Egypt Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

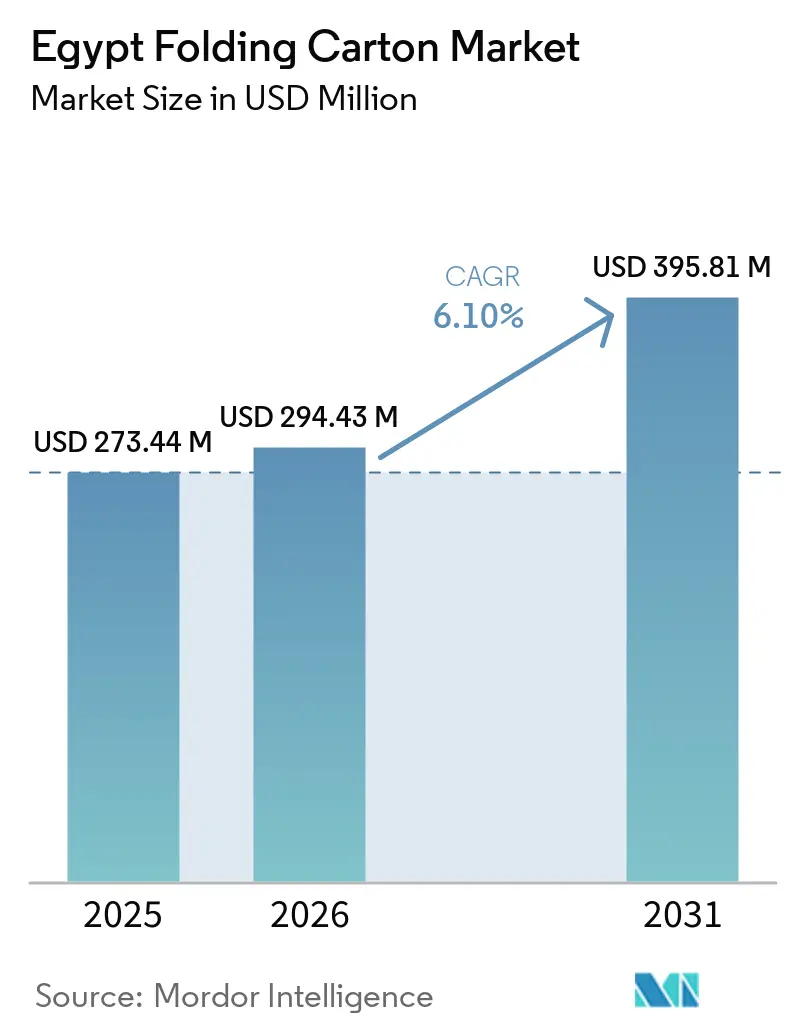

| Base Year Market Size (2025) | USD 273.44 Million |

| Market Size (2026) | USD 294.43 Million |

| Market Size (2031) | USD 395.81 Million |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

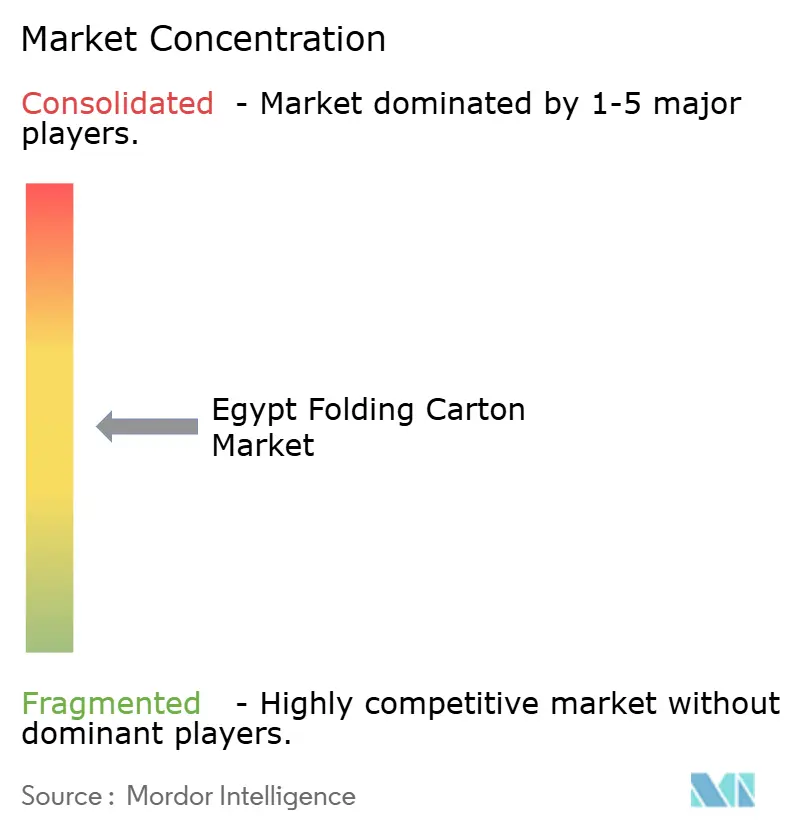

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Folding Carton Market Analysis by Mordor Intelligence

The Egypt folding carton market size is expected to be USD 273.44 million in 2025, USD 294.43 million in 2026, and reach USD 395.81 million by 2031, growing at a CAGR of 6.1% from 2026 to 2031. Rising exports of packaged fast-moving consumer goods, duty-free access to European Union markets, and a cost base largely denominated in Egyptian pounds are combining to lift converter margins and spur capital investment. Local producers are adding high-speed digital presses to serve short-run personalized orders placed by e-commerce sellers, while quick-service restaurants are switching to grease-resistant folding cartons that comply with Egypt’s plastic-reduction decree. Extended Producer Responsibility fees on plastic bags, along with upcoming pharmaceutical serialization rules, are accelerating demand for compliance-grade cartons with tamper-evident features and data-matrix codes. Although imported virgin pulp price volatility and currency swings remain near-term headwinds, sustained inflows of foreign direct investment and green-labeling initiatives are underpinning the medium-term outlook for the Egypt folding carton market.

Key Report Takeaways

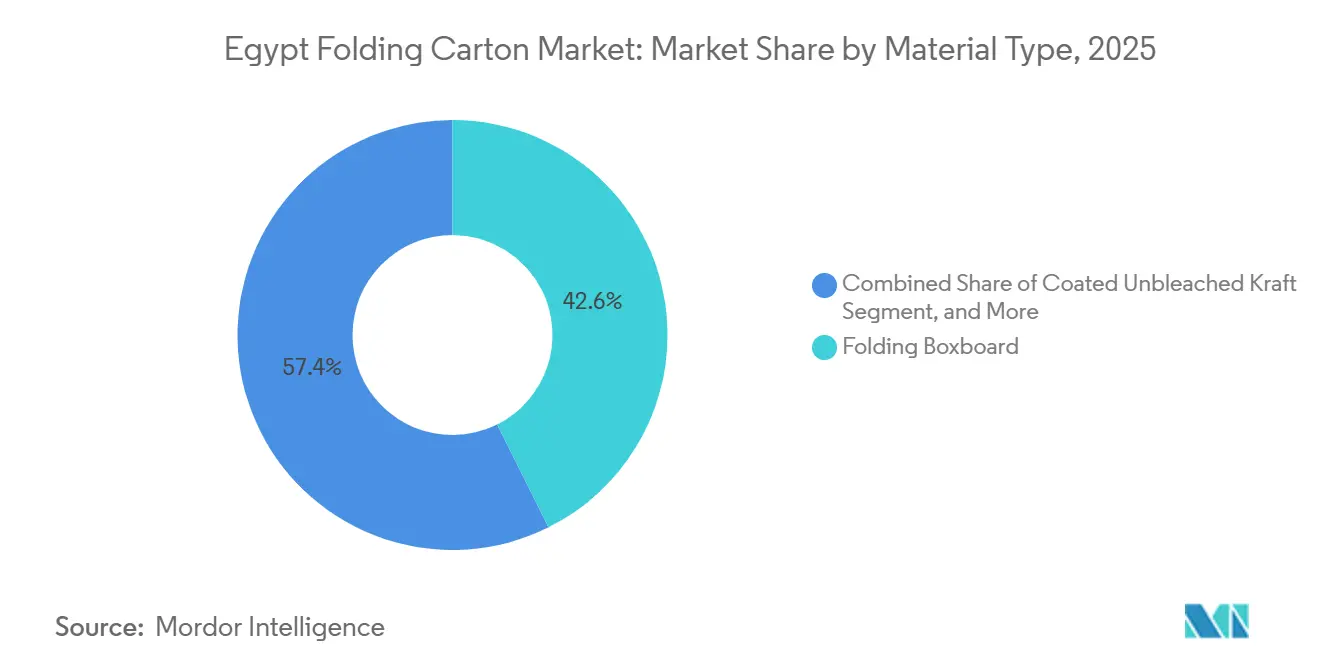

- By material type, folding boxboard captured with 42.63% of the Egypt folding carton market share in 2025.

- By printing technology, the Egypt folding carton market size for digital printing is projected to grow at a 8.61% CAGR to 2031.

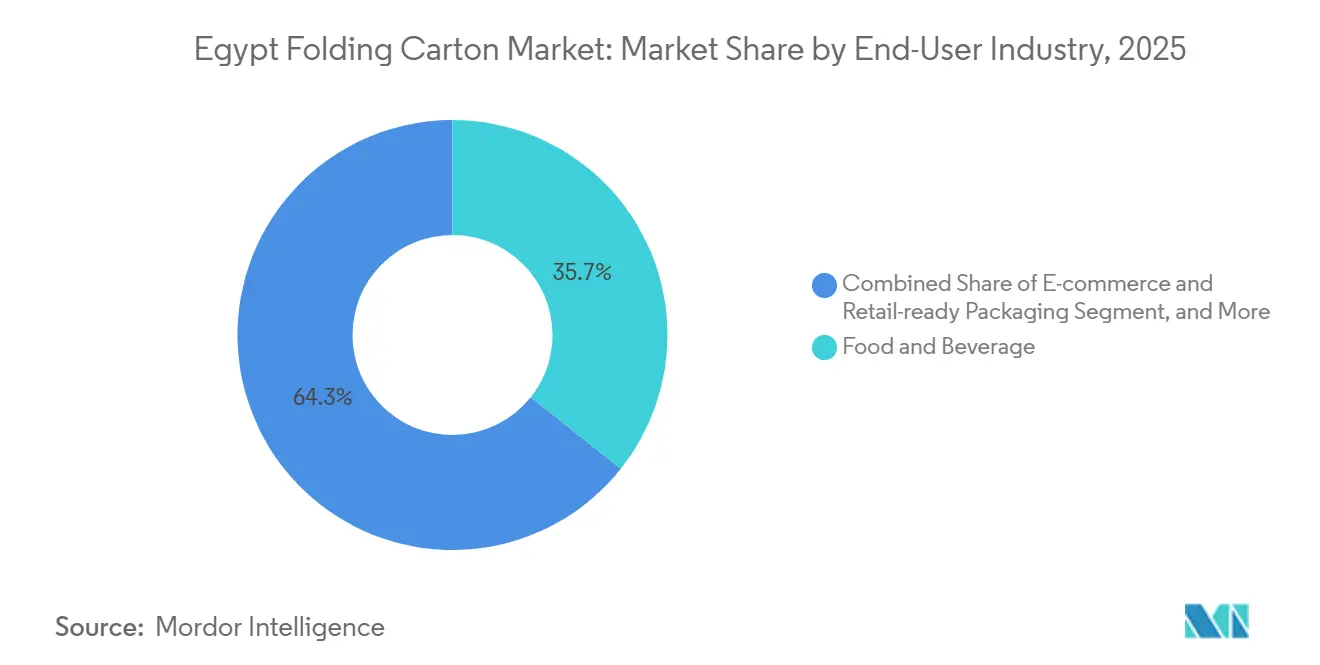

- By end-user industry, the food and beverage industry captured 35.69% of the Egypt folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Penetration Boosting Secondary Packaging Demand | +1.2% | National, concentrated in Greater Cairo, Alexandria, and Giza | Medium term (2-4 years) |

| Expanding Food Delivery and Takeaway Culture in Urban Areas | +0.9% | National, early gains in Cairo, Alexandria, Giza | Short term (≤ 2 years) |

| Government Plastic-Reduction Policies Favoring Recyclable Cartons | +1.1% | National | Medium term (2-4 years) |

| Investments in High-Speed Digital Printing by Local Converters | +0.7% | National spillover to regional export markets | Medium term (2-4 years) |

| Growth of Pharmaceutical Exports Requiring Compliance Packaging | +0.8% | National, export-oriented to the Middle East, Africa, and Europe | Long term (≥ 4 years) |

| Tourism Recovery Driving Souvenir Consumer Packaged Goods | +0.5% | National, focused on Cairo, Luxor, Aswan, and Red Sea resorts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Penetration Boosting Secondary Packaging Demand

Egypt’s e-commerce packaging market expanded from USD 1.11 billion in 2024 to a projected USD 4.17 billion by 2033, at a 15.87% compound annual growth rate, as smartphone use and digital payment apps proliferated.[1]E-Commerce Association of Egypt, “Egypt E-Commerce Market Report 2024,” ecommerceegypt.org Folding cartons dominate secondary packaging for electronics, apparel, and personal-care orders shipped by platforms such as Jumia and Noon, because standardized box sizes simplify fulfillment-center stacking and reduce damage in transit. Talabat recorded a gross merchandise value of USD 2.5 billion in the fourth quarter of 2025, up 21% year on year, highlighting the spillover effect of food delivery on quick-commerce packaging needs. Converters rely on high-speed digital presses to turn around small batches that carry variable barcodes or seasonal graphics, eliminating the plate-making delays of offset printing.

Expanding Food Delivery and Takeaway Culture in Urban Areas

Quick-service restaurants and cloud kitchens multiplied across Cairo, Alexandria, and Giza in 2025, driven by millennial disposable income and preference for off-premise dining. Grease-resistant folding cartons now replace polystyrene clamshells for fried chicken, pizza, and shawarma, as they help cover Extended Producer Responsibility fees that raise the cost of single-use plastics. Coated Unbleached Kraft, forecast to grow 8.37% through 2031, offers oil- and moisture-barrier protection while remaining recyclable, aligning with multinational restaurant sustainability targets. Huhtamaki reduced annual energy consumption by 5,000 megawatt-hours at its Cairo plant after installing a water-cooled chiller in 2025, underscoring how converters link operational efficiency with environmental credentials. Near-term growth is concentrated in metropolitan areas, but expanding intercity bus networks are extending takeaway demand to secondary cities such as Mansoura and Tanta.

Government Plastic-Reduction Policies Favoring Recyclable Carton

Decree 662/2025 imposes a USD 1.21 per kilogram fee on plastic bags, creating a cost differential that effectively subsidizes fiber-based alternatives. In parallel, the United Nations Industrial Development Organization's green-labeling scheme now certifies folding-carton packages that meet recycled-content thresholds, giving folding-carton producers a marketing advantage. National Printing recycled roughly 125,000 tonnes of paper in 2024, positioning the company to meet ISO 14001 procurement standards demanded by global FMCG brands. Enforcement will tighten over the next two to four years, raising penalties for non-compliance and accelerating the migration of substrates toward recyclable cartons.

Investments in High-Speed Digital Printing by Local Converters

Future Digital Pack installed Egypt’s first HP Indigo 20000 web press, enabling profitable runs as short as 500 units for personalized promotions. Digital printing is projected to expand at a 8.61% CAGR through 2031, propelled by direct-to-consumer brands that value rapid graphic changes and inventory-light supply chains. BOBST’s February 2026 Cairo roadshow drew more than 200 converters, signaling supplier confidence in the market’s capital-expenditure cycle. Mid-tier firms such as El Alamein Pack have coupled new Komori GL640 offset presses with digital overprint stations, blending lithographic economies with variable-data flexibility. As utilization surpasses 70%, converters cut setup waste and reduce volatile organic compound emissions, supporting both profitability and environmental objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Virgin Pulp Prices | -0.8% | National, linked to global commodity markets | Short term (≤ 2 years) |

| Competition from Flexible Plastic Pouches in Low-Cost Applications | -0.6% | National, concentrated in food and household segments | Medium term (2-4 years) |

| Foreign-Exchange Fluctuations Raising Printing Equipment Capex | -0.5% | National, affecting import-dependent converters | Short term (≤ 2 years) |

| Limited Domestic Recycling for High-Quality White Grades | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Virgin Pulp Prices

Egypt recorded a kraft paper trade deficit of USD 181 million in 2022, making converters vulnerable to Scandinavian energy price spikes and Brazilian eucalyptus shortfalls that kept global pulp prices firm through 2025. Spot price jumps compress margins for converters serving price-sensitive dry-food and industrial segments that lack long-term supply contracts. Uniboard mitigates exposure by sourcing wastepaper domestically, yet premium white-top grades still require virgin-pulp blends to satisfy pharmaceutical brightness standards. Currency depreciation amplifies cost swings because pulp invoices are denominated in euros or U.S. dollars, while carton sales are often in Egyptian pounds. Until domestic de-inking lines scale up, converters will continue to wrestle with short-term price volatility that dampens investment appetite.

Competition from Flexible Plastic Pouches in Low-Cost Applications

Stand-up pouches can undercut folding-carton unit costs by up to 40% for spices, condiments, and single-serve beverage powders, thanks to rapid changeovers and efficient material use. Huhtamaki’s EUR 23 million (USD 25 million) flexible-packaging plant in 6th of October City exemplifies how multinationals hedge substrate risk by operating both rigid and flexible assets. If EPR penalties do not fully bridge the cost gap, brand owners in low-margin segments may persist with plastic formats despite recyclability concerns. Folding-carton producers respond with hybrid trays that combine paperboard rigidity and film lids, yet such designs demand co-investment from brand owners and consumer education on end-of-life sorting. The medium-term restraint will linger until fiber substrates match the price-performance equation of flexible laminates in value-conscious applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Boxboard Grades Consolidate Leadership

Folding Boxboard captured 42.63% of the Egypt folding carton market share in 2025, reflecting its stronghold in pharmaceutical blister backers, cosmetic sets, and premium confectionery sleeves. The grade’s high stiffness-to-weight ratio lets converters down-gauge board calipers without compromising crush resistance, which helps offset virgin-pulp price spikes. Coated Unbleached Kraft is projected to register an 8.37% CAGR through 2031, fueled by quick-service restaurants that prefer grease-resistant takeaway boxes aligned with plastic-reduction rules.

Solid Bleached Sulfate remains the substrate of choice for luxury electronics where embossing and foil stamping reinforce brand equity, yet growth is capped by corporate mandates favoring recycled content. White Line Chipboard fills cost-sensitive niches, such as dry breakfast-cereal cartons, leveraging domestic waste paper to undercut virgin grades and stabilize margins when foreign-exchange volatility inflates import bills. Other material types, including metalized and holographic boards, serve anti-counterfeiting needs in tobacco and spirits, although volumes remain small relative to mainstream grades.

By Printing Technology: Digital Presses Accelerate Adoption Curve

Lithographic printing accounted for 48.15% of the Egyptian folding carton market in 2025, thanks to its wide color gamut, tight registration, and cost efficiency above 10,000 sheets. Converters run six-color offset lines with inline aqueous coaters to meet pharmaceutical clean-room audit requirements and cosmetic-brand gloss standards. Future Digital Pack’s HP Indigo 20,000 web press supports variable barcodes and multiple language versions in the same job, catering to exporters shipping to Africa, Europe, and the Gulf.[2]HP Inc., “HP Indigo 20000 Digital Press Installation in Egypt,” hp.com Digital printing, however, is set to advance at a 8.61% CAGR through 2031 as e-commerce sellers seek print-on-demand cartons to lower inventory carrying costs.

Flexographic presses hold share in micro-flute corrugated post-print and beverage carriers, while gravure presses serve long-run confectionery cartons, where cylinder amortization remains attractive. Screen units apply tactile varnishes and cold-foil units add metallic flashes, differentiating premium personal-care packs on retail shelves. Cost convergence between offset and digital remains the pivot variable. Click charges on liquid-toner presses run three to five times higher than offset ink on a coverage-adjusted basis, restraining digital use to SKUs that benefit from personalization, A/B marketing tests, or multilingual compliance.

By End-User Industry: E-Commerce Tilts the Demand Mix

Food and Beverage accounted for 35.69% of the Egypt folding carton market in 2025, encompassing dairy sleeves, frozen-food boxes, and beverage multipacks. Quick-service chains now specify grease-resistant board and moisture-proof coatings that survive hot holding cabinets, creating a technical moat for converters with in-house formulation expertise. E-commerce and retail-ready packaging will post 7.84% growth through 2031 as online grocery portals standardize secondary packaging to cut last-mile damage. Tamper-evident tear strips, double-wall crash locks, and easy-return perforations are becoming standard requirements for platform sellers.

Personal Care and Cosmetics drive demand for soft-touch coatings, spot UV, and pastel substrates that amplify shelf appeal in pharmacy chains and duty-free outlets. Electrical and Electronics cartons include electrostatic-discharge liners and foam inserts, protecting fragile circuit boards shipped by exporters in the New Administrative Capital technology park. The gifts and souvenirs vertical is rebounding as inbound tourism rises, requiring bespoke die-cuts for papyrus scrolls, spice assortments, and artisan soaps sold in Khan el-Khalili and Red Sea resorts.

Geography Analysis

Greater Cairo, Alexandria, and the Nile Delta corridor anchor more than 70% of Egypt folding carton market demand and production capacity. National Printing operates plants in Obour and Sadat cities, leveraging proximity to multinational FMCG distribution centers and skilled print labor pools. Huhtamaki’s EUR 24 million (USD 26 million) molded-fiber plant in Sadat City, scheduled to start up in August 2026, will add 61 jobs and supply egg cartons and cup carriers to local and export customers.

The Suez Canal Economic Zone is emerging as an export platform, with EROĞLU Global allocating USD 175 million to a Qantara West packaging hub that exploits zero-tariff access to the European Union. Alexandria port funnels European shipments, while Ain Sokhna channels cargo to Gulf Cooperation Council markets, allowing converters to hedge currency swings by billing exports in hard currencies. Upper Egypt and Red Sea governorates show rising carton demand from tourism and fresh-produce exporters. Luxor, Aswan, and Hurghada retailers source decorative cartons from Cairo, absorbing high freight costs that shrink margins.

Gulf Pack’s new 5,000-square-meter factory in 6th of October City targets a USD 51 million in sales by end-2026, adding capacity to serve both metropolitan and provincial customers.[3]Gulf Pack, “Sales Target Corporate Announcement,” gulfpack.com Cepack Group’s third BHS corrugator, operational in early 2026, lifts output 70% and supplies micro-flute sheets to folding-carton converters across the Delta and Upper Egypt, trimming dependence on imported containerboard. New Administrative Capital logistics hubs promise shorter lead times to emerging governorates, expanding the geographic footprint of the Egypt folding carton market.

Competitive Landscape

Roughly 1,000 large factories and more than 5,000 small and medium enterprises populate the Egypt folding carton market, yet consolidation accelerated after National Printing’s oversubscribed USD 14.5 million initial public offering in August 2025. Multinationals such as Huhtamaki and Mondi rely on global procurement networks and proprietary grease-barrier chemistries to win high-spec pharmaceutical and quick-service restaurant contracts.[4]Daily News Egypt, “Huhtamaki Egypt to Invest EGP 1.47 bn in Sustainable Packaging Plant,” dailynewsegypt.com The company’s vertically integrated model spans duplex board, folding cartons, corrugated boxes, and cup stock, capturing value across the supply chain and buffering raw-material shocks.

Mid-tier converters compete on rapid turnaround, using digital presses and laser-cutters to supply regional cosmetics and artisanal food brands that cannot meet multinational minimum-order quantities. Technology adoption separates leaders from laggards. Future Digital Pack’s HP Indigo 20,000 and GreenPack’s solvent-free plate processor demonstrate capital commitments that cut setup waste and volatile organic compound emissions, aligning with brand-owner environmental, social, and governance scorecards.

Foreign direct investment projects, such as UFlex’s USD 200 million PET-chip and aseptic-packaging complex, anchor backward integration and introduce advanced lamination technology to the domestic ecosystem. Flexible-packaging specialists blur substrate lines by marketing paperboard trays sealed with thin film lids, forcing rigid-carton incumbents to co-invest in heat-sealing modules to retain share. Competitive intensity is moderated by regulatory compliance costs. Decree-mandated pharmaceutical serialization and EPR levies on plastics favor well-capitalized converters that can certify tamper-evidence and recyclability attributes. Small firms lacking track-and-trace infrastructure face potential exit or acquisition.

Egypt Folding Carton Industry Leaders

Graphic Packaging Holding Company

Huhtamaki Oyj

Tetra Pak Egypt Ltd.

Mondi plc

Gulf Carton Factory Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cepack Group signed with BHS Corrugated to install a third corrugator line, boosting capacity 70%, with start-up slated for early 2026.

- February 2026: BOBST hosted a Cairo roadshow showcasing new flexographic, digital, and lamination equipment to over 200 Egyptian converters.

- February 2026: Sealed Air Corporation’s USD 10.3 billion acquisition by Clayton, Dubilier and Rice cleared regulatory review, creating a global packaging giant with Egyptian operations.

- August 2025: National Printing completed an EGP 450 million (USD 14.5 million) IPO, oversubscribed 23.6 times, earmarking proceeds for acquisition and greenfield expansion.

Egypt Folding Carton Market Report Scope

The scope of this report covers the analysis of the folding carton market in Egypt. Folding cartons are paper-based packaging solutions widely used across various industries, including food and beverage, personal care, pharmaceuticals, and others. These cartons are lightweight, customizable, and recyclable, making them a preferred choice for sustainable packaging. The report examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future prospects.

The Egypt Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Egypt folding carton market and how fast is it growing?

The market stands at USD 294.43 million in 2026 and is projected to reach USD 395.81 million by 2031, registering a 6.1% CAGR over 2026-2031, according to Mordor Intelligence.

Which material type commands the largest share in Egypt’s folding carton space?

Folding Boxboard led with 42.63% share of the Egypt folding carton market in 2025, driven by pharmaceutical and cosmetic applications.

How quickly will digital printing gain ground in Egyptian carton production?

Digital printing is forecast to grow at an 8.61% CAGR through 2031 because e-commerce sellers and direct-to-consumer brands demand short runs and personalization.

What regulations are accelerating the switch from plastic to paperboard in Egypt?

Decree 662/2025 imposes fees on plastic bags, while a national green-labeling scheme rewards recycled-content packaging, both steering retailers toward recyclable folding cartons.

Which geographic zones host the bulk of folding carton manufacturing in Egypt?

Greater Cairo, Alexandria, and the Nile Delta industrial corridor account for more than 70% of capacity thanks to skilled labor access and proximity to FMCG clients.

How are pulp price swings affecting Egyptian converters?

A reliance on imported virgin pulp exposes converters to global price volatility, compressing margins, though integrated recyclers such as Uniboard partially mitigate the impact.

Page last updated on: