Nordic Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.10 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic Folding Carton Market Analysis by Mordor Intelligence

The Nordic folding carton market size is projected to expand from USD 1.06 billion in 2025 and USD 1.10 billion in 2026 to USD 1.31 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031. Strong policy momentum toward circular packaging, spearheaded by the European Union’s Packaging and Packaging Waste Regulation, is accelerating substitution of legacy plastics with recyclable fiber solutions in food, cosmetics and household goods. Converters capitalize on proximity to Forest Stewardship Council-certified softwood resources, enabling lower-carbon supply chains and compliance with extended producer responsibility fee structures. Digital printing, molded-fiber innovations and government grant programs collectively improve the business case for short-run, premium folding cartons, while pulp price volatility and flexible-package competition temper profit margins. Despite these headwinds, the Nordic folding carton market continues to benefit from e-commerce parcel growth and retailer demand for shelf-ready formats that reduce in-store labor.

Key Report Takeaways

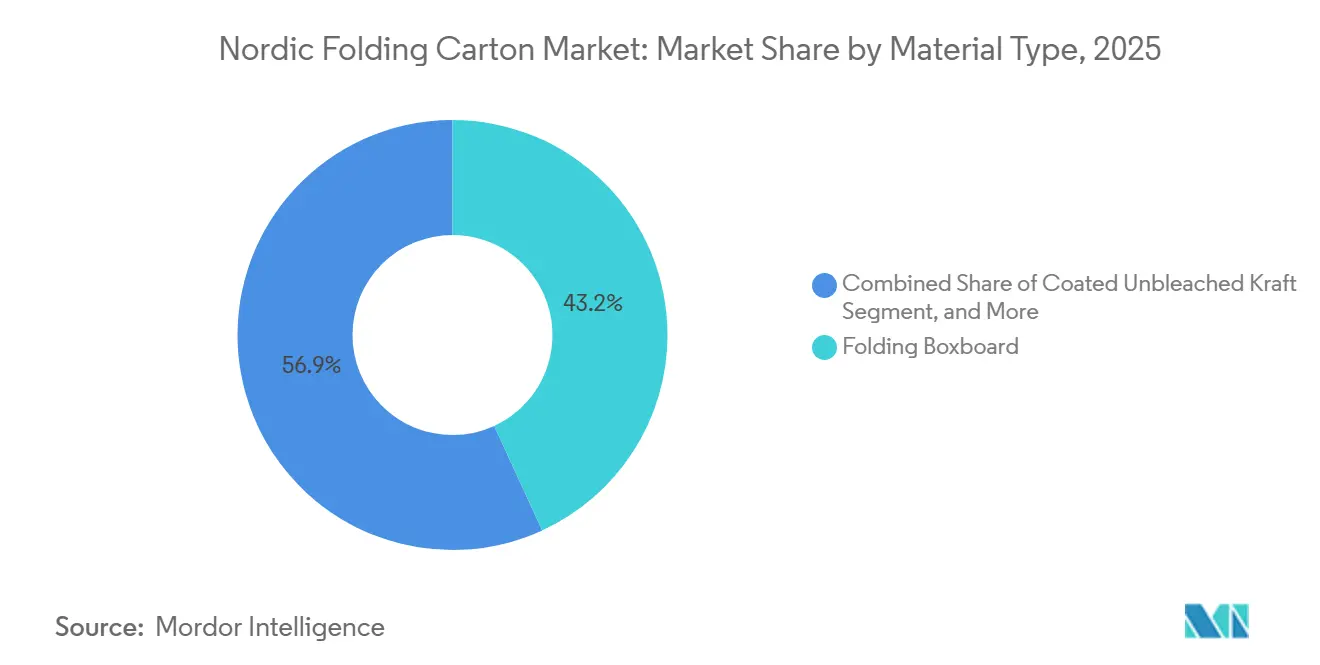

- By material type, folding boxboard captured with 43.15% of the Nordic folding carton market share in 2025.

- By printing technology, the Nordic folding carton market size for digital platforms is projected to grow at a 5.43% CAGR to 2031.

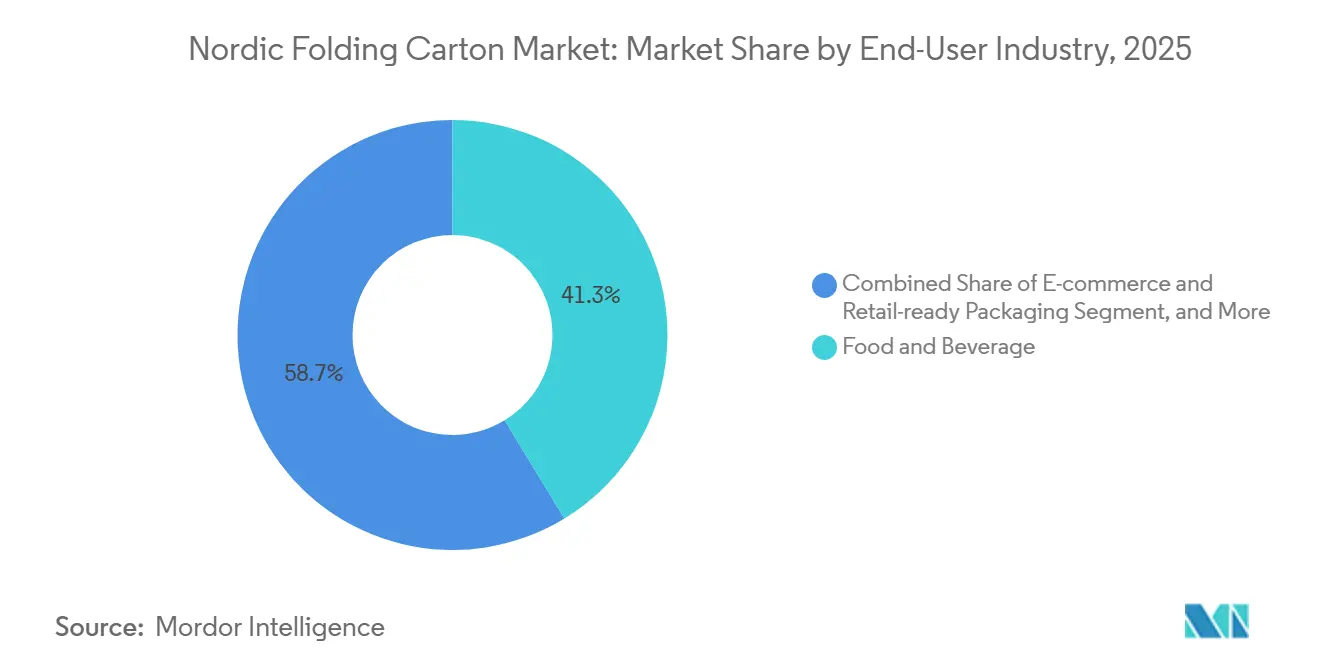

- By end-user industry, the food and beverage industry captured 41.28% of the Nordic folding carton market share in 2025.

- By country, the Nordic folding carton market in Iceland is projected to grow at a 5.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordic Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Packaging Solutions | +1.2% | Global, Nordic leadership | Medium term (2-4 years) |

| Rapid Expansion of E-commerce Fulfillment Networks | +0.9% | Sweden and Norway core, spillover to Denmark and Finland | Short term (≤ 2 years) |

| Technological Advancements in Digital Printing for Short Runs | +0.7% | Sweden and Finland, Denmark pharmaceutical clusters | Medium term (2-4 years) |

| Government Incentives for Fiber-Based Packaging Substitution | +0.5% | Nordic region and wider EU | Long term (≥ 4 years) |

| Rising Premiumization in Food and Beverage Packaging | +0.4% | Sweden and Denmark, Norway seafood | Medium term (2-4 years) |

| Increase in Automated Packaging Lines Across Industries | +0.3% | Sweden and Finland hubs, Norway seafood | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging Solutions

EU rules that all packaging sold after January 2030 be recyclable are accelerating brand-owner migration from multi-material laminates to mono-material folding cartons, particularly in personal care and household goods. Walki recorded a 27% increase in paper-based barrier products in 2025, as dispersion coatings displaced aluminum foil while maintaining oxygen transmission below 1 cc/m²/24 h.[1]Walki, “Business and Strategy | Walki – Advancing Circular Material Solutions,” walki.com Nordic converters enjoy local FSC-certified fiber, cutting supply chain carbon and lowering extended producer responsibility fees. Reuse targets for transport packaging have paradoxically raised demand for collapsible carton formats that replace shrink wrap. Tetra Pak’s pilot plant in Lund is pursuing a 90% fiber-content barrier carton that would qualify for mainstream paper-recycling streams. Yet multilingual labeling rules inflate print-plate costs, nudging converters toward digital presses able to vary data per job.

Rapid Expansion of E-commerce Fulfillment Networks

PostNord logged 12% annual parcel growth in 2025, with Sweden and Norway topping 80% online-purchase penetration. Brands consequently favor shelf-ready folding cartons that double as shipping and display units, trimming warehouse cube and store labor. Moltzau Packaging’s spring 2026 CefaTray system enables on-site forming of fiber trays, reducing inbound packaging volume by 40% and CO₂ emissions associated with return logistics. Iceland’s small but fast-growing e-commerce base further strengthens demand for the Nordic folding carton market by privileging locally printed cartons that meet two-day delivery expectations. Premium direct-to-consumer meal kits and coffee subscriptions willingly pay double-digit premiums for virgin folding boxboard that delivers an elevated unboxing experience.

Technological Advancements in Digital Printing for Short Runs

Digital presses such as the HP Indigo 25K rival offset economics in runs below 10,000 sheets, eliminating plate costs and slashing lead times from 12 weeks to 3 weeks. Pharmaceutical and seasonal confectionery suppliers capitalize on inline serialization and variable graphics impossible with lithographic workflows. Fujifilm’s Jet Press 750S, now deployed at Nordic drug-carton specialists, satisfies the EU Falsified Medicines Directive’s track-and-trace rules while maintaining FDA ink compliance. Substrate upgrades matter: Billerud’s headbox upgrade at Gruvön reduced basis-weight variation to ±2 g/m², improving ink laydown consistency and cutting digital print waste by 15%.

Government Incentives for Fiber-Based Packaging Substitution

EU and national grants de-risk capital outlays for novel fiber substrates. The Circular Bio-based Europe Joint Undertaking earmarked EUR 20 million (USD 21.6 million) for “circular-by-design” projects in 2025. Metsä Board secured EUR 86.5 million (USD 94.2 million) for its 3D Fiber molded-tray project targeting PET replacement in ready meals. The European Investment Bank added a EUR 20 million (USD 21.6 million) loan to PulPac for dry-molded fiber tooling that uses 90% less energy than wet pulp molding. Norway’s ReFiber-Pack initiative and Sweden’s HyPerPack PFAS-free barrier program broaden the pipeline of recyclable, grease-resistant cartons. Although grant disbursement can lag market demand, vertically integrated mills bridge the gap with balance-sheet funding, accelerating commercial rollouts ahead of SMEs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Pulp Prices | -0.6% | Global, acute in Nordic export mills | Short term (≤ 2 years) |

| Competition from Flexible Packaging Formats | -0.4% | Sweden and Denmark snack foods, Finland pet treats | Medium term (2-4 years) |

| Supply-Chain Disruptions for Recycled Fiber Feedstock | -0.3% | Nordic region and broader EU | Medium term (2-4 years) |

| Stricter Food-Contact Compliance Costs for SMEs | -0.2% | Denmark and Sweden are pharma hubs, and Norway is a seafood hub | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Pulp Prices

Nordic softwood bleached kraft pulp averaged USD 1,710 per tonne in early 2025, an 18% year-over-year hike that compressed converter margins. Spot swings between USD 1,580 and USD 1,750 during 2024-2025 left SMEs struggling to renegotiate contracts, with a 10% pulp uptick cascading into 4-5% higher carton costs. To hedge, converters mix recycled content, lock futures, or enter back-to-back supply contracts, yet virgin board remains indispensable for high-brightness pharmaceutical and luxury cosmetics cartons where recycled fiber fails to meet purity or tensile benchmarks.

Competition from Flexible Packaging Formats

Stand-up pouches for snacks and pet treats undercut folding cartons by 30-40% on material costs and offer superior moisture barriers, enticing private-label retailers in Sweden and Denmark. Converters fight back with dispersion-coated mono-material cartons that match oxygen barrier performance while still delivering the tactile shelf appeal clients crave. Speed to market also matters; pouching lines achieve higher fill rates, nudging brand owners to shift SKUs unless converters provide automated forming and sealing solutions like Moltzau’s CefaTray. Without continued innovation in barriers and automation, flexible formats threaten to siphon volume from commodity end-use segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Virgin Grades Sustain Leadership

In 2025, folding boxboard captured a 43.15% share of the Nordic folding carton market, thanks to its balanced cost, printability, and food-contact safety profile. Virgin SBS, with its ISO 92+ brightness and emboss depth, dominates the luxury cosmetics and prescription blister sleeve market, commanding price premiums of up to 30%. Coated unbleached kraft, growing at a 5.12% CAGR, is favored for its natural-brown aesthetic that aligns with eco-branding and its 15-20% lower grammage compared to FBB, helping to cut e-commerce dimensional-weight fees.

White line chipboard is making a comeback in budget cereal and mailer cartons, offering costs of EUR 0.45 (USD 0.49) per m² compared to EUR 0.72 (USD 0.78) for virgin FBB. However, brand owners are considering the optics of recycled-fiber speckles. Stora Enso’s Oulu line, set to ramp up to 750,000 t p.a. of SBS and FBB by 2027, and Metsä Board’s Simpele curtain-coat retrofit highlight a sustained investment in premium virgin board technologies.[2]Stora Enso, “Investor Relations,” storaenso.com Breakthroughs like Walki’s dispersion systems in barrier coatings ensure these substrates remain recyclable under municipal paper streams, mitigating regulatory risks.

By Printing Technology: Digital Accelerates in Versioning-Intensive SKUs

Lithographic offset captured 42.63% of the Nordic folding carton market share in 2025; its sub-USD 0.02 per-sheet economics are unbeatable in runs above 50,000 impressions and in categories with mandated health warnings that require razor-sharp type. Digital printing, expanding at a 5.43% CAGR, capitalizes on agile product lifecycles, enabling brand owners to rotate graphics for influencer collaborations or seasonal collections without excess inventory. Flexography remains entrenched in corrugated display and high-caliper packaging at roughly one-quarter share, valued for water-based inks and rough-surface compatibility. Gravure retreats alongside tobacco demand but retains niches that require an unrivaled tonal range.

Digital presses win on more than speed: HP Indigo’s ElectroInk permits serialized QR codes that unlock augmented-reality experiences, while Fujifilm’s Jet Press 750S supports pharmaceutical track-and-trace with 100% vision inspection. Substrate uniformity upgrades at mills like Billerud’s Gruvön narrow caliper deviation to ±2 %, reducing head-crash and color-shift rejects on B2 digital presses. Despite ink premiums, brand owners absorb added cost to reach market in under a month or to Test-and-Learn micro-batches across Nordic languages, a dynamic likely to embed double-digit digital share by 2031.

By End-User Industry: E-Commerce and Shelf-Ready Formats Drive Outperformance

Food and beverage commanded 41.28% of the Nordic folding carton market demand in 2025, anchored by premium organic dairy and craft spirits that leverage carton storytelling and gift-oriented secondary packs. Healthcare and pharmaceuticals hover at 15-18% share, propelled by aging populations and serialized drug packaging mandates, but price pressure on generics tempers volume growth. E-commerce and retail-ready cartons, however, surge at a 5.68% CAGR, outstripping the broader Nordic folding carton market by over two percentage points. Subscription meal-kit and specialty coffee purveyors insist on unboxing theater, energizing demand for high-resolution folding boxboard with tactile varnishes.

Personal care and cosmetics, with roughly a 13% share, sustain robust margins through limited-edition launches and personalized designs, ideal for digital printing. Electrical appliances and household cleaners use folding cartons for both transit protection and in-aisle instruction panels, benefiting from evolving logistics rules that favor barcode-readable, stackable shapes. Tobacco’s continued decline, partly masked by plain-pack laws that standardize carton size, reallocates lithographic capacity toward adjacent premium food and beverage SKUs.

Geography Analysis

Sweden retained the largest share of 35.48% of Nordic folding carton volume in 2025, due to integrated forestry-to-carton chains and 35 production sites that can supply Stockholm and Gothenburg on a just-in-time basis. Norway follows at roughly one-quarter share, its seafood processors demanding PE-coated solid board that endures icy supply chains while meeting EU compostability targets.[3]Norske Skog ASA, “Company News Q1 2026,” live.euronext.com Denmark’s 18-20% slice is rooted in pharmaceutical and organic dairy production concentrated near Copenhagen.

Finland contributes 15-17% by leveraging Metsä Board’s Simpele and Kyro mills to supply beverage-carton substrates to Tetra Pak and Elopak plants. Iceland remains a small 2-3% but is forecast to clock the region’s fastest CAGR of 5.32% as local fulfillment hubs reduce reliance on mainland European imports. Sweden’s dominance also reflects a strong R&D infrastructure, such as Stora Enso’s RISE-affiliated pilot lines that accelerate the qualification of barrier-coated board.

Norway’s seafood focus requires cartons rated for less than 2 °C cold chain and EN 13432 compostability, niches served by Ranheim’s solid board and Walki’s new flexographic assets in Säkylä. Denmark’s pharmaceutical cluster values ISO 8317 child-resistant cartons and 100-ppm-lead ink thresholds, driving high-margin lithographic work. Finland’s energy-intensive mills shift to biomass and wind power, aligning carbon intensity with EU taxonomy thresholds and safeguarding access to green loans. Iceland’s growth opportunity lies in on-island print capacity that slashes lead times for domestic retailers committed to 48-hour delivery.

Competitive Landscape

The Nordic folding carton market remains moderately concentrated, with the top five players, Stora Enso, Metsä Board, Billerud, Smurfit WestRock, and Mondi, controlling roughly 55-60% of converting capacity, yet product differentiation and captive R&D prevent any single firm from dictating price. Vertical integration is the strategic norm: Stora Enso’s USD 1.13 billion Oulu SBS line and Metsä Board’s USD 68 million Simpele curtain coat reflect sizeable bets on virgin fiber premiumization.

Smaller converters such as Moltzau Packaging and FrontPac win on agility, offering sub-three-week lead times and local fulfillment for SMEs that cannot commit to 200-tonne minimums. Innovation pipelines create defensible moats. Ahlstrom’s Acti-V RRF Natural addresses PFAS bans while maintaining silicone-liner performance, whereas PulPac’s dry-molded fiber offers 90% energy savings and potential in-house forming at brand owner facilities.[4]Ahlstrom, “Press Releases,” news.cision.com/ahlstrom

Automation further widens the gulf. Tetra Pak’s Factory OS pairs real-time print inspection with downstream cartoning to increase overall equipment efficiency by 20%. Market share movements remain incremental due to three- to five-year supply contracts, yet speed-to-market and compliance labs, such as Walki’s Recyclability Lab in Pietarsaari, are emerging differentiators as brand owners scramble to meet the EU’s 2030 recyclability deadline.

Nordic Folding Carton Industry Leaders

Stora Enso Oyj

Metsä Board Corporation

Billerud AB

Mayr-Melnhof Karton AG

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Billerud commissioned a new headbox at its Gruvön mill in Sweden, part of a SEK 1.2 billion (USD 113 million) upgrade that improves basis-weight control and digital-print performance.

- April 2026: Moltzau Packaging launched its patented CefaTray welding machine, enabling on-site forming of fiber trays that cut transport volume by 40 %.

- March 2026: Stora Enso reported the successful start-up of its EUR 1 billion (USD 1.13 billion) Oulu consumer board line, targeting 750,000 t p.a. capacity by 2027.

- February 2026: Ahlstrom introduced Acti-V RRF Natural recyclable release liner using recycled fibers and PFAS-free chemistry.

Nordic Folding Carton Market Report Scope

The Nordic Folding Carton Market refers to the industry that produces, distributes, and uses folding cartons across the Nordic region. Folding cartons are a type of packaging made from paperboard, designed to be folded into various shapes to package goods efficiently and attractively. The study focuses on analyzing the market dynamics, including key drivers, restraints, and opportunities influencing the Nordic Folding Carton Market. The study also examines the competitive landscape, supply chain trends, and technological advancements shaping the market during the forecast period.

The Nordic Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries), and Country (Denmark, Finland, Norway, Sweden, Iceland, Rest of Nordics). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| Denmark |

| Finland |

| Norway |

| Sweden |

| Iceland |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Country | Denmark |

| Finland | |

| Norway | |

| Sweden | |

| Iceland |

Key Questions Answered in the Report

What is the current Nordic folding carton market size and projected growth?

The Nordic folding carton market size reached USD 1.10 billion in 2026 and is forecast to hit USD 1.31 billion by 2031, growing at a 3.56% CAGR.

Which material type leads to Nordic folding carton demand?

Folding boxboard led with 43.15 % share in 2025, favored for its food-contact safety and print quality.

Why is digital printing gaining share in Nordic folding cartons?

Digital presses cut lead times, enable personalization and comply with serialization rules, propelling a 5.43 % CAGR to 2031.

Which end-use segment is expanding fastest?

E-commerce and retail-ready packaging is advancing at a 5.68 % CAGR through 2031 because parcel growth demands shelf-ready, branded cartons.

How are pulp price swings affecting Nordic converters?

Pulp volatility, with 2025 softwood prices at USD 1,710 per tonne, compresses margins and pushes converters toward long-term fiber contracts and recycled blends.

What regulations most influence future carton design?

The EU Packaging and Packaging Waste Regulation mandates all packaging be recyclable by 2030, steering brands to mono-material folding cartons and barrier-coated fiber solutions.

Page last updated on: