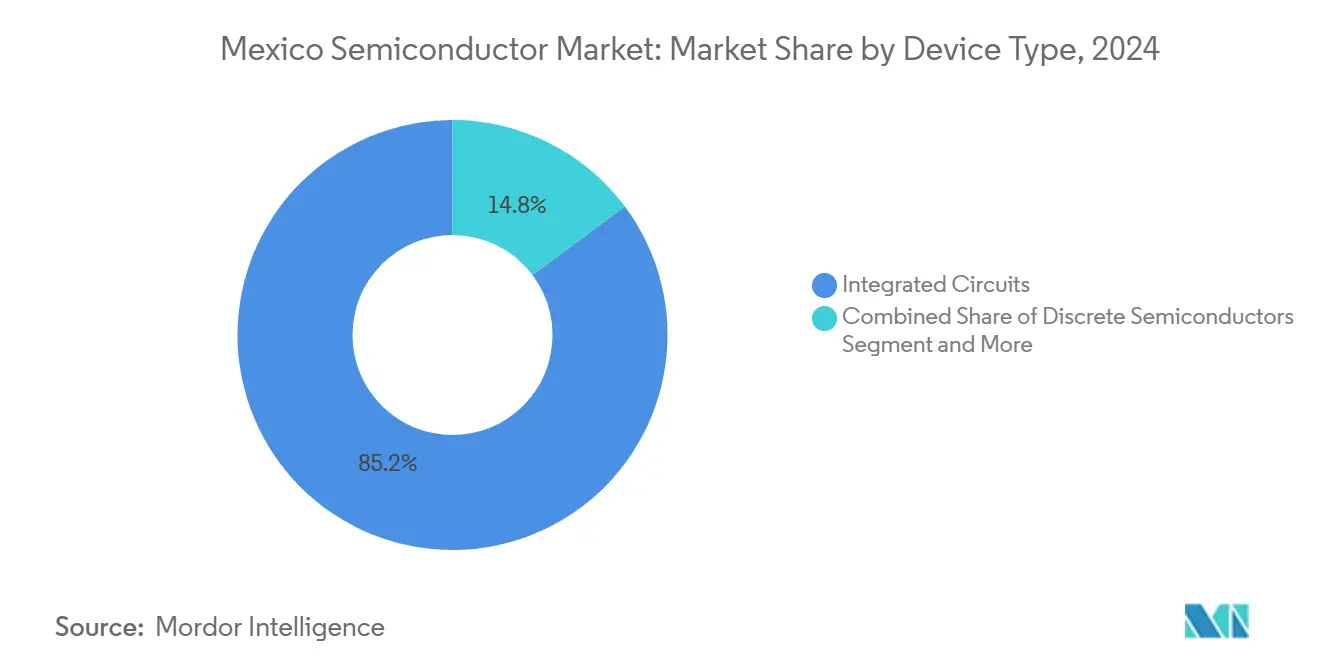

- By device type, integrated circuits led with an 85.22% revenue share of the Mexico semiconductor market in 2024; sensors and MEMS are projected to expand at a 3.8% CAGR through 2030.

- By business model, the IDM segment captured 58.3% of the Mexico semiconductor market share in 2024, while design/fabless vendors are on track for a 3.1% CAGR to 2030.

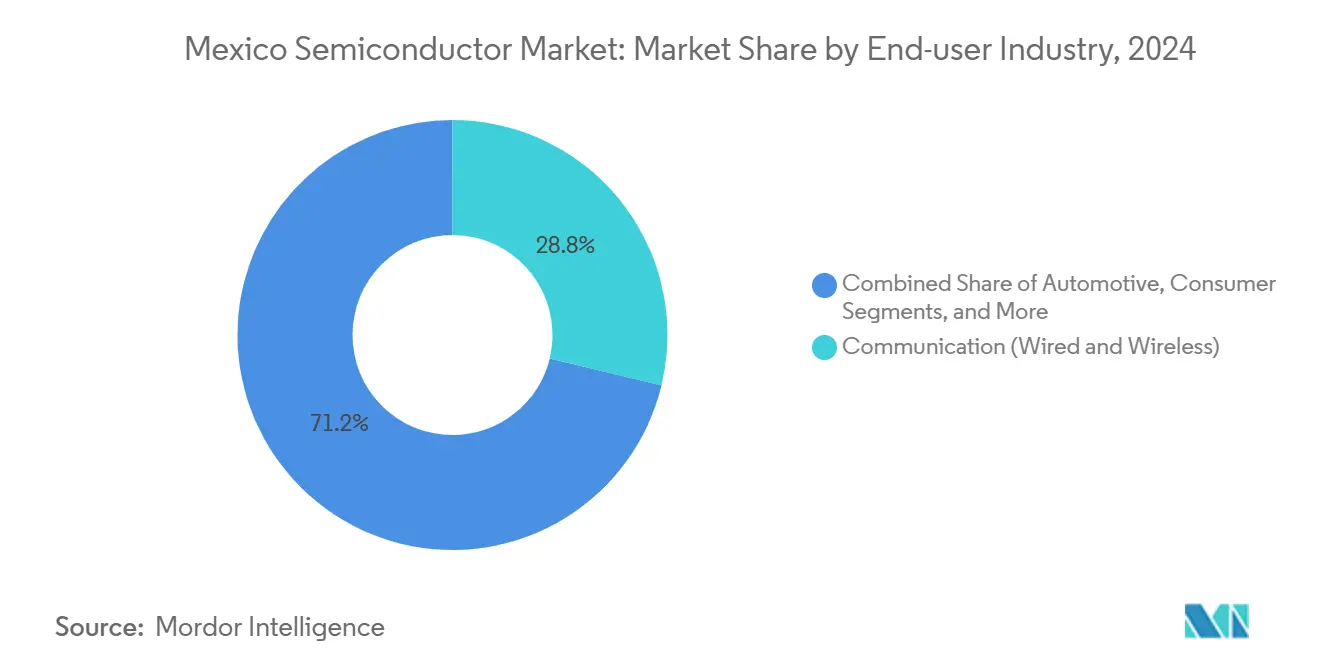

- By end-user industry, communication applications accounted for 28.77% of the Mexico semiconductor market size in 2024, and artificial-intelligence demand is advancing at a 4% CAGR through 2030.

Mexico Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring incentives under USMCA and CHIPS-Plus Act | +0.8% | North America (Jalisco, Sonora, Baja California) | Medium term (2-4 years) |

| Electrification of Mexico-based automotive supply chain | +0.6% | Bajío, Nuevo León, Puebla | Long term (≥ 4 years) |

| 5G and fibre-backhaul roll-outs | +0.4% | Major metropolitan areas | Short term (≤ 2 years) |

| Consumer-electronics rebound | +0.3% | Tijuana, Guadalajara | Short term (≤ 2 years) |

| Kutsari design-center program | +0.2% | Puebla, Jalisco, Sonora | Long term (≥ 4 years) |

| Jalisco-Sonora critical-minerals clusters | +0.1% | Jalisco and Sonora | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-shoring incentives under USMCA and CHIPS-Plus Act

USMCA duty-free provisions and CHIPS-Plus supply-chain requirements allow companies to move wafer-level inputs across borders without tariff friction, cutting lead times and costs for the Mexico semiconductor market. [1]Baker McKenzie, “Mexico: Foreign Trade General Rules for 2025,” bakermckenzie.com Plan México targets a 15% local-content boost, and the North American Semiconductor Conference prioritizes trilateral resilience, encouraging firms to re-anchor back-end assembly in Jalisco while routing advanced lithography to U.S. fabs. The policy mix fosters medium-term expansion yet introduces 2026 USMCA-review uncertainty that may restrain multiyear capex commitments.

Electrification of Mexico-based automotive supply chain

Electric-vehicle production jumped from 6,717 units in 2020 to 109,695 in 2023, and automakers project 161,000 units in 2024, multiplying the silicon content per vehicle. BMW’s USD 800 million battery-pack plant in San Luis Potosí underscores mounting demand for power-management ICs, while Sonora’s lithium reserves add local sourcing leverage. Long development cycles mean semiconductor orders track model-year ramps, locking in steady long-term volumes for the Mexico semiconductor market.

5G and fibre-backhaul roll-outs lifting RF and power devices demand

Telcel’s 5G service now blankets 125 cities and more than 10 million subscribers, while the IFT-12 spectrum auctions release 2,223 blocks to expand coverage. Enterprise 5G pilots at CEMEX’s testbed illustrate industrial-IoT demand for edge-AI accelerators and power-efficient RF components. Limited 31.5% population coverage leaves a long runway, sustaining device demand over the short term and unlocking automation-driven orders in manufacturing hubs as coverage widens.

Consumer-electronics rebound post-2024 downturn

Mexico shipped USD 103 billion in electronics to the United States in 2023, and FDI inflows of USD 206 million to electronics assembly through September 2023 set the stage for capacity add-ons in Baja California. Gen-Z’s preference for high-spec devices raises silicon content per unit, while the Programa Mi Compu.Mx laptop initiative underpins baseline demand. Tariff risk could raise semiconductor input costs by 20%, injecting volatility into near-term revenue for the Mexico semiconductor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic skills gap in sub-10 nm process engineering | –0.7% | National (advanced hubs) | Long term (≥ 4 years) |

| Grid instability and water scarcity | –0.5% | Queretaro, parts of Jalisco and Sonora | Medium term (2-4 years) |

| Rising cartel-related security surcharges | –0.3% | Cross-border routes | Short term (≤ 2 years) |

| Long patent-grant lead-time | –0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic skills gap in sub-10 nm process engineering

Mexico graduates 130,000 engineers yearly, yet only a fraction possess advanced lithography expertise. Arizona State University’s binational microelectronics curriculum registered 10,000 Mexican enrollees, but the hands-on mastery needed for extreme-ultraviolet processes still accrues overseas. [2]Arizona State University, “Opportunities in ASU-Mexico Partnership Equip Talent for North American Microelectronics Jobs,” asu.edu The mismatch confines the Mexico semiconductor industry to mature-node niches, capping upside for leading-edge fabs.

Grid instability and water scarcity near key tech parks

Queretaro faces a projected 23 million-cubic-meter water shortfall by 2030, while 76% of its systems exhibit contamination issues. Semiconductor fabs demand up to 10 million gallons daily and uninterrupted power; current infrastructure forces investors to fund costly on-site treatment and backup generation, inflating total landed costs for the Mexico semiconductor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Dominate Value Chain

Integrated circuits captured an 85.22% share of the Mexico semiconductor market size in 2024, buoyed by automotive, AI server, and 5G infrastructure orders. Foxconn’s superchip program exemplifies the shift from commodity assembly to data-center-grade packaging. Sensors and MEMS lead growth at a 3.8% CAGR, fed by electric-vehicle battery-management systems and industrial IoT retrofits. Discrete semiconductors remain essential for power conversion in EV drivetrains, while optoelectronics find niches in automotive lighting and fiber backhaul. Multiple Jalisco plants now co-locate IC and MEMS lines, shortening supply cycles for the Mexico semiconductor market.

The segment’s outlook depends on sustained EV penetration and AI cloud demand. Should water-recycling upgrades materialize, integrated-circuit fabs could scale beyond today’s mature nodes. Conversely, any slip in grid reliability would shift complex back-end orders to U.S. or Asian facilities, relegating domestic plants to low-margin SKUs. The strategic emphasis on joint university-IDM R&D aims to future-proof device-mix resilience within the Mexico semiconductor market.

By Business Model: IDM Leadership Faces Design-House Challenge

IDMs held 58.3% of the Mexico semiconductor market share in 2024, leveraging vertically integrated cost control and proximity to U.S. tier-1 customers. Fabless houses grew 3.1% CAGR, accelerated by Kutsari-backed ASIC incubators. Contract foundry options remain offshore, so Mexican fabless firms must navigate long supply chains for wafer starts, elevating cycle-time risk. Still, a design-heavy talent pool emerging from Guadalajara universities positions fabless ventures to climb the value curve without billion-dollar capex.

Over the medium term, co-located packaging sites could lower die-to-package transit, tipping economics toward fab-lite hybrids. Multinationals are already carving out Mexico-centric design teams for automotive and medical ASICs. If national patent-processing reforms shorten IP cycles, design-house penetration could erode IDM share, reshaping the competitive narrative of the Mexico semiconductor market.

By End-user Industry: Communication Leads While AI Accelerates

Communication equipment accounted for 28.77% of the Mexico semiconductor market size in 2024, fueled by 5G radio units and optical-transport builds. Artificial-intelligence servers show the fastest 4% CAGR through 2030 as data-center operators source GB200-based systems domestically. Automotive electrification sustains a rising power-device baseline, while industrial automation upgrades pull demand for sensors and control ASICs.

Looking forward, AI workloads could exceed telecom silicon volumes by decade-end if hyperscalers anchor additional GPU clusters in Guadalajara. Communication demand will remain steady, yet margin tailwinds favor AI accelerators requiring high-layer packaging skills. That shift underpins supplier diversification strategies throughout the Mexico semiconductor market.

Geography Analysis

Jalisco captures roughly 70% of semiconductor establishments and anchors USD 890 million in pledged Silicon Valley capital for 2025. Guadalajara’s airport and dense university network feed talent supply and logistics velocity, supporting Foxconn’s superchip complex and ASE Technology’s new packaging hub. Favorable state incentives and cluster density shorten time-to-scale for new entrants, making Jalisco the clear fulcrum of the Mexico semiconductor market.

Sonora leverages lithium reserves and a renewable-energy roadmap to entice power-device makers under the Plan Sonora sustainable-energy push. [3]Codeso, “Plan Sonora de Energías Sostenibles y la Prosperidad Compartida,” codeso.mx Cross-border proximity to Arizona’s fabs enables wafer swap agreements, embedding Sonora in a two-way North American flow of substrates and finished ICs. Baja California exploits near-shore PCBA heritage in Tijuana and Mexicali, expecting 35% growth in electronics production as U.S. OEMs reroute orders from Asia.

Emerging poles in Nuevo León, Puebla, and Queretaro receive Plan México incentives, yet water scarcity and grid instability could derail scale-up unless the USD 3 billion national water-treatment program shifts toward fab-grade infrastructure. [4]International Trade Administration, “Mexico – Environmental Technologies,” trade.gov Ciudad Juárez’s 60-hectare San Jerónimo pole unlocks border-adjacent real estate and tax breaks, but security surcharges on logistics add 8–12% to transit costs, pinching factory margins. The overall geographic dispersion cushions risk for the Mexico semiconductor market while underscoring the necessity of synchronized infrastructure execution.

Competitive Landscape

Mexico’s semiconductor arena remains moderately fragmented; top global suppliers run specialized cells rather than end-to-end fabs, leaving integration gaps ripe for local entrants. Intel, Infineon, Texas Instruments, and NXP defend share via embedded customer relationships and captive test lines, whereas QSM Semiconductors’ USD 12 million wafer plant epitomizes niche challengers seeking mature-node footholds. Market barriers—capital intensity, process IP, and talent scarcity—contain competitive sprawl, keeping rivalry tempered.

Strategic positioning skews toward specialization. Foxconn’s alliance with Nvidia unlocks AI server economics, while ASE Technology’s packaging gambit slashes delivery lead times to U.S. datacenters. White-space remains in 65 nm-plus nodes for automotive and industrial chips, where Asian fabs dominate today. Successful public-private infrastructure coordination could turn that gap into a defensible Mexican advantage, reinforcing the Mexico semiconductor market’s role in North American resiliency.

Consolidation talk centers on vertical tie-ups rather than horizontal M&A. IDMs eye partnerships with local design houses to secure low-cost ASIC talent, and mining-energy conglomerates explore wafer-grade input ventures. If these joint plays take hold, the Mexico semiconductor market could migrate from fragmented to moderately concentrated by decade-end.

Mexico Semiconductor Industry Leaders

Intel Technology de México, S. de R.L. de C.V.

Infineon Technologies de México, S.A. de C.V.

Texas Instruments de México, S. de R.L. de C.V.

ON Semiconductor México, S. de R.L. de C.V.

NXP Semiconductors México, S. de R.L. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ciudad Juárez joined Plan México as a semiconductor-focused development pole offering reduced income-tax rates and expedited permits.

- April 2025: Foxconn announced GB200 NVL72 data-center server production for Project Stargate, boosting Nvidia’s Mexico sales by 300%.

- March 2025: Hon Hai completed plans for a USD 900 million AI server assembly plant near Guadalajara, backed by local incentives.

- February 2025: Mexico launched the Kutsari National Semiconductor Design Center to cut reliance on USD 24 billion in annual chip imports.

- January 2025: President Claudia Sheinbaum unveiled Plan México, aiming for 15% local-content gains across global value chains with semiconductors as a flagship sector.

- December 2024: Silicon Valley investors pledged USD 890 million for the 2025 Jalisco projects.

Mexico Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

How large is the Mexico semiconductor market in 2025?

It stands at USD 13.19 billion with a projected rise to USD 14.73 billion by 2030.

Which device category dominates chip revenue in Mexico?

Integrated circuits generated 85.22% of 2024 value, far ahead of sensor, discrete, and optoelectronic lines.

Where are most Mexican semiconductor facilities located?

About 70% of companies cluster around Guadalajara in Jalisco, supported by Sonora and Baja California satellites.

What is the fastest-growing end-user segment?

Artificial-intelligence servers lead with a forecast 4% CAGR through 2030, fueled by Foxconn’s Nvidia projects.

How do infrastructure issues affect chip investors?

Water scarcity and grid instability raise capital outlays for self-sufficient utilities, trimming cost advantages.

What policy incentives support near-shoring?

USMCA duty-free rules and CHIPS-Plus supply-chain credits lower tariff friction and spur North American integration.

Page last updated on: