Bangladesh Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

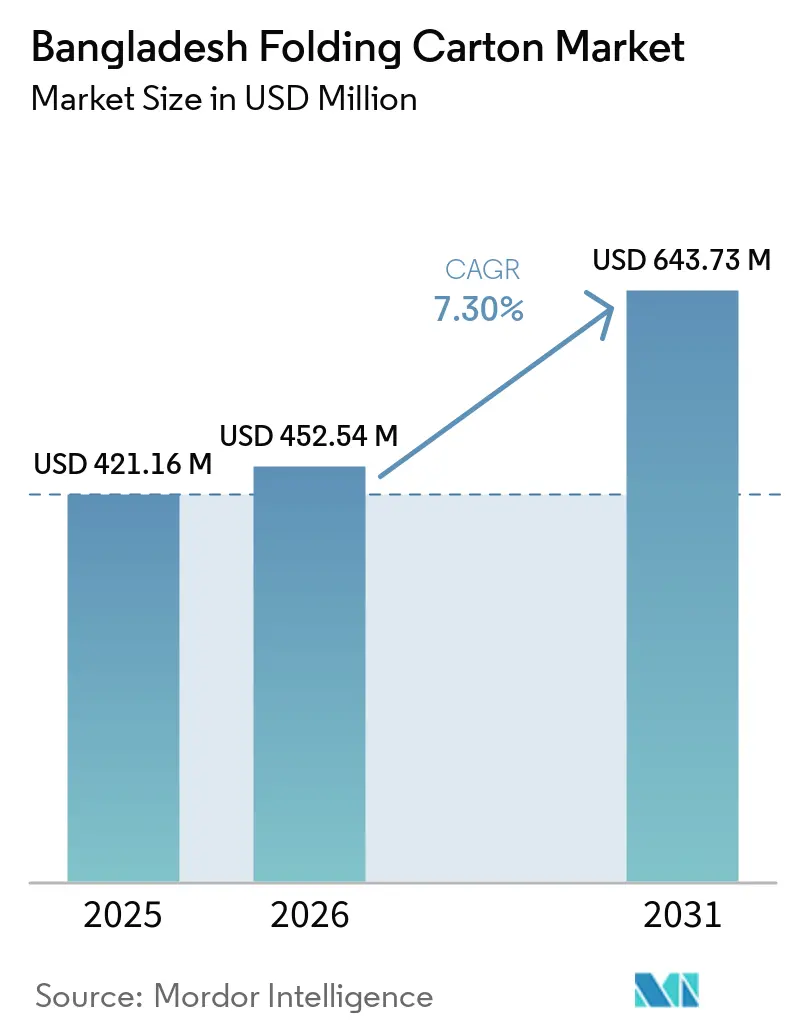

| Base Year Market Size (2025) | USD 421.16 Million |

| Market Size (2026) | USD 452.54 Million |

| Market Size (2031) | USD 643.73 Million |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

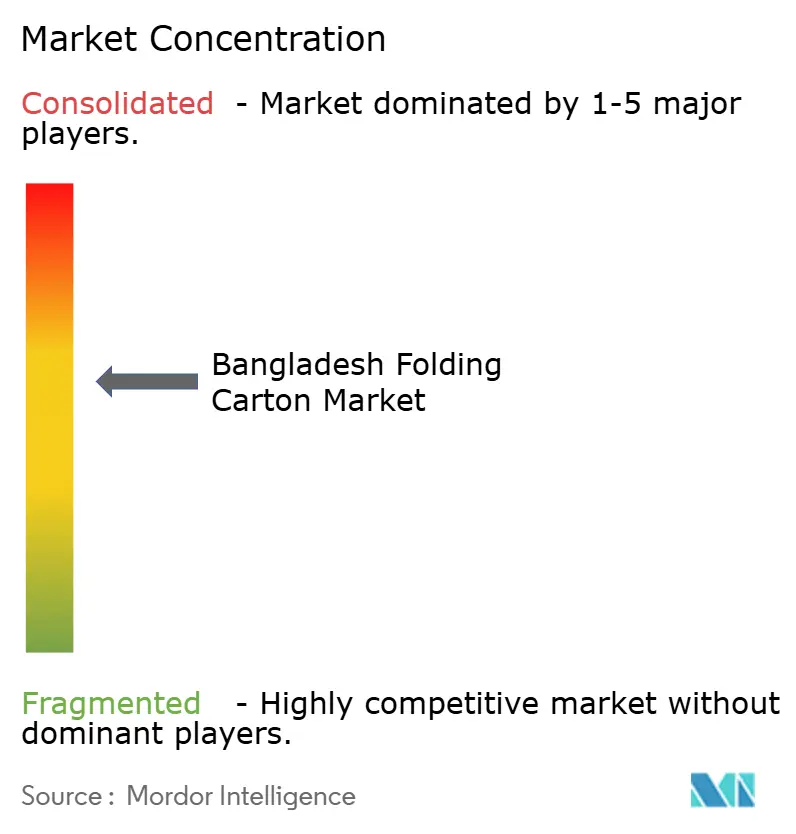

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Folding Carton Market Analysis by Mordor Intelligence

The Bangladesh folding carton market size is expected to grow from USD 421.16 million in 2025 to USD 452.54 million in 2026 and is forecast to reach USD 643.73 million by 2031 at a 7.30% CAGR over 2026-2031. Demand is pivoting from commodity garment accessories toward higher-margin FMCG, pharmaceutical and e-commerce applications, and converters are scrambling to add barrier-coated grades and variable-data capacity. Regulatory bans on 17 single-use plastic items, rising per-capita income, and a 6% cash incentive on paper-product exports are expanding the Bangladesh folding carton market footprint beyond captive domestic buyers into South Asian and Middle Eastern customers. Technology spending is tilting toward digital presses that support short-run personalization, while material substitution favors Solid Bleached Sulfate for premium packs. Power-supply instability and pulp-price volatility temper growth, yet backward integration by large local groups and foreign joint ventures is lifting operating scale and positioning the Bangladesh folding carton market for export-oriented growth.

Key Report Takeaways

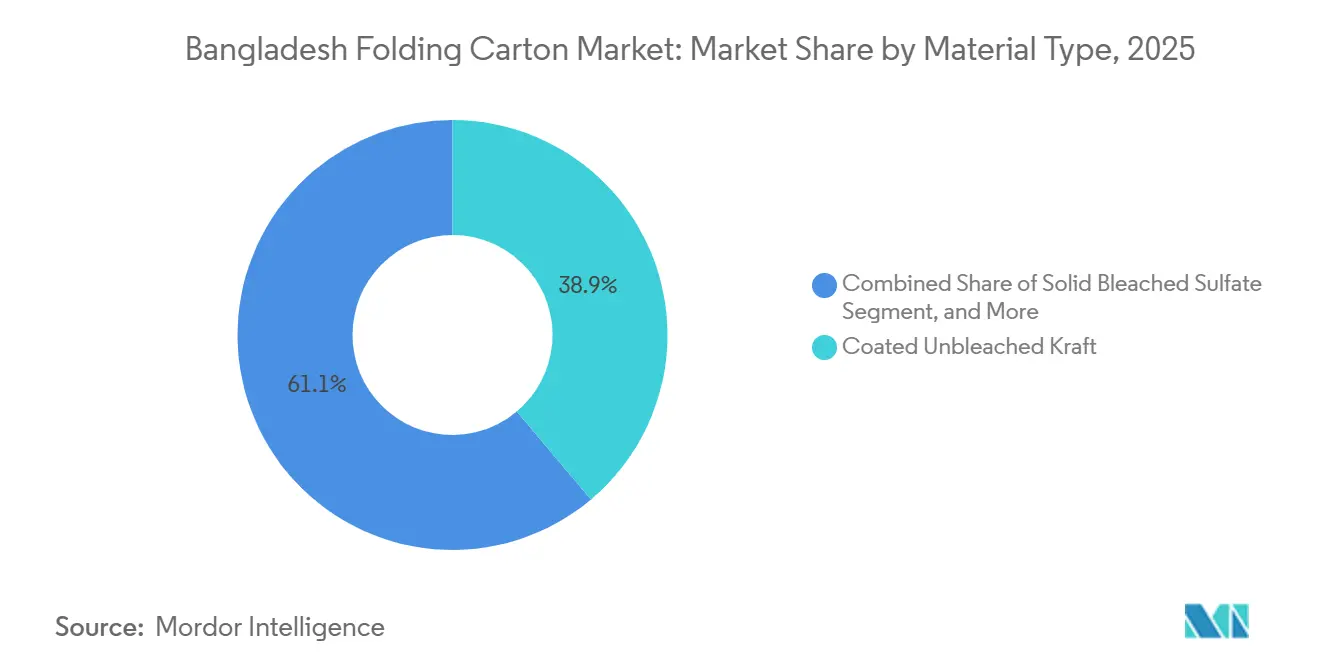

- By material type, coated unbleached kraft captured with 38.87% of the Bangladesh folding carton market share in 2025.

- By printing technology, the Bangladesh folding carton market size for digital printing is projected to grow at a 8.64% CAGR to 2031.

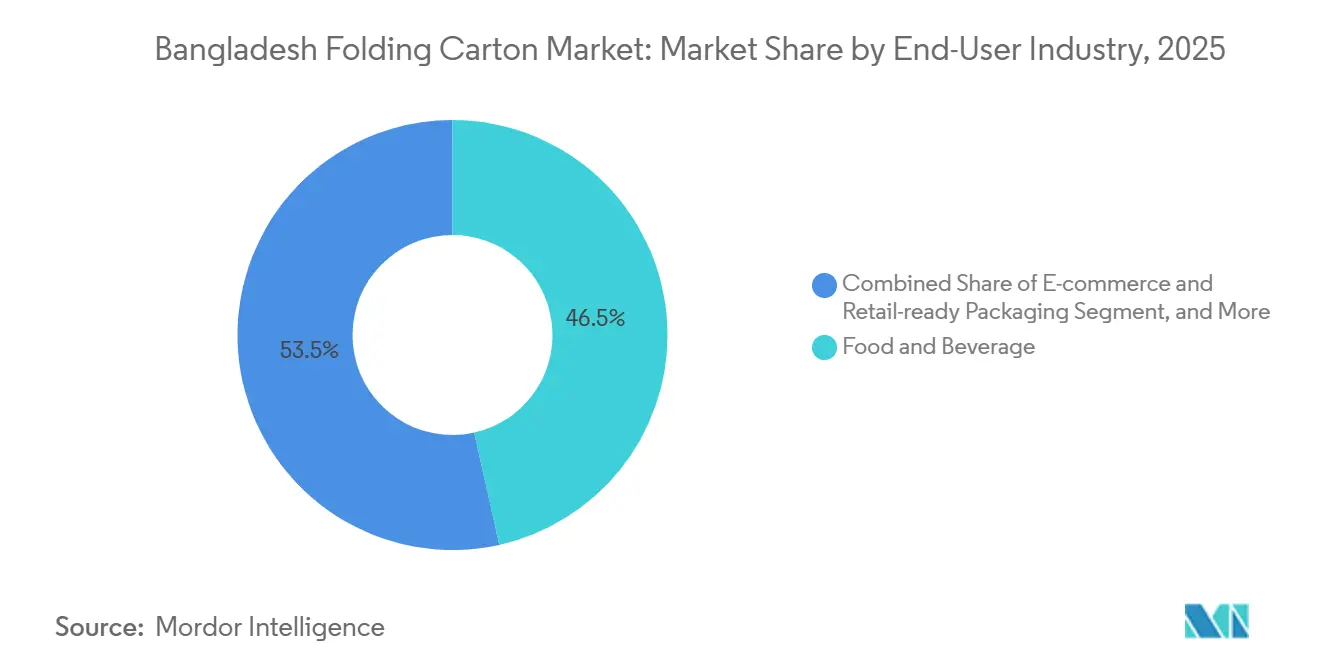

- By end-user industry, the food and beverage industry captured 46.52% of the Bangladesh folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bangladesh Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Ready-to-Eat Food Sector | +1.4% | National, metro clusters | Medium term (2-4 years) |

| Government Incentives for Export-Oriented Packaging | +1.1% | National, EPZs | Medium term (2-4 years) |

| Growing E-commerce Penetration | +1.3% | National, Dhaka-led | Short term (≤ 2 years) |

| Shift Toward Eco-Friendly Substrates | +1.0% | National, urban focus | Short term (≤ 2 years) |

| Rising Disposable Income for Personal Care | +0.8% | National, urban middle | Long term (≥ 4 years) |

| Capacity Expansion by Multinational FMCG | +0.9% | National, industrial belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Ready-to-Eat Food Sector

Urban packaged-food sales climbed from USD 4.8 billion in 2024 to a projected USD 5.8 billion by 2030, lifting demand for tamper-evident, grease-resistant cartons that withstand humid shelf conditions. Small-pack SKUs now account for a larger share of revenue for major processors, forcing converters to supply high-definition litho or digital prints on Solid Bleached Sulfate boards. Retailers also insist on QR-code traceability, rewarding converters that are certified to the BDS EN 12546 food-contact rules. This pull effect reinforces volume growth across the Bangladesh folding carton market.

Government Incentives for Export-Oriented Packaging Manufacturers

A 6% cash rebate on paper-product exports and a 10% rebate on jute-based packs lower the landed cost in duty-heavy Gulf and African markets. New EPZ approvals worth USD 480 million include several folding-carton projects, yet a 5% duty on raw-material imports versus zero on bonded finished cartons creates an arbitrage that undermines full backward integration. Resolving this gap would unlock additional gains in the Bangladesh folding carton market.

Growing E-commerce Penetration and Last-Mile Delivery Growth

Domestic GMV rose from USD 6.9 billion in 2023 to USD 7.5 billion in 2024, on track for USD 9.8 billion by 2028. Each online order uses nearly six times as many cartons as a store sale, and couriers now demand edge-crush-tested, retail-ready designs. Digital presses that print variable SKU data in hours rather than days are becoming essential, accelerating the transition of the Bangladesh folding carton market to short-run models.

Shift Toward Eco-Friendly Substrates Due to Single-Use Plastic Restrictions

The 2024-2025 plastic ban redirected fast-food and takeaway chains to Coated Unbleached Kraft, prized for its brown eco-aesthetic and grease resistance.[1]Bangladesh Standards and Testing Institution, “Annual Report 2024-2025,” bsti.portal.gov.bd While enforcement varies by city, multinational FMCG firms are standardizing on recyclable structures nationwide. Converters investing in water-based coatings and compostable adhesives gain preferred-supplier status and help the Bangladesh folding carton market capture share from plastic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Pulp Prices | -0.9% | Global import exposure | Short term (≤ 2 years) |

| High Capital Investment for Digital Presses | -0.6% | National, mid-tier firms | Medium term (2-4 years) |

| Frequent Power Outages | -1.2% | National, non-EPZ zones | Short term (≤ 2 years) |

| Limited Availability of Food-Grade Inks | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Pulp Prices

Benchmark pulp traded at USD 1,170 per tonne in Q1 2025, and Bangladeshi converters import 80% of their fiber, exposing them to price swings and currency risk.[2]SGS, “Bangladesh consults overdraft law on food contact materials,” sgs.com Fixed-price FMCG contracts absorb these costs, compressing margins and slowing reinvestment. Recycled-fiber lines now blend up to 30% recovered content, yet informal waste collection limits scale, keeping the Bangladesh folding carton market tethered to volatile imports.

Frequent Power Outages Causing Production Downtime

Gas shortages drove 7-9-hour daily load shedding outside Dhaka in April 2025, cutting packaging output by 25-30% and idling dozens of paper mills. While EPZ plants enjoy a near-continuous supply, legacy sites face diesel-generator costs that erode competitiveness. Unless grid reliability improves, energy risk will continue to shave growth from the Bangladesh folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Dominates While Premium Substrates Accelerate

Coated Unbleached Kraft secured 38.87% of Bangladesh's folding carton market share in 2025, propelled by takeaway food, bakery, and e-commerce shippers. Solid Bleached Sulfate, though smaller, is climbing at 8.48% CAGR because cosmetics and pharma brands specify bright-white boards with foil-stamping compatibility. Folding Boxboard tracks the overall Bangladesh folding carton market size, supplying cereal and detergent packs, whereas White Line Chipboard captures budget footwear and appliance inserts. Recycled-fiber capacity from new Andritz lines supports 30% post-consumer blends, signaling a gradual shift toward import substitution.

Brands setting 30%-recycled targets will push mills to formalize waste-paper collection and further deepen the Bangladesh folding carton market. Converters that certify material batches in line with forthcoming Food Contact Materials rules gain a pricing edge. Solid Bleached Sulfate also benefits as pharmaceutical firms adopt blister-and-carton combinations that need migration-tested substrates. Mono-material barrier grades are in pilot stages as converters chase plastic-free mandates, providing upside to the Bangladesh folding carton market size once scale economics improve.

By Printing Technology: Lithography Leads but Digital Scales Short Runs

Lithographic presses held 47.53% of Bangladesh's folding carton market share in 2025 due to cost efficiency on million-unit FMCG runs. Digital printing, growing at a 8.64% CAGR, meets the needs of e-commerce sellers who require 500-unit lots with SKU-specific QR codes. Flexography covers corrugated and industrial work, while gravure remains in ultra-long tobacco and cosmetics orders. Digital penetration is expected to jump once bank guarantees or FMCG co-investment models mature.

Credit constraints impede mid-tier firms from buying USD 2-3 million digital lines, bifurcating the Bangladesh folding carton market between capital-rich groups and plate-bound independents. BSTI’s national QR-code verification program is nudging brands toward digital presses that handle variable data seamlessly. Hybrid HD-flexo upgrades are narrowing quality gaps, but until sector-priority lending emerges, litho will dominate medium-run work.

By End-User Industry: Food Anchors While E-commerce Sprints

Food and beverage accounted for 46.52% of Bangladesh's folding carton market in 2025, led by instant noodles, biscuits, and dairy. Each shift to single-serve packs multiplies carton demand, and tighter BSTI oversight is raising board-quality specifications. E-commerce and retail-ready packaging, projected to grow at an 8.86% CAGR, is the fastest riser because every online order triggers nearly 2 cartons, and couriers require edge-crush-validated shippers. Healthcare and pharmaceuticals add stable, quality-driven demand as exporters integrate carton making in-house and seek migration-tested boards.

Personal care remains a premium niche: Solid Bleached Sulfate cartons with foil and tactile varnish command 10-15% premiums, and converters with OEKO-TEX-approved inks win long-term supply contracts. Tobacco volume is flat, constrained by 75% health-warning rules that compress branding space, but nicotine-pouch investment may cushion declines. Net effect keeps food the anchor, but e-commerce and pharma will chip away at share toward 2031.

Geography Analysis

Most folding-carton capacity clusters along the Dhaka-Gazipur-Narayanganj belt and Chittagong port, jointly hosting about 70% of output. Plastic bans are enforced more strictly in these metros, accelerating the shift in Bangladesh's folding carton market from polystyrene to paper. EPZs attract new plants because they guarantee 98% power uptime and duty concessions, whereas non-EPZ mills suffer blackouts that crimp productivity.

Secondary cities such as Sylhet, Rajshahi, and Khulna trail in regulatory enforcement, creating dual-speed adoption, yet new BSTI regional labs in Chittagong and Khulna cut test-cycle times and lower compliance costs.[3]BSTI, “List of Bangladesh Standards on Agricultural and Food Products,” bsti.portal.gov.bd This decentralization may slow capacity drift to Dhaka, helping spread Bangladesh's folding carton market investment nationwide. Export orders increasingly ship from Chittagong, where 24-hour customs and proximity to maritime lanes shave off lead times compared to Indian competitors.

Yet, disparities in raw-material duties continue to drive numerous high-value jobs overseas. Addressing this policy challenge could tap into the USD 50 billion export potential highlighted by the accessories association, solidifying a genuinely national folding carton market in Bangladesh. Resolving these issues would also enhance the competitiveness of local manufacturers in the global market.

Competitive Landscape

Roughly eight firms control one-half of national volume, leaving a long tail of small converters. Groups such as Akij, Bengal, Meghna, and Partex pursue backward-integrated pulp, film, and ink assets to hedge against input volatility, while foreign entrants bring recycling technology and global buyer links. Akij Biax Films runs a 90,000-tonne film complex and already exports 40% of output, though bonded-import tax breaks for finished films dampen utilization.

Mainetti’s 85,000-square-foot Dhaka plant targets 1.3 million flexible bags a day and will add paper banderoles and RFID tags, signaling rising vertical integration between garment accessories and folding cartons.[4]Mainetti, “Mainetti expands Bangladesh operations,” mainetti.com TAM-Meghna’s USD 10 million hanger venture illustrates niche diversification and circular-economy positioning. Compliance costs tied to mid-2026 food-contact rules will likely spur consolidation, and converters with accredited labs and QR-coded traceability already command premium contracts.

Strategic focus now splits: capacity expansion in lower-cost tier-two cities and high-spec upgrades near Dhaka for multinational audits. Digital embellishment, migration-tested materials, and mono-material barrier boards are key battlegrounds. As finance and regulation favor scale, the Bangladesh folding carton market is on course for higher concentration. Companies are increasingly focusing on sustainable packaging solutions to align with global environmental standards.

Bangladesh Folding Carton Industry Leaders

Meghna Group of Industries

Tetra Pak International S.A.

Huhtamäki Oyj

Mohona Packages (BD) Limited

PM Labels Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: TAM Hangers and Meghna Group opened a USD 10 million joint-venture hanger factory in Mirzapur, planning to scale from 16 to 100 molding machines within five years and target 50% of the USD 300-400 million hanger market.

- May 2026: The Dhaka Industrial Packaging Expo hosted 130 companies from 12 countries; the government named paper packaging “Product of the Year 2026.

- April 2026: The Bangladesh Economic Zones Authority cleared Philip Morris International to build a nicotine-pouch plant in Narayanganj, creating new small-format carton demand under tighter 75% health-warning rules.

- October 2025: Andritz installed two 150-tonne-per-day recycled-fiber lines at Lipy Paper Mills, introducing 30% post-consumer pulp blends to local folding-boxboard.

Bangladesh Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton market in Bangladesh, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton market in Bangladesh.

The Bangladesh Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the Bangladesh folding carton market?

The market reached USD 452.54 million in 2026 and is projected to grow to USD 643.73 million by 2031, according to Mordor Intelligence.

Which material type is expanding fastest in Bangladeshi folding cartons?

Solid Bleached Sulfate is advancing at an 8.48% CAGR through 2031, driven by cosmetics and pharmaceutical demand for bright-white, migration-tested boards.

How are single-use plastic bans changing packaging choices?

The 2024-2025 ban on 17 plastic items is steering restaurants and snack brands toward grease-resistant Coated Unbleached Kraft and molded-fiber cartons, accelerating paper substitution.

Why is digital printing adoption rising among local converters?

E-commerce sellers require short-run, variable-data cartons, and digital presses eliminate plate costs and enable same-day turnaround, leading to an 8.64% CAGR for the technology segment.

What production challenge do converters face with the power supply?

Gas shortages cause 7-9-hour daily load-shedding in non-EPZ zones, forcing reliance on diesel generators and cutting output by as much as 30%.

How do government export incentives affect competitiveness?

A 6% cash rebate on paper-product exports lowers landed costs in Gulf and African markets, but a 5% duty on raw materials versus zero on bonded finished cartons still distorts the playing field.

Page last updated on: