Netherlands Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

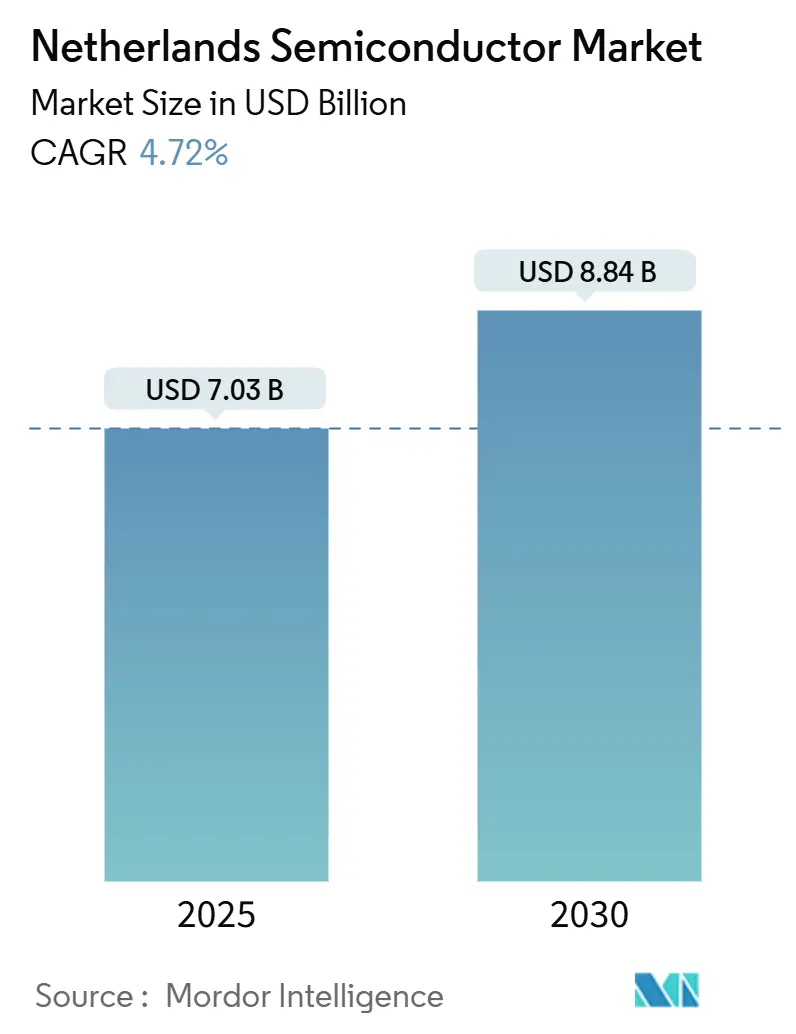

| Market Size (2025) | USD 7.03 Billion |

| Market Size (2030) | USD 8.84 Billion |

| Growth Rate (2025 - 2030) | 4.72% CAGR |

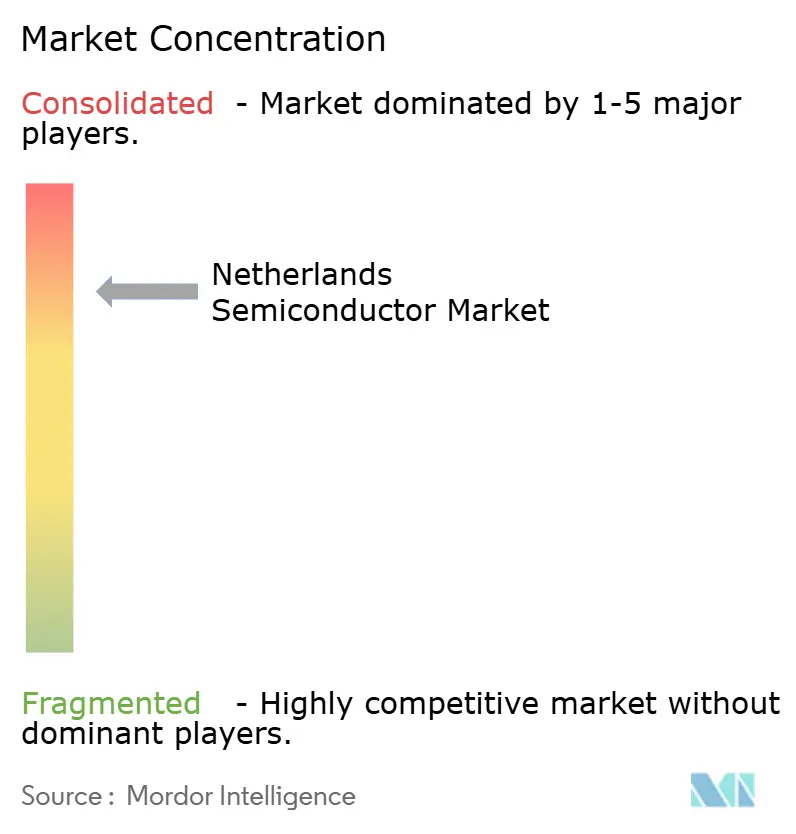

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Semiconductor Market Analysis by Mordor Intelligence

The Netherlands semiconductor market size equals USD 7.03 billion in 2025 and is forecast to reach USD 8.84 billion by 2030, translating into a 4.72% CAGR across the period. Current growth relies on the country’s monopoly in extreme-ultraviolet (EUV) lithography, rapid scale-up of integrated photonics pilots, and sustained public funding that mitigates geopolitical risk. Design-led business models, a transition toward wide-bandgap power devices, and stringent datacenter energy rules further shape revenue visibility. Collectively, these elements keep the Netherlands semiconductor market on a stable mid-single-digit growth path while reinforcing Europe’s strategic autonomy.

Investment incentives anchored in the EUR 2.5 billion (USD 2.75 billion) Project Beethoven program secure local manufacturing services and housing for highly skilled staff. Equipment exports stay resilient even as export licensing tightens, thanks to a deep backlog at leading customers in the United States, the Republic of Korea, and Taiwan. At the same time, shifting vehicle power-train architectures propel demand for silicon-carbide (SiC) and gallium-nitride (GaN) tools, which boost orders for Dutch epitaxy, packaging, and inspection systems. Integrated photonics projects centered in Eindhoven and Enschede open a second growth engine that aligns with national ambitions to lead in energy-efficient data movement. Labor shortages and export-control uncertainty remain the only meaningful drags on the Netherlands semiconductor market, yet ongoing visa simplification and diversified customer portfolios soften their near-term impact.

Key Report Takeaways

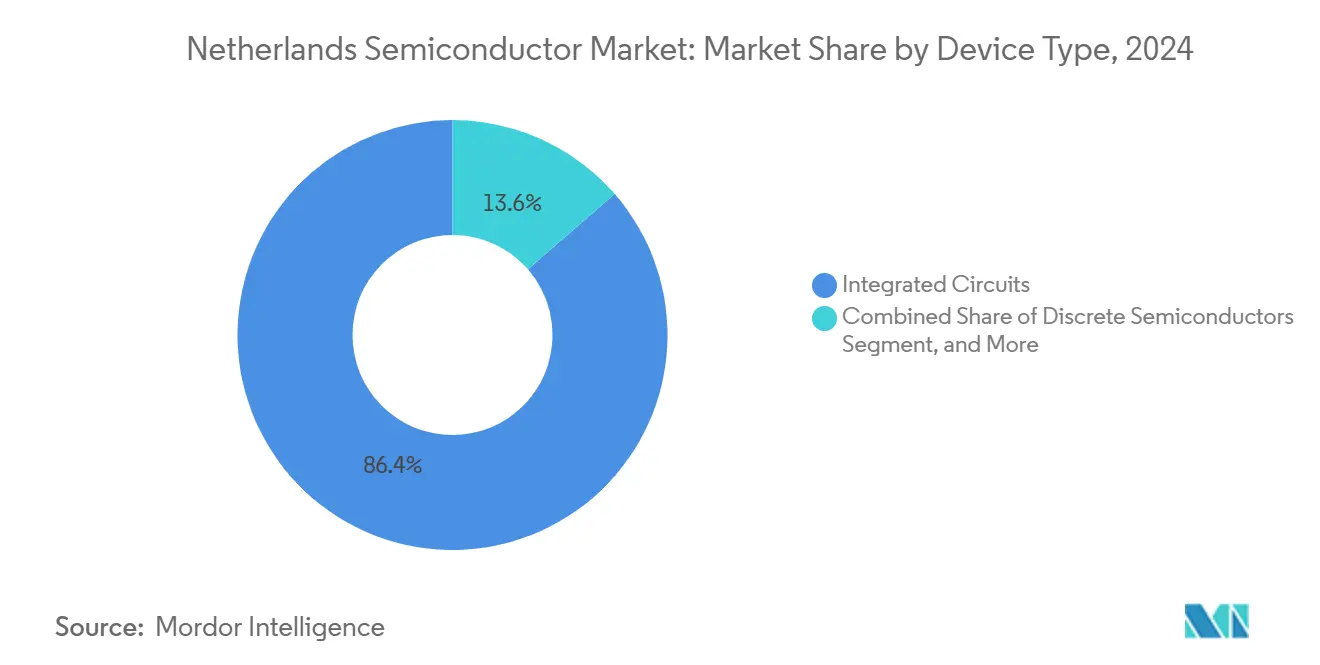

- By device type, integrated circuits led with an 86.4% revenue share in 2024; the same category is projected to expand at a 5.2% CAGR through 2030.

- By business model, design/fabless vendors commanded 67.7% of the Netherlands semiconductor market share in 2024 while advancing at a 5.1% CAGR to 2030.

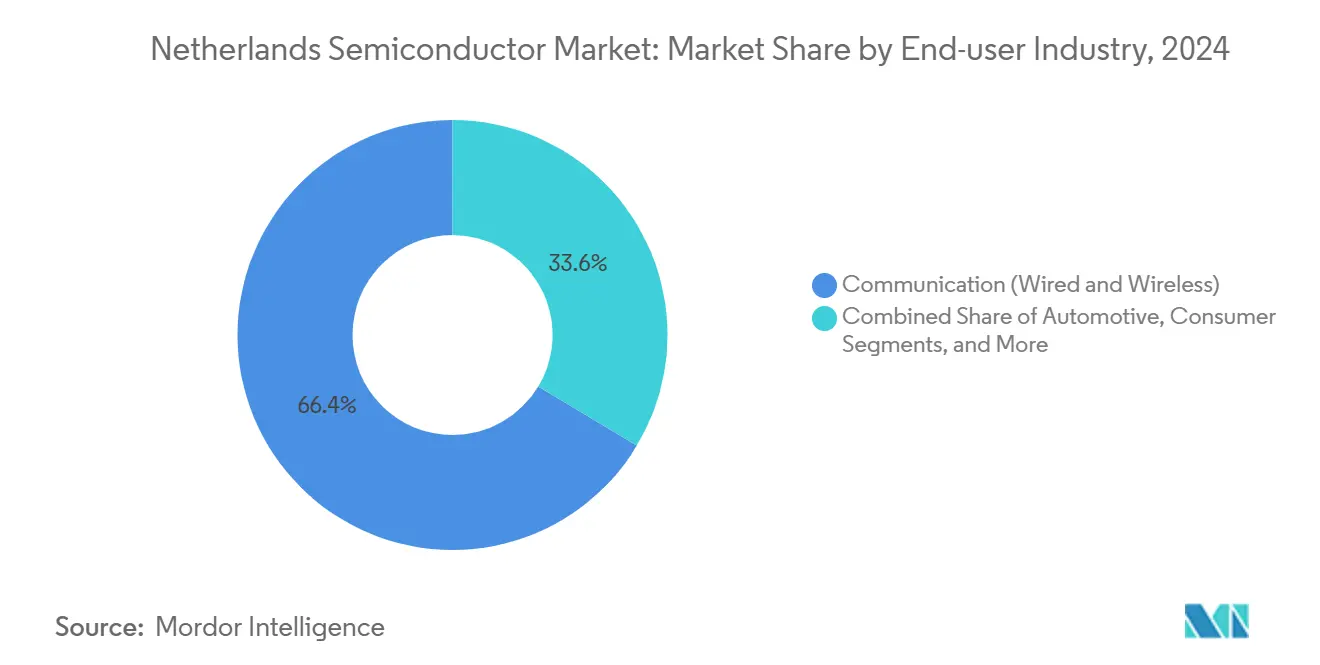

- By end-user, communication applications accounted for 66.4% of the Netherlands semiconductor market size in 2024, whereas AI applications are set to grow at a 9.3% CAGR between 2025 and 2030.

Netherlands Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EU-funded chip sovereignty programmes | +1.2% | EU-wide, concentrated in the Netherlands | Medium term (2-4 years) |

| Automotive electrification roadmap acceleration | +0.8% | Global, with strong European adoption | Long term (≥ 4 years) |

| Transition to 200 mm/300 mm SiC and GaN power fabs | +0.6% | Global, Netherlands equipment dependency | Medium term (2-4 years) |

| Growth of integrated photonics clusters | +0.5% | Netherlands, EU expansion | Long term (≥ 4 years) |

| EU Chips Act-driven foundry capacity incentives | +0.4% | EU-wide, the Netherlands equipment beneficiary | Medium term (2-4 years) |

| Net-zero data center energy-efficiency mandates | +0.3% | Netherlands, expanding to the EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Chips Act sovereignty programs reshape value chains

The EUR 43 billion (USD 50.01 billion) EU Chips Act redirects wafer-fab investments toward Europe and guarantees multi-year demand for high-NA EUV scanners, deposition modules, and packaging lines supplied from the Netherlands. Newly formed regional coalitions sign long-term offtake agreements that prioritize technology depth over direct cost parity. The ChipNL Competence Centre lines up Dutch universities, SMEs, and toolmakers to speed access to pilot lines and to keep incremental service, refurbishment, and upgrade revenue inside the country.[1]Government of the Netherlands, “European countries agree to strengthen position in semiconductor industry,” government.nl

Automotive electrification accelerates power-device demand

Battery-electric vehicles contain roughly two to three times more semiconductor content than combustion cars, elevating power-train silicon-carbide share, which propels inquiries for Dutch epitaxy reactors and advanced packaging platforms. Nexperia has earmarked EUR 200 million (USD 226 million) to convert Hamburg production for SiC and GaN, linking Dutch design expertise with local European capacity. The trend benefits EU carmakers that seek near-shore supplies and shorter logistics loops.[2]Nexperia, “Nexperia to Invest 200 Million USD in Hamburg,” nexperia.com

SiC and GaN fab transitions create equipment-upgrade cycles

Wide-bandgap material processing migrates from 200 mm to 300 mm wafers, forcing fresh capex in substrate cleaning, thermal budget control, and wafer-level testing. ASM International targets >30% market share in silicon epitaxy by 2025 and leverages proprietary dual-reactor platforms for higher uptime. BE Semiconductor Industries advances hybrid bonding tools that address elevated junction temperature demands, maintaining premium gross margins as fabs adapt to new process flows.[3]ASM International N.V., “ASM Annual Report 2023,” asm.com

Integrated photonics clusters establish national leadership

PhotonDelta and the PIXEurope consortium draw a combined EUR 186.8 million (USD 211 million) in public funding that finances 6-inch indium-phosphide and silicon-nitride pilot lines in Eindhoven and Enschede. The move scales photonic-integrated-circuit (PIC) throughput, cuts unit costs, and positions Dutch firms for optical-compute co-packaging inside AI accelerators. Cross-disciplinary talent pooling across TU Eindhoven and the University of Twente shortens R&D spin-up times, reinforcing the Netherlands semiconductor market as Europe’s PIC fulcrum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight specialised-talent pipeline | -0.9% | The Netherlands, spreading to the EU | Short term (≤ 2 years) |

| Export-control uncertainty for China sales | -0.7% | Netherlands companies, global impact | Medium term (2-4 years) |

| Sub-10 nm CAPEX inflation | -0.4% | Global, Netherlands equipment suppliers affected | Long term (≥ 4 years) |

| Chronic energy-price volatility | -0.2% | Netherlands, broader EU context | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Specialized talent pipeline constraints limit expansion

Industry projections indicate demand for an additional 38,000 technicians by 2030, outstripping current graduation rates. The Dutch government earmarked EUR 80.9 million (USD 91 million) for targeted training in Brainport Eindhoven, Delft, Twente, and Groningen, but housing shortages and lengthy visa processes still slow recruitment. Toolmakers have begun sponsoring local vocational programs while advocating for joint EU mobility frameworks that would streamline work-permit approvals.[4]IO+, “Training microchip talent gets solid boost in four Dutch regions,” ioplus.nl

Export-control uncertainty creates revenue volatility

Effective April 2025, the Netherlands extended licensing rules to include advanced inspection and metrology gear. China represented 26.3% of ASML revenue in 2023; any further rule tightening would dent shipment volumes and complicate service personnel deployments. Dutch suppliers are now accelerating diversification toward Southeast Asian and North American fabs to safeguard order books while remaining compliant with evolving dual-use regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated circuits sustain innovation leadership

Integrated circuits held 86.4% share of the Netherlands semiconductor market in 2024 and remain the fastest-growing device group at a 5.2% CAGR through 2030. Sub-3 nm logic ramps pull through more than 20 high-NA EUV scanners, locking in multi-year demand visibility. Discrete semiconductors keep niche relevance in automotive power-management blocks, whereas optoelectronics leverage the national photonics build-out. Sensors and MEMS gain traction after the establishment of Xiver, which re-localizes MEMS development and reduces dependency on overseas foundries.

The integrated-circuit focus dovetails with the Netherlands' semiconductor market share advantages in design tooling, wafer metrology, and cleanroom automation. Incremental heterogeneous-integration roadmaps, including backside power delivery and chiplet interposers, feed complementary revenues into assembly and test clusters around Eindhoven. As photonic interconnects mature, hybrid electronic-photonic ICs should lift the blended Netherlands semiconductor market size for the device category beyond USD 7 billion by 2030.

By Business Model: Design/fabless alignment reflects IP strategy

Design/fabless firms controlled 67.7% of the Netherlands' semiconductor market revenue in 2024 and will grow at a 5.1% CAGR, underscoring the country’s emphasis on capital-light innovation. NXP anchors the model, outsourcing large-scale wafer runs while retaining RF front-end and automotive MCU design in Eindhoven. Fabless independence lifts gross margin potential and fits an ecosystem where academic spin-outs and SME IP houses feed differentiated blocks into global foundry platforms.

Integrated-device-manufacturer (IDM) activity persists where vertical control grants strategic leverage, most notably for high-precision tool suppliers. Nonetheless, capex intensity deters wide adoption, signaling that incremental Netherlands semiconductor industry spin-outs will continue to favor fabless footprints. Government grants now target co-design pilot lines that let SMEs prototype on shared equipment, lowering entry barriers without shifting the established fabless orientation.

By End-User Industry: AI accelerates beyond communication-based

Communication infrastructure preserved a 66.4% contribution to the Netherlands semiconductor market revenue in 2024, but AI workloads show the sharpest trajectory at a 9.3% CAGR through 2030. Hyperscale datacenters upgrade to liquid-cooled racks and optical-electrical co-packages, thereby multiplying orders for Dutch inspection optics and laser-trimming stations. Mandatory 27 °C inlet-air rules in new halls heighten interest in photonic interconnect-enabled switches that cut power budget per bit transferred.

Automotive semiconductors stay on a steady climb as battery-electric vehicle penetration in the EU tops 50% mid-decade. NXP’s Q1-2024 automotive revenue of USD 1.804 billion validates sustained OEM commitments despite cyclical unit weakness elsewhere. Industrial IoT and factory automation add long-tail demand for robust microcontrollers and short-range connectivity, whereas consumer-device volumes plateau under global smartphone saturation. Government and aerospace orders gain a modest uplift from EU security initiatives that seek sovereign radar and satellite-link chipsets.

Geography Analysis

Cluster strength gives the Netherlands an outsized role in the global value chain. Brainport Eindhoven alone accounts a significant share of domestic semiconductor patent filings, anchored by ASML’s R&D campus. Project Beethoven allocates funds for housing, rail upgrades, and green energy links, directly supporting workforce scalability. Eindhoven’s proximity to high-precision machining SMEs such as VDL ETG shortens component lead times and accelerates EUV tool release cycles.

Delft complements the main hub with quantum-computing research. QuTech’s work on semiconductor spin qubits feeds longer-term roadmaps for cryogenic control ASICs, expanding future Netherlands semiconductor market opportunities. Twente and Enschede concentrate on photonics, housing a 6-inch pilot line that positions the region as Europe’s prime PIC volume ramp site. Groningen, meanwhile, emphasizes vocational channels to expand technician pools, directly helping to mitigate national talent bottlenecks.

Internationally, Dutch companies pursue a dual-location blueprint: keep design, tool engineering, and high-value assembly at home, while co-investing in offshore wafer fabs for cost leverage. NXP’s USD 7.8 billion 300 mm venture in Singapore exemplifies the model, linking secure supply with Asia-Pacific demand without diverting domestic R&D jobs. A separate memorandum with New York State centers on sustainability benchmarks and shared workforce certifications, reinforcing the Netherlands semiconductor market’s outward-looking yet IP-anchored strategy.

Competitive Landscape

Competitive dynamics are split between near-monopoly toolmakers and a long tail of niche suppliers. ASML retains 100% share in EUV scanners and secures lifetime service attachments that exceed 25 years, ensuring predictable annuity streams. ASM International holds >55% share in atomic-layer deposition tools and aims to translate epitaxy gains into expanded process-step coverage. BE Semiconductor Industries leads advanced die-attach and hybrid-bonding markets for logic-memory stacking.

Photonics start-ups such as Astrape leverage Eindhoven’s opto-electronic cleanrooms to prototype optical switches targeting AI cluster power budgets. Quantum Delta NL funnels EUR 615 million (USD 715.27 million) into quantum-device and cryo-electronic ventures, spawning next-gen challengers. Overall, the top five players collectively capture an estimated 80% of the Netherlands semiconductor market revenue, while over 300 supporting firms specialize in vacuum valves, wafer chuck systems, and cleanroom metrology. The coexistence of dominant champions and agile start-ups builds a resilient ecosystem against single-node disruptions.

Netherlands Semiconductor Industry Leaders

ASML Holding N.V.

NXP Semiconductors N.V.

BE Semiconductor Industries N.V.

ASM International N.V.

Nexperia B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BE Semiconductor Industries posted EUR 144.1 million (USD 163 million) Q1 revenue as Applied Materials bought a 9% stake, validating hybrid-bonding roadmaps.

- May 2025: The Netherlands and Singapore created a semiconductor working group focused on advanced packaging knowledge exchange.

- March 2025: ASML and imec signed a five-year agreement to equip sub-2 nm research lines and co-develop silicon-photonics packaging flows.

- March 2025: Nexperia released 12 e-mode GaN FETs aimed at telecom and industrial power systems.

Netherlands Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the Netherlands semiconductor market in 2025?

The market is expected to reach USD 7.03 billion in 2025 with a 4.72% CAGR projected to 2030.

Which device category leads Dutch semiconductor revenue?

Integrated circuits contribute 86.4% of 2024 revenue and remain the fastest-growing device group.

Why is ASML critical to global chip production?

ASML supplies 100% of EUV lithography tools, a prerequisite for sub-7 nm manufacturing nodes.

What role does photonics play in future Dutch growth?

Nationally funded pilot lines in Eindhoven and Enschede aim to industrialize photonic-integrated circuits that reduce datacenter power consumption.

How are export controls affecting Dutch suppliers?

New 2025 licensing rules create sales volatility in China, prompting Dutch firms to diversify toward Southeast Asian and North American fabs.

Where are talent shortages most acute?

Brainport Eindhoven needs thousands of additional technicians, leading the government to allocate EUR 80.9 million for targeted training across four regions.

Page last updated on: