Indonesia Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

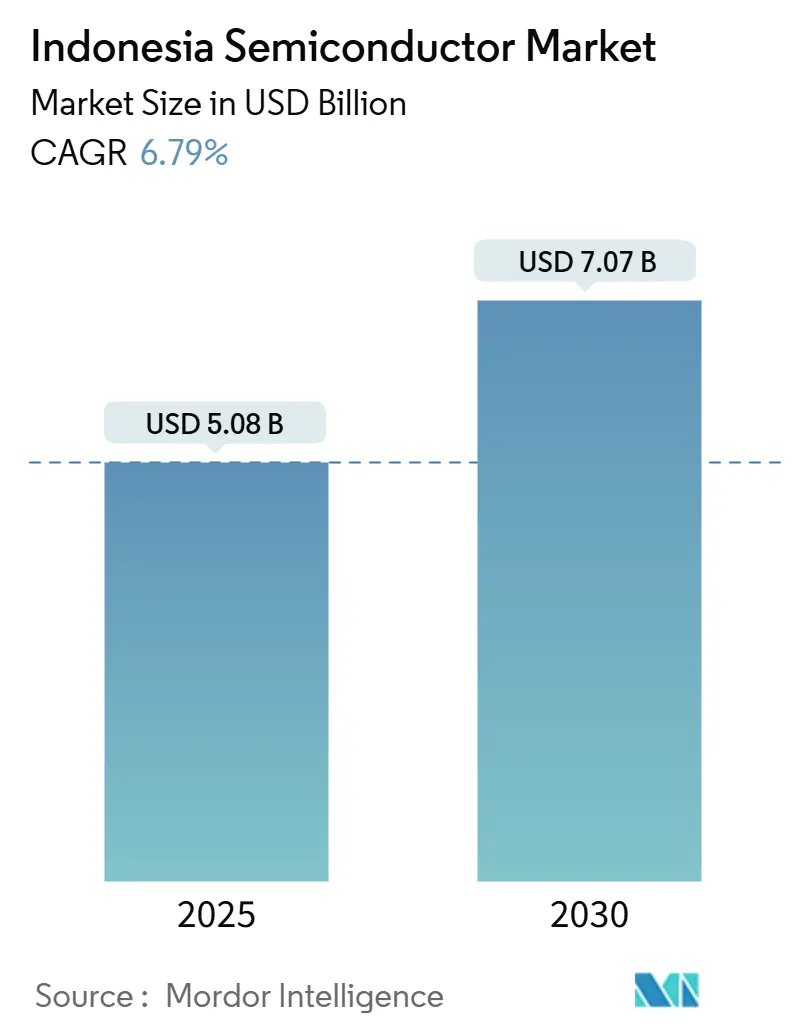

| Market Size (2025) | USD 5.08 Billion |

| Market Size (2030) | USD 7.07 Billion |

| Growth Rate (2025 - 2030) | 6.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Semiconductor Market Analysis by Mordor Intelligence

The Indonesia semiconductor market size reached USD 5.08 billion in 2025 and is forecast to climb to USD 7.07 billion by 2030, reflecting a 6.79% CAGR over the period. This momentum rests on Indonesia’s deep raw-material advantage in nickel and silica, the government’s downstreaming rules that favor domestic value addition, and a steady pipeline of foreign direct investment. Integrated circuit assembly and test operations dominate current revenues, yet the fastest demand acceleration is occurring in sensors, MEMS, and power devices used in electric vehicles and renewable-energy infrastructure. Large global manufacturers are scaling local capacity to secure supply-chain resilience, while a new wave of fabless startups is emerging around Jakarta and Bandung to address edge-AI and IoT niches. Investor interest remains high despite lingering uncertainty over local-content thresholds and foreign-investment screening, signaling a healthy opportunity landscape for technology transfer and joint ventures.

Key Report Takeaways

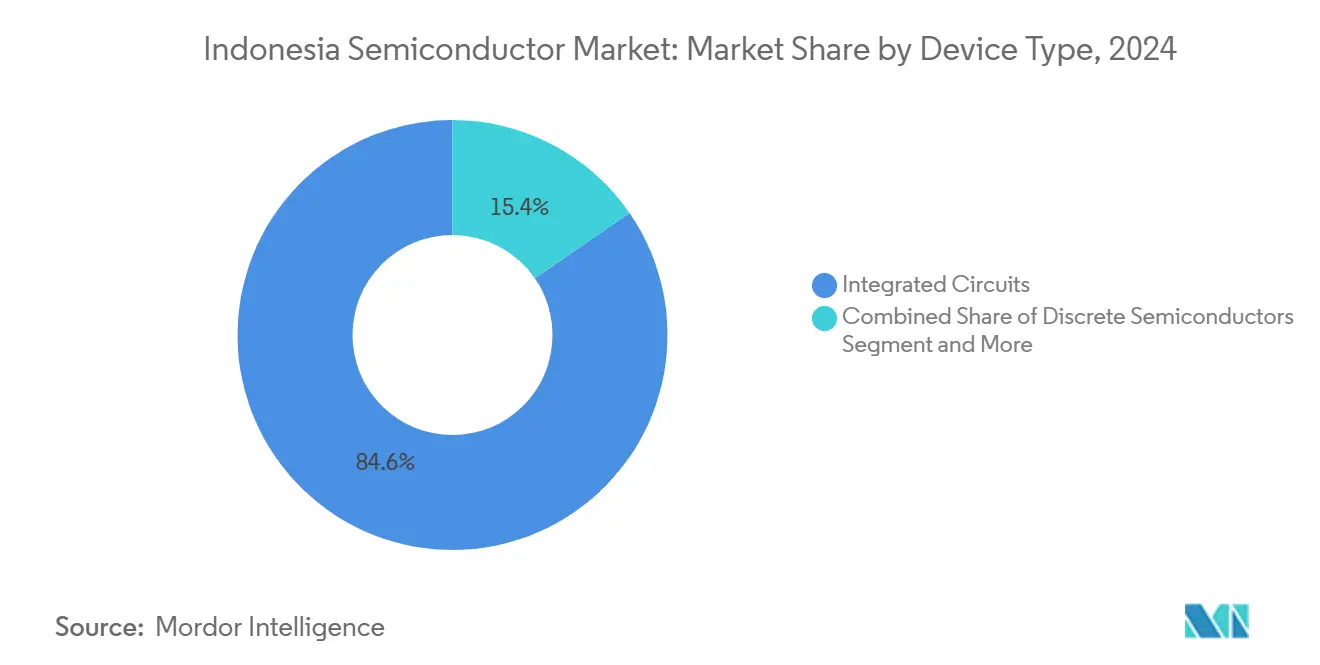

- By device type, integrated circuits held 84.6% of Indonesia semiconductor market share in 2024, while sensors and MEMS are projected to expand at an 8.1% CAGR through 2030.

- By business model, the IDM segment accounted for 58.3% of the Indonesia semiconductor market size in 2024; design/fabless vendors are expected to grow at a 7.9% CAGR between 2025 and 2030.

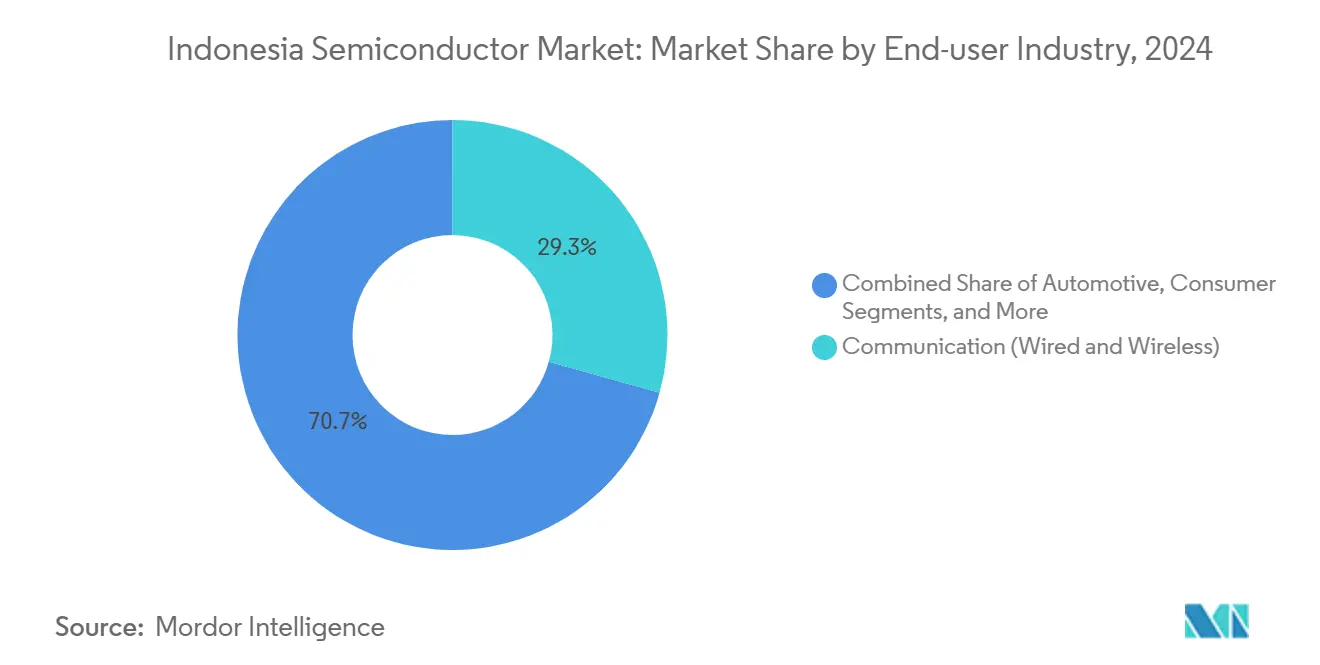

- By end-user industry, communication applications led with a 29.33% revenue share of the Indonesia semiconductor market in 2024, whereas AI-driven applications are advancing at an 8.3% CAGR to 2030.

Indonesia Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives and silica-downstreaming roadmap | +1.8% | National, with concentration in Java and Batam | Long term (≥ 4 years) |

| Surge in domestic consumer-electronics and smartphone demand | +1.2% | National, with urban concentration in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| EV and e-mobility push boosting power-device consumption | +1.0% | National, with manufacturing hubs in Java and Sumatra | Medium term (2-4 years) |

| 5G rollout and hyperscale data-centre build-out | +0.9% | National, with primary deployment in Greater Jakarta | Short term (≤ 2 years) |

| Emergence of local edge-AI startups driving accelerator uptake | +0.7% | National, with tech ecosystem concentration in Jakarta and Bandung | Medium term (2-4 years) |

| Export ban on raw silica sand spurring wafer-fab investment | +0.6% | National, with processing facilities in Java and Kalimantan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government incentives and silica-downstreaming roadmap

Indonesia mandates in-country processing of strategic minerals, including silica and nickel, to capture higher value addition before export. The Ministry of Industry projects USD 45.74 billion in silica-based investments by 2040; twenty-one processors already handle 738,536 t of sand annually at 68.48% utilization. [1]“ESDM Catat Ada 21 Perusahaan Pengolahan Pasir Silika,” KONTAN, kontan.co.id A full export ban on raw silica sand slated for 2027 is designed to force technology transfer into wafer fabrication and encourage integrated device manufacturing. Early responses from multinationals suggest a willingness to co-invest in processing facilities, leveraging Indonesia’s 42.3% share of global nickel reserves to build a vertically aligned supply base.

Surge in domestic consumer-electronics and smartphone demand

Rising disposable income among Indonesia’s 280 million population is fueling brisk sales of smartphones and household electronics. Samsung launched Galaxy S25 with 37.5% local content, surpassing the 35% threshold and shipping 1.56 million units from its Cikarang plant during 2024. Government programs under “Making Indonesia 4.0” accelerate digital adoption, spurring consistent demand for logic ICs, display drivers, and power-management chips. This domestic volume base stabilizes cash flows for manufacturers and justifies new assembly lines that also serve wider ASEAN markets.

EV and e-mobility push boosting power-device consumption

Indonesia aims to assemble 600,000 electric vehicles annually by 2030, offering luxury-tax exemptions and import-duty waivers through 2025 to entice OEMs. Large-scale projects include a USD 6 billion investment by Contemporary Amperex Technology, while policy volatility was underscored by LG Energy Solution’s withdrawal from a USD 8.45 billion battery venture in 2025. EV growth catalyzes demand for silicon-carbide power modules; STMicroelectronics and Semikron are locked in a billion-euro order with a German automaker for modules integrating SiC manufactured in Malaysia and soon Batam.

5G rollout and hyperscale data-centre build-out

Commercial 5G coverage has spread to major cities, and Telkomsel’s 5G Smart Warehouse pilot lifted picking efficiency by 25%. [2]“Telkomsel Enterprise and Huawei’s 5G Smart Warehouse,” GSMA, gsma.com Meanwhile, Oracle committed USD 6.5 billion to a Batam cloud campus and Microsoft pledged USD 1.7 billion for AI-ready capacity, driving robust orders for server CPUs, high-bandwidth memory, and network switches. The data-center market is projected to reach USD 3.63 billion by 2029 at a 5.91% CAGR, further sustaining semiconductor demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute talent gap in advanced IC design and fabrication | -1.5% | National, with critical shortages in Java and Batam industrial zones | Long term (≥ 4 years) |

| Immature domestic supply-chain for specialty gases and tools | -1.2% | National, with particular challenges in outer islands | Medium term (2-4 years) |

| High electricity costs and grid-reliability issues | -0.8% | National, with acute problems outside Java-Bali grid | Short term (≤ 2 years) |

| Regulatory uncertainty in FDI screening slows projects | -0.7% | National, affecting all foreign investment decisions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute talent gap in advanced IC design and fabrication

Local universities currently supply only 20% of the engineers demanded by the semiconductor sector, leaving firms reliant on expatriate talent or overseas training pipelines. Taiwan universities are actively recruiting Indonesian students to fill their own shortages, creating a brain-drain risk. Government scholarships and industry-university consortia are expanding, yet advanced analog-mixed-signal design and AI-accelerator architecture remain scarce skills.

High electricity costs and grid-reliability issues

User surveys show industrial sites suffer 2.6 to 3.9 times more outages than utility data reports, particularly outside Java-Bali. Semiconductor fabs rely on uninterrupted power; many install diesel or gas turbine backup, inflating opex and carbon footprints. The National Energy Policy targets 51.6% renewables by 2030, but until grid stability improves, large fabs remain clustered near the more reliable Java corridor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits sustain leadership while sensors accelerate

Integrated circuits commanded 84.6% of Indonesia semiconductor market share in 2024, underscoring the country’s role as an assembly and test node for automotive, communication, and computing logic. [3]Infineon Technologies, “Infineon to Expand Existing Backend Operations,” infineon.comThe Indonesia semiconductor market size tied to IC back-end services is expected to rise in line with foreign expansions such as Infineon’s Batam capacity upgrade and NXP’s USD 7.8 billion 300 mm JV fab in Singapore that funnels overflow packaging to Indonesia. Discrete devices keep steady volumes in power supplies, while optoelectronics grow with LED rollout across smart-city projects.

Sensors and MEMS are the fastest-growing device class, tracking an 8.1% CAGR to 2030 as IoT proliferation, automotive electrification, and factory automation lift unit demand. MediaTek’s partnership with Meta to optimize on-device generative AI underlines how edge-compute scenarios increase sensor fusion requirements. Local drone makers and agri-tech firms are integrating MEMS IMUs and environmental sensors, supporting a diversified revenue base beyond consumer electronics.

By Business Model: IDM strength faces mounting fabless momentum

IDMs captured 58.3% of Indonesia semiconductor market share in 2024, benefiting from vertically integrated cost control and policy incentives favoring local wafer and packaging investments. STMicroelectronics’ restructuring adds 4,000 300 mm wafers per week in Agrate and launches 200 mm silicon-carbide output in 2025, part of a strategy expected to yield triple-digit million-dollar annual savings. The Indonesia semiconductor market size attributable to IDM output is projected to grow steadily as downstreaming mandates nudge more global majors toward local fabs.

Fabless and design houses are the fastest-expanding cohort at a 7.9% CAGR. Qualcomm’s tie-up with STMicroelectronics couples best-in-class wireless IP with STM32 MCUs, enabling rapid prototyping for local IoT firms. Google Cloud’s accelerator offers up to USD 350,000 in credits for one hundred Indonesian AI startups, fueling demand for tape-out services at foundries in Taiwan and Singapore while anchoring software and IP creation onshore. This ecosystem shift gradually diversifies value capture from manufacturing toward design royalties.

By End-user Industry: Communication remains top but AI surges ahead

Communication equipment absorbed 29.33% of 2024 revenue, driven by 5G base-station rollout and backbone upgrades that rely on RF front-end modules, optical transceivers, and high-speed switch ASICs. The Indonesia semiconductor market size tied to communication hardware is supported by hyperscale capex from Oracle and Microsoft, as well as national projects like the Palapa Ring fiber network. Automotive demand is also rising as EV incentives push the adoption of traction inverters and battery-management ICs.

AI applications represent the fastest-growing end use at an 8.3% CAGR to 2030. Nvidia’s USD 200 million AI center in Solo will supply local cloud service providers with HGX and Grace Hopper systems, accelerating uptake of high-bandwidth memory and GPU accelerators. Open-source Bahasa models such as Sahabat-AI foster demand for inference-optimized SoCs that balance performance and power in edge devices. Consumer electronics, industrial automation, and data-center segments round out a robust multi-industry demand picture.

Geography Analysis

Java and Sumatra anchor most semiconductor activity owing to mature transport links, deep talent pools, and relatively stable power. Greater Jakarta hosts 35 operating data centers, with five hyperscale builds underway in nearby Batam that benefit from its free-trade zone and proximity to Singapore. Apple is negotiating a USD 1 billion AirTag facility in Batam targeting 65% of global output, further entrenching the region’s electronics cluster.

East Java’s first digital substation, installed by Hitachi Energy, enhances grid reliability critical for back-end fabs and SMT lines. Central Java draws AI-focused investment, notably the Solo AI center, leveraging lower labor costs and solid infrastructure. The Indonesia semiconductor market size generated in Java corridors captures the lion’s share of national revenue due to these locational advantages.

Outer islands such as Kalimantan and Sulawesi contribute raw materials—silica sand and nickel—to upstream stages. Kalimantan’s sand reserves and existing processors are pivotal for the planned wafer-fab ecosystem, though firms often invest in self-generation to overcome unreliable grids. Sulawesi’s Morowali Industrial Park hosts battery precursor plants that consume power semiconductors for EV supply chains. Government universal-service programs aim to extend fiber backhaul and stable electricity, potentially unlocking future manufacturing nodes beyond Java.

Competitive Landscape

Indonesia’s semiconductor arena is moderately concentrated. Samsung, Infineon, STMicroelectronics, and Qualcomm together control an estimated mid-60% share, supported by entrenched assembly lines and extensive patent portfolios. Under resource-nationalism rules, these leaders are deepening local supply chains; Samsung already meets 37.5% content on flagship handsets, and STMicroelectronics is upgrading Batam modules to include silicon-carbide final test.

Cost pressures and technology inflection points accelerate strategic shifts toward vertical integration. STMicroelectronics’ Agrate 300 mm ramp and silicon-carbide transition target sizable cost savings while shoring up automotive and industrial margins. [4]StockTitan, “STMicroelectronics Launches Massive Tech Upgrade,” stocktitan.net Nvidia’s collaboration with Indosat provides a reference architecture for sovereign AI clouds, giving the GPU giant an early foothold in Indonesia’s accelerator domain.

White-space opportunities arise for nimble local entrants. Google Cloud’s accelerator injects up to USD 35 million in total credits, enabling start-ups to prototype ASIC or RISC-V designs without heavy capex. Lintasarta’s GPU-as-a-Service, launched in 2025, illustrates how cloud providers can monetize AI demand before domestic wafer capacity scales. As policy clarity improves, both multinational and local firms are expected to intensify joint-venture and technology-licensing deals to secure market positioning.

Indonesia Semiconductor Industry Leaders

PT Sat Nusapersada Tbk

PT Infineon Technologies Batam

PT STMicroelectronics Batam

PT Samsung Electronics Indonesia

PT LG Electronics Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Google Cloud and the Ministry of Communications and Digital Affairs launched the “Indonesia, AI-Focused” accelerator to support 100 start-ups with up to USD 350,000 in credits each, enlarging demand for AI-centric semiconductors.

- April 2025: STMicroelectronics announced a global restructuring, adding 4,000 wafers/week 300 mm capacity and commencing 200 mm SiC production by Q4 2025.

- April 2025: LG Energy Solution exited an USD 8.45 billion Indonesian battery project, citing market conditions.

- April 2025: Apple discussed a USD 1 billion AirTag plant in Batam aimed at 65% global output by Q1 2026.

- November 2024: Nvidia and Indosat expanded their partnership to develop Bahasa Indonesia large-language models under the Sahabat-AI program.

Indonesia Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing/Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

What is the current value of the Indonesia semiconductor market?

The Indonesia semiconductor market size stood at USD 5.08 billion in 2025.

How fast will the market grow over the next five years?

Revenue is projected to expand to USD 7.07 billion by 2030, implying a 6.79% CAGR.

Which device category dominates sales?

Integrated circuits hold 84.6% of 2024 revenue, reflecting Indonesia’s strength in assembly and test operations.

Which segment is growing the quickest?

Sensors and MEMS are advancing at an 8.1% CAGR through 2030, driven by IoT and automotive electrification.

How significant is AI to future chip demand?

AI applications are the fastest-growing end use, with an 8.3% CAGR, supported by major investments such as Nvidias USD 200 million AI center in Solo.

Where are most fabs located?

Java and Batam host the bulk of manufacturing capacity owing to reliable power, skilled labor, and port access.

Page last updated on: