Germany Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

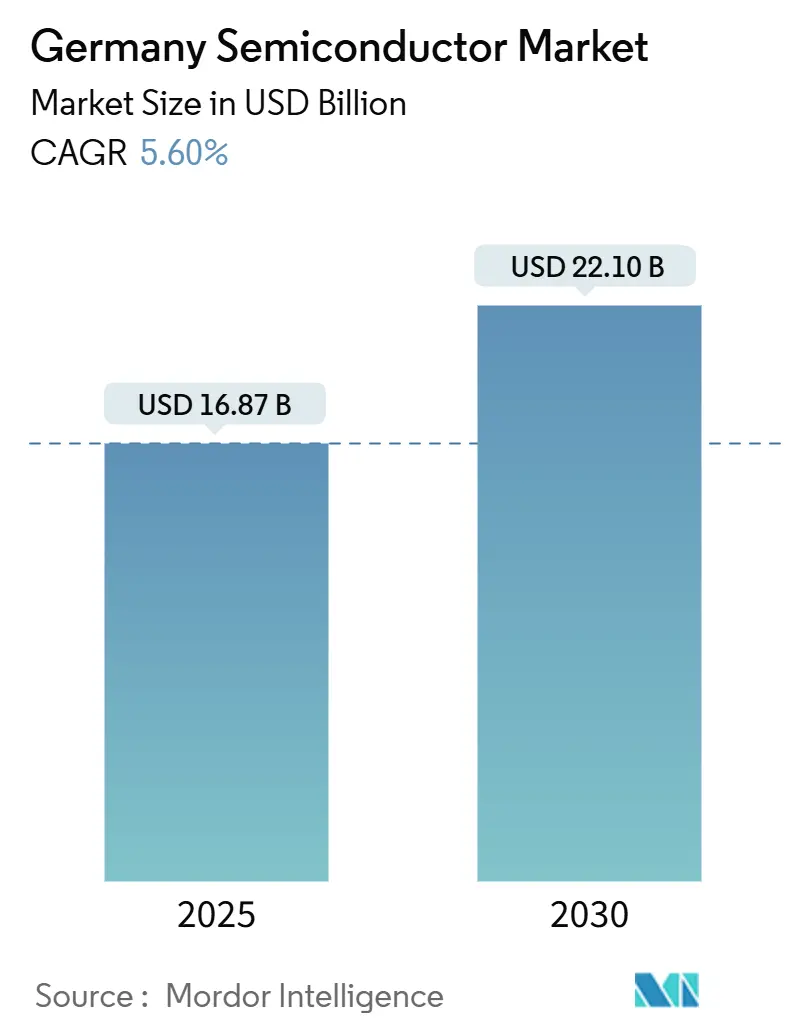

| Market Size (2025) | USD 16.87 Billion |

| Market Size (2030) | USD 22.10 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

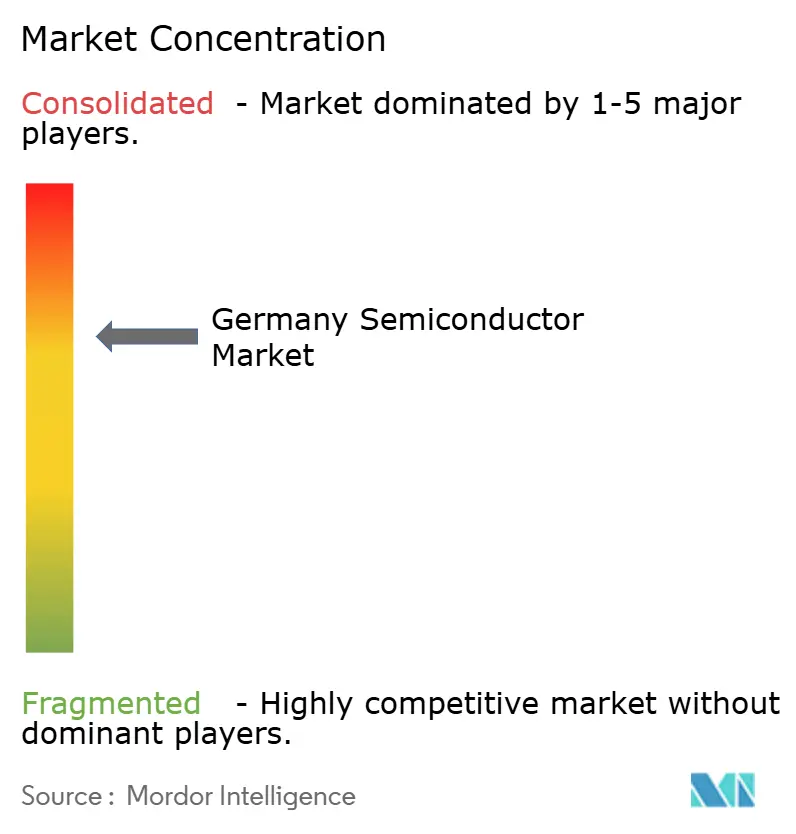

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Semiconductor Market Analysis by Mordor Intelligence

The German semiconductor market size stands at USD 16.87 billion in 2025 and is projected to climb to USD 22.10 billion by 2030, advancing at a 5.60% CAGR. Robust policy support under the EU Chips Act, sizeable private-sector commitments, and entrenched automotive electronics demand collectively underpin this trajectory. Integrated Circuits command the revenue mix, while silicon carbide (SiC) and gallium nitride (GaN) devices accelerate the shift toward high-efficiency power conversion. Automotive electrification and Industry 4.0 automation continue to widen the customer base, even as energy-price volatility and talent shortages temper near-term profitability. Medium-term growth catalysts include Dresden’s expanding “Silicon Saxony” cluster and a rapidly maturing local supply chain that decreases reliance on advanced nodes produced in East Asia.

Key Report Takeaways

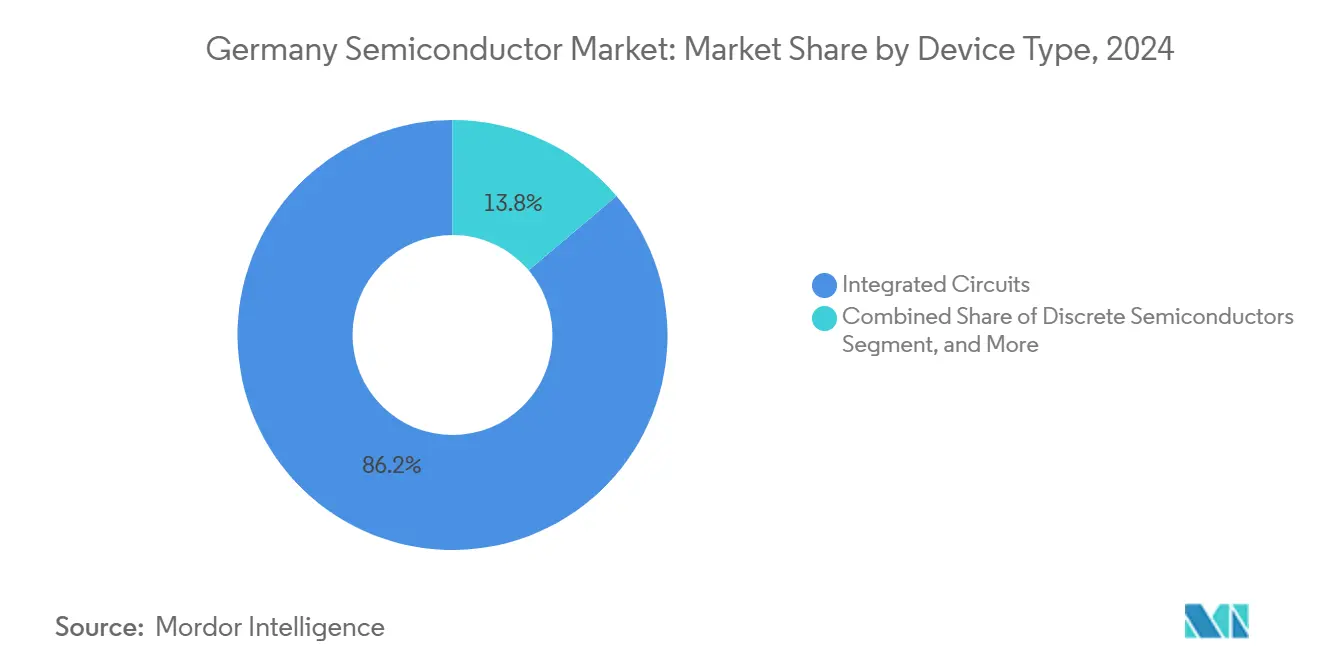

- By device type, Integrated Circuits captured 86.2% of the German semiconductor market share in 2024; Discrete SiC and GaN devices are forecast to post the highest 6.1% CAGR to 2030.

- By business model, Design/Fabless vendors held 67.8% share of the German semiconductor market size in 2024, while the segment continues to expand at a 5.9% CAGR through 2030.

- By end-user industry, the Communication segment led with 66.1% revenue share in 2024, yet AI-centric applications are advancing at a 9.5% CAGR to 2030.

Germany Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing EV-driven power semiconductor demand | +1.8% | Global, with concentration in Germany and EU automotive hubs | Medium term (2-4 years) |

| Expansion of Dresden "Silicon Saxony" cluster | +1.2% | Saxony region, spillover effects across Germany | Long term (≥ 4 years) |

| Government EU Chips Act subsidies | +0.9% | Germany and the broader EU, with a focus on strategic locations | Medium term (2-4 years) |

| Rising adoption of SiC/GaN in renewable-energy inverters | +0.7% | Global, early adoption in Germany and Northern Europe | Medium term (2-4 years) |

| Industrial automation and Industry 4.0 sensor proliferation | +0.6% | Germany, expanding to Central and Eastern Europe | Long term (≥ 4 years) |

| Edge-AI chips for automotive ADAS | +0.4% | Global automotive markets, German OEM leadership | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing EV-driven Power-Semiconductor Demand

Electric vehicles embed up to USD 2,000 worth of semiconductors per unit, lifting local content requirements for traction inverters and on-board chargers. Infineon’s 200 mm SiC rollout in 2025—supported by customer commitments of roughly EUR 5 billion (USD 5.35 billion)—positions the firm to attain 30% global SiC share by 2030. Complementary investments by Bosch and Continental in power-electronics back-end lines reinforce a vertically integrated ecosystem that curbs dependency on offshore fabs. EU rules favoring regional sourcing for critical vehicle systems further amplify demand visibility, making EV electrification the linchpin for incremental wafer starts in Germany.

Expansion of the Dresden “Silicon Saxony” Cluster

Dresden already delivers every third chip produced in Europe, and the EUR 10 billion (USD 10.7 billion) ESMC foundry—backed by TSMC, Bosch, Infineon, and NXP—will lift local FinFET capacity to 40,000 wafers per month by 2029.[1]“ESMC Breaks Ground on Dresden Fab,” tsmc.com Parallel upgrades at Infineon’s Smart Power Fab and GlobalFoundries’ EUR 1.1 billion (USD 1.28 billion) debottlenecking program extend the cluster’s economies of scale. Vendor colocation accelerates learning curves, boosts equipment-utilization rates, and anchors a dense supplier network, all of which collectively raise regional productivity. The ecosystem’s increasing stickiness attracts design houses and research institutes, reinforcing Germany’s bid for technological sovereignty in the European value chain.

Government EU Chips Act Subsidies

Germany has ring-fenced EUR 20 billion (USD 21.4 billion) for semiconductor incentives through 2030, securing headline projects such as Intel’s Magdeburg megaplant and TSMC’s Dresden JV. The funding prioritizes first-of-a-kind technologies, ties support to local R&D commitments, and triggers staggered disbursements tied to milestones. Infineon obtained EUR 920 million (USD 984 million) for its Smart Power Fab under the Important Project of Common European Interest (IPCEI) umbrella. While bureaucratic lead times stretch project start-ups, the subsidy playbook markedly improves the risk-adjusted returns needed to green-light high-capex fabs within German borders.

Rising Adoption of SiC/GaN in Renewable-Energy Inverters

SiC devices enable lighter, more efficient solar inverters by operating at higher switching frequencies and temperatures, trimming system losses by up to 50%. Infineon’s CoolSiC portfolio alone secured design wins worth EUR 5 billion (USD 5.35 billion) as of early 2025. Nexperia’s USD 200 million Hamburg expansion centers on 200 mm SiC MOSFETs destined for both automotive and industrial power stages. Widespread feed-in tariff reforms and corporate decarbonization targets accelerate demand visibility, ensuring that wide-bandgap devices remain a structural growth lever rather than a cyclical upswing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-price volatility | -0.8% | Germany and the energy-intensive EU | Short term (≤ 2 years) |

| Skilled-labor shortage | -1.1% | Germany and EU hubs | Long term (≥ 4 years) |

| Supply-chain exposure to East-Asian fabs | -0.6% | Global | Medium term (2-4 years) |

| Lengthy environmental permitting | -0.4% | Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy-Price Volatility Post-2022

Electricity costs spiked after 2022, lifting European semiconductor operating expenses well above Asian benchmarks.[2]Siemens AG, “Annual Financial Report 2024,” siemens.com Although Berlin rolled out temporary industrial power subsidies, the relief does not offset fundamental cost gaps for 24/7 cleanroom operations. Fabs are adopting renewable power purchase agreements and energy-recovery systems, but the high-carbon-price environment still pressures wafer pricing and margin resilience. Elevated utility tariffs can delay equipment-tool moves and disincentivize future 300 mm investments—especially for logic processes where economies of scale are critical.

Skilled-Labor Shortage for Advanced Nodes

Germany faces a structural shortfall of specialized engineers as baby boomer retirements accelerate and STEM enrollments lag. The Saxon state government, industry chambers, and major fabs signed cooperation charters in 2024 to expand dual-education pathways and retrain mid-career technicians, yet time-to-competence still stretches to several years. Short supply in process-integration and lithography experts complicates efforts to ramp sophisticated FinFET lines, causing a multiquarter lag between tool installation and yield optimization. Persistent labor scarcity could dilute the German semiconductor market’s ability to internalize next-generation nodes despite substantial capital outlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Drive Innovation

Integrated Circuits contributed USD 14.6 billion—or 86.2%—to the German semiconductor market size in 2024, outpacing other categories with an expected 6.1% CAGR to 2030. Infineon’s 29% global share in automotive microcontrollers underpins the segment’s premium mix, while ESMC’s foundry entrance unlocks local FinFET supply for logic-heavy ICs.

Power-discrete SiC and GaN volumes are smaller but more lucrative per die, explaining robust fab expansions in Hamburg and Kulim. Sensor and MEMS lines ride the Industry 4.0 wave, capturing content gains in predictive-maintenance modules. Optoelectronics, led by AMS OSRAM, leverages Germany’s LED and LiDAR heritage to serve both automotive headlights and industrial machine-vision markets. Overall, mature-node specialization and stringent automotive qualification requirements fortify the German semiconductor market against commoditization pressures.

By Business Model: Design Excellence Prevails

Design/Fabless vendors held 67.8% of the German semiconductor market in 2024, supported by IP-rich portfolios tailored for automotive and industrial customers. Proximity to OEMs shortens feedback loops, enabling rapid tape-outs for application-specific ICs.

Integrated-Device Manufacturers (IDMs) like Infineon and Bosch wield vertical integration to guarantee supply security for safety-critical vehicle functions. Hybrid models, in which design houses tap foundry partners for peak demand, proliferate as capital intensity rises. The structure nurtures a collaborative ecosystem where fabless ingenuity coexists with IDM scale, jointly reinforcing Germany's claim as Europe's semiconductor powerhouse.

By End-user Industry: AI Disrupts Traditional Patterns

Communication applications delivered 66.1% of 2024 revenue, reflecting entrenched strengths in industrial fieldbus and automotive networking chips. Yet AI-centric use cases—particularly edge inference for advanced driver-assistance systems (ADAS)—are posting a segment-leading 9.5% CAGR through 2030, lifting the German semiconductor market size allocated to AI chips.

Automotive electrification boosts silicon content per vehicle from USD 250 in 2020‐era internal-combustion cars to roughly USD 2,000 in 2025-era battery-electric models. Industrial automation layers incremental demand for edge-vision processors and smart-sensor ASICs. Computing and data-center exposure remains modest, shielding local vendors from hyperscale pricing pressures while enabling focus on high-reliability niches.

Geography Analysis

Germany accounted for roughly one-third of total EU chip exports in 2024, sustaining trade surpluses with China and South Korea but deficits with Taiwan and Japan. Saxony’s Silicon Saxony hub leads production, hosting GlobalFoundries, Infineon, and the ESMC FinFET fab underway. The alliance cements Dresden’s status as Europe’s most advanced logic cluster while generating 2,000 direct jobs upon ramp-up.

Bavaria follows with power semiconductor depth centered on Infineon’s headquarters in Munich and wafer fabs in Regensburg. Saarland was slated to gain momentum through Wolfspeed’s SiC project, although ZF’s withdrawal in early 2025 clouds that outlook.[3]“ZF Said to Be Withdrawing from Wolfspeed’s German SiC Fab Project,” semiconductor-today.com Hamburg sustains discrete device specialization via Nexperia’s high-volume diode lines, producing nearly 100 billion units annually.

Federal incentives distribute investments across regions, aligning with Germany’s decentralized industrial fabric. Intel’s deferred Magdeburg complex still symbolizes future upside for Saxony-Anhalt, pending resolution of subsidy tranches. Overall, geographic diversification mitigates regional supply-chain risks, yet also amplifies competition for scarce process engineers, underscoring the skilled-labor restraint highlighted earlier.

Competitive Landscape

The German semiconductor market exhibits moderate concentration: the top five vendors control just under 70% of national revenue, anchored by Infineon’s leadership in automotive MCUs and power devices. Infineon strengthened its portfolio by acquiring Marvell’s Automotive Ethernet unit for USD 2.5 billion in April 2025, integrating low-latency networking with compute domains crucial for software-defined vehicles.[4]“Infineon Further Strengthens Its Number One Position with Acquisition of Marvell’s Automotive Ethernet Business,” infineon.com

Bosch leverages vertical integration to supply sensors, ASICs, and complete power-electronics modules to its Tier 1 automotive customers, translating system knowledge into sticky design wins. X-FAB’s niche foundry services remain pivotal for mixed-signal and MEMS wafers, benefitting from the broader pivot toward sensor-rich EV platforms.

Emergent challengers include Black Semiconductor, which raised USD 273 million to commercialize graphene-based photonic ICs by 2027. The ESMC joint venture complicates traditional fabless–foundry delineations, offering domestic FinFET capacity to European designers previously reliant on Taiwanese fabs. Strategic arsenals thus center on SiC/GaN process know-how, automotive functional-safety certification, and sovereign manufacturing footprints—all decisive factors for maintaining margin resilience in a tightening global cycle.

Germany Semiconductor Industry Leaders

Infineon Technologies AG

Robert Bosch GmbH (Semi Division)

GlobalFoundries Dresden

X-FAB Silicon Foundries SE

Elmos Semiconductor SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon secured final German government funding for its EUR 5 billion (USD 5.35 billion) Smart Power Fab in Dresden, with production slated for 2026.

- April 2025: Infineon agreed to acquire Marvell Technology’s Automotive Ethernet business for USD 2.5 billion, bolstering in-vehicle networking capabilities.

- February 2025: Infineon launched its first 200 mm silicon carbide products manufactured in Villach, Austria, aimed at renewable-energy and EV traction inverters.

- February 2025: SkyWater Technology will acquire Infineon’s Austin 200 mm fab, adding nearly 1,000 U.S. jobs and expanding foundational-chip capacity.

Germany Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the German semiconductor market in 2025?

The German semiconductor market size is USD 16.87 billion in 2025.

What CAGR is expected for German semiconductor revenue through 2030?

Revenue is forecast to rise at a 5.60% CAGR from 2025 to 2030.

Which device category leads German chip sales?

Integrated Circuits account for 86.2% of 2024 revenue.

Why is Dresden significant for chipmaking?

Dresdens Silicon Saxony cluster produces one-third of European chips and hosts new FinFET capacity.

How is Germany addressing skilled-labor shortages?

Industrygovernment partnerships in Saxony expand dual-education and retraining programs for fab engineers.

Page last updated on: