Turkey Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

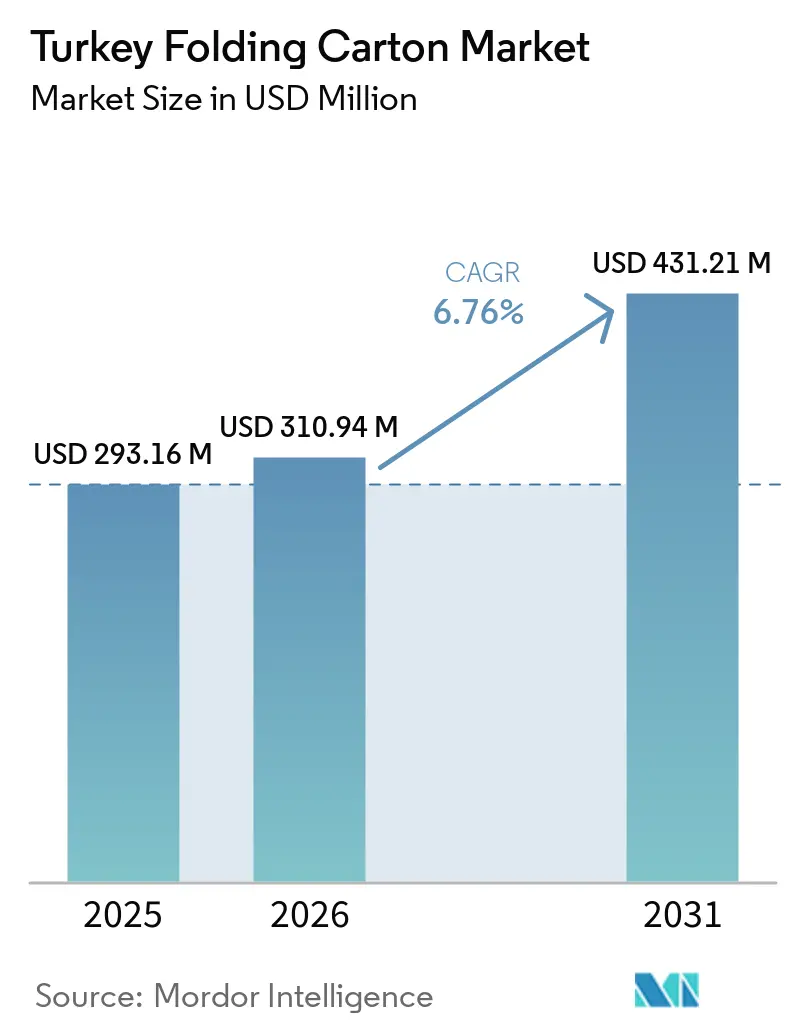

| Base Year Market Size (2025) | USD 293.16 Million |

| Market Size (2026) | USD 310.94 Million |

| Market Size (2031) | USD 431.21 Million |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

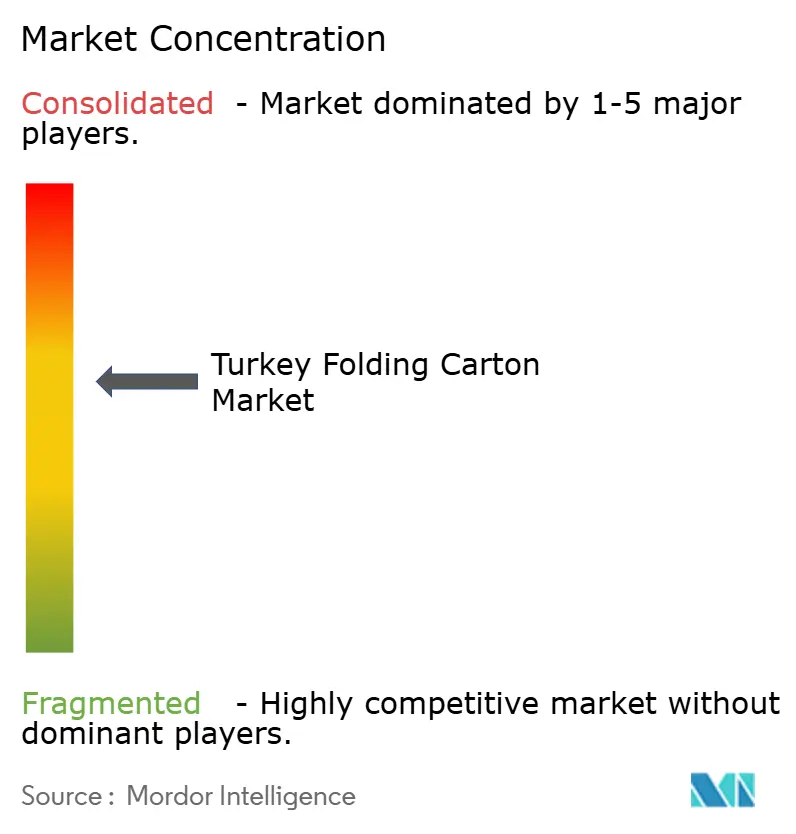

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Folding Carton Market Analysis by Mordor Intelligence

The Turkey folding carton market size is projected to expand from USD 293.16 million in 2025 and USD 310.94 million in 2026 to USD 431.21 million by 2031, registering a 6.76% CAGR between 2026 and 2031. Sustained growth is tied to the country’s role as a production base for European brands that want cost-competitive secondary packaging and to steady gains in domestic organized retail. Pharmaceuticals account for an outsized share of incremental demand because ninety percent of medicines exported from Turkey are produced locally under GMP conditions that mandate high-grade cartons. Parallel momentum comes from e-commerce fulfillment investments, which anchor short-run packaging orders that favor digital printing and lighter substrates. Government incentives under the Industrial Green Transformation program, aligned with recycled-content targets in the National Circular Economy Strategy, are tilting material choices toward paperboard and hastening the switch from solvent to water-based and digital workflows. Input-cost volatility and competition from flexible plastic pouches temper the outlook, yet converters that secure SYD certification and adopt emission-compliant technology are positioned to capture premium orders.

Key Report Takeaways

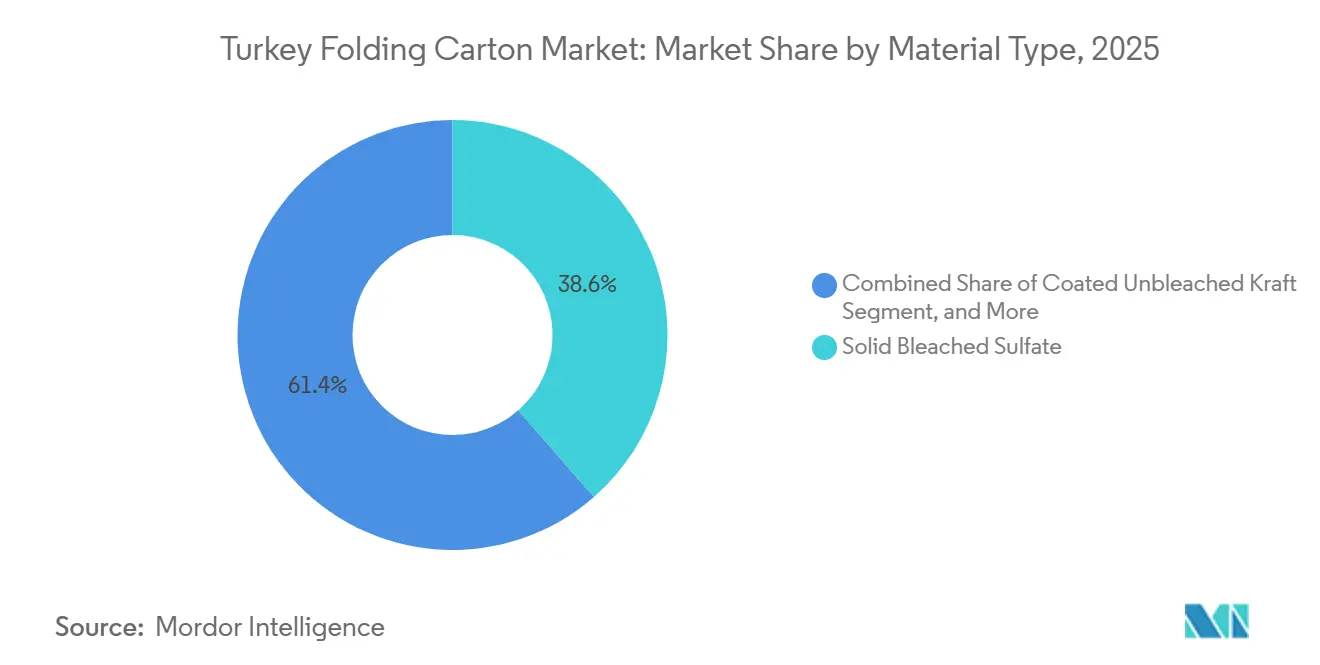

- By material type, solid bleached sulfate captured with 38.57% of the Turkey folding carton market share in 2025.

- By printing technology, the Turkey folding carton market size for digital printing is projected to grow at a 8.84% CAGR to 2031.

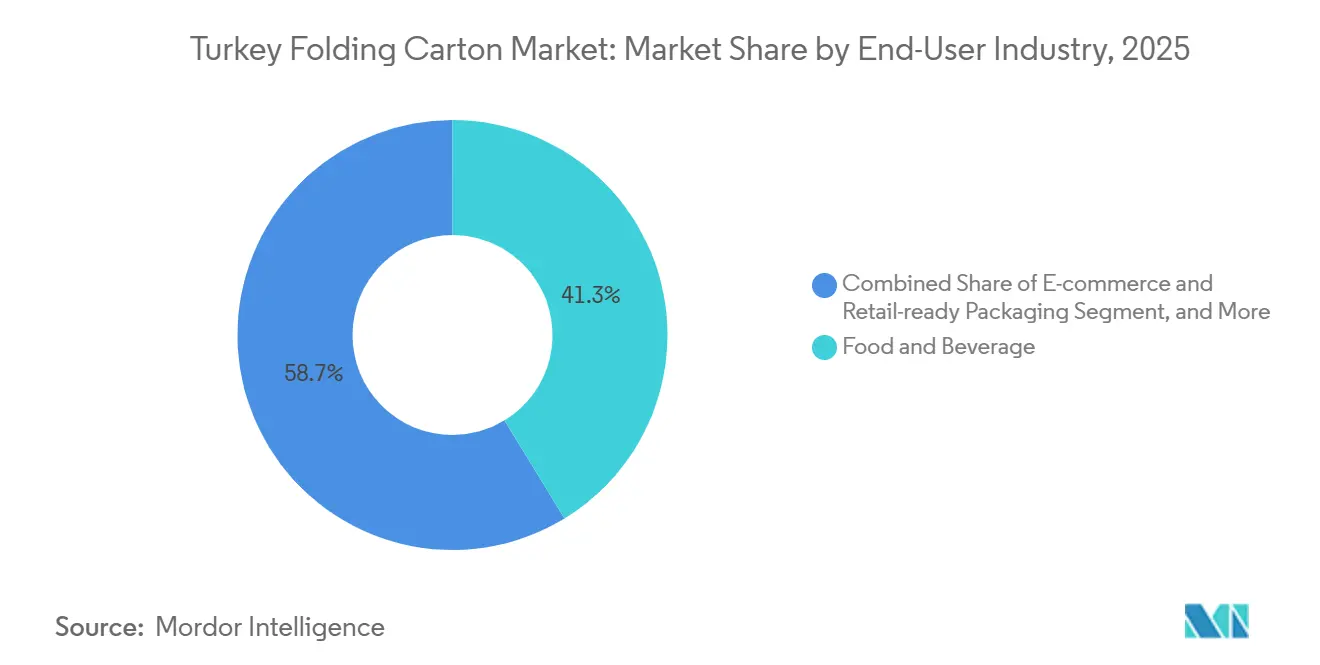

- By end-user industry, the food and beverage industry captured 41.28% of the Turkey folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Shelf-Ready Packaging in Organized Retail | +1.2% | National, concentrated in Istanbul, Izmir, and Ankara metropolitan areas | Medium term (2-4 years) |

| Rising Pharmaceutical Exports from Turkey | +1.5% | National production, exports to the Middle East, North Africa, and Eastern Europe | Long term (≥ 4 years) |

| Expansion of E-Commerce Fulfillment Centers | +1.3% | National, early concentration in Istanbul, Ankara, and the Aegean region | Short term (≤ 2 years) |

| Government Incentives for Sustainable Paper Packaging | +0.9% | National, preferential support for facilities achieving D-level SYD certification | Medium term (2-4 years) |

| Rapid Growth of Quick-Service Restaurant Chains | +0.7% | National, urban centers | Medium term (2-4 years) |

| Integration of Smart Packaging Features | +0.4% | National, pharmaceutical and cosmetics clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Shelf-Ready Packaging in Organized Retail

Modern grocery chains are expanding across Turkey and replacing manual shelf stocking with perforated, retail-ready cartons that reduce labor by about 40% and increase sales by up to 20%. CarrefourSA’s divestiture to A101 and Gurme’s footprint growth illustrate the race for merchandising efficiency. Converters respond by installing rotary die-cutters and inline gluers that create complex tear-strip designs at high speed. Brand owners in snacks, beverages, and personal care specify graphic-rich cartons to offset in-store crowding and lock in higher-unit-value orders. The pull-through effect is strongest around Istanbul, where store density and wage pressure are highest, making shelf-ready formats a structural growth pillar for the Turkey folding carton market.

Rising Pharmaceutical Exports from Turkey

Domestic manufacturers shipped USD 2.3 billion in medicines during 2024, and 90% originated from Turkish plants that insist on traceable, tamper-evident cartons. Solid Bleached Sulfate is preferred because its smooth, virgin fiber layer yields crisp variable data for serialization. Export orientation also demands multilingual labeling, which is easier to change digitally than on plate-based presses. As Europe and Middle East buyers outsource contract manufacturing to Turkey for cost and proximity benefits, secondary packaging volume is set to outpace overall production, anchoring double-digit gains in the Turkey folding carton market.

Expansion of E-Commerce Fulfillment Centers

Arvato’s 31,000 square-meter Istanbul hub and OPLOG’s capacity additions illustrate rapid warehouse build-out that underpins direct-to-consumer shipping. Online orders require cartons that survive automated sortation and last-mile handling yet deliver an engaging unboxing moment. The format shift favors lighter folding boxboard to curb shipping weight and digital presses that personalize interior graphics. Demand is pronounced in cosmetics, electronics and specialty foods, lifting the e-commerce segment’s 8.39% CAGR and broadening the application base for the Turkey folding carton market.

Government Incentives for Sustainable Paper Packaging

The Industrial Emissions Management Regulation links SYD certification scores to grants, loans, and tax relief, steering investment into energy-efficient, low-VOC paper converting lines. Installations must hit at least F-level by 2028 and D-level by 2030, accelerating retrofits of water-based flexo and digital systems that inherently meet solvent caps. Because paperboard is more easily recycled than multi-material laminates, brand owners lean toward cartons to satisfy upcoming recycled-content mandates, reinforcing demand across food, pharma, and personal care applications within the Turkish folding carton market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Pulp and Paper Prices | -0.8% | National, exposed to global pulp markets | Short term (≤ 2 years) |

| Competition From Flexible Plastic Pouches | -0.6% | National, strong in dry-food and snack lines | Medium term (2-4 years) |

| Limited Domestic Collection of High-Quality Recovered Paper | -0.5% | National, regions with weak segregation infrastructure | Long term (≥ 4 years) |

| Stringent Offset Printing Emission Regulations | -0.3% | National, solvent-based printers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Pulp and Paper Prices

Bleached eucalyptus kraft prices swung by USD 40 per tonne in April 2025, and spot markets fluctuated near USD 600 per tonne for much of the year, squeezing converters locked into fixed-price contracts. Imported recovered paper remains capped at fifty percent of mill capacity, limiting substitution when virgin pulp surges. Independent converters without hedging tools experience the sharpest margin erosion, prompting consolidation as scale becomes vital to counter swings that dilute profits in the Turkey folding carton market.

Competition From Flexible Plastic Pouches

Pouches undercut cartons on material cost and moisture barrier, driving share gains in snacks, detergents, and pet food. Resealable zippers, spouts, and shaped formats enhance convenience, yet multi-layer films are difficult to recycle under Turkey’s extended producer responsibility rules.[1]Packaging Europe Team, “Flexible Packaging Sustainability Debate,” Packaging Europe, packagingeurope.com Paperboard’s 83.1% recycling rate in the European Union offers a sustainability edge for premium and organic brands, but price-sensitive categories will continue to test the resilience of the Turkey folding carton market against pouch conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Solid Bleached Sulfate Extends Premium Lead

Solid Bleached Sulfate captured 38.57% of Turkey folding carton market share in 2025, and its eight-plus percent CAGR through 2031 underscores its stronghold in pharmaceuticals and luxury cosmetics. The bright, virgin surface delivers high-definition graphics, supports anti-counterfeiting inks, and meets stringent fiber purity tests favored by regulators. Folding Boxboard remains the mid-tier workhorse, balancing cost and performance, though rising pulp prices are narrowing its price gap with SBS. Coated Unbleached Kraft and White Line Chipboard occupy niches where tensile strength or cost override aesthetics, yet contamination in local wastepaper streams restricts their advance. Specialty grades, including grease-resistant and metalized variants, are winning orders from quick-service restaurants seeking compostable yet functional packaging, a trend driven by McDonald’s target of 500 stores.[2]McDonald’s Turkey Investor Relations, “Restaurant Development Update 2025,” McDonald’s Turkey, mcdonalds.com.tr These dynamics keep the Turkey folding carton market size for SBS and allied premium substrates on a faster trajectory than recycled grades.

Second-tier materials mirror these forces. White Line Chipboard benefits when recovered fiber is clean, but current 50% national recycling rates limit quality, pushing converters to import or upgrade screening systems. Hybrid constructions that laminate thin barrier films to SBS are emerging to meet extended shelf life needs without abandoning recyclability. Material innovation coupled with regulatory pressure is sharpening the competitive gap in favor of converters that can engineer performance without violating forthcoming recycled-content thresholds, reinforcing SBS leadership in the Turkey folding carton market.

By Printing Technology: Digital Captures Short-Run Flexibility

Lithography accounted for 46.63% of output in 2025 thanks to entrenched infrastructure and long-run economies of scale, yet digital presses are accelerating at an 8.84% CAGR through 2031. Brand owners launching region-specific flavors or promotional bundles opt for variable images without plate costs, slashing lead times from days to hours. Flexography, using water-based inks, is also on the rise because it meets low-VOC requirements embedded in SYD scoring. Gravure is retreating under capital demands for emission-control units and falling tobacco volumes. Hybrid workflows that marry digital imaging with inline foiling and die-cutting are coming to the fore, letting converters offer mass personalization at near-offset speeds.

Early adopters already win e-commerce and pharmaceutical jobs that require serialized or scannable codes, proving that technology agility is a key differentiator in the Turkey folding carton market. Longer term, software-driven color management and automated job changeovers will further compress minimum economical run sizes, eroding lithography’s barrier to entry. Equipment financing schemes tied to government green loans reduce capital hurdles for digital upgrades, accelerating diffusion beyond Istanbul into Anatolian plants. As digital’s cost curve falls, its share is likely to double by decade end, cementing a structural shift in the printing technology mix that underpins the Turkey folding carton market.

By End-User Industry: E-Commerce and Pharmaceuticals Propel Demand

Food and beverage still dominate volume with 41.28% of the Turkey folding carton market size in 2025, anchored in cereal, confectionery, and multipack drinks. However, e-commerce and retail-ready packaging will log the fastest CAGR at 8.39% because every incremental online order requires a ship-ready display box or protective sleeve. Fulfillment operators mandate right-sized cartons that absorb shocks on high-speed sorters and double as branding canvases, sending converters scrambling for CAD software and digital printing capacity. Pharmaceuticals represent the second-fastest lane, buoyed by USD 2.3 billion in exports that rely on high-barrier SBS with security features. Personal care customers overlay smart tags that authenticate provenance, moving folding cartons up the value ladder.

Other categories show mixed signals. Household cleaners flirt with flexible pouches to save costs, while premium detergents revert to cartons to make recyclability claims. Electronics packaging contracts as devices shrink, though high-value smartphones still use rigid folding boxes as part of brand theater. Tobacco continues to decline under plain-pack rules. Diversified converters hedge exposure by servicing multiple end-users, a strategy that stabilizes throughput amid category swings and sustains a balanced order book within the Turkey folding carton market.

Geography Analysis

Istanbul and the wider Marmara corridor dominate installed converting capacity, drawing on dense pharmaceutical clusters, e-commerce hubs, and organized retail headquarters.[3]Arvato Supply Chain Solutions Press Office, “Istanbul Fulfillment Center Launch,” Packaging Europe, packagingeurope.com Arvato’s flagship fulfillment site anchors a web of last-mile operators that demand customized cartons on a 24-hour cycle. Kocaeli’s industrial zones host GMP-certified plants, such as Nobel İlaç’s 40,000-square-meter facility, which drives consistent SBS demand for serialized pharma cartons. Bursa adds automotive component suppliers that ship parts in moisture-barrier boxboard, expanding industrial uptake within the Turkey folding carton market.

The Aegean region around Izmir serves as Turkey’s export gateway for olive oil, dried fruit, and confectionery, producing visually striking gift cartons that must pass European migration tests. Converters here emphasize FSC-certified fibers to meet European import requirements. Central Anatolia, led by Ankara, benefits from public sector procurement and quick-service restaurant rollouts. Lower labor costs encourage greenfield packaging sites, but recovered paper quality lags, complicating recycled-grade output. Southeastern and Eastern Anatolia remain underpenetrated due to limited organized retail and fragmented logistics.

Government incentives for regional manufacturing aim to shift capacity eastward, yet many converters hesitate until waste segregation infrastructure improves. Export backhauls to the Middle East and North Africa amplify carton flows from Izmir and Mersin ports, leveraging free trade agreements. Competitive pressure from Chinese board imports has thinned margins on outbound sales, yet proximity keeps Turkish suppliers cost-advantaged for short lead time orders. These geographic patterns create a multi-speed landscape inside the Turkey folding carton market, rewarding firms that balance domestic pull with export diversification.

Competitive Landscape

The field balances multinational scale and domestic agility. Mondi’s USD 70.8 million Olmuksan takeover in 2025 knit together nine factories into a platform targeting pharmaceutical and food converters and exploiting Turkey’s export corridors to the Middle East and North Africa.[4]Mondi Group Investor News, “Completion of Olmuksan Acquisition,” Mondi, mondigroup.com Despite revenue softness in H1 2025 due to pulp swings, the group’s integration unlocked broader grade availability, raising switching costs for brand owners. SCA Packaging, Tetra Pak, and Metsä Board compete on virgin fiber pedigree and on global supply alliances with consumer goods majors, challenging local independents for premium shelf space.

Domestic specialists carve niches. Dentaş Kağıt offers molded cellulose inserts for cosmetics, reducing the need for plastic trays. Korozo Ambalaj earned a CDP “A” climate score that resonates with multinational buyers seeking verifiable carbon credentials. Kâğıt Sanayi Ofset leverages rotary die-cutters to dominate shelf-ready boxes for discount grocers and is upgrading to low-VOC inks to reach D-level SYD status ahead of the 2030 deadline. Technology investment is a strategic divider: converters financing digital presses and energy-efficient dryers unlock green tax credits and gain emission headroom, a necessity after the Industrial Emissions Management Regulation tightened solvent limits.

Competitive intensity is amplified by Chinese exporting mills that flood Europe and Turkey with low-cost folding boxboard, depressing prices and testing loyalty to domestic supply chains. Integrated players counter through design services, shorter lead times and bilingual pre-press that overseas sellers cannot match. Rising capital needs for BAT retrofits and for smart packaging integration are nudging sub-scale operators toward mergers or orderly exits, driving moderate consolidation that reshapes the Turkey folding carton market landscape.

Turkey Folding Carton Industry Leaders

Tetra Pak International S.A.

Mondi plc

Kartonsan Karton Sanayi ve Ticaret A.Ş.

Dentaş Kağıt Sanayi A.Ş.

Konya Kağıt Sanayi ve Ticaret A.Ş

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CarrefourSA’s 1,250-store network was sold to A101 for USD 325 million, prompting accelerated rollout of shelf-ready cartons as the acquirer harmonizes merchandising.

- February 2026: Graphic Packaging Holding Company reported FY 2025 net sales of USD 8.61 billion and confirmed USD 1.67 billion invested in its Waco recycled board mill, signaling continued capital commitment to fiber-based packaging.

- September 2026: Kartonsan approved a 300 million TRY (USD 8.8 million) capital raise to shore up liquidity and fund SYD compliance projects.

- January 2025: Mondi completed the USD 70.8 million acquisition of Olmuksan, expanding to nine Turkish plants and 1,600 employees.

Turkey Folding Carton Market Report Scope

The report on Turkey's Folding Carton Market provides a comprehensive analysis of the market dynamics, trends, and growth opportunities. It examines the production, consumption, and demand for folding cartons across various industries, including food and beverage, healthcare, personal care, and others. The study covers the market's scope, including key drivers, challenges, and the competitive landscape, and offers insights into the forecast period and the factors influencing market growth.

The Turkey Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Turkey folding carton market?

The Turkey folding carton market size reached USD 310.94 million in 2026 and is projected to grow to USD 431.21 million by 2031 at a 6.76% CAGR.

Which material is gaining the most share in Turkish folding cartons?

Solid Bleached Sulfate leads with a 38.57% share in 2025 and is expanding fastest at an 8.63% CAGR, driven by premium cosmetics and pharmaceuticals that demand high-printability boards.

How are government incentives affecting folding carton converters?

Facilities that attain D-level SYD certification by 2030 qualify for green grants and tax relief, steering investment toward water-based flexographic and digital lines that comply with Turkey’s Industrial Emissions Management Regulation.

Why is digital printing growing in Turkish carton production?

E-commerce and retail-ready packaging require short runs and variable data; digital presses remove plate costs and meet low-VOC standards, resulting in an 8.84% CAGR for digital printing through 2031.

Which end-user segment will post the fastest growth?

E-commerce and retail-ready packaging is forecast to lead with an 8.39% CAGR as online retailers demand right-sized, branded cartons that enhance unboxing experiences.

What competitive moves are reshaping the market?

Mondi’s USD 70.8 million Olmuksan acquisition, Kartonsan’s TRY 300 million (USD 8.8 million) recapitalization and Chinese board import pressures are accelerating consolidation and technology upgrades among Turkish converters.

Page last updated on: