Egypt Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

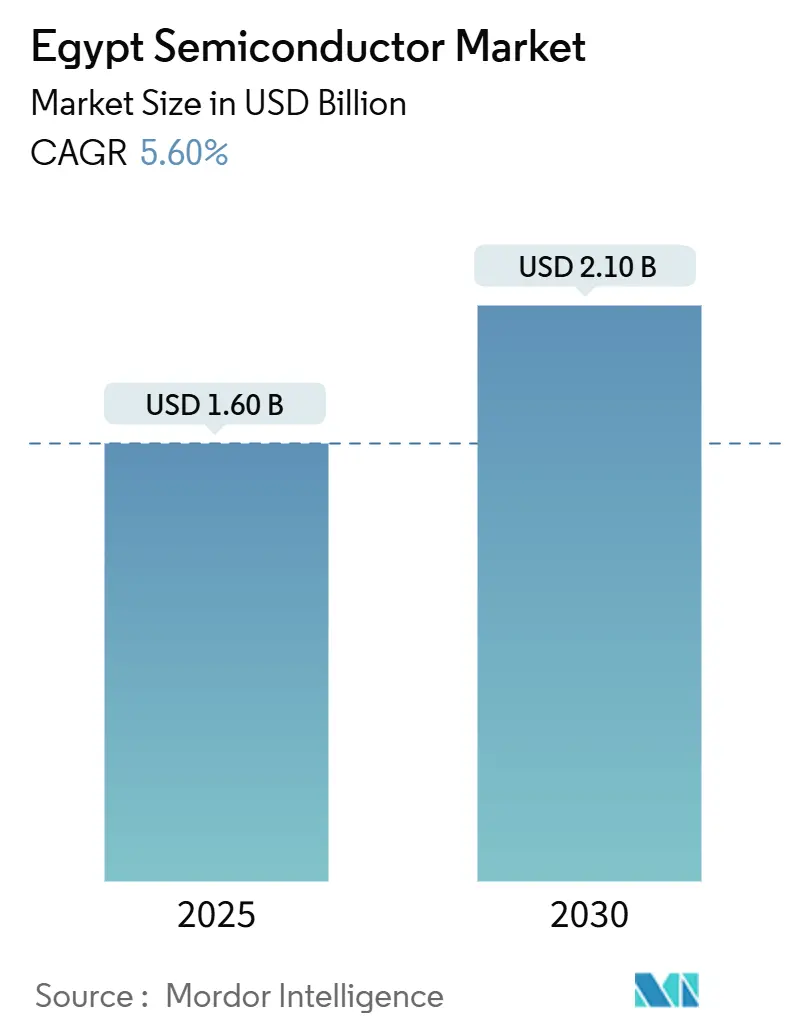

| Market Size (2025) | USD 1.60 Billion |

| Market Size (2030) | USD 2.10 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Semiconductor Market Analysis by Mordor Intelligence

The Egypt semiconductor market size stood at USD 1.60 billion in 2025 and is projected to climb to USD 2.10 billion by 2030, reflecting a 5.60% CAGR across the forecast horizon. Egypt’s Vision 2030 incentives, its role in the African Continental Free Trade Area (AfCFTA), and steadily rising foreign direct investment are reinforcing this growth momentum. Rapid gains in local smartphone assembly, the roll-out of hyperscale data-center projects, and robust demand from renewable-energy installations are widening addressable opportunities for chip vendors. Multinational integrated-device manufacturers (IDMs) continue to anchor the domestic value chain through design centers and board-level assembly agreements, while a nascent fabless ecosystem is emerging around the Smart Village technology park. At the same time, U.S. export controls on advanced lithography tools, intermittent grid reliability outside industrial zones, and hard-currency constraints for capital-equipment imports pose structural headwinds that manufacturers must navigate.

Key Report Takeaways

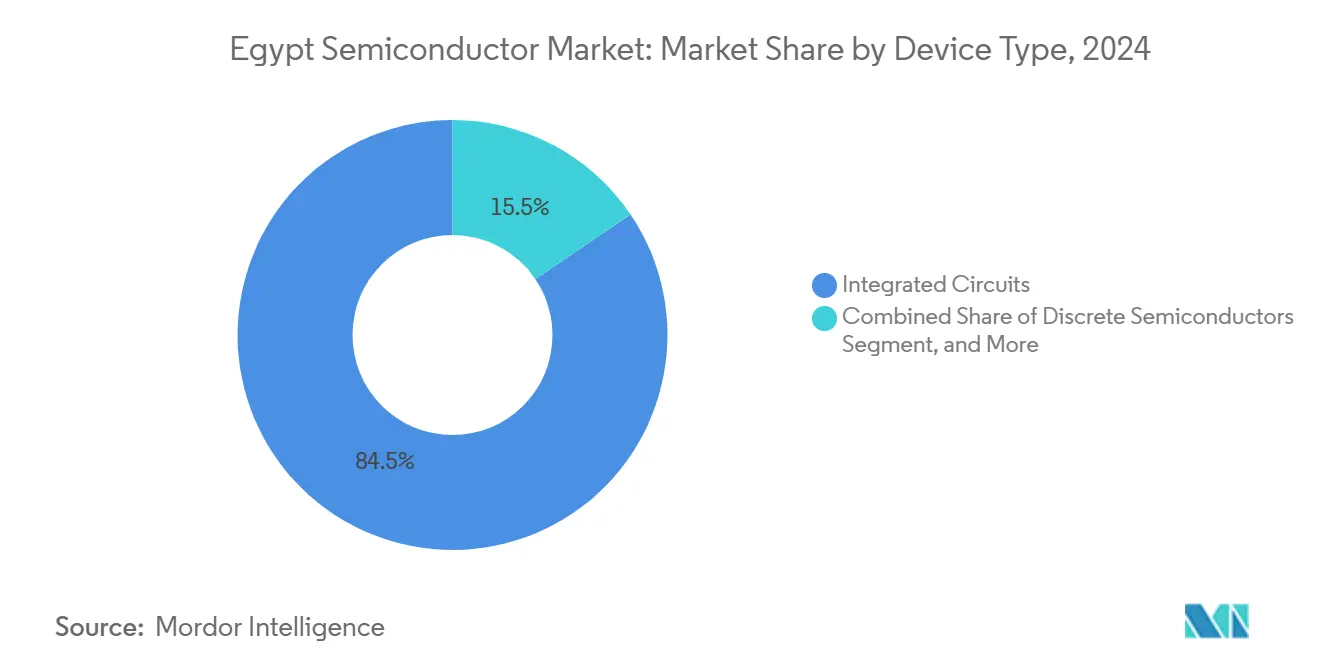

- By device type, integrated circuits accounted for an 84.47% Egypt semiconductor market share in 2024, while Sensors and MEMS are forecast to deliver the fastest growth, advancing at a 7.2% CAGR through 2030.

- By business model, IDM companies held a 68.3% share of the Egypt semiconductor market size in 2024, while the design/fabless segment is set to expand at a 6.6% CAGR to 2030.

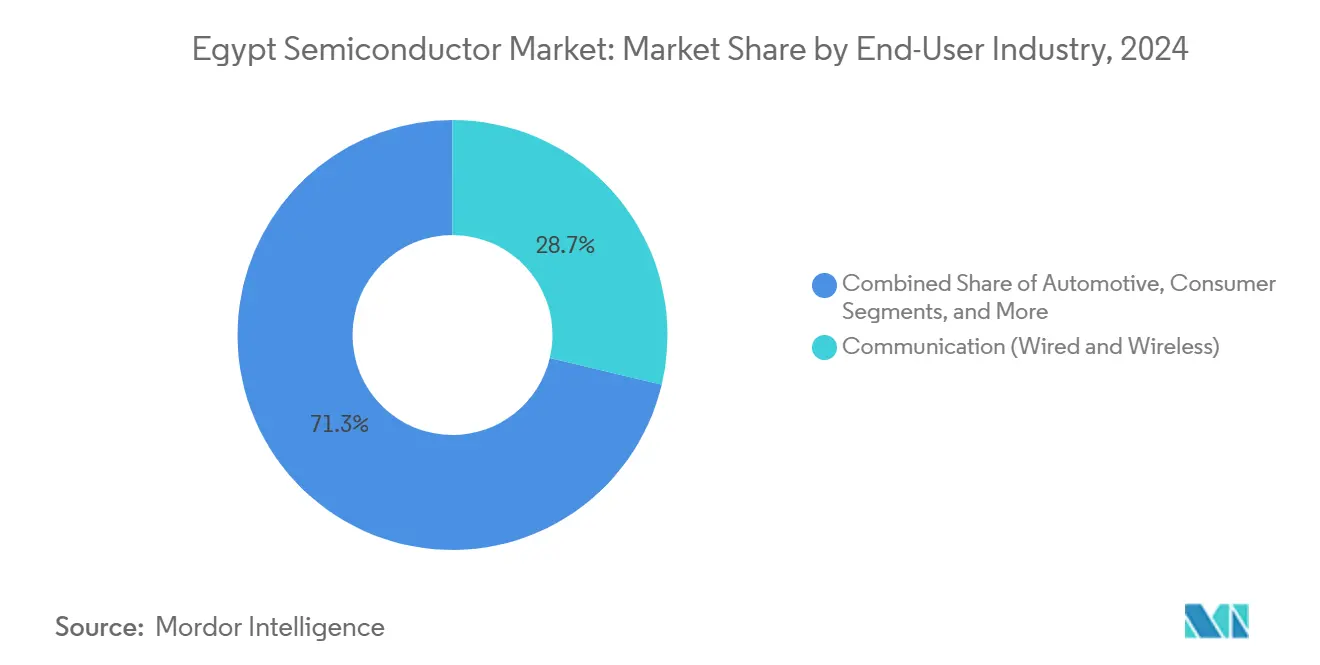

- By end-user, communication applications led with 28.71% of the Egypt semiconductor market share in 2024, whereas artificial-intelligence deployments are poised for a 7% CAGR through 2030.

Egypt Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Egypt Vision 2030 semiconductor incentives | +1.2% | National (Smart Village, industrial zones) | Medium term (2-4 years) |

| Expansion of local automotive-electronics assembly | +0.8% | National (10th of Ramadan, Beni Suef) | Medium term (2-4 years) |

| Utility-scale renewables boosting power-device demand | +0.6% | National (New Administrative Capital, Benban) | Long term (≥ 4 years) |

| Hyperscale and sovereign data-center build-out | +0.9% | National (Smart Village, Suez Canal Economic Zone) | Short term (≤ 2 years) |

| AfCFTA export-tariff advantages for Egypt fabs | +0.4% | Continental Africa | Long term (≥ 4 years) |

| China-Egypt design-house partnerships | +0.7% | National (Smart Village) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government “Egypt Vision 2030” semiconductor incentives

Major policy levers such as tax holidays, subsidized land, and accelerated customs clearance are lowering entry barriers for semiconductor investors. The inauguration of Egypt’s first Government Data and Cloud Computing Center in 2024 created a baseline domestic node with 120 petabytes of capacity, immediately boosting demand for advanced processors and memory chips.[1]Egypt Today, “President Sisi Inaugurates Egypt’s 1st Government Data and Cloud Computing Center,” egypttoday.comA USD 300 million co-investment fund with Tsinghua Unigroup earmarks R&D spending for chip-design facilities, encouraging value-added activities that move Egypt beyond simple board assembly. These incentives dovetail with the Ministry of Communications’ target of lifting the ICT sector’s GDP contribution from 5.8% to 8% by 2030, intensifying chip pull-through across multiple verticals. The policy suite also mandates that private-sector capital contribute 50% of total investment by FY 2024/2025, creating a predictable pipeline for commercial fabs. Collectively, these measures add an estimated 1.2 percentage points to the overall CAGR of the Egypt semiconductor market.

Expansion of local automotive-electronics assembly

Geely Auto’s 30,000-unit CKD plant in Giza, operational since January 2025, deploys laser-welding robots and high-speed SMT lines that rely on microcontrollers, sensors, and power devices. Government cash incentives for EV purchasers, alongside customs-duty exemptions on imported batteries, accelerate demand for battery-management ICs and wide-bandgap power modules. Samsung’s USD 700 million consumer-electronics complex in Beni Suef exports to 55 countries, underlining Egypt’s role as a regional electronics hub that absorbs significant semiconductor content. Local content rules that push EV components to 60% by 2027 incentivize domestic sourcing, driving strategic partnerships between automotive OEMs and fabless chip designers. Together, these developments add roughly 0.8 percentage points to the Egypt semiconductor market’s forecast CAGR.

Hyperscale and sovereign data-center build-out

Telecom Egypt’s Tier III datacenter connects to 10 subsea landing stations, positioning the country as a regional interconnection node and lifting demand for networking ASICs, optical transceivers, and high-density memory. The USD 450 million Kemet Data Center under construction in the Suez Canal Economic Zone will house AI-accelerated cloud services that rely on GPUs, high-bandwidth memory, and specialized inference chips. Huawei Cloud’s first Northern-Africa public-cloud region, launched in 2024, brings AI training workloads onshore and intensifies requirements for advanced server processors. Sovereign compute initiatives such as the G42-Benya partnership amplify specialized chip uptake for defense-grade cryptography. These combined projects add approximately 0.9 percentage points to long-run growth.

Utility-scale renewables boosting power-device demand

The 1.1 GW Obelisk hybrid solar-battery plant integrates 200 MWh of storage, necessitating high-current silicon-carbide MOSFETs and robust gate drivers. Egypt plans to raise renewables’ share of the energy mix from 13% in 2023 to 42% in 2030, multiplying demand for inverter dies, power management ICs, and grid-tie modules. A USD 172 million silicon complex in New Alamein taps 40 million tons of quartz reserves, offering upstream materials for localized wafer starts. ROHM’s 2 kV SiC devices already feature in SMA Solar Technology’s utility systems, confirming that the market is pivoting toward wide-bandgap solutions. Altogether, renewables contribute about 0.6 percentage points to industry CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced lithography export restrictions | −1.8% | Global access to leading-edge tools | Short term (≤ 2 years) |

| Grid-reliability concerns outside industrial zones | −0.7% | National (rural, suburban) | Medium term (2-4 years) |

| Hard-currency shortages for equipment imports | −1.1% | National | Short term (≤ 2 years) |

| Scarcity of senior IC-design talent | −0.9% | Cairo, Alexandria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced lithography export restrictions

The November 2023 U.S. rules classify Egypt as a license-requiring jurisdiction for sub-7 nm tools, photomasks, and EUV scanners, effectively capping domestic fabs at mature technology nodes.[2]Clyde and Co, “U.S. Issues Updated Semiconductor Export Controls Aimed at Intermediary Jurisdictions,” clydeco.com License processing can prolong delivery timelines by up to 12 months, eroding competitiveness in fast-refresh consumer electronics. Restricted access compels local players to rely on overseas foundries for advanced logic dies, diluting the value capture of domestic manufacturing. The constraint subtracts an estimated 1.8 percentage points from forecast CAGR.

Grid-reliability concerns outside industrial zones

Fault-tree analyses reveal voltage sag and frequency instability in regions beyond premium industrial parks, exposing fabs to unplanned downtime and yield loss. While backup diesel and gas turbines mitigate risks, they inflate operating costs by 5-10% for firms situated in Alexandria and Upper Egypt. Government-sponsored transmission-upgrade projects are underway but will not achieve national coverage before 2027. The issue dampens market growth by 0.7 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated circuits sustain dominance amid sensor surge

Integrated circuits retained an 84.47% Egypt semiconductor market share in 2024, supported by datacenter and smartphone assembly projects that ingest high volumes of CPUs, application processors, and DRAM. The Egypt semiconductor market size for integrated circuits is projected to expand in lockstep with hyperscale compute rollouts, while secure-element chips gain traction in government e-ID programs. Microcontroller demand mirrors rising output from appliance and automotive lines, as evidenced by Samsung securing 16 nm MCU orders destined for global handset brands.

Sensors and MEMS, advancing at a 7.2% CAGR, benefit from expanded automotive assembly and industrial automation. Geely’s robotic welding cells require inertial and position sensors, while EV battery-management packs utilize MEMS pressure gauges. Discrete power devices, including SiC MOSFETs, support solar-farm inverters, and optoelectronics capitalize on Egypt’s plan to build the region’s largest fiber-optic cable plant.

By Business Model: IDM control faces a fast-rising fabless cohort

IDMs accounted for 68.3% of the Egypt semiconductor market size in 2024, leveraging captive fabs and local assembly partnerships to navigate currency and customs pressures. Intel’s motherboard line with METRA-BORAQ exemplifies this vertically integrated resilience. However, design-centric houses are scaling quickly: the American University in Cairo’s cloud-based CAD platform slashes design-cycle barriers and spurs startup formation.

Design/fabless vendors—growing at 6.6% CAGR—are riding the USD 300 million China-Egypt fund’s R&D pipeline to tape-out application-specific chips for AI inference and automotive telematics. Si-Ware Systems already grosses USD 20 million annually from spectroscopy and timing devices, showcasing the commercial viability of the fabless pathway.

By End-User Industry: Communication holds the lead while AI accelerates

Communication infrastructure commanded 28.71% of the Egypt semiconductor market share in 2024 on the back of 10 subsea cable landings and aggressive 5G rollout timetables. Local smartphone factories operated by four of the world’s five largest OEMs collectively target 9 million handsets by 2026, bolstering RF-front end and baseband demand.

Artificial-intelligence deployments are forecast to post a 7% CAGR through 2030, propelled by Egypt’s National AI Strategy to train 30,000 specialists and incubate 250 AI-focused firms. Automotive and industrial users add steady volume through EV powertrains and smart-factory retrofits, whereas consumer white-goods lines absorb mixed-signal ASICs and motor-driver ICs.

Geography Analysis

Egypt’s semiconductor value chain is spatially concentrated along four corridors: Smart Village in Cairo, 10th of Ramadan/Beni Suef, the Suez Canal Economic Zone, and New Alamein. Participation in AfCFTA gives fabs domiciled in these zones tariff-free access to a 1.3-billion-person market, and Egypt captured 22% of Africa’s manufacturing value added by 2020.[3]UNCTAD, “Progress on Africa’s Integration Boosts Prospects for Economic Transformation in Egypt,” unctad.org The Suez Canal hub—already home to the USD 450 million Kemet Data Center—offers expedited customs and a purpose-built 500 MW power substation, making it the preferred site for data-center-grade silicon assembly.

Smart Village aggregates chip-design talent, buoyed by the Tsinghua Unigroup-supported R&D center and the national CAD cloud. Industrial power stability inside the 10th of Ramadan attracts smartphone and appliance assembly; Samsung’s USD 700 million campus and Vivo’s 500,000-unit-per-month handset factory are flagship tenants. New Alamein’s quartz-to-silicon plant integrates upstream feedstock, lowering wafer-substrate import dependence. Despite these advantages, uniform export-licensing rules mean no Egypt province can sidestep the advanced-lithography ceiling, underscoring the need for strategic alliances with offshore foundries.

Competitive Landscape

The Egypt semiconductor market exhibits a moderate degree of fragmentation. No single firm controls a significant share of domestic revenue, and the top five vendors collectively hold only a nominal share, positioning the market in a contestable middle ground. Global IDMs such as STMicroelectronics and Intel leverage co-location strategies to pair design hubs with board-level assembly, mitigating logistical and currency-exchange friction. Local champions like Si-Ware Systems and Atoms differentiate by targeting niche applications—near-infrared spectroscopy and AI-enabled verification, respectively—with lighter capital footprints.[4]The FutureList, “Atoms AI Innovation Memo,” thefuturelist.com

Strategic moves in 2025 underline competitive dynamism. ROHM’s SiC device insertion into SMA inverters accelerates Egypt’s adoption of wide-bandgap technologies, pressuring rivals to match efficiency benchmarks. Signify’s joint venture with Gila Al Tawakol Electric for LED fabrication demonstrates lateral integration into optoelectronics while anchoring supply security for regional lighting projects. Education-industry linkages further shape the competitive narrative; for example, the American University in Cairo’s Nanoelectronics Center feeds graduates directly into both multinational and indigenous design houses, easing the talent bottleneck that restrains advanced projects.

Egypt Semiconductor Industry Leaders

Intel Corporation

Samsung Electronics Co., Ltd.

Taiwan Semiconductor Manufacturing Company Limited

STMicroelectronics N.V.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Egypt’s Ministry of Communications confirmed plans to triple local smartphone output to 9 million units by 2026, with four global OEMs committed to factories.

- May 2025: ROHM Semiconductor deployed 2 kV SiC MOSFETs in SMA Solar Technology’s utility-scale PV systems.

- March 2025: Government launched the National AI Strategy (2025-2030), targeting 30,000 trained specialists and 250 AI-centric companies.

- February 2025: Vivo began full-rate production of 500,000 smartphones monthly at its 10th of Ramadan plant.

Egypt Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing/Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

How large is the Egypt semiconductor market in 2025?

The market stands at USD 1.60 billion in 2025 and is projected to reach USD 2.10 billion by 2030.

What is the expected CAGR for Egypts semiconductor sector?

Growth is forecast at 5.60% between 2025 and 2030.

Which device category dominates shipments in Egypt?

Integrated circuits lead with an 84.47% share in 2024, reflecting strong demand from smartphones and data centers.

Which end-user area is expanding fastest?

Artificial-intelligence deployments show the quickest rise, projected at a 7% CAGR through 2030.

How do U.S. export controls affect Egyptian fabs?

Licensing requirements for sub-7 nm tools limit access to advanced lithography, capping Egypts ability to produce leading-edge chips.

What role does AfCFTA play for local semiconductor firms?

Tariff-free access to African markets enhances export competitiveness for assembly and packaging operations based in Egypt.

Page last updated on: