Vietnam Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

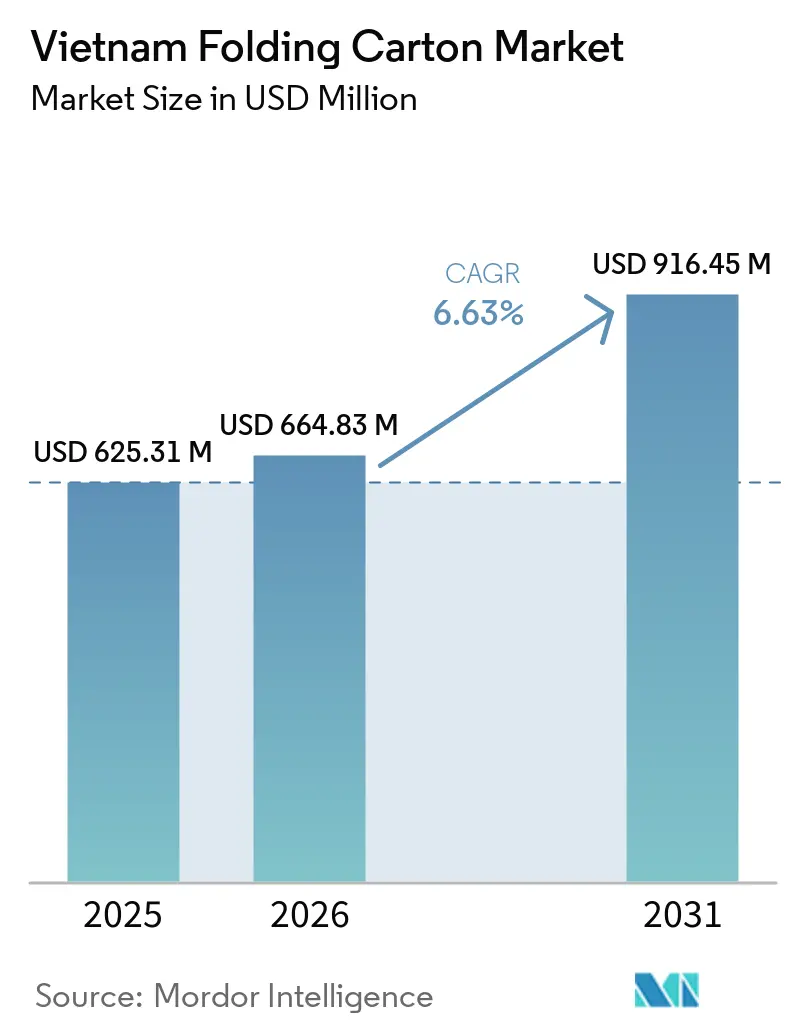

| Base Year Market Size (2025) | USD 625.31 Million |

| Market Size (2026) | USD 664.83 Million |

| Market Size (2031) | USD 916.45 Million |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Folding Carton Market Analysis by Mordor Intelligence

The Vietnam folding carton market size was valued at USD 625.31 million in 2025 and is estimated to grow from USD 664.83 million in 2026 to reach USD 916.45 million by 2031, at a CAGR of 6.63% during 2026-2031. Unfolding demand from modern trade, widening e-commerce logistics networks, and the government’s Extended Producer Responsibility mandates are accelerating the shift toward lighter-weight, recycled-content substrates. Foreign direct investment in containerboard capacity is shortening lead times for brand owners, while port congestion and pulp price volatility are forcing converters to rethink inventory strategies. Integrated multinationals are leveraging backward integration for fiber security, whereas domestic firms are countering with agile regional distribution and faster artwork-to-print cycles. As the Vietnam folding carton market matures, converters that align capital spending with sustainability standards and digital workflow automation are positioned to outperform.

Key Report Takeaways

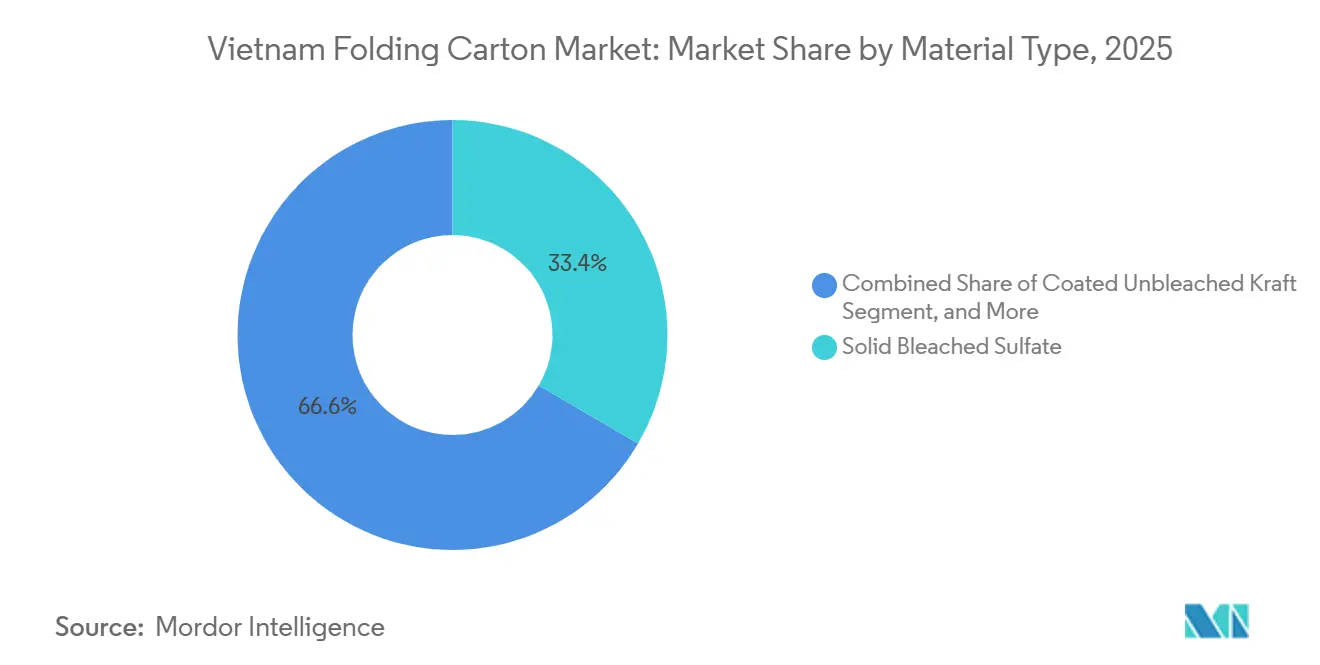

- By material type, solid bleached sulfate captured with 33.42% of the Vietnam folding carton market share in 2025.

- By printing technology, the Vietnam folding carton market size for digital printing is projected to grow at a 8.92% CAGR to 2031.

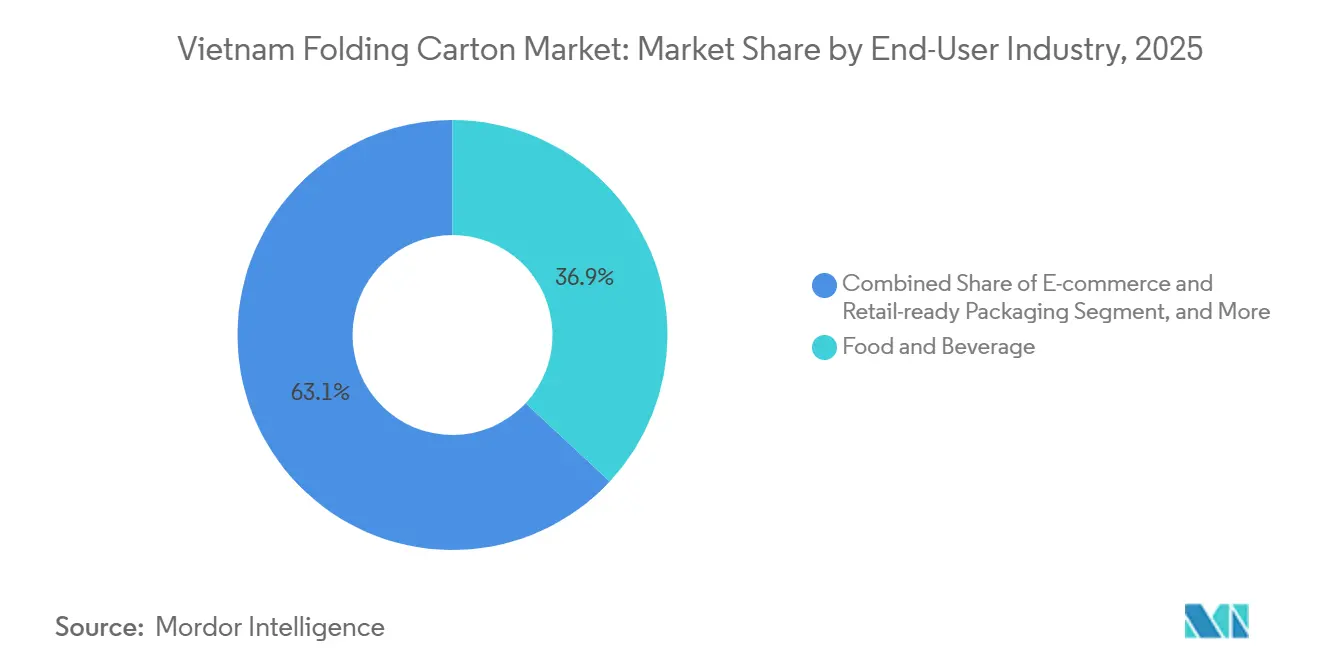

- By end-user industry, the food and beverage industry captured 36.93% of the Vietnam folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from the E-Commerce Sector | +1.8% | National, Hanoi, and Ho Chi Minh City hubs | Medium term (2-4 years) |

| Government Push for Sustainable Packaging | +1.5% | National, driven by Decree 110/2026 and Decree 05/2025 | Short term (≤ 2 years) |

| Growth in Food and Beverage Exports | +1.2% | National, export hubs in Binh Duong and Dong Nai | Long term (≥ 4 years) |

| Rising Disposable Income and Urbanization | +1.0% | National, strongest in urban centers | Long term (≥ 4 years) |

| Rise of High-Color Digital Short Runs for SMEs | +0.7% | National, early adopters in Hanoi and Da Nang | Medium term (2-4 years) |

| Premium Carton Demand From Domestic Craft Beer Brands | +0.5% | Urban markets, mainly Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from the E-Commerce Sector

Vietnam’s online retail channel consumed 332,000 tons of packaging materials in 2023, of which folding cartons supplied roughly 40% by volume. The channel now accounts for 12% of retail goods sales, having climbed 4% points in just 3 years. Merchants increasingly prefer shelf-ready formats that cut fulfillment labor by up to 20%, a dynamic that is funneling steady orders toward converters able to combine tamper-evident engineering with striking graphics. Cross-border platforms such as Lazada and Shopee embed FSC certification into seller eligibility, instantly redefining baseline specifications for every carton shipped through their networks. The Vietnam folding carton market, therefore, benefits twice: in higher absolute volumes and in the migration to premium substrates that command superior margins.

Government Push for Sustainable Packaging

Decree 110/2026 obliges producers to finance post-consumer collection and recycling, setting a 30% paper recovery target by 2028, while Decree 05/2025 restricts single-use plastics in urban food service.[1]Ministry of Natural Resources and Environment, “Decree 110/2026 Implementation Guidelines,” vietnamnews.vn Together, the regulations are channeling quick-service restaurants, electronics assemblers, and household-goods makers toward recycled-fiber carton solutions. Penalties for non-compliance range from VND 50 million (USD 2,100) to VND 100 million (USD 4,200), spurring brand owners to specify Folding Boxboard and Coated Unbleached Kraft with at least 50% recycled content. Converters that invested early in de-inking and waste-paper aggregation lines, or that formed alliances with Producer Responsibility Organizations, now enjoy a distinct licensing edge in the Vietnamese folding carton market.

Growth in Food and Beverage Exports

First-quarter 2026 food and beverage exports reached USD 16.69 billion, buoyed by dairy, confectionery, and processed seafood shipments that rely on aseptic or modified-atmosphere cartons. Craft brewers are using metallic-ink litho cartons to differentiate on retail shelves, lifting premium-carton usage by close to double digits. Tetra Pak’s capacity expansion to 30 billion packs annually positions Vietnam as a supply base for ASEAN dairy exporters, reinforcing long-run demand for high-barrier Solid Bleached Sulfate structures.[2]Tetra Pak, “Binh Duong Capacity Expansion Press Release,” tetrapak.com As export certifications under ISO 22000 and HACCP become table stakes, converters with in-house quality laboratories are widening their lead.

Rising Disposable Income and Urbanization

Household spending is projected to hit VND 3.952 quadrillion (USD 152 billion) in 2026, supported by a working-age population of 67 million and 2.5-3.0% annual urbanization. Retail sales grew 10.6% in the third quarter of 2025, outpacing the Vietnam folding carton market’s 6.63% CAGR and flagging potential supply gaps during holiday peaks. Consumers are willing to pay 15-20% premiums for embossed or soft-touch packaging in cosmetics and confectionery, prompting converters to invest in offline foil stamping, tactile coatings, and digital embellishment. Premiumization directly feeds higher-value tonnage into the Vietnam folding carton market rather than mere volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Prices | -0.9% | National, tied to global pulp spot markets | Short term (≤ 2 years) |

| Intensifying Competition From Flexible Packaging | -0.7% | National, especially in food and beverage lines | Medium term (2-4 years) |

| Logistics Bottlenecks at Key Port Facilities | -0.5% | Ho Chi Minh City and Hai Phong port clusters | Short term (≤ 2 years) |

| Limited Advanced Paper Recycling Capacity | -0.4% | National dependence on imported recovered fiber | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Prices

January 2026 quotations moved European Bleached Eucalyptus Kraft to USD 1,220-1,250 per ton and Northern Bleached Softwood Kraft to USD 1,600, trimming converter margins by as much as 300 basis points under contracts that cap pass-through clauses. With 70% of virgin pulp imported, exchange-rate swings and geopolitical freight surcharges add USD 80-120 to every ton landed. Only 18% of converters use forward contracts, leaving most exposed to quarterly resets that can jump 10-15%. The squeeze is most acute for Solid Bleached Sulfate grades, where brightness consistency bars substitution, weighing on earnings across the Vietnam folding carton market.

Intensifying Competition from Flexible Packaging

Stand-up pouches, flow-wrapped films, and laminated sachets have siphoned share in snack foods, coffee, and personal-care refills, trimming carton penetration from roughly two-thirds to just over one-half of volumes in five years. Flexible formats weigh 30-40% less and lower freight cost by up to USD 0.08 per unit, an advantage amplified by brand carbon-footprint disclosures. Craft brewers are shifting multipacks from glass to aluminum cans, further denting carton demand. Folding-carton converters now differentiate on structural design, tactile finishes, and recyclability claims, but margin pressure from film converters remains a central restraint on the Vietnam folding-carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Solid Bleached Sulfate Anchors Premium Tiers

Solid Bleached Sulfate captured 33.42% of the Vietnam folding carton market share in 2025, firmly anchoring premium applications in cosmetics, pharmaceuticals, and high-end confectionery. Brand owners select the grade for brightness levels above 88 GE and print surfaces that enable photographic lithography, reinforcing its grip on price-sensitive but graphics-intensive categories. Folding Boxboard is expected to post an 8.75% CAGR, the fastest rate among substrates, as quick-service restaurants and e-commerce fulfillment centers adopt weights in the 250-300 gsm range to curb freight surcharges. Coated Unbleached Kraft is strengthening its foothold in electronics and household-goods shippers because Decree 110/2026 rewards recycled-content compliance, while White Line Chipboard supplies cost-conscious dry-food fillers.

Tetra Pak’s expansion to 30 billion packs annually highlights the centrality of barrier-coated Solid Bleached Sulfate to aseptic dairy and juice lines, a niche that shields profits even amid pulp inflation. As recycled-content thresholds climb, converters are blending virgin and secondary fiber to safeguard tensile integrity without breaching cost targets. Inline basis-weight scanners, near-infrared moisture controls, and high-consistency refiners help large mills deliver tighter grammage tolerances, a precondition for multinationals that link payout terms to statistical process control metrics. Smaller converters unable to finance such upgrades risk relegation to low-margin commodity cartons. The Vietnam folding carton market size advantage therefore gravitates toward operators that couple substrate versatility with capital-intensive quality systems.

By Printing Technology: Digital Commands the Growth Spotlight

Lithographic workflows accounted for 41.26% of the printed volume in 2025 and remain the baseline for runs of 50,000 units or more, where six-color plus spot varnish campaigns dominate. Digital printing, on the other hand, is forecast to grow at an 8.92% CAGR through 2031, outpacing all other processes as SMEs push SKUs with lifecycles measured in weeks, not seasons. Variable data enables batch-level traceability for cosmetics and nutraceuticals, while eliminating the plate-cutting setup cost to nearly zero for sub-500-unit orders. Flexographic units maintain relevance in outer corrugated wraps and beverage carriers, where two-color jobs prevail, and gravure cylinders continue to serve ultra-high-volume cigarette cartons, but both lose share to digital in lifestyle brands.

The Vietnam folding carton market size allocated to digital presses is expanding as HP Indigo, Canon varioPRINT, and Xerox iGen installations move beyond Hanoi and Ho Chi Minh City into Da Nang, Hai Phong, and Can Tho. Inline spectrophotometers push Delta E variation below 1.5, satisfying luxury-brand tolerances, while cloud-linked MIS systems slash order-to-ship lead times by a fifth. Each efficiency step compounds demand for short-run elasticity, encouraging converters to layer Web-to-print storefronts onto their ERP stack. As digital sheets approach offset-comparable unit economics at 2,000-3,000 units, their addressable market swells into mainstream promotion cycles, boosting overall revenue density inside the Vietnam folding carton market.

By End-User Industry: E-Commerce Redefines Volume Mix

Food and beverage users accounted for 36.93% of folding cartons in 2025, driven by dairy, seafood, and confectionery exports, underpinned by stringent shelf-life and traceability rules. However, e-commerce and retail-ready packaging are on track for a 9.16% CAGR through 2031, the fastest among all sectors, as online sales penetration jumps and sellers refine the “unboxing” theatre. Healthcare and pharmaceuticals maintain steady volumes, yet serialization, tamper-evidence, and track-and-trace raise complexity, favoring converters with GAMP-compliant data capture. Personal care and cosmetics carve out premiums with soft-touch and foil-stamped finishes, while electrical and electronic products rely on anti-static and moisture-barrier materials that meet IEC 61340-5-1.

The Vietnam folding carton market size earmarked for e-commerce enjoys a virtuous cycle: FSC-certified mandates by marketplaces up the recycled-fiber quotient, ISO 14001 procurement rules shrink vendor pools, and brand marketers invest in high-color corrugated inserts that complement folding cartons in hybrid “box-in-box” shipments. These requirements shift the competitive bar from pure cost to holistic compliance and graphics excellence. Tobacco cartons retreat amid declining smoking prevalence, but converters backfill the gap with craft-beer multipacks and pet-food liners that exploit similar substrate gauges.

Geography Analysis

Vietnam’s two industrial corridors anchor the country’s folding-carton demand. The southern cluster centered on Ho Chi Minh City, Binh Duong, and Dong Nai accounts for roughly 58% of shipped volume, buoyed by export-oriented food processors and electronics assemblers. Port congestion at Cat Lai, operating at 115-120% of design capacity, has prolonged dwell times to three days and tacked USD 150-200 onto each twenty-foot equivalent unit, creating working-capital strain for converters that must hold extra safety stock. Nevertheless, the zone’s integrated containerboard mills afford logistics advantages that safeguard service-level agreements for multinational brand owners. The Vietnam folding carton market, therefore, continues to deploy most new litho and digital capacity within a 100-kilometer radius of Bien Hoa and Thu Duc.

In the north, the Hanoi-Hai Phong axis is capturing incremental share as infrastructure upgrades on the Hai Phong-Ha Long expressway shave 1/3 off transit time to deep-sea ports. Foreign direct investment in Bac Ninh electronics hubs catalyzes demand for ESD-compliant cartons, while specialty food exporters in Thai Binh specify grease-proof coatings for frozen seafood. The government’s Logistics Master Plan earmarks Dong Anh and Long Bien districts for bonded warehousing to ease container backlogs at Hai Phong, thereby indirectly improving reliability for local converters.[3]Hai Phong Port Authority, “Annual Throughput Statistics 2025,” vinamarine.gov.vn The Vietnam folding carton market responds by establishing satellite converting plants that combine digital presses with auto-platen die-cutters, enabling next-day delivery across the Red River Delta.

Secondary demand pockets span the central coast and emerging Mekong Delta cities. Da Nang’s tourism revival fuels premium confectionery gifting, prompting mid-size converters to set up storefronts that bundle design, pre-press, and digital print under one roof. Meanwhile, Can Tho’s aquaculture processors are trialing coated folding cartons that replace polystyrene foam boxes, fulfilling the Decree 05/2025 plastic restrictions. Though volumes remain smaller than the core north-south corridors, growth rates hover in the high single digits, making these regions attractive for asset-light digital print deployments. Taken together, geographic diversification safeguards supply resilience for the Vietnam folding carton market against localized port or labor disruptions.

Competitive Landscape

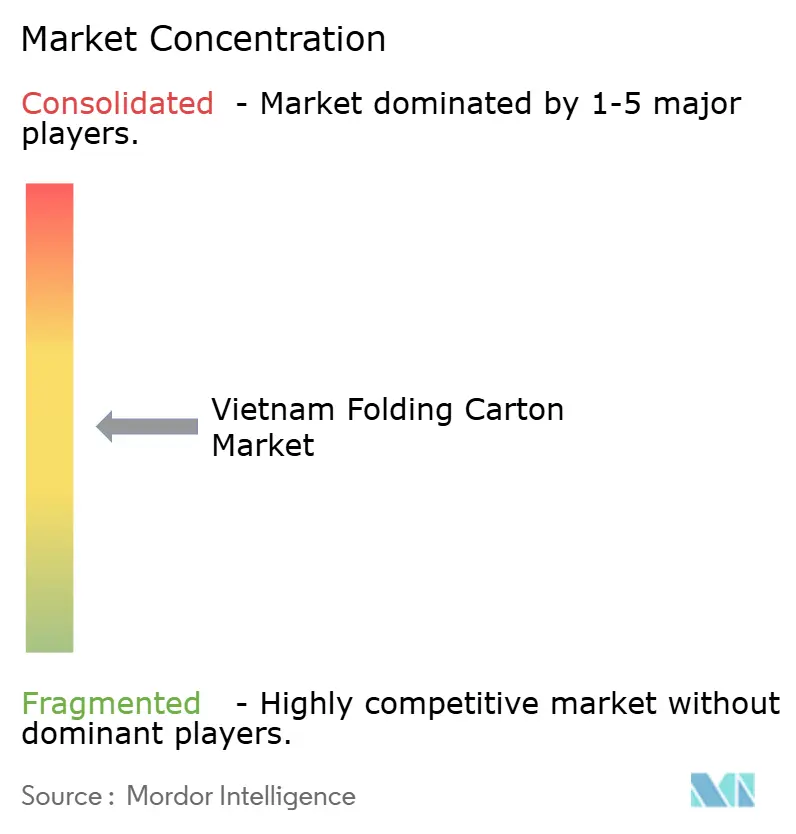

The Vietnam folding carton market shows moderate fragmentation: the top five suppliers command roughly 47% of the market share, leaving more than half the pie to regional independents and family-owned converters. Japanese-owned Oji, Rengo, and Lee and Man run integrated pulp-to-carton chains that blunt volatility in virgin fiber prices, a decisive edge when global Kraft prices spike. Oji’s USD 104 million liquid-carton facility, scheduled for Dong Nai by 2028, augments that moat by offering aseptic technology under one roof, while Rengo’s Bien Hoa acquisition adds local brand relationships within the fast-moving consumer goods universe.[4]Oji Holdings, “Dong Nai Liquid Carton Plant Announcement,” oji-fs.co.jp Tetra Pak, though specialized, embeds proprietary filling technology, locking partners into multi-year carton supply contracts.

Domestic players compete by leveraging proximity and adaptability. Dong Tien and Thuan An maintain satellite plants within commuting distance of brand-owner breweries and confectioners, allowing artwork changes within 48 hours, compared with the one-week cycle at centralized, foreign-owned hubs. AnBinh Printing Carton Packaging uses HP Indigo digital presses to produce artisanal food and craft-beer labels, with no more than 5,000 units per SKU. These pockets of agility are widening, fragmenting print-run economics and nudging large incumbents to roll out their own digital islands.

Technology differentiation is widening the capability gap. AI-enabled color control slashes waste by up to 5% and delivers Delta E consistency below 1.5, a metric increasingly codified in multinational purchase orders. Tetra Pak’s USD 67.5 million pilot plant for aluminum-free paper-based barriers signals an industry tilt toward mono-material recyclability that could ripple through substrate recipes well beyond aseptic beverage lines. Converters aiming to remain in qualified supplier pools are earmarking capex for substrate analytics, passed-through carbon accounting, and blockchain-enabled track-and-trace. Against that backdrop, sustained profitability inside the Vietnam folding carton market rests on marrying cost discipline with innovation spending, a balance easier for cash-rich multinationals than for under-capitalized independents.

Vietnam Folding Carton Industry Leaders

Dong Tien Packaging and Paper Co. Ltd.

Oji Interpack Vietnam Co., Ltd.

Rengo Co. Ltd.

Tetra Pak Vietnam JSC

Song Lam Packaging JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ANDRITZ secured a contract to supply two tissue production lines to Koro Viet Nam, with start-up slated for 2027, broadening the domestic base for hygiene grades that feed secondary carton demand.

- March 2026: Xuan Mai Paper commissioned a 75-ton-per-day de-inking pulp line, easing reliance on imported recovered fiber and supporting Decree 110/2026 recycled-content thresholds.

- January 2026: Tetra Pak inaugurated a EUR 60 million (USD 67.5 million) Binh Duong pilot plant aimed at replacing aluminum foil in aseptic cartons with paper-based barriers.

- November 2025: Oji Holdings announced a USD 104 million investment for a liquid-carton plant in Dong Nai Province, targeting commercial operations in 2028.

Vietnam Folding Carton Market Report Scope

The folding carton market in Vietnam refers to the industry that produces, distributes, and uses folding cartons, paper-based packaging solutions widely used across industries such as food and beverage, personal care, healthcare, and others. The study analyzes market trends, growth drivers, challenges, and opportunities in the Vietnam folding carton market. It also examines the competitive landscape, supply chain dynamics, and key developments influencing the market during the forecast period.

The Vietnam Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Vietnam folding carton market, and what is the forecast growth?

The Vietnam folding carton market size was valued at USD 625.31 million in 2025 and is estimated to grow from USD 664.83 million in 2026 to reach USD 916.45 million by 2031.

Which material type leads demand inside Vietnam’s carton sector?

Solid Bleached Sulfate led with a 33.42% share in 2025, primarily due to its superior printability and barrier properties.

How fast is digital printing growing relative to lithography?

Digital printing is expected to post an 8.92% CAGR through 2031, outpacing lithography and gaining ground in short-run, high-color jobs.

What regulatory measures are reshaping carton specifications?

Decree 110/2026 imposes Extended Producer Responsibility financing for collection and recycling, while Decree 05/2025 restricts single-use plastics, collectively steering brands toward recycled-content folding cartons.

Which end-user industry is expanding the quickest?

E-commerce and retail-ready packaging is forecast to rise at a 9.16% CAGR through 2031, more than any other end-use segment in the Vietnam folding carton market.

How fragmented is the competitive landscape?

The top five suppliers collectively command roughly 47% share, indicating moderate fragmentation with strong opportunities for agile regional converters.

Page last updated on: